Key Insights

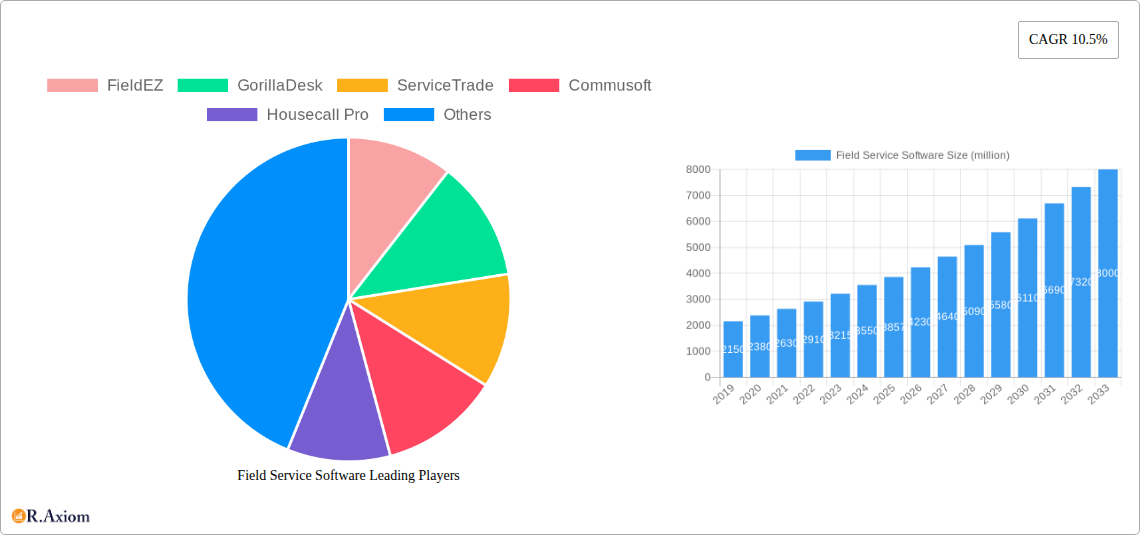

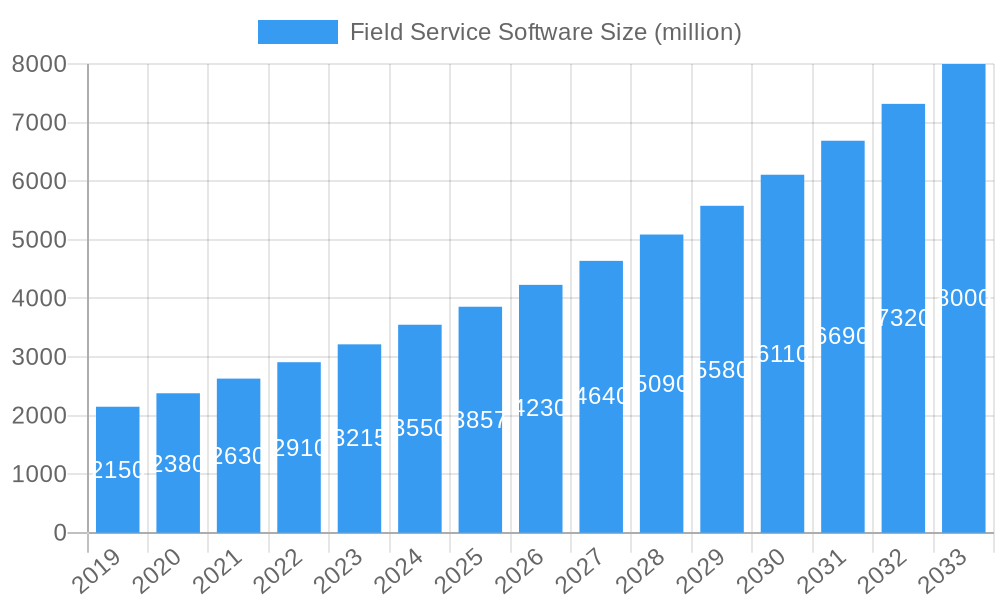

The global Field Service Software market is poised for significant expansion, projected to reach an estimated market size of approximately USD 3,857 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 10.5%. This impressive growth trajectory is propelled by a confluence of factors, primarily the increasing need for operational efficiency and streamlined workflows within service-oriented businesses. The adoption of cloud-based solutions is a dominant trend, offering scalability, accessibility, and cost-effectiveness, particularly for Small and Medium-sized Enterprises (SMEs) seeking to optimize their field operations. Large enterprises are also investing heavily, driven by the demand for sophisticated features like real-time tracking, automated scheduling, and enhanced customer communication. Key drivers include the digitalization initiatives across industries, the growing complexity of service delivery models, and the imperative for improved customer satisfaction through faster response times and more accurate service delivery. The market’s expansion is further fueled by advancements in mobile technology, enabling field technicians to access critical information and update job status on the go, thereby enhancing productivity and reducing administrative overhead.

Field Service Software Market Size (In Billion)

The competitive landscape features a dynamic array of players, from established giants to agile innovators, all vying for market share. Companies like ServiceTitan, FieldEdge, and WorkWave Service are at the forefront, offering comprehensive suites of solutions catering to diverse service verticals. The market's growth is further supported by the increasing integration of IoT devices and artificial intelligence, which are set to revolutionize predictive maintenance and proactive service delivery. While the market is experiencing substantial growth, potential restraints such as the initial cost of implementation, data security concerns, and the need for skilled personnel to manage these advanced systems, need to be carefully addressed by solution providers. Nevertheless, the overarching trend towards digital transformation and the undeniable benefits of field service software in boosting productivity, improving customer service, and driving revenue growth position this market for sustained and substantial expansion throughout the forecast period.

Field Service Software Company Market Share

Field Service Software Market Concentration & Innovation

The global Field Service Software market exhibits moderate concentration, with a few dominant players like ServiceTitan, FieldEdge, and Housecall Pro commanding significant market share, estimated at over 40% collectively in 2025. However, a dynamic ecosystem of innovative companies, including GorillaDesk, ServiceTrade, Commusoft, and Tradify, contributes to intense competition and continuous technological advancement. Innovation drivers are primarily fueled by the increasing demand for operational efficiency, enhanced customer experience, and real-time data insights. Regulatory frameworks, particularly those related to data privacy (e.g., GDPR, CCPA) and industry-specific compliance, are shaping software development and implementation strategies, requiring robust security features and audit trails. Product substitutes, such as manual scheduling, spreadsheets, and generic CRM solutions, are gradually being phased out as businesses recognize the specialized benefits of dedicated field service management tools. End-user trends point towards a growing preference for mobile-first solutions, AI-powered automation for scheduling and dispatch, and integrated customer communication platforms. Mergers and acquisitions (M&A) are a notable feature, with an estimated M&A deal value exceeding $500 million in the historical period (2019-2024), indicating consolidation and strategic expansion by larger entities to acquire niche technologies or customer bases. Companies like Jobber and ServiceTitan have been active in this space, acquiring smaller players to broaden their service offerings and market reach.

Field Service Software Industry Trends & Insights

The Field Service Software market is poised for substantial growth, driven by a confluence of technological advancements, evolving business needs, and a persistent demand for operational excellence across various industries. The compound annual growth rate (CAGR) is projected to be robust, estimated at 12.5% for the forecast period (2025-2033). This expansion is underpinned by several key market growth drivers. The increasing adoption of cloud-based solutions continues to be a dominant trend, offering scalability, accessibility, and reduced IT overhead for businesses of all sizes, from SMEs to large enterprises. Technological disruptions, particularly in the realm of Artificial Intelligence (AI) and Machine Learning (ML), are revolutionizing field service operations. AI is being leveraged for predictive maintenance, intelligent scheduling and dispatch optimization, automated customer communication, and even route planning, leading to significant improvements in efficiency and cost reduction. The integration of the Internet of Things (IoT) devices in equipment allows for real-time monitoring and proactive service, further enhancing the value proposition of field service software. Consumer preferences are increasingly dictating the pace of innovation. Customers now expect seamless communication, real-time updates on technician arrival, and convenient payment options, all of which are facilitated by sophisticated field service management platforms. The demand for mobile accessibility is paramount, with field technicians requiring intuitive and robust mobile applications to manage their daily tasks, access job details, capture data, and communicate with the back office. Competitive dynamics are intense, with established players like ServiceTitan, FieldEdge, and Housecall Pro constantly innovating to maintain their market leadership, while agile newcomers like FieldEZ, GorillaDesk, and ServiceTrade are carving out niches with specialized features or pricing models. The market penetration of field service software is still evolving, with significant opportunities for growth in emerging economies and in sectors that have historically lagged in digital transformation. The focus is shifting from basic scheduling to comprehensive workflow automation, customer relationship management, and advanced analytics, empowering businesses to gain deeper insights into their operations and customer behavior. The integration of Augmented Reality (AR) for remote assistance and training is also an emerging trend that promises to enhance the capabilities of field service professionals. The emphasis on data security and compliance with evolving regulations is also a critical factor shaping product development and market strategies.

Dominant Markets & Segments in Field Service Software

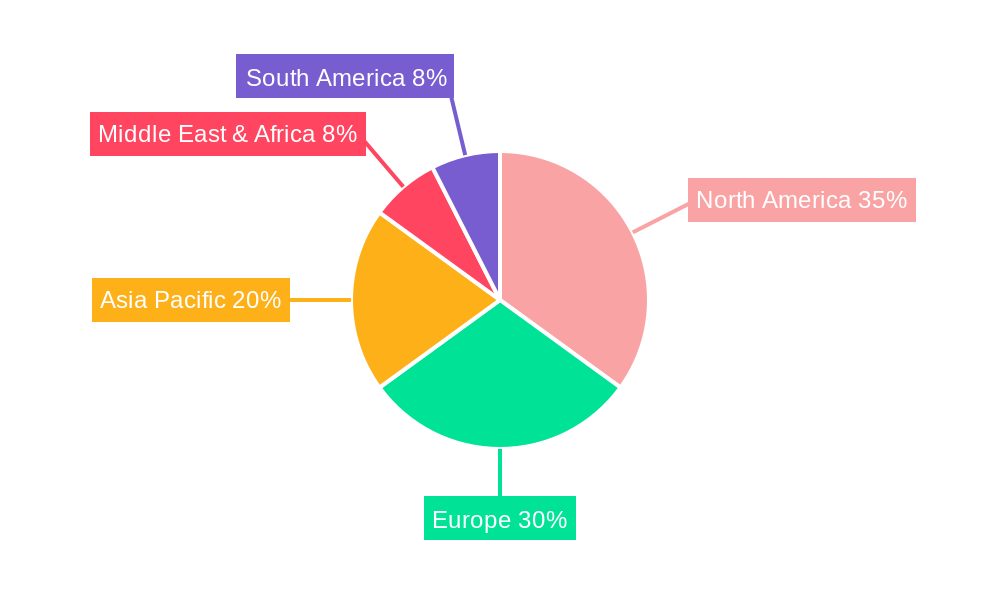

The global Field Service Software market is witnessing a significant surge in adoption, with particular strength emanating from North America, estimated to account for over 45% of the global market share in 2025. Within this region, the United States leads due to its mature service-based economy, high adoption of technology, and robust presence of key industry players. Economic policies that encourage business investment and innovation, coupled with extensive digital infrastructure, further bolster the dominance of this market.

Application Segments:

SMEs (Small and Medium-sized Enterprises): This segment represents a rapidly expanding area for field service software.

- Key Drivers:

- Cost-Effectiveness: Cloud-based solutions offer scalable and affordable options for SMEs that may lack large IT budgets.

- Operational Efficiency: SMEs are increasingly reliant on optimizing their limited resources, making field service software essential for streamlining scheduling, dispatch, and invoicing.

- Competitive Pressure: To compete with larger businesses, SMEs need to offer professional and efficient service delivery, which field service software enables.

- Ease of Use: Many solutions are designed with intuitive interfaces that are easy for smaller teams to adopt and manage.

- Dominance Analysis: The demand from SMEs is fueled by a desire to professionalize operations, improve customer satisfaction, and gain a competitive edge without incurring substantial capital expenditure. Companies like Housecall Pro and Jobber have a strong focus on this segment.

- Key Drivers:

Large Enterprises: This segment, while mature, continues to drive significant revenue and innovation.

- Key Drivers:

- Complexity Management: Large enterprises manage vast fleets of technicians and complex service schedules, requiring sophisticated dispatching, route optimization, and workforce management capabilities.

- Integration Needs: These businesses often require deep integration with existing enterprise resource planning (ERP), customer relationship management (CRM), and accounting systems.

- Data Analytics and Reporting: The ability to generate comprehensive reports and gain deep insights into operational performance, technician productivity, and customer trends is crucial for large organizations.

- Scalability and Customization: Field service software for large enterprises needs to be highly scalable and offer extensive customization options to meet specific operational requirements.

- Dominance Analysis: Leading players like ServiceTitan and FieldEdge excel in serving large enterprises by offering feature-rich platforms capable of handling complex workflows and high volumes of service calls. Their ability to integrate with other business systems and provide advanced analytics is a key differentiator.

- Key Drivers:

Type Segments:

Cloud-based Field Service Software: This segment is experiencing exponential growth and is expected to dominate the market.

- Key Drivers:

- Accessibility and Flexibility: Cloud solutions allow for anytime, anywhere access to critical information for both office staff and field technicians.

- Lower Upfront Costs: Subscription-based models make these solutions more accessible to businesses of all sizes.

- Automatic Updates and Maintenance: Cloud providers handle software updates and maintenance, reducing the burden on IT departments.

- Enhanced Collaboration: Facilitates seamless communication and data sharing between the office and the field.

- Dominance Analysis: The inherent advantages of cloud technology, including rapid deployment, scalability, and cost-effectiveness, make it the preferred choice for most businesses. This trend is expected to continue, further solidifying the dominance of cloud-based field service software.

- Key Drivers:

On-premise Field Service Software: This segment is experiencing a decline in market share but still holds relevance for specific use cases.

- Key Drivers:

- Data Security and Control: Some organizations, particularly those in highly regulated industries, prefer on-premise solutions for greater control over their data.

- Existing Infrastructure: Businesses with significant investments in on-premise IT infrastructure may opt for these solutions to leverage their existing assets.

- Customization Needs: In rare cases, highly specialized customization requirements might favor an on-premise deployment.

- Dominance Analysis: While on-premise solutions are becoming less prevalent, they will continue to cater to a niche market that prioritizes absolute data sovereignty and has unique integration or security mandates. However, their overall market share is expected to shrink in favor of cloud offerings.

- Key Drivers:

Field Service Software Product Developments

Recent product developments in the field service software market are largely characterized by an emphasis on enhanced automation, AI-driven insights, and improved user experience. Innovations such as AI-powered scheduling and dispatching algorithms are optimizing technician routes and job assignments, leading to significant time and cost savings. The integration of IoT capabilities allows for predictive maintenance, enabling companies to proactively address equipment issues before they lead to costly downtime. Mobile applications are becoming increasingly sophisticated, offering offline capabilities, real-time GPS tracking, and seamless digital invoicing and payment processing. Furthermore, advanced customer portals are providing end-users with greater transparency and control over their service appointments. These developments are driven by the need for greater operational efficiency, enhanced customer satisfaction, and a competitive edge in a rapidly evolving market.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the global Field Service Software market, segmented by Application into SMEs and Large Enterprises, and by Type into Cloud and On-premise solutions. The SME segment, projected to grow at a CAGR of approximately 13.0% from 2025 to 2033, is driven by increasing adoption of affordable and scalable cloud solutions by smaller businesses seeking to professionalize their operations. The Large Enterprises segment, with an estimated market size of over $3,000 million in 2025, continues to demand advanced features for complex workflow management and integration capabilities, with a projected CAGR of around 11.5%. The Cloud segment is the dominant force, expected to capture over 85% of the market by 2033, benefiting from its flexibility, scalability, and lower total cost of ownership. The On-premise segment, while facing a decline, will continue to serve niche markets prioritizing data control, with a projected market share of approximately 15% by 2033 and a CAGR of around 4.0%.

Key Drivers of Field Service Software Growth

The growth of the Field Service Software market is propelled by several interconnected factors. Technologically, the widespread adoption of mobile devices and the increasing sophistication of cloud computing have made advanced field service management accessible and affordable. The integration of Artificial Intelligence (AI) and Machine Learning (ML) for optimized scheduling, route planning, and predictive maintenance is a significant catalyst. Economically, the pursuit of operational efficiency and cost reduction across industries is driving demand for software that can streamline service delivery and enhance technician productivity. Regulatory factors, such as evolving data privacy laws and industry-specific compliance requirements, are also pushing businesses towards robust and secure software solutions.

Challenges in the Field Service Software Sector

Despite robust growth, the Field Service Software sector faces several challenges. One significant barrier is the initial cost and complexity of implementation for some advanced platforms, particularly for smaller businesses with limited IT resources. Resistance to change from field technicians accustomed to traditional methods can hinder adoption. Data security concerns and the need to comply with an ever-evolving landscape of data privacy regulations present ongoing hurdles. Furthermore, intense competition can lead to pricing pressures, impacting profit margins for some vendors. Supply chain disruptions, impacting hardware availability for IoT integrations, could also pose a temporary challenge.

Emerging Opportunities in Field Service Software

Emerging opportunities in the Field Service Software market are abundant, driven by ongoing technological advancements and evolving customer expectations. The increasing integration of the Internet of Things (IoT) allows for real-time equipment monitoring and predictive maintenance, creating new revenue streams and service offerings. The application of Artificial Intelligence (AI) in areas like autonomous dispatch and customer service chatbots offers further avenues for innovation and efficiency gains. The growing demand for personalized customer experiences presents an opportunity for software that facilitates seamless communication and transparent service delivery. Furthermore, the expansion into emerging markets and the development of specialized solutions for niche industries, such as renewable energy or specialized healthcare services, represent significant untapped potential.

Leading Players in the Field Service Software Market

- ServiceTitan

- FieldEdge

- Housecall Pro

- GorillaDesk

- ServiceTrade

- Commusoft

- P3

- Tradify

- RazorSync

- Vonigo

- Jobber

- Fergus

- Praxedo

- ServiceBox

- Service Fusion

- Synchroteam

- mHelpDesk

- WorkWave Service

- Mobiwork MWS

- ThermoGRID

- ServSuite

Key Developments in Field Service Software Industry

- 2023: Integration of advanced AI-powered route optimization features becoming standard in leading platforms.

- 2023: Increased focus on mobile-first design and offline capabilities to enhance field technician productivity.

- 2024: Rise of IoT integration for predictive maintenance becoming a key differentiator for enterprise solutions.

- 2024: Enhanced customer portal functionalities offering real-time appointment tracking and communication.

- 2024: Market consolidation through strategic acquisitions of smaller, innovative field service software providers.

- 2025: Widespread adoption of automated invoicing and digital payment processing integrated within core platforms.

- 2025: Emergence of augmented reality (AR) for remote assistance and technician training in select advanced solutions.

Strategic Outlook for Field Service Software Market

The strategic outlook for the Field Service Software market remains exceptionally positive, driven by the undeniable value it brings in terms of operational efficiency, cost reduction, and enhanced customer satisfaction. The continued evolution and integration of AI, IoT, and mobile technologies will be crucial for vendors to maintain a competitive edge. Businesses of all sizes will continue to invest in these solutions to streamline their service operations and adapt to the increasing demands for real-time responsiveness and transparency. The expansion into new geographic markets and the development of specialized solutions for emerging industries represent significant growth catalysts, ensuring a dynamic and expanding market landscape for the foreseeable future.

Field Service Software Segmentation

-

1. Application

- 1.1. SMEs

- 1.2. Large Enterprises

-

2. Type

- 2.1. Cloud

- 2.2. On-premise

Field Service Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Field Service Software Regional Market Share

Geographic Coverage of Field Service Software

Field Service Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Field Service Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. SMEs

- 5.1.2. Large Enterprises

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Field Service Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. SMEs

- 6.1.2. Large Enterprises

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud

- 6.2.2. On-premise

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Field Service Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. SMEs

- 7.1.2. Large Enterprises

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud

- 7.2.2. On-premise

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Field Service Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. SMEs

- 8.1.2. Large Enterprises

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud

- 8.2.2. On-premise

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Field Service Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. SMEs

- 9.1.2. Large Enterprises

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud

- 9.2.2. On-premise

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Field Service Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. SMEs

- 10.1.2. Large Enterprises

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud

- 10.2.2. On-premise

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 FieldEZ

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 GorillaDesk

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ServiceTrade

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Commusoft

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Housecall Pro

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 P3

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Tradify

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 RazorSync

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Vonigo

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Jobber

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Fergus

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Praxedo

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 ServiceBox

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Service Fusion

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Synchroteam

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 mHelpDesk

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 WorkWave Service

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 FieldEdge

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 ServiceTitan

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Mobiwork MWS

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 ThermoGRID

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 ServSuite

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.1 FieldEZ

List of Figures

- Figure 1: Global Field Service Software Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Field Service Software Revenue (million), by Application 2025 & 2033

- Figure 3: North America Field Service Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Field Service Software Revenue (million), by Type 2025 & 2033

- Figure 5: North America Field Service Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Field Service Software Revenue (million), by Country 2025 & 2033

- Figure 7: North America Field Service Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Field Service Software Revenue (million), by Application 2025 & 2033

- Figure 9: South America Field Service Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Field Service Software Revenue (million), by Type 2025 & 2033

- Figure 11: South America Field Service Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Field Service Software Revenue (million), by Country 2025 & 2033

- Figure 13: South America Field Service Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Field Service Software Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Field Service Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Field Service Software Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Field Service Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Field Service Software Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Field Service Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Field Service Software Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Field Service Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Field Service Software Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Field Service Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Field Service Software Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Field Service Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Field Service Software Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Field Service Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Field Service Software Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Field Service Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Field Service Software Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Field Service Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Field Service Software Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Field Service Software Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Field Service Software Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Field Service Software Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Field Service Software Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Field Service Software Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Field Service Software Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Field Service Software Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Field Service Software Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Field Service Software Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Field Service Software Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Field Service Software Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Field Service Software Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Field Service Software Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Field Service Software Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Field Service Software Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Field Service Software Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Field Service Software Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Field Service Software Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Field Service Software?

The projected CAGR is approximately 10.5%.

2. Which companies are prominent players in the Field Service Software?

Key companies in the market include FieldEZ, GorillaDesk, ServiceTrade, Commusoft, Housecall Pro, P3, Tradify, RazorSync, Vonigo, Jobber, Fergus, Praxedo, ServiceBox, Service Fusion, Synchroteam, mHelpDesk, WorkWave Service, FieldEdge, ServiceTitan, Mobiwork MWS, ThermoGRID, ServSuite.

3. What are the main segments of the Field Service Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 3857 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Field Service Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Field Service Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Field Service Software?

To stay informed about further developments, trends, and reports in the Field Service Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence