Key Insights

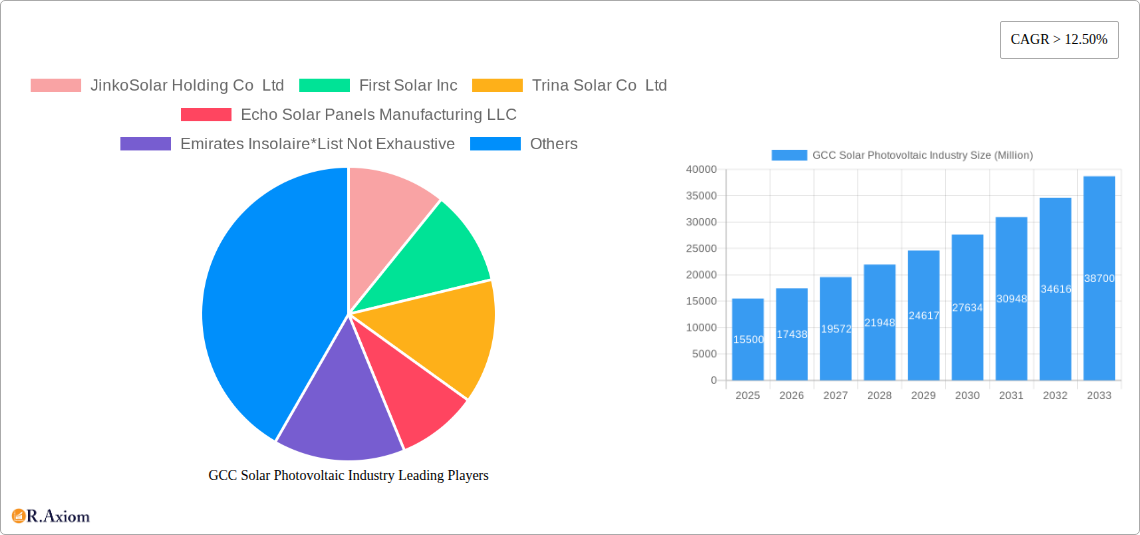

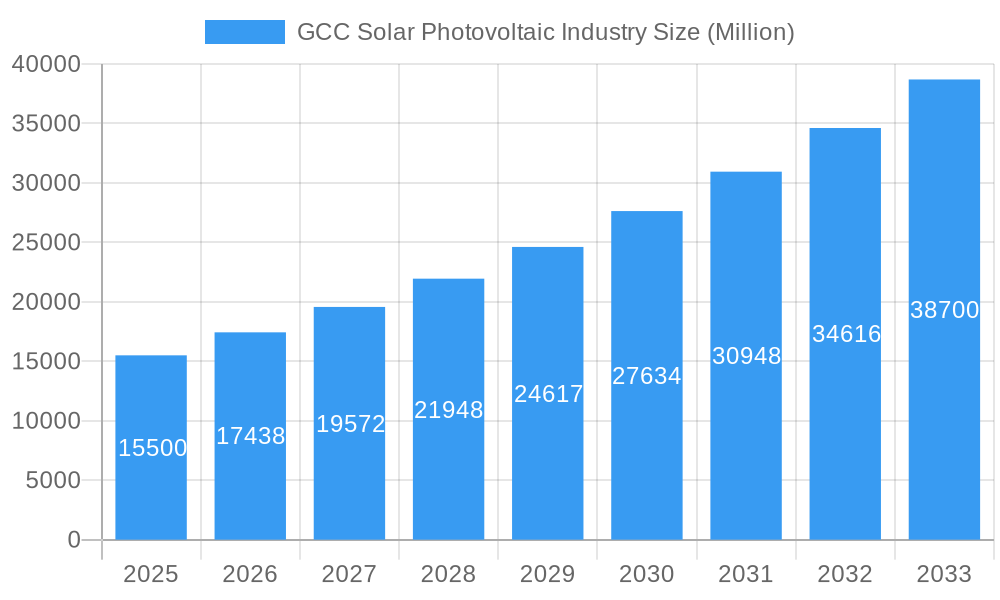

The GCC Solar Photovoltaic (PV) industry is poised for exceptional growth, with a current market size projected to exceed USD 15,000 million and a robust Compound Annual Growth Rate (CAGR) of over 12.50%. This surge is primarily driven by the region's ambitious renewable energy targets, substantial government investments in clean energy infrastructure, and the decreasing cost of solar technology. Key drivers include the urgent need to diversify economies away from fossil fuels, enhance energy security, and meet rapidly increasing electricity demand. Governments are actively promoting solar adoption through supportive policies, incentives, and large-scale utility projects, fostering a favorable investment climate. The ongoing development of mega-projects, coupled with a growing awareness of environmental sustainability, further accelerates market expansion.

GCC Solar Photovoltaic Industry Market Size (In Billion)

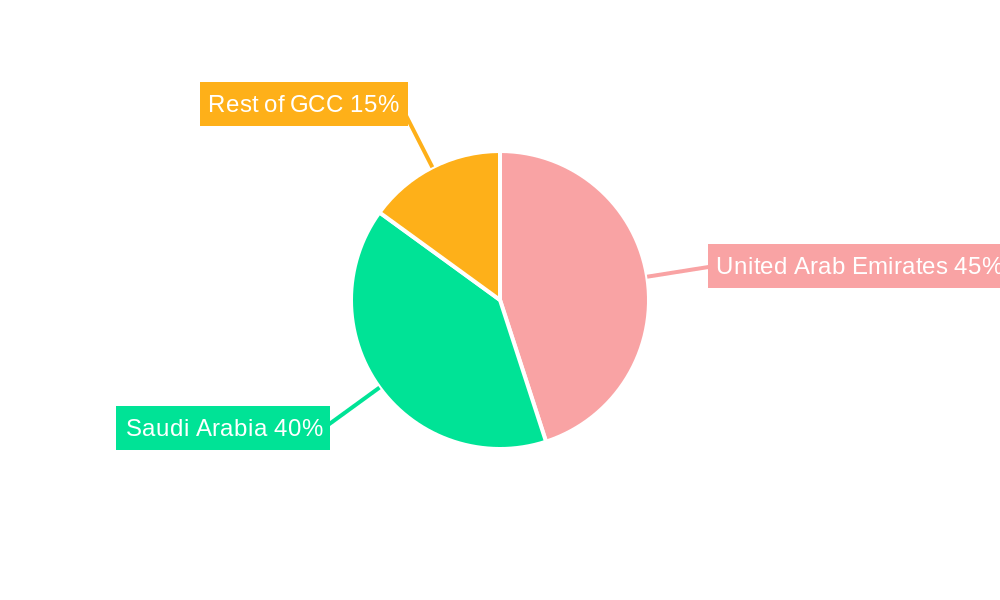

The market is strategically segmented across deployment types, with the Utility sector leading the charge, followed by Commercial and Industrial (C&I) and Residential applications. The United Arab Emirates and Saudi Arabia are the dominant geographical markets, spearheading the region's solar PV revolution, with the Rest of the GCC countries showing significant potential for growth. Key players like JinkoSolar, First Solar, Trina Solar, and local entities such as Echo Solar Panels Manufacturing LLC and Emirates Insolaire are actively shaping the market landscape through innovation and capacity expansion. Emerging trends include the integration of battery storage solutions with solar PV systems to address intermittency, advancements in bifacial solar panel technology for enhanced efficiency, and the increasing adoption of smart grid technologies to optimize solar energy integration. While the market exhibits immense promise, challenges such as grid integration complexities, land acquisition for large-scale projects, and the availability of skilled labor need to be strategically addressed to ensure sustained and efficient growth.

GCC Solar Photovoltaic Industry Company Market Share

GCC Solar Photovoltaic Industry Market Concentration & Innovation

The GCC solar photovoltaic (PV) industry is characterized by a moderate level of market concentration, with key global players alongside emerging regional manufacturers vying for dominance. Companies like JinkoSolar Holding Co. Ltd, First Solar Inc., and Trina Solar Co. Ltd command significant market share due to their established manufacturing capabilities and extensive global supply chains. Regionally, entities such as Echo Solar Panels Manufacturing LLC and Emirates Insolaire are increasingly contributing to the local production landscape. Innovation is a critical driver, fueled by the pursuit of higher efficiency modules, advanced bifacial solar technologies, and integrated energy storage solutions. Regulatory frameworks are continuously evolving to support renewable energy adoption, including feed-in tariffs, net metering policies, and ambitious national targets for solar power integration. Product substitutes, such as concentrated solar power (CSP) and other renewable energy sources, present competition, but the falling cost and improving efficiency of PV make it a strong contender. End-user trends are shifting towards distributed generation and smart grid integration, with a growing interest in rooftop solar for residential and commercial sectors. Mergers and acquisitions (M&A) activities, though less prevalent than in mature markets, are expected to increase as larger players seek to expand their regional footprint and smaller companies consolidate to achieve economies of scale. The investment in M&A deals is projected to grow significantly in the coming years as strategic partnerships and acquisitions become more common.

GCC Solar Photovoltaic Industry Industry Trends & Insights

The GCC solar photovoltaic industry is poised for substantial growth, driven by a confluence of factors including aggressive renewable energy targets, declining technology costs, and a growing imperative for energy diversification. The market is expected to witness a robust Compound Annual Growth Rate (CAGR) of approximately 15-20% during the forecast period of 2025–2033. This expansion is underpinned by significant government initiatives aimed at reducing reliance on fossil fuels and bolstering the clean energy sector. Technological disruptions are continuously reshaping the industry, with advancements in solar panel efficiency, such as the increasing adoption of PERC (Passivated Emitter and Rear Cell) and TOPCon (Tunnel Oxide Passivated Contact) technologies, leading to higher energy yields from smaller footprints. Bifacial solar panels, which capture sunlight from both sides, are gaining traction, offering enhanced energy generation. The integration of artificial intelligence (AI) and machine learning in solar farm management and predictive maintenance is also improving operational efficiency and reliability. Consumer preferences are evolving, with a growing demand for sustainable energy solutions from both residential and industrial sectors. This is evident in the rising adoption of rooftop solar installations and power purchase agreements (PPAs) for commercial and industrial (C&I) projects. The competitive dynamics within the GCC solar PV market are intensifying, with both established international manufacturers and increasingly capable local players competing on price, quality, and service. Market penetration for solar PV is still relatively nascent in some segments, presenting significant opportunities for further expansion. The increasing awareness of climate change and the economic benefits of renewable energy are further fueling this positive market outlook. Strategic investments in large-scale solar projects, coupled with supportive policies, are creating a fertile ground for sustained growth and innovation within the GCC solar PV landscape.

Dominant Markets & Segments in GCC Solar Photovoltaic Industry

The United Arab Emirates (UAE) and Saudi Arabia are the undisputed dominant markets within the GCC solar photovoltaic industry, driven by their ambitious renewable energy mandates and substantial investments in large-scale solar projects.

- United Arab Emirates: The UAE has consistently led the region in solar PV deployment.

- Key Drivers:

- National Renewable Energy Targets: The UAE's vision to achieve a significant percentage of its energy mix from clean sources by 2050 necessitates massive solar installations.

- Government Support and Incentives: Policies such as net metering, tax exemptions, and competitive tendering processes for renewable energy projects have accelerated adoption.

- World-Class Infrastructure: The development of robust grid infrastructure capable of integrating large volumes of solar power is a critical enabler.

- Leading Utilities: Dubai Electricity and Water Authority (DEWA) has been a frontrunner in developing and managing utility-scale solar parks, such as the Mohammed bin Rashid Al Maktoum Solar Park.

- Key Drivers:

- Saudi Arabia: Saudi Arabia is rapidly emerging as a major player, with massive pipeline projects and a strong commitment to its Vision 2030.

- Key Drivers:

- Vision 2030 Goals: The nation's economic diversification plan places a strong emphasis on renewable energy, including solar PV, to reduce oil dependency.

- Strategic Investments: Significant investments from entities like ACWA Power are driving the development of utility-scale projects, exemplified by the Sakaka PV IPP.

- Favorable Resource Potential: Abundant solar irradiation across the country makes solar PV a highly viable and cost-effective energy source.

- Industrial Development: Initiatives like the planned thin-film industrial park by Hanergy Thin Film Power Group signal a move towards local manufacturing and job creation.

- Key Drivers:

Dominant Deployment Segments:

- Utility-Scale Deployment: This segment currently dominates the GCC solar PV market, characterized by the development of mega solar power plants (e.g., hundreds of megawatts to gigawatts). These projects are crucial for meeting national energy demands and achieving renewable energy targets. The investment in utility-scale projects often involves international developers and financiers, attracted by the competitive tariffs and government backing.

- Commercial and Industrial (C&I) Deployment: This segment is experiencing significant growth, driven by businesses seeking to reduce operational costs through lower electricity bills and enhance their corporate social responsibility (CSR) profiles by adopting clean energy. Policies encouraging self-consumption and the installation of rooftop solar on commercial buildings are gaining momentum.

- Residential Deployment: While still a smaller segment compared to utility-scale, residential solar PV is on an upward trajectory. Falling system costs, attractive financing options, and increasing environmental awareness among homeowners are contributing to its expansion. Government incentives and simplified interconnection processes are crucial for fostering this segment's growth.

The "Rest of GCC" (comprising Kuwait, Oman, Qatar, and Bahrain) is also actively pursuing solar PV development, albeit at a different pace and scale. These countries are implementing their own renewable energy targets and are gradually increasing their solar PV capacity, often looking to the successes of the UAE and Saudi Arabia as blueprints for their strategies.

GCC Solar Photovoltaic Industry Product Developments

Product development in the GCC solar photovoltaic industry is increasingly focused on enhancing efficiency and durability to withstand the region's harsh climatic conditions. Innovations include advanced multi-busbar (MBB) solar cells, which improve current collection and reduce resistance, leading to higher power output. The widespread adoption of bifacial solar panels, capable of generating electricity from both sides, is a significant trend, offering up to 20% increased energy yield. Anti-reflective coatings and self-cleaning surfaces are being integrated to maximize light absorption and minimize performance degradation due to dust and sand. Furthermore, the development of robust mounting structures and advanced inverters designed for desert environments is crucial. These product advancements aim to deliver higher lifetime energy yields, lower levelized cost of energy (LCOE), and improved reliability, making solar PV an even more competitive and attractive energy solution in the GCC.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the GCC solar photovoltaic industry, encompassing key segments across deployment and geography. The market is segmented by deployment types: Utility, Commercial and Industrial (C&I), and Residential. The Utility segment focuses on large-scale solar power plants developed by governments and independent power producers, contributing significantly to the region's energy mix. The C&I segment examines solar installations on commercial and industrial facilities, driven by cost savings and sustainability goals. The Residential segment explores rooftop solar solutions for homes, indicating growing consumer adoption. Geographically, the report analyzes the market within the United Arab Emirates and Saudi Arabia, recognizing their leadership roles, as well as the "Rest of GCC" comprising Oman, Kuwait, Qatar, and Bahrain. Growth projections and market sizes are provided for each segment, alongside an assessment of the competitive dynamics and key growth drivers influencing their development throughout the study period of 2019–2033.

Key Drivers of GCC Solar Photovoltaic Industry Growth

Several key factors are propelling the growth of the GCC solar photovoltaic industry.

- Ambitious Renewable Energy Targets: Nations across the GCC have set aggressive goals to increase the share of renewable energy in their power generation mix, directly driving demand for solar PV.

- Declining Technology Costs: The continuous reduction in the cost of solar panels and balance-of-system components makes solar PV increasingly economically competitive with conventional energy sources.

- Government Support and Policies: Favorable regulatory frameworks, including feed-in tariffs, net metering policies, and attractive tendering processes, are creating an enabling environment for solar investment.

- Energy Diversification Imperative: The strategic need to diversify energy sources away from oil and gas, driven by economic and environmental considerations, is a significant catalyst.

- Technological Advancements: Improvements in solar panel efficiency, bifacial technology, and energy storage solutions enhance the performance and reliability of solar installations.

Challenges in the GCC Solar Photovoltaic Industry Sector

Despite its promising growth, the GCC solar photovoltaic industry faces several challenges.

- Intermittency and Storage: The inherent intermittency of solar power necessitates significant investment in energy storage solutions to ensure a stable and reliable power supply, which can increase project costs.

- Grid Integration and Infrastructure: Integrating large-scale solar power into existing grid infrastructure requires substantial upgrades and smart grid technologies, which can be complex and costly.

- Harsh Environmental Conditions: High temperatures, dust, and humidity in the GCC region can impact the performance and longevity of solar panels, requiring specialized, more expensive equipment and increased maintenance.

- Supply Chain Vulnerabilities: Reliance on imported solar panels and components can expose the industry to global supply chain disruptions and price volatility.

- Regulatory Uncertainty: While frameworks are improving, any shifts in government policies or incentives can create uncertainty for investors and developers.

Emerging Opportunities in GCC Solar Photovoltaic Industry

The GCC solar photovoltaic industry is ripe with emerging opportunities. The increasing focus on green hydrogen production, powered by solar energy, presents a significant new market. The expansion of smart cities and sustainable development initiatives across the region will drive demand for distributed solar generation and integrated renewable energy solutions. Advancements in floating solar technology offer potential for deployment on reservoirs and water bodies, conserving land resources. Furthermore, the growth of electric vehicle (EV) charging infrastructure, powered by solar, creates synergistic opportunities. The development of regional manufacturing capabilities for solar components presents a chance to reduce import dependency and create local employment.

Leading Players in the GCC Solar Photovoltaic Industry Market

- JinkoSolar Holding Co Ltd

- First Solar Inc

- Trina Solar Co Ltd

- Echo Solar Panels Manufacturing LLC

- Emirates Insolaire

- Sunergy Solar

- Canadian Solar Inc

- Dubai Electricity and Water Authority

- Masdar Abu Dhabi Future Energy Company

- ACWA Power

Key Developments in GCC Solar Photovoltaic Industry Industry

- April 2021: ACWA Power inaugurated the 300 MW Sakaka PV IPP, the country's first utility-scale renewable energy project, at an investment cost of SAR 1.2 billion. The project was awarded to ACWA Power at a record-breaking tariff of USD 2.3417 cents/kWh (8.781 halalas/kWh). This development set a new benchmark for cost-competitiveness in utility-scale solar in Saudi Arabia and the wider GCC.

- Early 2020: Hanergy Thin Film Power Group announced its plan to build a thin-film industrial park in Saudi Arabia, at an estimated cost of USD 1 billion (EUR 870 million). Upon completion, this project is set to be the first of its kind in the Middle East, signifying a push towards local manufacturing and advanced solar technology development within the region.

Strategic Outlook for GCC Solar Photovoltaic Industry Market

The strategic outlook for the GCC solar photovoltaic industry remains exceptionally strong, driven by unwavering government commitment to energy transition and economic diversification. The continuous decline in solar PV costs, coupled with advancements in efficiency and storage technologies, will further enhance its competitiveness. Increased focus on utility-scale projects, alongside the burgeoning C&I and residential segments, will fuel market expansion. Strategic partnerships and potential M&A activities among leading players are anticipated, leading to market consolidation and enhanced capabilities. The region's abundant solar resources, coupled with supportive regulatory environments, position it as a prime destination for significant solar PV investment and innovation in the coming decade.

GCC Solar Photovoltaic Industry Segmentation

-

1. Deployment

- 1.1. Utility

- 1.2. Commercial and Industrial

- 1.3. Residential

-

2. Geography

- 2.1. United Arab Emirates

- 2.2. Saudi Arabia

- 2.3. Rest of GCC

GCC Solar Photovoltaic Industry Segmentation By Geography

- 1. United Arab Emirates

- 2. Saudi Arabia

- 3. Rest of GCC

GCC Solar Photovoltaic Industry Regional Market Share

Geographic Coverage of GCC Solar Photovoltaic Industry

GCC Solar Photovoltaic Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Utility

- 5.1.2. Commercial and Industrial

- 5.1.3. Residential

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United Arab Emirates

- 5.2.2. Saudi Arabia

- 5.2.3. Rest of GCC

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Rest of GCC

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Global GCC Solar Photovoltaic Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Utility

- 6.1.2. Commercial and Industrial

- 6.1.3. Residential

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United Arab Emirates

- 6.2.2. Saudi Arabia

- 6.2.3. Rest of GCC

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. United Arab Emirates GCC Solar Photovoltaic Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. Utility

- 7.1.2. Commercial and Industrial

- 7.1.3. Residential

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United Arab Emirates

- 7.2.2. Saudi Arabia

- 7.2.3. Rest of GCC

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Saudi Arabia GCC Solar Photovoltaic Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. Utility

- 8.1.2. Commercial and Industrial

- 8.1.3. Residential

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United Arab Emirates

- 8.2.2. Saudi Arabia

- 8.2.3. Rest of GCC

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Rest of GCC GCC Solar Photovoltaic Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. Utility

- 9.1.2. Commercial and Industrial

- 9.1.3. Residential

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. United Arab Emirates

- 9.2.2. Saudi Arabia

- 9.2.3. Rest of GCC

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 JinkoSolar Holding Co Ltd

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 First Solar Inc

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Trina Solar Co Ltd

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Echo Solar Panels Manufacturing LLC

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Emirates Insolaire*List Not Exhaustive

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Sunergy Solar

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Canadian Solar Inc

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Dubai Electricity and Water Authority

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Masdar Abu Dhabi Future Energy Company

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 ACWA Power

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.1 JinkoSolar Holding Co Ltd

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global GCC Solar Photovoltaic Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: United Arab Emirates GCC Solar Photovoltaic Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 3: United Arab Emirates GCC Solar Photovoltaic Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 4: United Arab Emirates GCC Solar Photovoltaic Industry Revenue (billion), by Geography 2025 & 2033

- Figure 5: United Arab Emirates GCC Solar Photovoltaic Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 6: United Arab Emirates GCC Solar Photovoltaic Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: United Arab Emirates GCC Solar Photovoltaic Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Saudi Arabia GCC Solar Photovoltaic Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 9: Saudi Arabia GCC Solar Photovoltaic Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 10: Saudi Arabia GCC Solar Photovoltaic Industry Revenue (billion), by Geography 2025 & 2033

- Figure 11: Saudi Arabia GCC Solar Photovoltaic Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 12: Saudi Arabia GCC Solar Photovoltaic Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Saudi Arabia GCC Solar Photovoltaic Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Rest of GCC GCC Solar Photovoltaic Industry Revenue (billion), by Deployment 2025 & 2033

- Figure 15: Rest of GCC GCC Solar Photovoltaic Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 16: Rest of GCC GCC Solar Photovoltaic Industry Revenue (billion), by Geography 2025 & 2033

- Figure 17: Rest of GCC GCC Solar Photovoltaic Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 18: Rest of GCC GCC Solar Photovoltaic Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Rest of GCC GCC Solar Photovoltaic Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 2: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 3: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 5: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 8: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 9: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 11: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Global GCC Solar Photovoltaic Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the GCC Solar Photovoltaic Industry?

The projected CAGR is approximately 10.8%.

2. Which companies are prominent players in the GCC Solar Photovoltaic Industry?

Key companies in the market include JinkoSolar Holding Co Ltd, First Solar Inc, Trina Solar Co Ltd, Echo Solar Panels Manufacturing LLC, Emirates Insolaire*List Not Exhaustive, Sunergy Solar, Canadian Solar Inc, Dubai Electricity and Water Authority, Masdar Abu Dhabi Future Energy Company, ACWA Power.

3. What are the main segments of the GCC Solar Photovoltaic Industry?

The market segments include Deployment, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 368.7 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Solar Energy Demand4.; Declining Cost of Solar PV Systems.

6. What are the notable trends driving market growth?

Utility Sector as a Significant Sector.

7. Are there any restraints impacting market growth?

4.; Strong Dependence on Prevailing Weather Condition.

8. Can you provide examples of recent developments in the market?

In April 2021, ACWA Power inaugurated the 300 MW Sakaka PV IPP, the country's first utility-scale renewable energy project, at an investment cost of SAR 1.2 billion. The project was awarded to ACWA Power at a record-breaking tariff of USD 2.3417 cents/kWh (8.781 halalas/kWh).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "GCC Solar Photovoltaic Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the GCC Solar Photovoltaic Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the GCC Solar Photovoltaic Industry?

To stay informed about further developments, trends, and reports in the GCC Solar Photovoltaic Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence