Key Insights

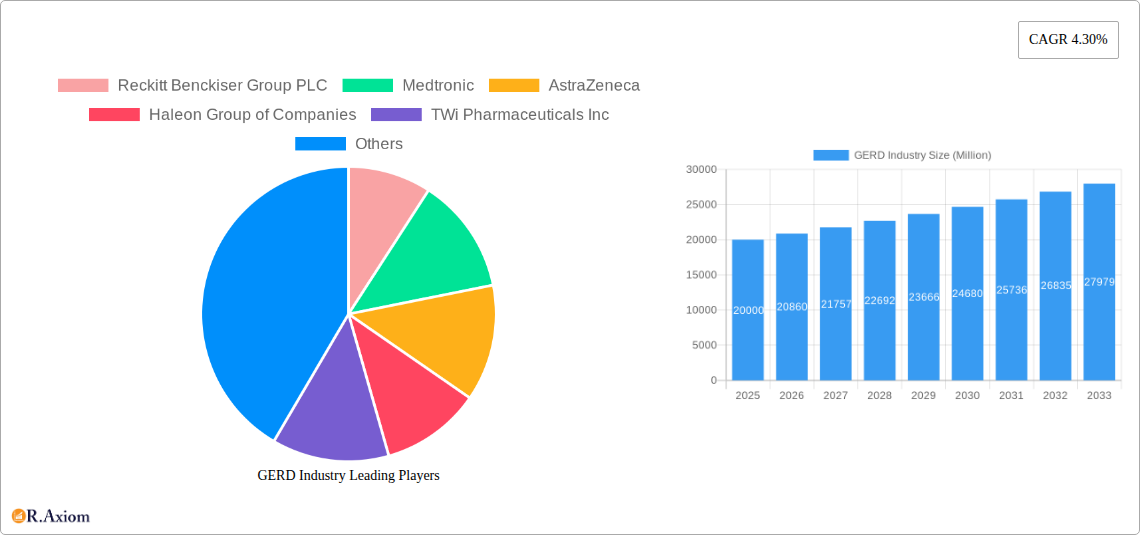

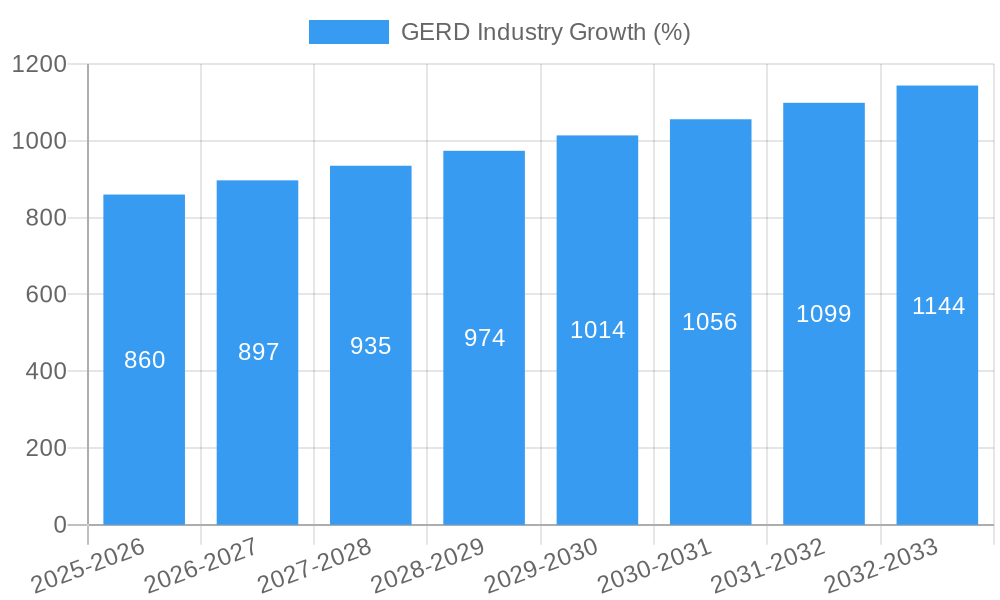

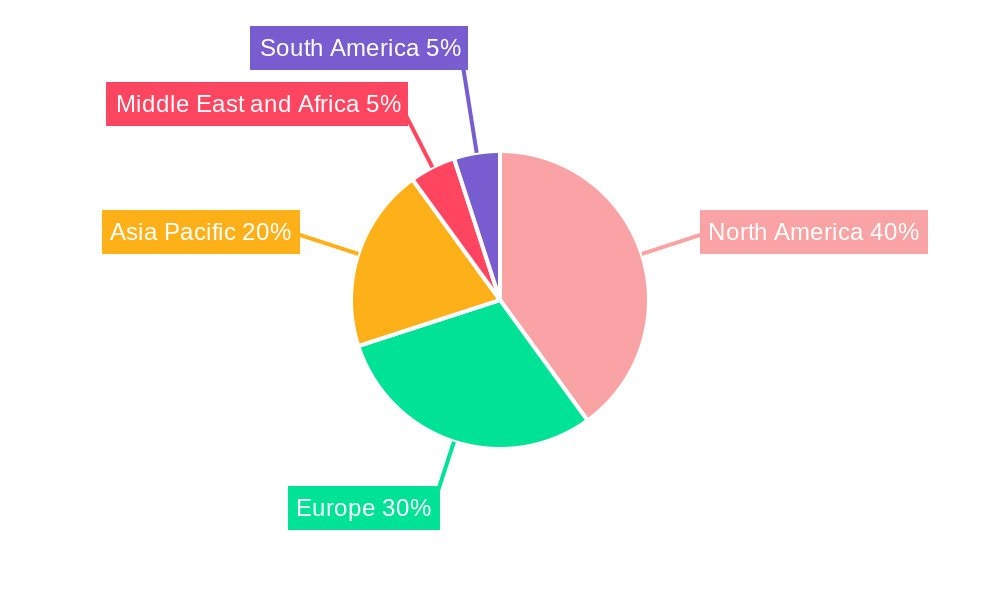

The global Gastroesophageal Reflux Disease (GERD) market, valued at approximately $20 billion in 2025, is projected to experience steady growth, driven by rising prevalence of obesity, unhealthy lifestyles, and an aging population. A Compound Annual Growth Rate (CAGR) of 4.30% from 2025 to 2033 indicates a substantial market expansion, reaching an estimated value exceeding $30 billion by 2033. Key drivers include increased awareness and diagnosis rates, advancements in diagnostic technologies like upper endoscopy and ambulatory pH monitoring, and the availability of various treatment options, including Proton Pump Inhibitors (PPIs) and H2 Receptor Blockers. However, the market faces restraints such as potential side effects associated with long-term PPI use, the emergence of drug resistance, and variations in healthcare access across different regions. Market segmentation reveals a significant share held by PPIs due to their widespread efficacy and affordability, while the upper endoscopy segment dominates diagnostic procedures owing to its accuracy in identifying GERD-related complications. North America and Europe currently hold larger market shares, attributable to high healthcare expenditure and advanced healthcare infrastructure. However, Asia-Pacific is poised for significant growth, driven by rising disposable incomes and increasing healthcare awareness in emerging economies.

The competitive landscape is characterized by the presence of major pharmaceutical companies such as Reckitt Benckiser, AstraZeneca, and Pfizer, along with other significant players. These companies are actively engaged in research and development to improve existing treatments and introduce novel therapies. The market is expected to witness increased competition with the entry of generic drug manufacturers, potentially influencing pricing dynamics. Furthermore, the focus on personalized medicine and the development of targeted therapies tailored to specific patient subgroups are emerging trends expected to significantly shape the future trajectory of the GERD market. Growth will be further influenced by factors like technological advancements, regulatory approvals of new drugs and devices, and evolving treatment guidelines. Continued expansion is expected across all geographical regions, with developing economies exhibiting particularly robust growth potential.

This in-depth report provides a comprehensive analysis of the GERD (Gastroesophageal Reflux Disease) industry, encompassing market size, growth projections, competitive landscape, and future trends. The report covers the period from 2019 to 2033, with a focus on the forecast period of 2025-2033 and a base year of 2025. The study leverages extensive primary and secondary research to deliver actionable insights for industry stakeholders, investors, and businesses operating within this dynamic sector. The market is valued at xx Million in 2025 and is projected to reach xx Million by 2033.

GERD Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the GERD industry, examining market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and merger & acquisition (M&A) activities. The industry is characterized by a moderately concentrated market with key players holding significant market share. However, the presence of numerous generic drug manufacturers contributes to competitive intensity.

Market Concentration: The top five companies, including Reckitt Benckiser Group PLC, Medtronic, AstraZeneca, and others, account for approximately xx% of the global market share in 2025. This concentration is expected to remain relatively stable throughout the forecast period, although smaller players continue to emerge through innovation and acquisitions.

Innovation Drivers: Innovation in the GERD industry is primarily driven by the development of new and improved drug formulations, advanced diagnostic technologies, and minimally invasive treatment procedures. The push for more effective and tolerable therapies, along with a growing demand for personalized medicine, further fuels innovation.

Regulatory Framework: Stringent regulatory requirements, particularly from agencies like the FDA, significantly influence industry developments. These regulations impact drug approvals, clinical trial processes, and market entry strategies. Compliance is a critical factor for success in this sector.

Product Substitutes: Over-the-counter (OTC) antacids and lifestyle modifications represent key substitutes for prescription GERD medications. The availability and affordability of these substitutes influence market dynamics.

End-User Trends: The increasing prevalence of GERD globally, coupled with rising healthcare expenditure and improved awareness among patients, are driving market growth. A growing preference for minimally invasive treatment options is shaping the market.

M&A Activities: The GERD industry has witnessed several significant M&A activities in recent years. For example, Glenmark Pharmaceuticals' acquisition of generic drugs from Wockhardt in 2022 demonstrates the strategic importance of expanding product portfolios. These deals often involve substantial investments (xx Million in aggregate in the last five years) to expand market reach and diversify product offerings. The average deal value is approximately xx Million.

GERD Industry Industry Trends & Insights

The GERD industry exhibits robust growth, driven by several key factors. The market is projected to register a CAGR of xx% during the forecast period (2025-2033). This growth is attributed to several key factors:

- Rising Prevalence of GERD: The global prevalence of GERD is increasing steadily, primarily due to lifestyle changes, such as an increased consumption of processed foods, obesity, and sedentary lifestyles.

- Technological Advancements: Ongoing research and development in diagnostic tools and treatment modalities, including minimally invasive procedures and advanced drug delivery systems, have greatly impacted the market. The market penetration of advanced diagnostic techniques is currently at xx% and is projected to increase to xx% by 2033.

- Growing Awareness and Patient Education: Increasing awareness among the general population about the symptoms and management of GERD is driving demand for both prescription and over-the-counter medications.

- Favorable Regulatory Landscape: While stringent, the regulatory environment has facilitated the introduction of improved and innovative therapeutics. This has encouraged investments in R&D, propelling market growth.

- Increasing Healthcare Expenditure: Rising healthcare spending globally, particularly in developing economies, positively impacts market growth, enhancing access to diagnostic and therapeutic options.

Dominant Markets & Segments in GERD Industry

The North American region holds the dominant position in the GERD market, followed by Europe and Asia-Pacific. This dominance is attributed to factors such as high healthcare expenditure, advanced healthcare infrastructure, and increased prevalence of GERD.

By Diagnosis:

- Proton Pump Inhibitors (PPIs): This segment holds the largest market share due to the high efficacy and widespread use of PPIs in treating GERD.

- H2 Receptor Blockers: This segment is characterized by a significant market share and is expected to grow steadily, driven by the availability of generic medications and their cost-effectiveness.

- Upper Endoscopy: This diagnostic procedure remains a crucial diagnostic tool, driving significant revenue for the segment.

Key Drivers for Dominant Regions:

- North America: High healthcare expenditure, advanced medical infrastructure, and a relatively higher prevalence of GERD compared to other regions.

- Europe: Similar to North America, strong healthcare infrastructure and healthcare spending contribute to the relatively high market size. Stringent regulatory requirements impact market entry strategies.

- Asia-Pacific: This region demonstrates significant growth potential driven by rising disposable income, improved healthcare infrastructure, and increasing awareness of GERD.

GERD Industry Product Developments

Recent product innovations in the GERD industry include novel drug formulations with improved efficacy, reduced side effects, and enhanced patient compliance. These innovations are aimed at addressing unmet needs and improving the overall management of GERD. Advancements in diagnostic tools, such as high-resolution endoscopy and advanced manometry techniques, also contribute to improved diagnosis and personalized treatment. The focus on developing targeted therapies, leveraging biomarkers, and integrating digital health technologies further shapes the future of the GERD market.

Report Scope & Segmentation Analysis

The report provides a detailed segmentation analysis of the GERD market across various parameters.

By Diagnosis: The market is segmented by diagnostic methods: Upper Endoscopy, Ambulatory Acid (pH) Probe Test, Esophageal Manometry, and Others. Each segment's growth projections, market sizes, and competitive dynamics are analyzed. Upper endoscopy is currently the largest segment.

By Drug Type: The market is further segmented by drug type: Proton Pump Inhibitors (PPIs), H2 Receptor Blockers, and Others. PPIs represent the largest market segment in terms of value and volume.

Key Drivers of GERD Industry Growth

Several factors contribute to the growth of the GERD industry: the increasing prevalence of GERD globally, advancements in treatment options, rising healthcare expenditure, and increased patient awareness. Technological advancements, such as the development of novel drug formulations and minimally invasive surgical procedures, are also driving market growth. Furthermore, favorable regulatory environments in several key markets facilitate the adoption of new therapies.

Challenges in the GERD Industry Sector

The GERD industry faces certain challenges, including the stringent regulatory landscape, which can delay the launch of new products. Generic competition also exerts pressure on pricing and profitability. Furthermore, the development of new therapies faces significant R&D costs and inherent risks associated with clinical trials. Supply chain disruptions can also lead to temporary shortages and market instability. The overall impact of these challenges is estimated to result in a xx% reduction in market growth in certain years.

Emerging Opportunities in GERD Industry

Emerging opportunities in the GERD industry include the development of personalized medicine approaches, leveraging advanced diagnostics and biomarkers to tailor treatment to individual patients. The integration of digital health technologies to improve patient engagement and remote monitoring also presents significant growth potential. Furthermore, expanding into emerging markets and developing cost-effective treatment options can tap into unmet needs in several regions.

Leading Players in the GERD Industry Market

- Reckitt Benckiser Group PLC

- Medtronic

- AstraZeneca

- Haleon Group of Companies

- TWi Pharmaceuticals Inc

- Glenmark

- Aurobindo Pharma

- Johnson & Johnson

- Teva Pharmaceuticals Industries Limited

- SRS Life Sciences

- Zydus Group

- Takeda Pharmaceutical Co Ltd

- Pfizer Inc

Key Developments in GERD Industry Industry

- June 2022: Glenmark Pharmaceuticals Ltd acquired generic over-the-counter drugs from Wockhardt Ltd in the US, including famotidine and lansoprazole, expanding its market presence.

- June 2022: Zydus Lifesciences received FDA approval for its famotidine tablets (20mg and 40mg), increasing competition in the H2 receptor blocker segment.

Strategic Outlook for GERD Industry Market

The GERD industry is poised for continued growth, driven by advancements in treatment options, rising healthcare expenditure, and growing patient awareness. Future opportunities lie in personalized medicine, digital health technologies, and expanding into emerging markets. The focus on developing innovative therapies with improved efficacy and reduced side effects will shape future market trends and competition. The overall outlook remains positive, with the industry expected to witness substantial growth over the coming years.

GERD Industry Segmentation

-

1. Diagnosis

- 1.1. Upper Endoscopy

- 1.2. Ambulatory Acid (pH) Probe Test

- 1.3. Esophageal Manometry

- 1.4. Others

-

2. Drug Type

- 2.1. Proton Pump Inhibitors (PPIs)

- 2.2. H2 Receptor Blockers

- 2.3. Others

GERD Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

GERD Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.30% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Prevalence of Gastrointestinal Reflux Diseases and Changing Lifestyle; Increasing Awareness about GERD

- 3.3. Market Restrains

- 3.3.1. Patent Expiry of Blockbuster Drugs and Frequent Product Recalls

- 3.4. Market Trends

- 3.4.1. H2 Receptor Blockers Segment is Expected to Witness Growth Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global GERD Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Diagnosis

- 5.1.1. Upper Endoscopy

- 5.1.2. Ambulatory Acid (pH) Probe Test

- 5.1.3. Esophageal Manometry

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Drug Type

- 5.2.1. Proton Pump Inhibitors (PPIs)

- 5.2.2. H2 Receptor Blockers

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Diagnosis

- 6. North America GERD Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Diagnosis

- 6.1.1. Upper Endoscopy

- 6.1.2. Ambulatory Acid (pH) Probe Test

- 6.1.3. Esophageal Manometry

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Drug Type

- 6.2.1. Proton Pump Inhibitors (PPIs)

- 6.2.2. H2 Receptor Blockers

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Diagnosis

- 7. Europe GERD Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Diagnosis

- 7.1.1. Upper Endoscopy

- 7.1.2. Ambulatory Acid (pH) Probe Test

- 7.1.3. Esophageal Manometry

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Drug Type

- 7.2.1. Proton Pump Inhibitors (PPIs)

- 7.2.2. H2 Receptor Blockers

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Diagnosis

- 8. Asia Pacific GERD Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Diagnosis

- 8.1.1. Upper Endoscopy

- 8.1.2. Ambulatory Acid (pH) Probe Test

- 8.1.3. Esophageal Manometry

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Drug Type

- 8.2.1. Proton Pump Inhibitors (PPIs)

- 8.2.2. H2 Receptor Blockers

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Diagnosis

- 9. Middle East and Africa GERD Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Diagnosis

- 9.1.1. Upper Endoscopy

- 9.1.2. Ambulatory Acid (pH) Probe Test

- 9.1.3. Esophageal Manometry

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Drug Type

- 9.2.1. Proton Pump Inhibitors (PPIs)

- 9.2.2. H2 Receptor Blockers

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Diagnosis

- 10. South America GERD Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Diagnosis

- 10.1.1. Upper Endoscopy

- 10.1.2. Ambulatory Acid (pH) Probe Test

- 10.1.3. Esophageal Manometry

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Drug Type

- 10.2.1. Proton Pump Inhibitors (PPIs)

- 10.2.2. H2 Receptor Blockers

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Diagnosis

- 11. North America GERD Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe GERD Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Italy

- 12.1.5 Spain

- 12.1.6 Rest of Europe

- 13. Asia Pacific GERD Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 South Korea

- 13.1.6 Rest of Asia Pacific

- 14. Middle East and Africa GERD Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 GCC

- 14.1.2 South Africa

- 14.1.3 Rest of Middle East and Africa

- 15. South America GERD Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Reckitt Benckiser Group PLC

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Medtronic

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 AstraZeneca

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Haleon Group of Companies

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 TWi Pharmaceuticals Inc

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Glenmark

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Aurobindo Pharma*List Not Exhaustive

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Johnson & Johnson

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Teva Pharmaceuticals Industries Limited

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 SRS Life Sciences

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Zydus Group

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 Takeda Pharmaceutical Co Ltd

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Pfizer Inc

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.1 Reckitt Benckiser Group PLC

List of Figures

- Figure 1: Global GERD Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America GERD Industry Revenue (Million), by Diagnosis 2024 & 2032

- Figure 13: North America GERD Industry Revenue Share (%), by Diagnosis 2024 & 2032

- Figure 14: North America GERD Industry Revenue (Million), by Drug Type 2024 & 2032

- Figure 15: North America GERD Industry Revenue Share (%), by Drug Type 2024 & 2032

- Figure 16: North America GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe GERD Industry Revenue (Million), by Diagnosis 2024 & 2032

- Figure 19: Europe GERD Industry Revenue Share (%), by Diagnosis 2024 & 2032

- Figure 20: Europe GERD Industry Revenue (Million), by Drug Type 2024 & 2032

- Figure 21: Europe GERD Industry Revenue Share (%), by Drug Type 2024 & 2032

- Figure 22: Europe GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific GERD Industry Revenue (Million), by Diagnosis 2024 & 2032

- Figure 25: Asia Pacific GERD Industry Revenue Share (%), by Diagnosis 2024 & 2032

- Figure 26: Asia Pacific GERD Industry Revenue (Million), by Drug Type 2024 & 2032

- Figure 27: Asia Pacific GERD Industry Revenue Share (%), by Drug Type 2024 & 2032

- Figure 28: Asia Pacific GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa GERD Industry Revenue (Million), by Diagnosis 2024 & 2032

- Figure 31: Middle East and Africa GERD Industry Revenue Share (%), by Diagnosis 2024 & 2032

- Figure 32: Middle East and Africa GERD Industry Revenue (Million), by Drug Type 2024 & 2032

- Figure 33: Middle East and Africa GERD Industry Revenue Share (%), by Drug Type 2024 & 2032

- Figure 34: Middle East and Africa GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East and Africa GERD Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: South America GERD Industry Revenue (Million), by Diagnosis 2024 & 2032

- Figure 37: South America GERD Industry Revenue Share (%), by Diagnosis 2024 & 2032

- Figure 38: South America GERD Industry Revenue (Million), by Drug Type 2024 & 2032

- Figure 39: South America GERD Industry Revenue Share (%), by Drug Type 2024 & 2032

- Figure 40: South America GERD Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: South America GERD Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global GERD Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global GERD Industry Revenue Million Forecast, by Diagnosis 2019 & 2032

- Table 3: Global GERD Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 4: Global GERD Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Germany GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Japan GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: India GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Australia GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: South Korea GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Asia Pacific GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: GCC GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Africa GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Middle East and Africa GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Brazil GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Argentina GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of South America GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global GERD Industry Revenue Million Forecast, by Diagnosis 2019 & 2032

- Table 32: Global GERD Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 33: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: United States GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Canada GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Mexico GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global GERD Industry Revenue Million Forecast, by Diagnosis 2019 & 2032

- Table 38: Global GERD Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 39: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 40: Germany GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: United Kingdom GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: France GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Italy GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Spain GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Rest of Europe GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global GERD Industry Revenue Million Forecast, by Diagnosis 2019 & 2032

- Table 47: Global GERD Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 48: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 49: China GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Japan GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: India GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Australia GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: South Korea GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Rest of Asia Pacific GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Global GERD Industry Revenue Million Forecast, by Diagnosis 2019 & 2032

- Table 56: Global GERD Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 57: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: GCC GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: South Africa GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Rest of Middle East and Africa GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Global GERD Industry Revenue Million Forecast, by Diagnosis 2019 & 2032

- Table 62: Global GERD Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 63: Global GERD Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 64: Brazil GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Argentina GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Rest of South America GERD Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the GERD Industry?

The projected CAGR is approximately 4.30%.

2. Which companies are prominent players in the GERD Industry?

Key companies in the market include Reckitt Benckiser Group PLC, Medtronic, AstraZeneca, Haleon Group of Companies, TWi Pharmaceuticals Inc, Glenmark, Aurobindo Pharma*List Not Exhaustive, Johnson & Johnson, Teva Pharmaceuticals Industries Limited, SRS Life Sciences, Zydus Group, Takeda Pharmaceutical Co Ltd, Pfizer Inc.

3. What are the main segments of the GERD Industry?

The market segments include Diagnosis, Drug Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Gastrointestinal Reflux Diseases and Changing Lifestyle; Increasing Awareness about GERD.

6. What are the notable trends driving market growth?

H2 Receptor Blockers Segment is Expected to Witness Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Patent Expiry of Blockbuster Drugs and Frequent Product Recalls.

8. Can you provide examples of recent developments in the market?

In June 2022, Glenmark Pharmaceuticals Ltd acquired the approved generic versions of certain over-the-counter drugs from Wockhardt Ltd in the United States. The acquisition by the company's fully owned subsidiary Glenmark Pharmaceuticals Inc, USA includes the approved abbreviated new drug applications (ANDAs) for famotidine tablets (10 mg and 20 mg) used to treat and prevent ulcers in the stomach and intestine, including indigestion, heartburn, and acid reflux treatment drug Lansoprazole delayed-release capsules USP, 15 mg, among other drugs.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "GERD Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the GERD Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the GERD Industry?

To stay informed about further developments, trends, and reports in the GERD Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence