Key Insights

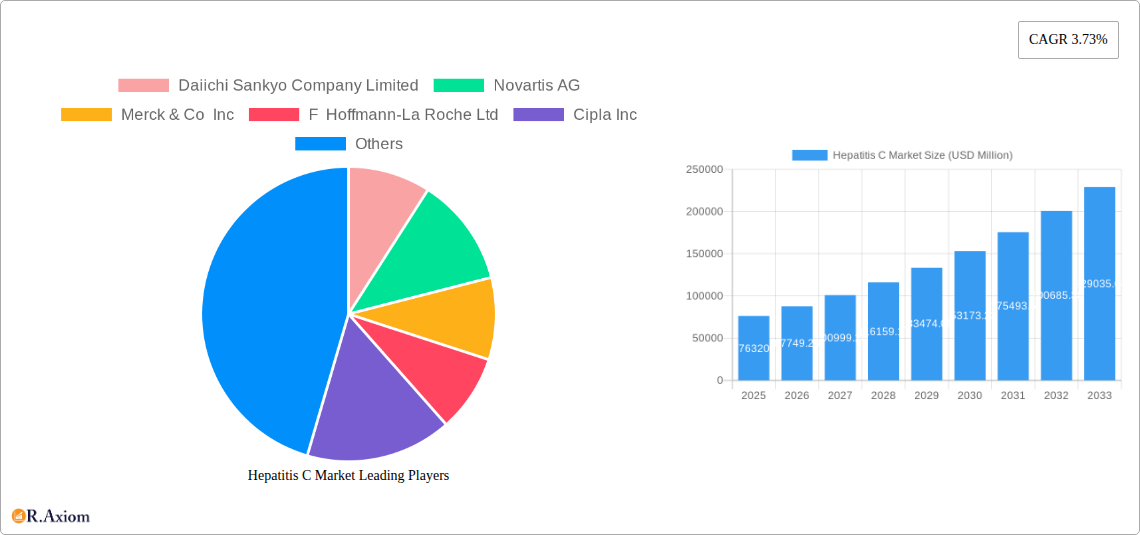

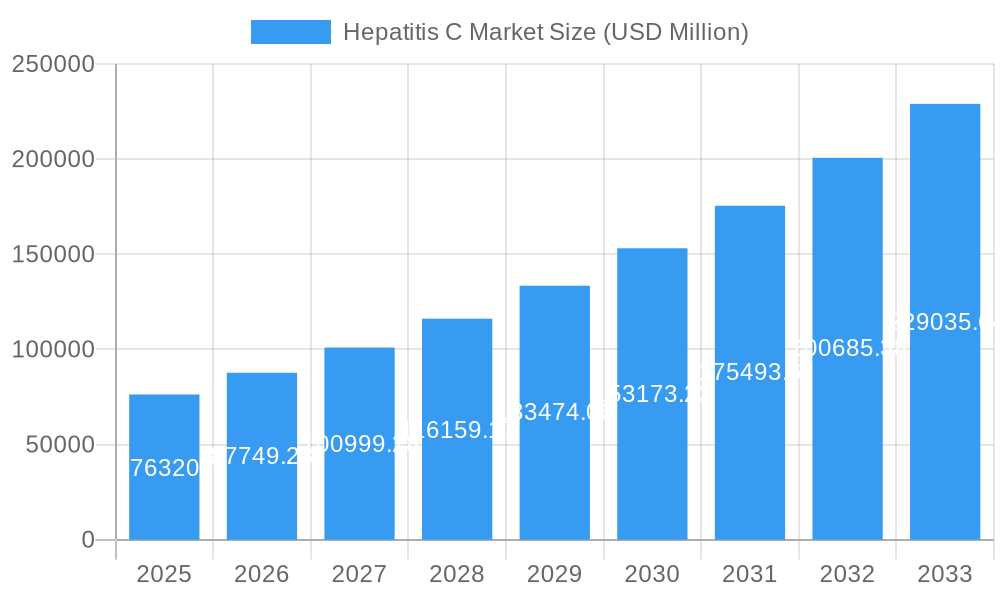

The global Hepatitis C market is poised for significant expansion, projected to reach USD 76.32 billion in 2025 and exhibit a robust Compound Annual Growth Rate (CAGR) of 15.1% throughout the forecast period of 2025-2033. This impressive growth trajectory is underpinned by advancements in diagnostic tools and therapeutic interventions. The increasing prevalence of Hepatitis C globally, coupled with a growing emphasis on early detection and effective treatment regimens, fuels market expansion. Innovations in antiviral drugs are a primary driver, offering higher cure rates and improved patient outcomes. Furthermore, heightened awareness campaigns and government initiatives aimed at disease eradication contribute to the market's upward momentum. The diagnosis segment is driven by the development of more accessible and accurate blood tests, reducing reliance on invasive procedures like liver biopsies. The treatment segment, in turn, benefits from the continuous research and development of novel drug formulations and combination therapies that address drug resistance and improve patient compliance.

Hepatitis C Market Market Size (In Billion)

The market's expansion is also influenced by the expanding healthcare infrastructure and increased healthcare spending in emerging economies, particularly in the Asia Pacific and Latin America regions. Key market players are actively investing in research and development, strategic collaborations, and mergers and acquisitions to strengthen their market positions and expand their product portfolios. While the market exhibits strong growth potential, certain factors like the high cost of advanced treatments and challenges in patient access in some regions may pose moderate restraints. However, the overall outlook remains highly optimistic, driven by a comprehensive approach to Hepatitis C management encompassing early diagnosis, effective treatment, and a commitment to global elimination efforts. The market segmentation, covering various diagnostic methods, treatment options, and end-user segments like hospitals and diagnostic laboratories, reflects the diverse landscape and opportunities within the Hepatitis C market.

Hepatitis C Market Company Market Share

This in-depth report provides a comprehensive analysis of the global Hepatitis C market, offering critical insights into its trajectory from 2019 to 2033, with a base year of 2025. The market is segmented by Type (Diagnosis and Treatment), End-User (Hospitals and Clinics, Diagnostic Laboratory, and Other End-Users), and is driven by significant advancements in diagnostic tools and highly effective antiviral therapies. Industry stakeholders will gain a profound understanding of market dynamics, competitive landscapes, and emerging opportunities within this vital healthcare sector. The global Hepatitis C market is projected to reach substantial valuations, exceeding $XX billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025–2033).

Hepatitis C Market Market Concentration & Innovation

The Hepatitis C market exhibits a moderate to high concentration, primarily dominated by a few key players who have pioneered the development of revolutionary direct-acting antiviral (DAA) drugs. Innovation in this sector is largely driven by the ongoing pursuit of pan-genotypic treatments with improved efficacy, shorter treatment durations, and reduced side effects. Regulatory frameworks, such as those established by the FDA and EMA, play a crucial role in accelerating the approval of novel therapies and diagnostic methods, thereby fostering innovation. Product substitutes, while present in earlier treatment regimens (e.g., interferon-based therapies), have been largely supplanted by DAAs due to their superior safety and effectiveness. End-user trends are shifting towards increased demand for outpatient treatment models and integrated care pathways to manage co-infections and chronic liver disease. Mergers and acquisitions (M&A) have been a significant strategy for market consolidation, with several multi-billion dollar deals shaping the competitive landscape. For instance, the acquisition of potential pipeline assets or companies specializing in novel drug delivery mechanisms could significantly alter market shares. The overall market share of leading DAA manufacturers remains high, reflecting the significant R&D investment required for drug development.

Hepatitis C Market Industry Trends & Insights

The Hepatitis C market is characterized by dynamic growth, fueled by an increasing global prevalence of the virus and a growing emphasis on early diagnosis and effective treatment. Technological advancements in diagnostic techniques, including highly sensitive blood tests and improved molecular diagnostics, are crucial for identifying infected individuals more efficiently. The advent of direct-acting antivirals (DAAs) has revolutionized Hepatitis C treatment, offering cure rates exceeding 95% with significantly shorter treatment durations compared to older therapies. This has led to a substantial increase in market penetration as healthcare systems prioritize the elimination of Hepatitis C. Consumer preferences are increasingly leaning towards minimally invasive diagnostic procedures and outpatient treatment options that offer convenience and minimize disruption to daily life. The competitive dynamics are intense, with global pharmaceutical giants investing heavily in research and development to discover next-generation therapies, expand treatment indications, and address emerging drug resistance. Market growth drivers include rising healthcare expenditures globally, increased awareness campaigns, and government initiatives aimed at Hepatitis C eradication. The market penetration of effective treatments is projected to continue its upward trend, particularly in regions with high disease burden. The CAGR is expected to remain strong, driven by the sustained demand for curative therapies and ongoing efforts to reach underserved populations.

Dominant Markets & Segments in Hepatitis C Market

The Treatment segment, particularly Antiviral Drugs, is the dominant force within the Hepatitis C market. This dominance is primarily attributed to the transformative impact of Direct-Acting Antivirals (DAAs) that offer high cure rates and significantly improved patient outcomes.

- Antiviral Drugs: This sub-segment's leadership is propelled by the widespread adoption of DAAs. Key drivers include:

- High Efficacy Rates: Curative potential exceeding 95% for most genotypes.

- Improved Safety Profiles: Reduced side effects compared to older interferon-based treatments.

- Shorter Treatment Durations: Typically 8-12 weeks, improving patient adherence and reducing healthcare burden.

- Pan-Genotypic Options: Treatments effective against multiple Hepatitis C genotypes, simplifying treatment selection.

- Government Initiatives: National strategies focused on Hepatitis C elimination are increasing demand.

- Cost-Effectiveness: Despite high initial costs, the long-term benefits of a cure (preventing cirrhosis and liver cancer) make DAAs cost-effective.

The Diagnosis segment, specifically Blood Tests, plays a crucial supporting role, with its growth intrinsically linked to the treatment segment.

- Blood Tests: The increasing focus on screening and early detection drives this segment. Key drivers include:

- Accessibility and Affordability: Routine blood tests are widely available and relatively inexpensive.

- Technological Advancements: Development of more sensitive and specific serological and molecular assays.

- Public Health Campaigns: Increased awareness encourages individuals to undergo screening.

- Screening Recommendations: Guidelines for at-risk populations and universal screening are expanding.

In terms of End-Users, Hospitals and Clinics represent the largest share, as they are the primary points of care for diagnosis, treatment initiation, and ongoing management of Hepatitis C patients.

- Hospitals and Clinics: Their dominance stems from:

- Integrated Care: Ability to offer comprehensive services from diagnosis to treatment and follow-up.

- Specialized Hepatology and Gastroenterology Departments: Expertise required for complex cases and co-infections.

- Access to Infusion Services: Necessary for certain treatment regimens.

- Established Infrastructure: Readily equipped to handle diagnostic procedures and administer medications.

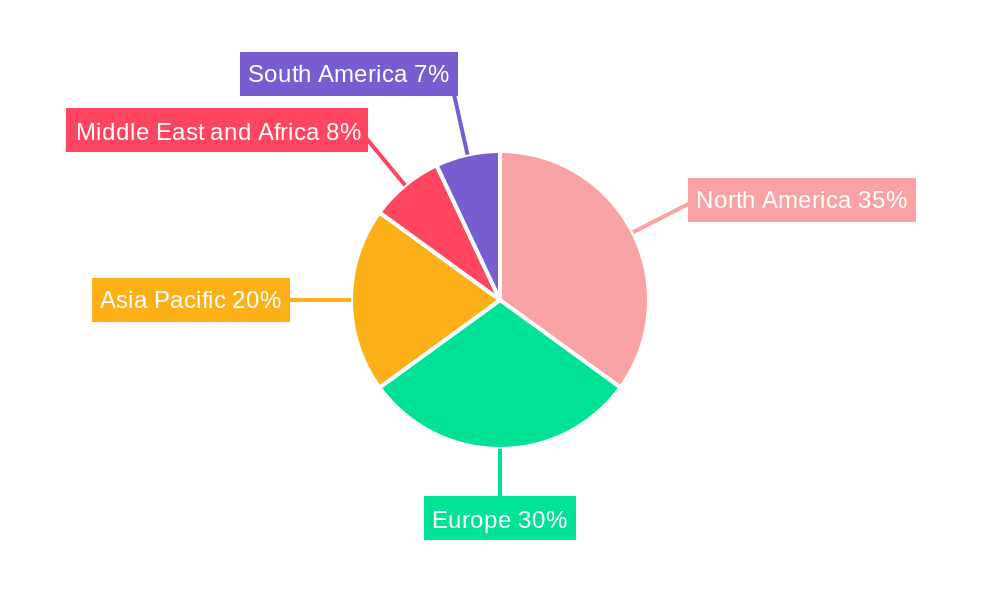

Geographically, North America and Europe currently lead the Hepatitis C market due to high per capita healthcare spending, well-established healthcare infrastructure, and proactive public health initiatives aimed at Hepatitis C eradication. However, the Asia Pacific region is poised for significant growth, driven by increasing disease prevalence, improving healthcare access, and rising disposable incomes.

Hepatitis C Market Product Developments

Recent product developments in the Hepatitis C market have focused on enhancing treatment efficacy and expanding access to cure. Innovation centers on developing pan-genotypic regimens with shorter durations and improved tolerability, aiming to simplify treatment protocols and reduce costs. The competitive advantage for manufacturers lies in offering highly effective, all-oral therapies that can treat all major genotypes of the Hepatitis C virus with minimal side effects. Furthermore, advancements in diagnostic technologies are contributing to earlier and more accurate identification of infected individuals, thereby facilitating timely intervention. The market is also witnessing a trend towards combination therapies and exploring novel drug delivery systems to further improve patient adherence and therapeutic outcomes.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Hepatitis C market across its key segments. The Diagnosis segment encompasses Liver Biopsy, Blood Tests, and Other Diagnoses, with Blood Tests currently holding the largest market share due to their widespread use in screening and confirmation. The Treatment segment includes Antiviral Drugs, Immune Modulator Drugs, and Other Treatments, where Antiviral Drugs, particularly DAAs, are the dominant category, projected for substantial growth driven by high cure rates. The End-User segment comprises Hospitals and Clinics, Diagnostic Laboratory, and Other End-Users. Hospitals and Clinics are expected to maintain their leading position due to the integrated nature of Hepatitis C care. Each segment is analyzed for its projected market size, growth trajectory, and competitive dynamics throughout the study period.

Key Drivers of Hepatitis C Market Growth

The Hepatitis C market's growth is primarily propelled by several critical factors. Firstly, increasing global awareness and extensive public health campaigns are leading to higher rates of diagnosis and screening, particularly in at-risk populations. Secondly, significant advancements in medical technology have resulted in the development of highly effective direct-acting antiviral (DAA) drugs, offering cure rates exceeding 95% and significantly reducing treatment durations and side effects. Thirdly, favorable reimbursement policies and government initiatives focused on Hepatitis C elimination in various countries are expanding access to treatment. Lastly, the growing prevalence of Hepatitis C, coupled with an aging global population, contributes to a sustained demand for effective diagnostic and therapeutic solutions.

Challenges in the Hepatitis C Market Sector

Despite its positive trajectory, the Hepatitis C market faces several challenges. The high cost of innovative direct-acting antiviral (DAA) therapies remains a significant barrier to access, particularly in low and middle-income countries, impacting market penetration. Navigating complex regulatory approval processes and stringent post-market surveillance requirements can also slow down the introduction of new treatments. Furthermore, ensuring equitable access to diagnosis and treatment across diverse geographical regions and socioeconomic strata presents an ongoing challenge. The potential development of drug resistance, though less common with current DAAs, remains a concern that necessitates continuous research and development for next-generation therapies. Supply chain disruptions and intellectual property disputes can also affect market stability.

Emerging Opportunities in Hepatitis C Market

Emerging opportunities in the Hepatitis C market are primarily centered around expanding access to treatment in underserved regions and developing novel therapeutic approaches. The focus on Hepatitis C elimination strategies by global health organizations presents a significant opportunity for market growth. Innovations in drug formulation and delivery systems that further simplify treatment regimens and improve patient adherence are highly sought after. Furthermore, the development of cost-effective generic versions of existing DAAs in emerging markets will drive significant volume growth. Opportunities also lie in integrated care models that manage co-infections, such as Hepatitis C and HIV, and in leveraging digital health technologies for patient monitoring and support. Research into potential cures beyond antiviral therapy and understanding the long-term impact of cured Hepatitis C on liver health also present future avenues.

Leading Players in the Hepatitis C Market Market

- Gilead Sciences Inc

- AbbVie Inc

- Bristol-Myers Squibb Company

- Merck & Co Inc

- Novartis AG

- Johnson & Johnson

- F Hoffmann-La Roche Ltd

- GlaxoSmithKline plc

- Daiichi Sankyo Company Limited

- Takeda Pharmaceutical Company Limited

- Eli Lilly and Company

- Cipla Inc

- Astellas Pharma Inc

Key Developments in Hepatitis C Market Industry

- January 2023: HIVMA created guidance for treating patients with COVID-19 with nirmatrelvir-ritonavir (Paxlovid) who have HIV or hepatitis C. The guidance includes a link to IDSA's clinical guidance for using nirmatrelvir- ritonavir and potential drug interactions.

- September 2022: Texas Medicaid designated MAVYRET medication as the primary preferred direct-acting antiviral (DAA) drug option for treating a hepatitis C infection.

Strategic Outlook for Hepatitis C Market Market

The strategic outlook for the Hepatitis C market is overwhelmingly positive, driven by a strong pipeline of innovative therapies and a global commitment to Hepatitis C elimination. Key growth catalysts include the ongoing expansion of direct-acting antiviral (DAA) treatments, with a focus on pan-genotypic efficacy and reduced treatment durations. Manufacturers are strategically investing in expanding market access in high-burden regions and developing more affordable treatment options. The increasing emphasis on early diagnosis through widespread screening programs will further fuel demand for both diagnostic tools and curative therapies. Strategic partnerships and collaborations to develop novel treatment combinations and address any remaining unmet needs, such as treating difficult-to-cure genotypes or patients with advanced liver disease, will also shape the future landscape. The market's trajectory is firmly set towards achieving significant reductions in Hepatitis C prevalence and incidence globally.

Hepatitis C Market Segmentation

-

1. Type

-

1.1. Diagnosis

- 1.1.1. Liver Biopsy

- 1.1.2. Blood Tests

- 1.1.3. Other Diagnoses

-

1.2. Treatment

- 1.2.1. Antiviral Drugs

- 1.2.2. Immune Modulator Drugs

- 1.2.3. Other Treatments

-

1.1. Diagnosis

-

2. End-User

- 2.1. Hospitals and Clinics

- 2.2. Diagnostic Laboratory

- 2.3. Other End-Users

Hepatitis C Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Hepatitis C Market Regional Market Share

Geographic Coverage of Hepatitis C Market

Hepatitis C Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Diagnosis

- 5.1.1.1. Liver Biopsy

- 5.1.1.2. Blood Tests

- 5.1.1.3. Other Diagnoses

- 5.1.2. Treatment

- 5.1.2.1. Antiviral Drugs

- 5.1.2.2. Immune Modulator Drugs

- 5.1.2.3. Other Treatments

- 5.1.1. Diagnosis

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Hospitals and Clinics

- 5.2.2. Diagnostic Laboratory

- 5.2.3. Other End-Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Hepatitis C Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Diagnosis

- 6.1.1.1. Liver Biopsy

- 6.1.1.2. Blood Tests

- 6.1.1.3. Other Diagnoses

- 6.1.2. Treatment

- 6.1.2.1. Antiviral Drugs

- 6.1.2.2. Immune Modulator Drugs

- 6.1.2.3. Other Treatments

- 6.1.1. Diagnosis

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Hospitals and Clinics

- 6.2.2. Diagnostic Laboratory

- 6.2.3. Other End-Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Hepatitis C Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Diagnosis

- 7.1.1.1. Liver Biopsy

- 7.1.1.2. Blood Tests

- 7.1.1.3. Other Diagnoses

- 7.1.2. Treatment

- 7.1.2.1. Antiviral Drugs

- 7.1.2.2. Immune Modulator Drugs

- 7.1.2.3. Other Treatments

- 7.1.1. Diagnosis

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Hospitals and Clinics

- 7.2.2. Diagnostic Laboratory

- 7.2.3. Other End-Users

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Hepatitis C Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Diagnosis

- 8.1.1.1. Liver Biopsy

- 8.1.1.2. Blood Tests

- 8.1.1.3. Other Diagnoses

- 8.1.2. Treatment

- 8.1.2.1. Antiviral Drugs

- 8.1.2.2. Immune Modulator Drugs

- 8.1.2.3. Other Treatments

- 8.1.1. Diagnosis

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Hospitals and Clinics

- 8.2.2. Diagnostic Laboratory

- 8.2.3. Other End-Users

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Hepatitis C Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Diagnosis

- 9.1.1.1. Liver Biopsy

- 9.1.1.2. Blood Tests

- 9.1.1.3. Other Diagnoses

- 9.1.2. Treatment

- 9.1.2.1. Antiviral Drugs

- 9.1.2.2. Immune Modulator Drugs

- 9.1.2.3. Other Treatments

- 9.1.1. Diagnosis

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Hospitals and Clinics

- 9.2.2. Diagnostic Laboratory

- 9.2.3. Other End-Users

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Hepatitis C Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Diagnosis

- 10.1.1.1. Liver Biopsy

- 10.1.1.2. Blood Tests

- 10.1.1.3. Other Diagnoses

- 10.1.2. Treatment

- 10.1.2.1. Antiviral Drugs

- 10.1.2.2. Immune Modulator Drugs

- 10.1.2.3. Other Treatments

- 10.1.1. Diagnosis

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Hospitals and Clinics

- 10.2.2. Diagnostic Laboratory

- 10.2.3. Other End-Users

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South America Hepatitis C Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Diagnosis

- 11.1.1.1. Liver Biopsy

- 11.1.1.2. Blood Tests

- 11.1.1.3. Other Diagnoses

- 11.1.2. Treatment

- 11.1.2.1. Antiviral Drugs

- 11.1.2.2. Immune Modulator Drugs

- 11.1.2.3. Other Treatments

- 11.1.1. Diagnosis

- 11.2. Market Analysis, Insights and Forecast - by End-User

- 11.2.1. Hospitals and Clinics

- 11.2.2. Diagnostic Laboratory

- 11.2.3. Other End-Users

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Daiichi Sankyo Company Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Novartis AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Merck & Co Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 F Hoffmann-La Roche Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cipla Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 GlaxoSmithKline plc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Takeda Pharmaceutical Company Limited

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Eli Lilly and Company

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AbbVie Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Johnson & Johnson

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Astellas Pharma Inc *List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Gilead Sciences Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Bristol-Myers Squibb Company

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Daiichi Sankyo Company Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Hepatitis C Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Hepatitis C Market Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Hepatitis C Market Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Hepatitis C Market Revenue (billion), by End-User 2025 & 2033

- Figure 5: North America Hepatitis C Market Revenue Share (%), by End-User 2025 & 2033

- Figure 6: North America Hepatitis C Market Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Hepatitis C Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Hepatitis C Market Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Hepatitis C Market Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Hepatitis C Market Revenue (billion), by End-User 2025 & 2033

- Figure 11: Europe Hepatitis C Market Revenue Share (%), by End-User 2025 & 2033

- Figure 12: Europe Hepatitis C Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Hepatitis C Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Hepatitis C Market Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific Hepatitis C Market Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Hepatitis C Market Revenue (billion), by End-User 2025 & 2033

- Figure 17: Asia Pacific Hepatitis C Market Revenue Share (%), by End-User 2025 & 2033

- Figure 18: Asia Pacific Hepatitis C Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Hepatitis C Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Hepatitis C Market Revenue (billion), by Type 2025 & 2033

- Figure 21: Middle East and Africa Hepatitis C Market Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East and Africa Hepatitis C Market Revenue (billion), by End-User 2025 & 2033

- Figure 23: Middle East and Africa Hepatitis C Market Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Middle East and Africa Hepatitis C Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Hepatitis C Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Hepatitis C Market Revenue (billion), by Type 2025 & 2033

- Figure 27: South America Hepatitis C Market Revenue Share (%), by Type 2025 & 2033

- Figure 28: South America Hepatitis C Market Revenue (billion), by End-User 2025 & 2033

- Figure 29: South America Hepatitis C Market Revenue Share (%), by End-User 2025 & 2033

- Figure 30: South America Hepatitis C Market Revenue (billion), by Country 2025 & 2033

- Figure 31: South America Hepatitis C Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hepatitis C Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Hepatitis C Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 3: Global Hepatitis C Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Hepatitis C Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Hepatitis C Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 6: Global Hepatitis C Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Hepatitis C Market Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Hepatitis C Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 12: Global Hepatitis C Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Hepatitis C Market Revenue billion Forecast, by Type 2020 & 2033

- Table 20: Global Hepatitis C Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 21: Global Hepatitis C Market Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Hepatitis C Market Revenue billion Forecast, by Type 2020 & 2033

- Table 29: Global Hepatitis C Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 30: Global Hepatitis C Market Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Hepatitis C Market Revenue billion Forecast, by Type 2020 & 2033

- Table 35: Global Hepatitis C Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 36: Global Hepatitis C Market Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Hepatitis C Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hepatitis C Market?

The projected CAGR is approximately 13.1%.

2. Which companies are prominent players in the Hepatitis C Market?

Key companies in the market include Daiichi Sankyo Company Limited, Novartis AG, Merck & Co Inc, F Hoffmann-La Roche Ltd, Cipla Inc, GlaxoSmithKline plc, Takeda Pharmaceutical Company Limited, Eli Lilly and Company, AbbVie Inc, Johnson & Johnson, Astellas Pharma Inc *List Not Exhaustive, Gilead Sciences Inc, Bristol-Myers Squibb Company.

3. What are the main segments of the Hepatitis C Market?

The market segments include Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 71.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Disease Burden of Hepatitis C; Increasing Awareness and Advances in Diagnosis; Surge In Availability of Advanced Therapeutic Products.

6. What are the notable trends driving market growth?

Antiviral Drugs Segment is Expected to Hold a Major Share in the Hepatitis C Market.

7. Are there any restraints impacting market growth?

High Cost of Treatment; Social Stigma and Undiagnosed Cases.

8. Can you provide examples of recent developments in the market?

January 2023: HIVMA created guidance for treating patients with COVID-19 with nirmatrelvir-ritonavir (Paxlovid) who have HIV or hepatitis C. The guidance includes a link to IDSA's clinical guidance for using nirmatrelvir- ritonavir and potential drug interactions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hepatitis C Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hepatitis C Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hepatitis C Market?

To stay informed about further developments, trends, and reports in the Hepatitis C Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence