Key Insights

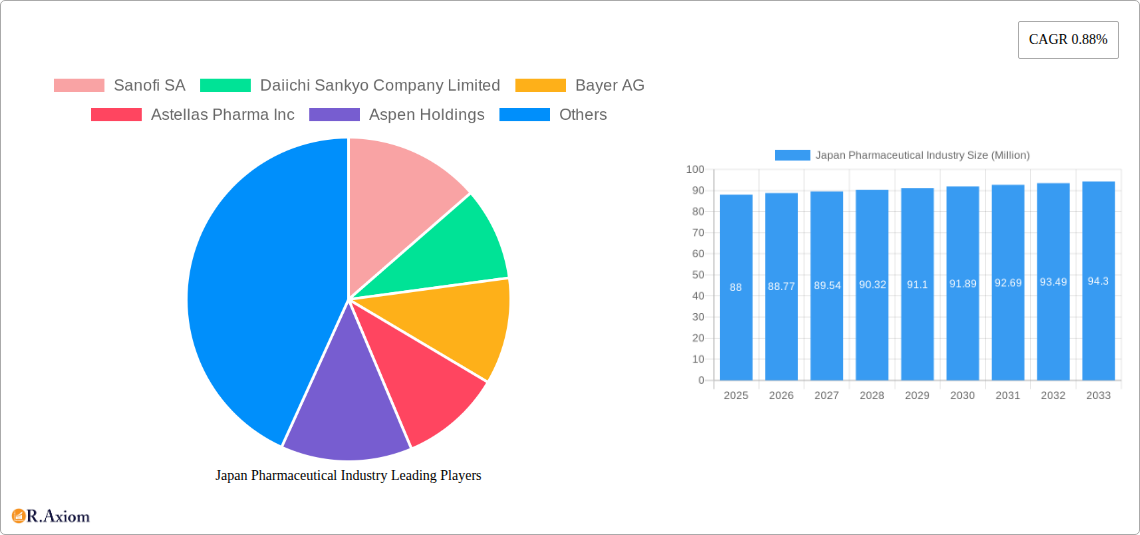

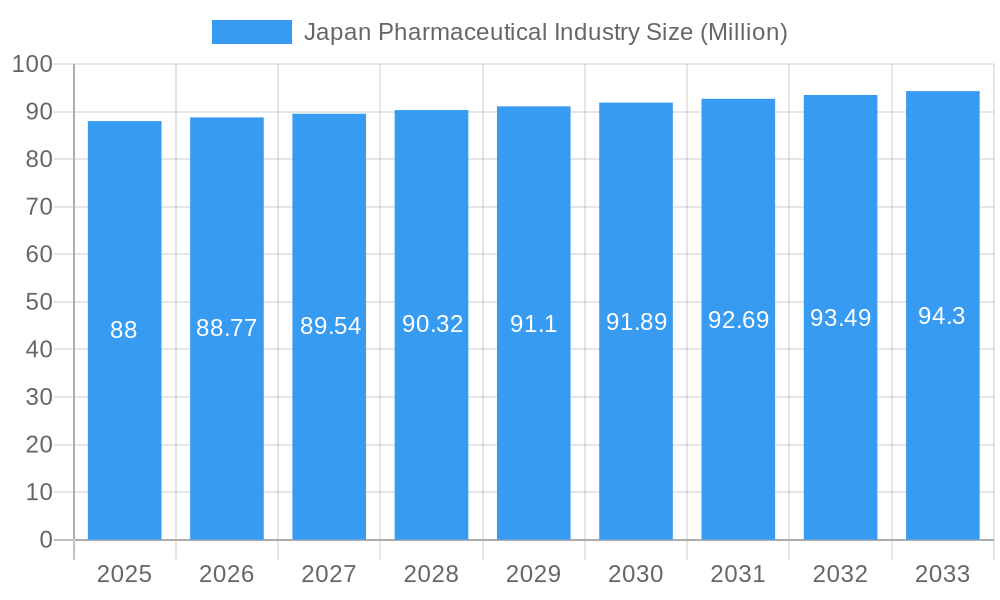

The Japanese pharmaceutical market is poised for steady expansion, projected to reach $88.00 million in 2025, with a compound annual growth rate (CAGR) of 0.88% during the forecast period of 2025-2033. This growth is underpinned by a confluence of factors, including an aging population that drives demand for treatments across various therapeutic areas, particularly cardiovascular and dermatological conditions. The increasing prevalence of lifestyle-related diseases and a strong emphasis on healthcare innovation further contribute to market buoyancy. Furthermore, the growing adoption of over-the-counter (OTC) drugs for minor ailments and proactive health management presents a significant opportunity for market players. Strategic investments in research and development for novel therapies, coupled with supportive government initiatives aimed at fostering pharmaceutical innovation and ensuring drug accessibility, are expected to propel the market forward.

Japan Pharmaceutical Industry Market Size (In Million)

Key market segments contributing to this growth include the Cardiovascular System, Dermatologicals, and Respiratory System, reflecting the demographic and health trends prevalent in Japan. The market is characterized by a dual approach to prescription drugs and OTC offerings, catering to a broad spectrum of healthcare needs. Leading global and domestic pharmaceutical companies such as Sanofi SA, Novartis International AG, Merck & Co Inc, Pfizer Inc, and Takeda Pharmaceutical Company Limited are actively engaged in this dynamic landscape, focusing on innovation and strategic partnerships to capture market share. While the market benefits from a robust healthcare infrastructure and a high level of patient awareness, potential challenges include stringent regulatory approvals and intense competition, necessitating continuous adaptation and strategic market entry.

Japan Pharmaceutical Industry Company Market Share

This comprehensive report delves into the dynamic Japan Pharmaceutical Industry, offering in-depth analysis, market segmentation, and strategic insights from 2019 to 2033. Examining key trends, dominant segments, and emerging opportunities, this report is an essential resource for stakeholders navigating the Japanese pharmaceutical landscape.

Japan Pharmaceutical Industry Market Concentration & Innovation

The Japan Pharmaceutical Industry exhibits a moderate level of market concentration, with a mix of large multinational corporations and significant domestic players vying for market share. Innovation is primarily driven by substantial R&D investments, a highly educated workforce, and a strong emphasis on life sciences research. Key innovation drivers include advancements in biotechnology, personalized medicine, and digital health solutions. The regulatory framework, governed by the Pharmaceuticals and Medical Devices Agency (PMDA) and the Ministry of Health, Labour and Welfare (MHLH), emphasizes stringent quality control and patient safety, which can influence innovation timelines. Product substitutes, while present, are often limited by the complexity of drug development and regulatory hurdles. End-user trends indicate a growing demand for advanced therapies, preventative medicines, and treatments for an aging population. Mergers and acquisitions (M&A) activities, while not as pervasive as in some global markets, play a role in consolidating market positions and acquiring novel technologies. The total M&A deal value is estimated to be in the billions of dollars, reflecting strategic moves to expand portfolios and market reach.

Japan Pharmaceutical Industry Industry Trends & Insights

The Japan Pharmaceutical Industry is characterized by robust growth, driven by an aging population, increasing prevalence of chronic diseases, and a strong commitment to healthcare innovation. The market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 5.5% over the forecast period. Technological disruptions, such as the integration of artificial intelligence (AI) in drug discovery and development, advanced gene therapies, and novel drug delivery systems, are reshaping the industry. Consumer preferences are shifting towards more targeted and effective treatments with fewer side effects, alongside a growing interest in preventative health measures and over-the-counter (OTC) medications for minor ailments. Competitive dynamics are intensifying, with both domestic giants and international players actively seeking to expand their footprint through strategic partnerships, R&D collaborations, and market access initiatives. The penetration of innovative therapies for oncology, cardiovascular diseases, and neurological disorders continues to rise, fueling market expansion. The increasing adoption of digital health solutions and telemedicine is also influencing market penetration and patient engagement strategies, presenting a significant area for future growth and innovation within the sector.

Dominant Markets & Segments in Japan Pharmaceutical Industry

The Japanese pharmaceutical market is segmented by therapeutic categories and prescription types, with significant dominance observed in specific areas.

Therapeutic Categories:

- Cardiovascular System: This segment consistently holds a dominant position due to the high prevalence of cardiovascular diseases in Japan's aging population. Key drivers include the demand for antihypertensives, statins, and antiplatelet agents. Market size is estimated to be in the tens of billions of dollars.

- Other Therapeutic Categories: This broad category, encompassing treatments for cancer, metabolic disorders, and infectious diseases, represents another significant and growing segment. The ongoing advancements in oncology treatments and the continued need for novel antibiotics contribute to its dominance.

- Blood and Blood-forming Organs: This segment is crucial, driven by treatments for anemia, hemophilia, and other blood-related disorders.

- Respiratory System: With increasing concerns about air quality and the prevalence of respiratory illnesses, this segment sees steady demand for treatments like bronchodilators and anti-inflammatory inhalers.

- Sensory Organs: This segment, including treatments for ophthalmological and otological conditions, is expanding due to advancements in treatments for age-related eye diseases and hearing loss.

- Antiallergics: Growing awareness and the prevalence of allergies contribute to the consistent demand in this segment.

- Genito Urinary System: This segment addresses a range of conditions, with ongoing research and development contributing to its market presence.

- Dermatologicals: While a smaller segment, advancements in treating chronic skin conditions are driving growth.

Prescription Type:

- Prescription Drugs: This segment overwhelmingly dominates the Japanese pharmaceutical market, accounting for over 90% of market value. The stringent regulatory environment and the complexity of treating serious conditions necessitate physician-prescribed medications. Growth drivers include the launch of novel biologics and specialized therapies. Market size is estimated to be in the hundreds of billions of dollars.

- OTC Drugs: While a smaller segment, OTC drugs cater to self-medication needs for common ailments, showing steady growth driven by consumer demand for convenience and accessibility for minor health concerns.

Japan Pharmaceutical Industry Product Developments

Product developments in the Japan Pharmaceutical Industry are characterized by a strong focus on innovative biologics, gene therapies, and personalized medicine. Companies are investing heavily in R&D to address unmet medical needs, particularly in oncology, rare diseases, and neurodegenerative disorders. Key competitive advantages stem from cutting-edge research, robust clinical trial pipelines, and strategic collaborations with research institutions. Technological trends such as AI-driven drug discovery and advanced delivery systems are enabling the development of more targeted and effective therapies, ensuring strong market fit and significant patient benefit.

Report Scope & Segmentation Analysis

This report segments the Japan Pharmaceutical Industry by Therapeutic Category and Prescription Type. The Cardiovascular System segment is projected to maintain its leading position, driven by an aging demographic and high disease prevalence, with an estimated market size exceeding $30 Billion. The Prescription Drugs segment will continue its dominance, representing over 90% of the market value, with projected growth driven by novel drug approvals. The Other Therapeutic Categories segment, encompassing oncology and metabolic disorders, is expected to exhibit the highest growth rate due to significant R&D investments and unmet needs, with market sizes for each major category often reaching several billion dollars. The OTC Drugs segment, while smaller, is anticipated to see steady growth due to consumer demand for accessible health solutions.

Key Drivers of Japan Pharmaceutical Industry Growth

The growth of the Japan Pharmaceutical Industry is propelled by several key factors:

- Aging Population: Japan's rapidly aging demographic directly translates to an increased demand for pharmaceutical products to manage chronic age-related diseases.

- Technological Advancements: Continuous innovation in drug discovery, development, and manufacturing, including the integration of AI and biotechnology, drives the introduction of novel and effective treatments.

- Government Initiatives & Healthcare Spending: Supportive government policies aimed at promoting healthcare innovation and increased public healthcare expenditure provide a fertile ground for industry expansion.

- R&D Investment: Significant investments in research and development by both domestic and international pharmaceutical companies fuel the pipeline of new drugs and therapies.

Challenges in the Japan Pharmaceutical Industry Sector

Despite its growth, the Japan Pharmaceutical Industry faces several challenges:

- Stringent Regulatory Approval Processes: The rigorous approval pathways overseen by the PMDA can lead to longer time-to-market for new drugs.

- Price Controls and Reimbursement Policies: Government efforts to control healthcare costs can impact profit margins for pharmaceutical companies.

- Intense Competition: The presence of both established multinational corporations and innovative domestic players creates a highly competitive landscape.

- Drug Development Costs and Risks: The high cost and inherent risks associated with developing new drugs, coupled with patent expirations, pose ongoing challenges.

Emerging Opportunities in Japan Pharmaceutical Industry

The Japan Pharmaceutical Industry presents numerous emerging opportunities:

- Rare Diseases and Orphan Drugs: The unmet medical needs in rare disease treatment present a significant opportunity for specialized drug development and market penetration.

- Digital Health and Telemedicine Integration: The growing adoption of digital health solutions and telemedicine offers new avenues for patient engagement, remote monitoring, and improved healthcare delivery.

- Personalized Medicine: Advancements in genomics and diagnostics are paving the way for personalized medicine, enabling more targeted and effective treatments.

- Biologics and Biosimilars: The expanding market for biologics and the growing potential of biosimilars offer significant growth prospects.

Leading Players in the Japan Pharmaceutical Industry Market

- Sanofi SA

- Daiichi Sankyo Company Limited

- Bayer AG

- Astellas Pharma Inc

- Aspen Holdings

- Novartis International AG

- Merck & Co Inc

- Johnson and Johnson (Janssen Global Services)

- Eli Lilly and Company

- Takeda Pharmaceutical Company Limited

- Chugai Pharmaceutical Co Ltd

- Eisai Co Ltd

- Catalent Inc

- GlaxoSmithKline PLC

- Pfizer Inc

Key Developments in Japan Pharmaceutical Industry Industry

- April 2022: Takeda Pharmaceuticals received manufacturing and marketing approval from the Japan Ministry of Health, Labour and Welfare (MHLW) for Nuvaxovid Intramuscular Injection (Nuvaxovid), a novel recombinant protein-based COVID-19 vaccine for primary and booster immunization in individuals aged 18 and older.

- March 2022: Chugai Pharmaceutical Co. Ltd obtained regulatory approval from the Ministry of Health, Labour and Welfare (MHLW) of Japan for Vabysmo for Intravitreal Injection 120 mg/ mL (generic name: farcical), an anti-VEGF/anti-Ang-2 bispecific antibody for the treatment of age-related macular degeneration associated with subfoveal choroidal neovascularization and diabetic macular edema (DME).

Strategic Outlook for Japan Pharmaceutical Industry Market

The strategic outlook for the Japan Pharmaceutical Industry remains highly positive, driven by a confluence of demographic shifts, technological innovation, and a robust healthcare infrastructure. Continued investment in R&D for novel therapies, particularly in oncology and rare diseases, will be a key growth catalyst. The increasing integration of digital health solutions and personalized medicine approaches presents substantial opportunities for market expansion and improved patient outcomes. Strategic partnerships and collaborations will be crucial for navigating the competitive landscape and leveraging emerging technologies. The industry is well-positioned to address the evolving healthcare needs of Japan's population, ensuring sustained growth and a strong future market potential.

Japan Pharmaceutical Industry Segmentation

-

1. Therapeutic Category

- 1.1. Antiallergics

- 1.2. Blood and Blood-forming Organs

- 1.3. Cardiovascular System

- 1.4. Dermatologicals

- 1.5. Genito Urinary System

- 1.6. Respiratory System

- 1.7. Sensory Organs

- 1.8. Other Therapeutic Categories

-

2. Prescription Type

- 2.1. Prescription Drugs

- 2.2. OTC Drugs

Japan Pharmaceutical Industry Segmentation By Geography

- 1. Japan

Japan Pharmaceutical Industry Regional Market Share

Geographic Coverage of Japan Pharmaceutical Industry

Japan Pharmaceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.88% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 5.1.1. Antiallergics

- 5.1.2. Blood and Blood-forming Organs

- 5.1.3. Cardiovascular System

- 5.1.4. Dermatologicals

- 5.1.5. Genito Urinary System

- 5.1.6. Respiratory System

- 5.1.7. Sensory Organs

- 5.1.8. Other Therapeutic Categories

- 5.2. Market Analysis, Insights and Forecast - by Prescription Type

- 5.2.1. Prescription Drugs

- 5.2.2. OTC Drugs

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 6. Japan Pharmaceutical Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 6.1.1. Antiallergics

- 6.1.2. Blood and Blood-forming Organs

- 6.1.3. Cardiovascular System

- 6.1.4. Dermatologicals

- 6.1.5. Genito Urinary System

- 6.1.6. Respiratory System

- 6.1.7. Sensory Organs

- 6.1.8. Other Therapeutic Categories

- 6.2. Market Analysis, Insights and Forecast - by Prescription Type

- 6.2.1. Prescription Drugs

- 6.2.2. OTC Drugs

- 6.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sanofi SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Daiichi Sankyo Company Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Bayer AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Astellas Pharma Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Aspen Holdings

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Novartis International AG

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Merck & Co Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Johnson and Johnson (Janssen Global Services)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Eli Lilly and Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Takeda Pharmaceutical Company Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Chugai Pharmaceutical Co Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Eisai Co Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Catalent Inc

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 GlaxoSmithKline PLC

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Pfizer Inc

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 Sanofi SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Pharmaceutical Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Japan Pharmaceutical Industry Share (%) by Company 2025

List of Tables

- Table 1: Japan Pharmaceutical Industry Revenue Million Forecast, by Therapeutic Category 2020 & 2033

- Table 2: Japan Pharmaceutical Industry Volume K Unit Forecast, by Therapeutic Category 2020 & 2033

- Table 3: Japan Pharmaceutical Industry Revenue Million Forecast, by Prescription Type 2020 & 2033

- Table 4: Japan Pharmaceutical Industry Volume K Unit Forecast, by Prescription Type 2020 & 2033

- Table 5: Japan Pharmaceutical Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Japan Pharmaceutical Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Japan Pharmaceutical Industry Revenue Million Forecast, by Therapeutic Category 2020 & 2033

- Table 8: Japan Pharmaceutical Industry Volume K Unit Forecast, by Therapeutic Category 2020 & 2033

- Table 9: Japan Pharmaceutical Industry Revenue Million Forecast, by Prescription Type 2020 & 2033

- Table 10: Japan Pharmaceutical Industry Volume K Unit Forecast, by Prescription Type 2020 & 2033

- Table 11: Japan Pharmaceutical Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Japan Pharmaceutical Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Pharmaceutical Industry?

The projected CAGR is approximately 0.88%.

2. Which companies are prominent players in the Japan Pharmaceutical Industry?

Key companies in the market include Sanofi SA, Daiichi Sankyo Company Limited, Bayer AG, Astellas Pharma Inc, Aspen Holdings, Novartis International AG, Merck & Co Inc, Johnson and Johnson (Janssen Global Services), Eli Lilly and Company, Takeda Pharmaceutical Company Limited, Chugai Pharmaceutical Co Ltd, Eisai Co Ltd, Catalent Inc, GlaxoSmithKline PLC, Pfizer Inc.

3. What are the main segments of the Japan Pharmaceutical Industry?

The market segments include Therapeutic Category, Prescription Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 88.00 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Geriatric Population and Increasing Burden of Chronic Diseases; Increasing Research and Development Activities Along with Growing R&D Investments.

6. What are the notable trends driving market growth?

Prescription Drugs Segment is Expected to Hold a Significant Share in the Market Over Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Regulatory Scenario.

8. Can you provide examples of recent developments in the market?

In April 2022, Takeda pharmaceuticals received manufacturing and marketing approval from the Japan Ministry of Health, Labour and Welfare (MHLW) for Nuvaxovid Intramuscular Injection (Nuvaxovid), a novel recombinant protein-based COVID-19 vaccine for primary and booster immunization in individuals aged 18 and older.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Pharmaceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Pharmaceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Pharmaceutical Industry?

To stay informed about further developments, trends, and reports in the Japan Pharmaceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence