Key Insights

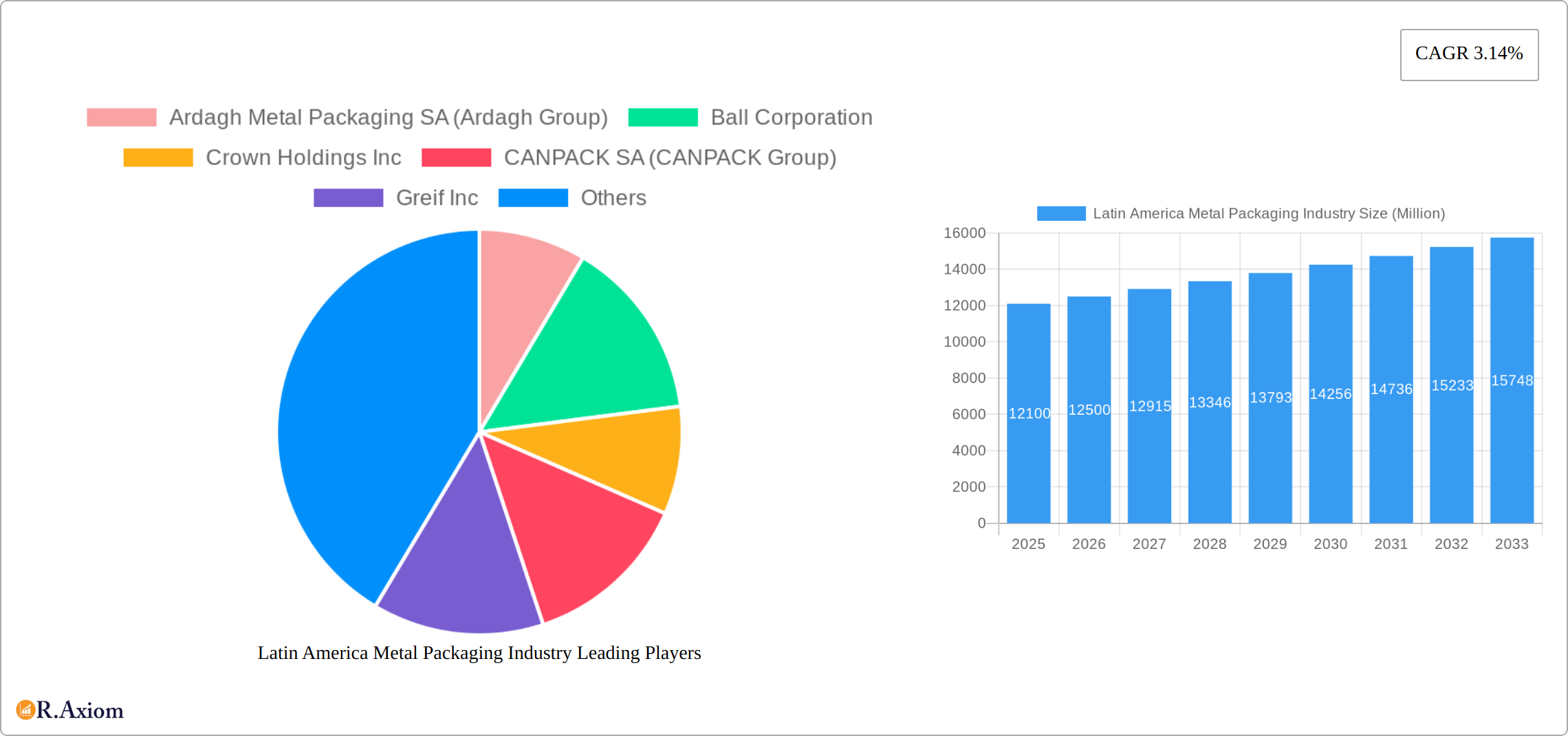

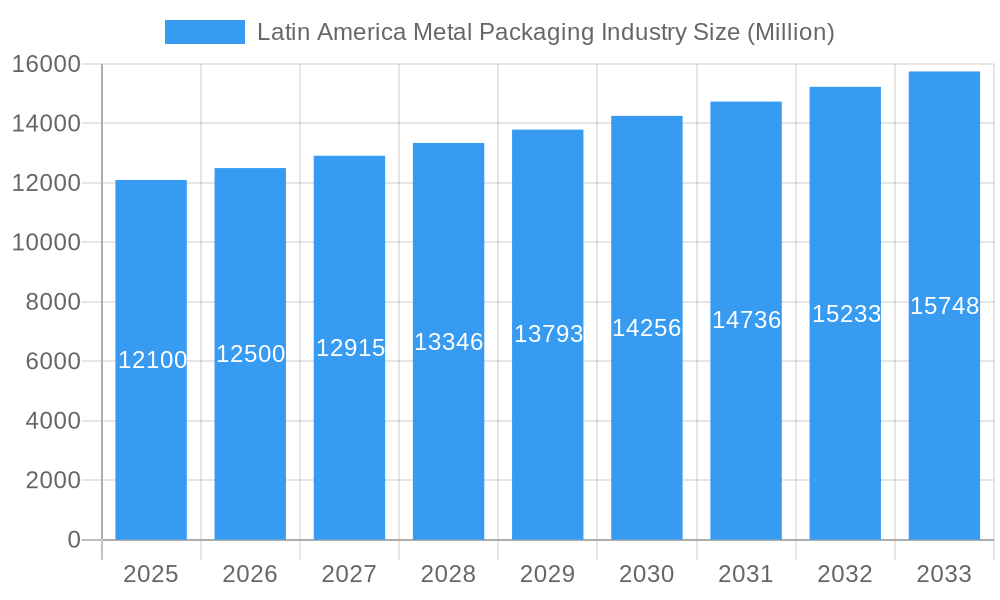

The Latin American metal packaging market, valued at $12.10 billion in 2025, is projected to experience steady growth, driven by a robust CAGR of 3.14% from 2025 to 2033. This expansion is fueled by several key factors. The rising demand for convenient and shelf-stable food and beverage products across the region is a significant driver. Increasing urbanization and a growing middle class are contributing to higher consumption levels, boosting the need for effective packaging solutions. Furthermore, the metal packaging industry's inherent sustainability advantages, such as recyclability and its ability to protect product quality, are resonating with environmentally conscious consumers and brands alike. This positive perception is further strengthened by ongoing industry efforts to improve sustainability practices. However, fluctuating raw material prices, particularly for aluminum and steel, pose a challenge to consistent growth. Economic volatility within certain Latin American countries could also impact market expansion. The market is segmented by packaging type (cans, bottles, closures, etc.) and end-use industries (food & beverage, personal care, industrial, etc.), offering further opportunities for specialized players. Companies like Ardagh Metal Packaging, Ball Corporation, and Crown Holdings Inc. are major players, actively investing in innovation and expansion within the region to capitalize on this growth potential.

Latin America Metal Packaging Industry Market Size (In Billion)

Despite challenges posed by economic fluctuations and material costs, the long-term outlook remains positive for the Latin American metal packaging market. Continued investment in advanced manufacturing techniques, coupled with a focus on sustainable packaging solutions, is expected to drive innovation. The rising popularity of e-commerce and the associated need for robust and secure packaging solutions represent an emerging growth avenue. Furthermore, government initiatives promoting sustainable packaging practices and reducing plastic waste are creating a favorable regulatory environment. Competition is expected to intensify as existing players expand their operations and new entrants explore market opportunities. However, this competition will ultimately benefit consumers by driving innovation and improving the affordability of high-quality metal packaging.

Latin America Metal Packaging Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Latin America metal packaging industry, covering market size, growth drivers, competitive landscape, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. This report is essential for industry stakeholders, investors, and businesses seeking to understand and capitalize on the opportunities within this dynamic market.

Latin America Metal Packaging Industry Market Concentration & Innovation

The Latin American metal packaging market is characterized by a dynamic and evolving landscape, with established global leaders and regional champions vying for significant market share. Key players such as Ardagh Metal Packaging SA (Ardagh Group), Ball Corporation, Crown Holdings Inc, and CANPACK SA (CANPACK Group) continue to shape the industry, alongside other notable entities like Greif Inc., Mauser Packaging Solutions, Trivium Packaging, Closure Systems International Inc (CSI), Guala Closures SpA, and Schutz GmbH & Co KGaA. While specific market share figures are detailed within comprehensive industry reports, the collective influence of these major players is substantial, indicating a market that is both competitive and consolidating. A primary driver of innovation is the escalating global and regional demand for sustainable packaging solutions. This has spurred significant investment in the development and adoption of recyclable and, increasingly, infinitely recyclable materials. Regulatory frameworks across Latin America, particularly those emphasizing environmental sustainability and waste reduction, are actively steering the industry towards eco-friendly alternatives. Beyond materials, innovation is also evident in the advancement of lightweighting technologies, which reduce material usage and transportation costs, and sophisticated printing techniques that offer enhanced branding and consumer engagement. The market is also witnessing considerable strategic M&A activity, with significant deal values reflecting consolidation efforts, the integration of cutting-edge technologies, and the expansion of operational footprints. While substitutes like plastic and glass packaging remain present, the growing consumer and regulatory preference for sustainable and circular economy-aligned options is increasingly favoring metal packaging. Furthermore, evolving end-user trends towards convenient, shelf-stable, and premium-quality packaged goods are continuously enhancing the demand for metal packaging's inherent protective and aesthetic qualities.

- Key Market Players: Ardagh Metal Packaging SA (Ardagh Group), Ball Corporation, Crown Holdings Inc, CANPACK SA (CANPACK Group), Greif Inc, Mauser Packaging Solutions, Trivium Packaging, Closure Systems International Inc (CSI), Guala Closures SpA, Schutz GmbH & Co KGaA. (List Not Exhaustive)

- Innovation Drivers: Growing consumer and regulatory demand for sustainable and infinitely recyclable packaging, advancements in lightweighting technologies for reduced environmental impact and cost efficiencies, adoption of sophisticated digital printing and coating techniques for superior branding and product protection.

- M&A Activity: The market has experienced significant strategic mergers, acquisitions, and joint ventures, with recent deal values exceeding $xx Million, reflecting consolidation, capacity expansion, and the integration of innovative technologies.

Latin America Metal Packaging Industry Industry Trends & Insights

The Latin America metal packaging market is experiencing robust growth, driven by the expanding food and beverage industry, rising consumer disposable income, and increasing demand for convenient packaging solutions. The Compound Annual Growth Rate (CAGR) during the forecast period (2025-2033) is projected to be xx%, with market penetration reaching xx% by 2033. Technological disruptions, such as the adoption of advanced manufacturing processes and automation, are enhancing efficiency and reducing production costs. Consumer preferences are shifting towards sustainable and eco-friendly packaging, creating significant opportunities for manufacturers. Competitive dynamics are characterized by intense rivalry amongst established players and the emergence of new entrants focusing on niche segments and innovative product offerings. The market is also witnessing increasing demand for customized packaging solutions tailored to meet specific brand requirements, further driving growth and innovation.

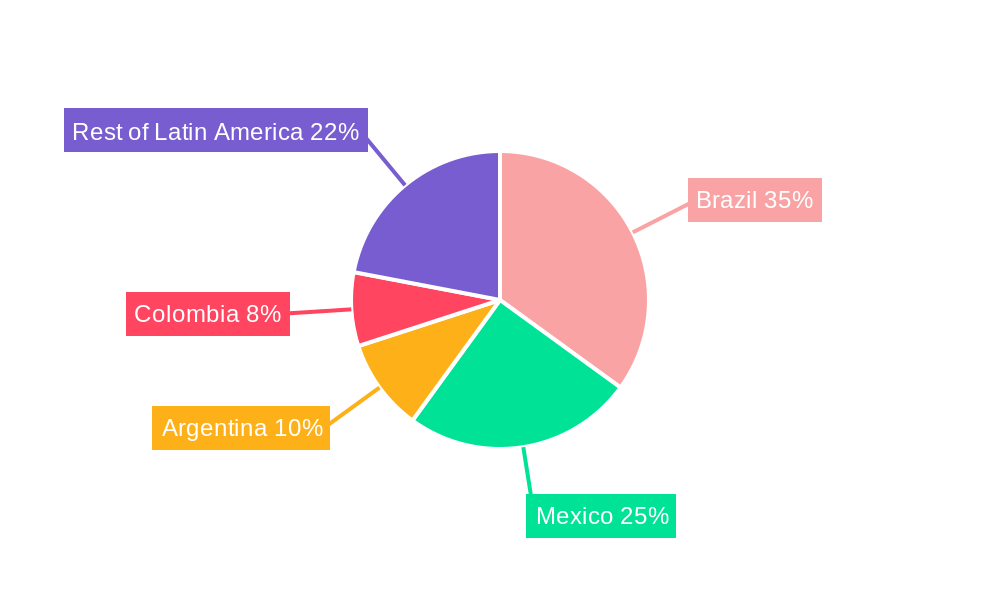

Dominant Markets & Segments in Latin America Metal Packaging Industry

Brazil and Mexico stand out as the primary powerhouses within the Latin American metal packaging market, collectively representing a significant portion of the total market value, often exceeding xx%. This leadership is underpinned by a confluence of robust economic factors and established industrial bases:

- Brazil: Benefits from a large and highly diversified economy, a substantial consumer base, a mature and expansive food & beverage industry, and a well-developed logistical and manufacturing infrastructure.

- Mexico: Its strategic proximity to the significant US market, coupled with a growing middle class and increasing demand for packaged goods across various sectors, alongside supportive government policies for manufacturing and trade, contribute to its market dominance.

Beyond these leading nations, key industry segments are experiencing notable growth. The beverage sector, particularly aluminum cans for soft drinks and beer, remains a cornerstone. Similarly, the food sector, with a rising demand for cans for ready-to-eat meals, preserved foods, and pet food, is a significant growth engine. These trends are directly fueled by increasing per capita consumption, a greater consumer preference for convenience and portability, and the inherent shelf-stability offered by metal packaging. A comprehensive industry analysis delves deeper into the granular regional and segmental performance, providing detailed insights into the specific growth catalysts for each segment, as well as identifying potential challenges that may impact future expansion.

Latin America Metal Packaging Industry Product Developments

Recent product innovations in the Latin American metal packaging sector are sharply focused on addressing environmental imperatives and evolving consumer preferences. The introduction of infinitely recyclable cans and increasingly lightweight aluminum packaging solutions are direct responses to heightened environmental consciousness and the growing demand for sustainable alternatives. These advanced products offer compelling competitive advantages, including enhanced cost-effectiveness through material reduction, superior durability and product integrity, and unparalleled branding and aesthetic appeal through advanced finishing techniques. Technological advancements are playing a pivotal role in shaping these developments. Innovations such as improved internal and external coatings are enhancing product protection against spoilage and contamination, thereby extending shelf life. Furthermore, the adoption of digital printing techniques allows for highly customized branding, variable data printing, and reduced lead times for packaging runs, catering to niche markets and promotional campaigns. A pervasive trend across product development is a commitment to lightweighting. This strategy not only reduces the overall amount of raw material required, thereby lowering production costs, but also significantly diminishes transportation expenses and the associated carbon footprint. Concurrently, research and development efforts are focused on creating novel metal alloys and composite materials that offer enhanced functionality, such as improved barrier properties or greater resistance to specific environmental conditions.

Report Scope & Segmentation Analysis

This report segments the Latin American metal packaging market based on packaging type (cans, closures, and others), material (aluminum, steel, and others), end-use industry (food and beverages, personal care, industrial, and others), and region (Brazil, Mexico, Argentina, Colombia, Chile, and Rest of Latin America). Each segment's growth projections, market sizes, and competitive dynamics are detailed in the full report. The forecast period provides a comprehensive overview of the predicted market growth within each segmented area, taking into account regional differences and their overall contribution to the total market value. Detailed competitive analysis within each segment, examining prominent players and their market share, is also available.

Key Drivers of Latin America Metal Packaging Industry Growth

Several key factors are driving the growth of the Latin America metal packaging industry. These include:

- Expanding Food & Beverage Sector: The burgeoning food and beverage sector is a significant driver, demanding increased packaging solutions.

- Rising Disposable Incomes: Growing disposable incomes are fueling demand for convenience and packaged goods.

- Government Initiatives: Supportive government policies and regulations promoting sustainable packaging are beneficial.

- Technological Advancements: Continuous technological advancements improve efficiency and product quality.

Challenges in the Latin America Metal Packaging Industry Sector

Despite the positive outlook, the Latin America metal packaging industry faces certain challenges, including:

- Fluctuating Raw Material Prices: Raw material price volatility impacts production costs and profitability.

- Supply Chain Disruptions: Global supply chain disruptions can impact the timely delivery of raw materials and finished products.

- Intense Competition: The presence of numerous players creates intense competition, affecting pricing and profitability. The impact of this competition on profit margins is reflected by a decrease of xx% over the last five years.

Emerging Opportunities in Latin America Metal Packaging Industry

Emerging opportunities lie in:

- Sustainable Packaging Solutions: Growing demand for eco-friendly packaging options opens avenues for innovation and growth.

- E-commerce Growth: The expansion of e-commerce necessitates robust and protective packaging solutions.

- Niche Market Segmentation: Targeting specific niche markets with customized packaging can lead to success.

- Technological Innovation: Investing in advanced technologies for increased efficiency, cost optimization, and superior product quality provides a competitive advantage.

Leading Players in the Latin America Metal Packaging Industry Market

- Ardagh Metal Packaging SA (Ardagh Group)

- Ball Corporation

- Crown Holdings Inc

- CANPACK SA (CANPACK Group)

- Greif Inc

- Mauser Packaging Solutions

- Trivium Packaging

- Closure Systems International Inc (CSI)

- Guala Closures SpA

- Schutz GmbH & Co KGaA (List Not Exhaustive)

Key Developments in Latin America Metal Packaging Industry Industry

- February 2024: São Geraldo partnered with CANPACK SA to launch its flagship beverage in 350 ml infinitely recyclable cans. This strategic collaboration highlights a significant industry shift towards embracing sustainable packaging solutions for mainstream consumer products.

- October 2023: Colep Packaging and Envases Group announced a joint venture aimed at constructing a new aerosol packaging plant in Mexico. This initiative represents a strategic move to expand production capacity, enhance regional market reach, and meet the growing demand for aerosol packaging in the Latin American market.

Strategic Outlook for Latin America Metal Packaging Industry Market

The Latin American metal packaging market is on a robust trajectory for significant expansion and transformation. This growth is propelled by a combination of favorable macroeconomic trends, rising consumer disposable income and demand for packaged goods, and a pronounced and accelerating industry-wide focus on sustainability. Emerging opportunities are particularly prevalent for companies that can effectively leverage the increasing consumer and corporate preference for eco-friendly and circular packaging solutions, as well as those that can deliver customized and innovative packaging designs. Strategic alliances, proactive investment in cutting-edge technologies, and calculated expansion into underserved or emerging markets will be paramount for achieving sustained success in this highly competitive and dynamic industry. The long-term outlook for the market is exceptionally strong, intrinsically linked to the continued growth and evolution of the region's vital food and beverage industry, which is projected to maintain its expansionary path in the coming years and further drive demand for versatile and sustainable metal packaging solutions.

Latin America Metal Packaging Industry Segmentation

-

1. Material Type

- 1.1. Aluminum

- 1.2. Steel

-

2. Product Type

-

2.1. Cans

- 2.1.1. Food Cans

- 2.1.2. Beverage Cans

- 2.1.3. Aerosol Cans

- 2.2. Bulk Containers

- 2.3. Shipping Barrels and Drums

- 2.4. Caps & Closures

- 2.5. Other Product Types

-

2.1. Cans

-

3. End-user Industry

- 3.1. Beverage

- 3.2. Food

- 3.3. Cosmetics & Personal Care

- 3.4. Household

- 3.5. Paints & Varnishes

- 3.6. Other End-user Industries

Latin America Metal Packaging Industry Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Metal Packaging Industry Regional Market Share

Geographic Coverage of Latin America Metal Packaging Industry

Latin America Metal Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.14% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Aluminum

- 5.1.2. Steel

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Cans

- 5.2.1.1. Food Cans

- 5.2.1.2. Beverage Cans

- 5.2.1.3. Aerosol Cans

- 5.2.2. Bulk Containers

- 5.2.3. Shipping Barrels and Drums

- 5.2.4. Caps & Closures

- 5.2.5. Other Product Types

- 5.2.1. Cans

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Beverage

- 5.3.2. Food

- 5.3.3. Cosmetics & Personal Care

- 5.3.4. Household

- 5.3.5. Paints & Varnishes

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Latin America Metal Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Aluminum

- 6.1.2. Steel

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Cans

- 6.2.1.1. Food Cans

- 6.2.1.2. Beverage Cans

- 6.2.1.3. Aerosol Cans

- 6.2.2. Bulk Containers

- 6.2.3. Shipping Barrels and Drums

- 6.2.4. Caps & Closures

- 6.2.5. Other Product Types

- 6.2.1. Cans

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Beverage

- 6.3.2. Food

- 6.3.3. Cosmetics & Personal Care

- 6.3.4. Household

- 6.3.5. Paints & Varnishes

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ardagh Metal Packaging SA (Ardagh Group)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Ball Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Crown Holdings Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 CANPACK SA (CANPACK Group)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Greif Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mauser Packaging Solutions

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Trivium Packaging

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Closure Systems International Inc (CSI)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Guala Closures SpA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Schutz GmbH & Co KGaA*List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Ardagh Metal Packaging SA (Ardagh Group)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America Metal Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Latin America Metal Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Metal Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Latin America Metal Packaging Industry Volume Billion Forecast, by Material Type 2020 & 2033

- Table 3: Latin America Metal Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 4: Latin America Metal Packaging Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 5: Latin America Metal Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Latin America Metal Packaging Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 7: Latin America Metal Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Latin America Metal Packaging Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Latin America Metal Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 10: Latin America Metal Packaging Industry Volume Billion Forecast, by Material Type 2020 & 2033

- Table 11: Latin America Metal Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 12: Latin America Metal Packaging Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 13: Latin America Metal Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Latin America Metal Packaging Industry Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Latin America Metal Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Latin America Metal Packaging Industry Volume Billion Forecast, by Country 2020 & 2033

- Table 17: Brazil Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Brazil Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Argentina Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Argentina Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: Chile Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Chile Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: Colombia Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Colombia Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Mexico Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Mexico Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: Peru Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Peru Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Venezuela Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Venezuela Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Ecuador Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Ecuador Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Bolivia Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Bolivia Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

- Table 35: Paraguay Latin America Metal Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Paraguay Latin America Metal Packaging Industry Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Metal Packaging Industry?

The projected CAGR is approximately 3.14%.

2. Which companies are prominent players in the Latin America Metal Packaging Industry?

Key companies in the market include Ardagh Metal Packaging SA (Ardagh Group), Ball Corporation, Crown Holdings Inc, CANPACK SA (CANPACK Group), Greif Inc, Mauser Packaging Solutions, Trivium Packaging, Closure Systems International Inc (CSI), Guala Closures SpA, Schutz GmbH & Co KGaA*List Not Exhaustive.

3. What are the main segments of the Latin America Metal Packaging Industry?

The market segments include Material Type, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.10 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increasing Beverage Consumption in Brazil Driving Sales of Metal Packaging Solutions.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

February 2024: São Geraldo announced its partnership with CANPACK SA to launch its flagship beverage in 350 ml infinitely recyclable cans. São Geraldo included cans as a packaging solution for its cashew fruit-flavor drink, which was previously only available in PET or glass bottles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Metal Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Metal Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Metal Packaging Industry?

To stay informed about further developments, trends, and reports in the Latin America Metal Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence