Key Insights

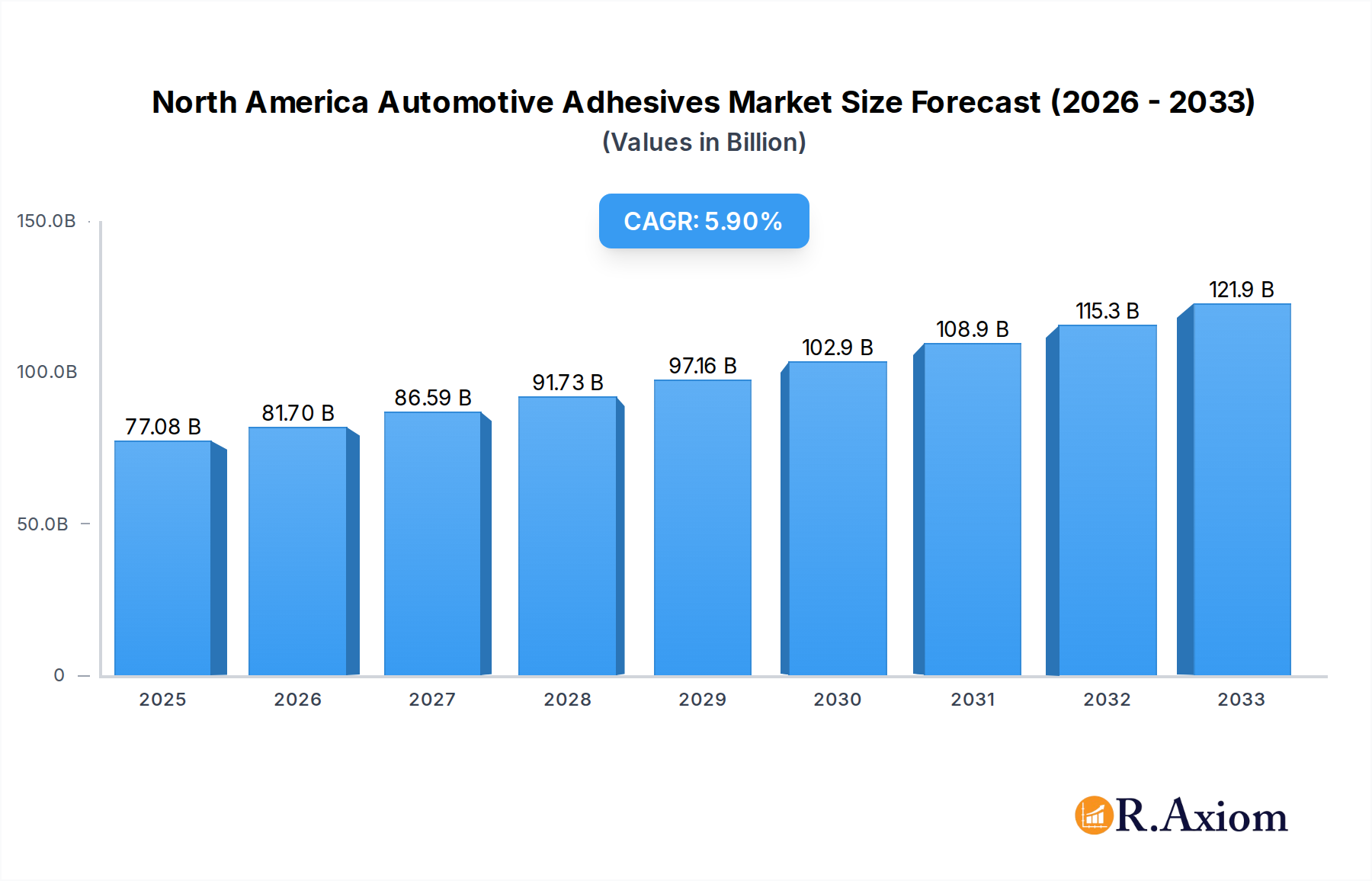

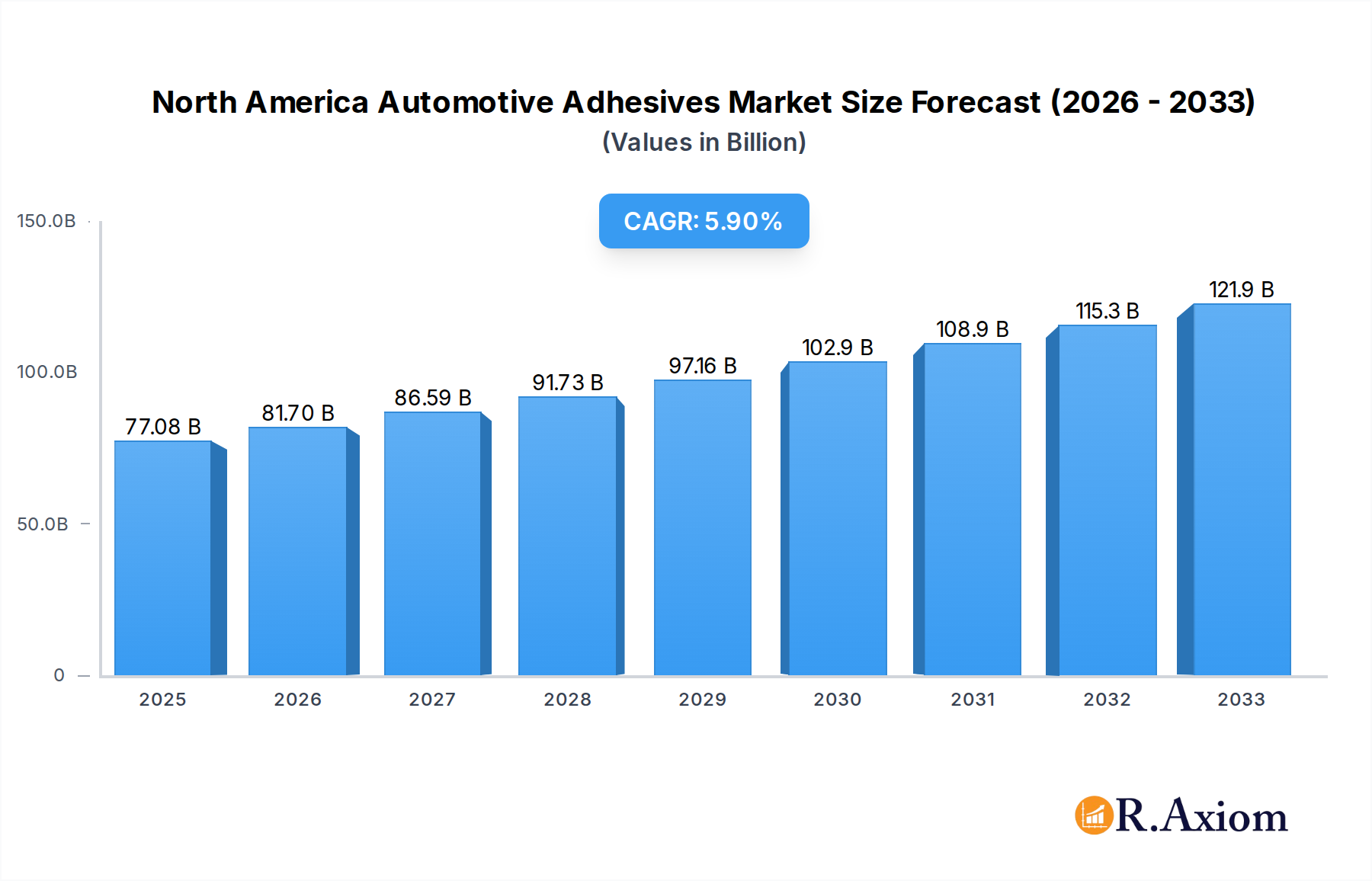

The North America Automotive Adhesives & Sealants Market is poised for robust expansion, projected to reach approximately USD 77.08 billion by 2025. This growth is underpinned by a healthy Compound Annual Growth Rate (CAGR) of 6%, indicating sustained demand and innovation within the sector. Several key drivers are fueling this upward trajectory. The increasing sophistication of vehicle design, which often incorporates lighter materials like aluminum and composites to enhance fuel efficiency and performance, necessitates advanced bonding solutions. Furthermore, stringent automotive safety regulations worldwide are driving the adoption of high-strength adhesives and sealants for structural integrity and occupant protection. The burgeoning electric vehicle (EV) market also presents a significant opportunity, as EVs often require specialized adhesives for battery pack assembly, thermal management, and lightweighting initiatives. Emerging trends such as the development of sustainable and environmentally friendly adhesive formulations, along with advancements in smart adhesives with sensing capabilities, are also shaping the market landscape. The demand for improved NVH (Noise, Vibration, and Harshness) reduction in vehicles further stimulates the market for specialized sealants.

North America Automotive Adhesives & Sealants Market Market Size (In Billion)

Despite the promising growth, certain restraints may influence the market dynamics. Fluctuations in raw material prices, particularly for petrochemical-based inputs, can impact manufacturing costs and profit margins. The initial investment in advanced adhesive application technologies and the need for skilled labor can also pose challenges for some manufacturers. However, the overarching trend is towards greater integration and specialization. The market is segmented by resin types, with Acrylic, Epoxy, and Polyurethane resins being prominent due to their versatile properties and applications in automotive assembly. Technology-wise, Hot Melt and Reactive adhesives are widely adopted for their efficiency and bonding strength, while UV Cured and Water-borne technologies are gaining traction due to their environmental benefits. Leading companies such as Henkel AG & Co KGaA, 3M, and Illinois Tool Works Inc. are at the forefront, driving innovation and catering to the evolving needs of the North American automotive industry, which includes the United States, Canada, and Mexico.

North America Automotive Adhesives & Sealants Market Company Market Share

This comprehensive market research report provides an in-depth analysis of the North America Automotive Adhesives & Sealants Market, meticulously examining historical trends, current market dynamics, and future projections. Spanning the study period from 2019 to 2033, with a base year of 2025, this report offers actionable insights for industry stakeholders, including manufacturers, suppliers, investors, and automotive OEMs. Our analysis delves into the intricate landscape of resins, technologies, and key market developments, providing a robust understanding of growth drivers, challenges, and emerging opportunities. The North America Automotive Adhesives & Sealants Market is projected to reach significant valuations, driven by evolving automotive manufacturing processes, the increasing demand for lightweighting, and advancements in vehicle safety and performance.

North America Automotive Adhesives & Sealants Market Market Concentration & Innovation

The North America Automotive Adhesives & Sealants Market exhibits a moderate to high degree of market concentration, with a few key players dominating significant market share. Innovation is a critical differentiator, fueled by the relentless pursuit of enhanced performance, reduced environmental impact, and improved manufacturing efficiency in the automotive sector. Key innovation drivers include the development of advanced adhesives for electric vehicle (EV) battery assembly, structural bonding for lightweighting, and high-strength sealants for improved NVH (Noise, Vibration, and Harshness) reduction. Regulatory frameworks, such as those concerning volatile organic compound (VOC) emissions and recyclability, are increasingly shaping product development and market entry strategies. Product substitutes, while present, often struggle to match the specialized performance characteristics offered by advanced adhesives and sealants in demanding automotive applications. End-user trends, particularly the shift towards EVs and autonomous driving technologies, are creating new application demands and driving innovation. Mergers and acquisitions (M&A) are significant strategic moves within the industry, with recent activities indicating consolidation and a drive to acquire specialized technologies and market access. For instance, the acquisition of Ashland's Performance Adhesives business by Arkema Group in February 2022 highlights this trend, strengthening Arkema's position in high-performance adhesives within the North American market. The market anticipates continued M&A activity as companies seek to expand their portfolios and global reach.

North America Automotive Adhesives & Sealants Market Industry Trends & Insights

The North America Automotive Adhesives & Sealants Market is experiencing robust growth, projected to achieve a substantial Compound Annual Growth Rate (CAGR) between 2025 and 2033. This expansion is primarily propelled by the increasing sophistication of automotive manufacturing, the imperative for vehicle lightweighting to improve fuel efficiency and EV range, and the growing demand for enhanced safety and durability features. Technological disruptions are at the forefront, with significant advancements in reactive adhesives, UV-cured technologies, and water-borne formulations offering superior performance characteristics and reduced environmental footprints. The burgeoning electric vehicle segment represents a significant market penetration opportunity, requiring specialized adhesives for battery pack assembly, thermal management, and structural integrity. Consumer preferences are evolving, with a heightened focus on vehicle acoustics, interior comfort, and advanced driver-assistance systems (ADAS), all of which rely heavily on effective sealing and bonding solutions. Competitive dynamics are intense, characterized by innovation-driven product development, strategic partnerships, and the ongoing consolidation of market players. The market is witnessing a shift towards sustainable and eco-friendly adhesive and sealant solutions, aligning with global environmental mandates and consumer consciousness. The increasing complexity of vehicle designs, integration of diverse materials (e.g., composites, aluminum, high-strength steels), and the demand for faster assembly times are further solidifying the indispensable role of automotive adhesives and sealants.

Dominant Markets & Segments in North America Automotive Adhesives & Sealants Market

The United States stands as the dominant market within the North America Automotive Adhesives & Sealants Market. This supremacy is attributed to its large automotive manufacturing base, extensive research and development infrastructure, and a strong adoption rate of advanced automotive technologies, including electric vehicles. Economically, the robust automotive industry in the US, coupled with supportive government initiatives aimed at promoting domestic manufacturing and technological innovation, significantly bolsters the demand for high-performance adhesives and sealants.

Key Drivers of Dominance:

- Automotive Manufacturing Hub: The presence of major automotive OEMs and Tier-1 suppliers facilitates a consistent and high volume of demand.

- Technological Advancement: Leading research institutions and corporate R&D centers drive innovation in adhesive and sealant formulations.

- EV Adoption: The US is a key market for electric vehicle sales and manufacturing, creating a unique demand for specialized battery adhesives and thermal management solutions.

- Regulatory Support: While regulations exist, supportive frameworks for advanced manufacturing and sustainability initiatives indirectly benefit the adhesive and sealant market.

- Infrastructure Investment: Investments in automotive manufacturing facilities and the broader industrial ecosystem contribute to sustained demand.

Within the Resin segment, Polyurethane adhesives and sealants are expected to hold a dominant position. Their versatility, excellent adhesion to a wide range of substrates, flexibility, and durability make them indispensable for structural bonding, sealing, and vibration dampening applications in vehicles. The increasing use of mixed materials in automotive construction further amplifies the demand for polyurethane-based solutions.

Key Drivers of Dominance (Polyurethane Resin):

- Structural Integrity: Superior tensile strength and flexibility make them ideal for body-in-white applications and crash performance.

- Versatile Adhesion: Bonds well with metals, plastics, composites, and glass, crucial for multi-material vehicles.

- NVH Reduction: Effective in sealing and dampening vibrations, enhancing passenger comfort.

- Weatherability & Durability: Withstands extreme temperatures and environmental conditions, ensuring long-term performance.

- Cost-Effectiveness: Offers a balance of performance and cost for large-scale automotive manufacturing.

In terms of Technology, Reactive Adhesives are projected to lead the market. This category encompasses a broad range of technologies, including epoxies, polyurethanes, and cyanoacrylates, which undergo chemical reactions to cure and form strong, permanent bonds. Their ability to provide high strength, durability, and resistance to challenging environments makes them critical for structural applications, contributing significantly to vehicle safety and performance.

Key Drivers of Dominance (Reactive Adhesives):

- High Strength & Durability: Essential for critical structural components and impact resistance.

- Chemical Resistance: Withstands automotive fluids, fuels, and environmental contaminants.

- Temperature Stability: Maintains performance across a wide range of operating temperatures.

- Reduced Fasteners: Enables the replacement of mechanical fasteners, contributing to weight reduction and design flexibility.

- Wide Application Range: Suitable for bonding dissimilar materials and complex assemblies.

North America Automotive Adhesives & Sealants Market Product Developments

Product innovations in the North America Automotive Adhesives & Sealants Market are characterized by a focus on enhancing performance, sustainability, and manufacturing efficiency. Key developments include the introduction of advanced structural adhesives with faster curing times and superior mechanical properties, enabling lighter and safer vehicle designs. The growing demand for electric vehicles is driving the development of specialized adhesives for battery pack assembly, thermal management, and lightweight component bonding. Furthermore, there is a significant push towards environmentally friendly formulations, such as low-VOC and water-borne adhesives, aligning with stringent environmental regulations and growing consumer preference for sustainable products. These innovations offer competitive advantages by improving manufacturing throughput, reducing assembly costs, and enabling automakers to meet evolving performance and regulatory demands.

Report Scope & Segmentation Analysis

The North America Automotive Adhesives & Sealants Market is segmented across a comprehensive range of resin types and adhesive technologies. The Resin segmentation includes Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, and Other Resins. Each resin type offers distinct properties tailored for specific automotive applications, such as structural bonding, sealing, gasketing, and interior trim assembly. The Technology segmentation encompasses Hot Melt, Reactive, Sealants, Solvent-borne, UV Cured Adhesives, and Water-borne technologies. This segmentation highlights the diverse curing mechanisms and application methods employed, from rapid UV curing for precision applications to robust reactive systems for structural integrity. Market sizes and growth projections for each segment are analyzed to provide a granular understanding of market dynamics and future potential.

Key Drivers of North America Automotive Adhesives & Sealants Market Growth

The growth of the North America Automotive Adhesives & Sealants Market is propelled by several key drivers. The increasing demand for lightweight vehicles to enhance fuel efficiency and extend EV range is a primary catalyst, promoting the use of adhesives in structural bonding and panel assembly. Technological advancements, such as the development of high-strength, temperature-resistant adhesives for EV battery systems, are crucial. Furthermore, stringent safety regulations and the pursuit of improved vehicle performance, including enhanced NVH reduction and crashworthiness, necessitate advanced sealing and bonding solutions. The growing adoption of electric vehicles and the trend towards autonomous driving also create new application opportunities.

Challenges in the North America Automotive Adhesives & Sealants Market Sector

Despite robust growth, the North America Automotive Adhesives & Sealants Market faces several challenges. Stringent environmental regulations regarding VOC emissions and the recyclability of materials can increase development costs and complexity. Fluctuations in raw material prices and supply chain disruptions can impact profitability and product availability. The high capital investment required for R&D and manufacturing facilities presents a barrier to entry for new players. Moreover, the intense competition among established players and the constant need for innovation to keep pace with evolving automotive technologies pose significant challenges. The development of specialized adhesives for new material combinations and complex vehicle architectures also requires substantial technical expertise and investment.

Emerging Opportunities in North America Automotive Adhesives & Sealants Market

Emerging opportunities in the North America Automotive Adhesives & Sealants Market are largely driven by the rapid evolution of the automotive industry. The substantial growth in the electric vehicle sector presents a significant opportunity for specialized adhesives used in battery assembly, thermal management, and lightweighting components. The increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies creates demand for sophisticated sensor bonding and integration solutions. Furthermore, the trend towards multimodal manufacturing, incorporating a wider range of materials like advanced composites and high-strength steels, opens avenues for novel adhesive formulations with enhanced compatibility and performance. The increasing focus on sustainability also drives opportunities for bio-based and recyclable adhesive solutions.

Leading Players in the North America Automotive Adhesives & Sealants Market Market

- Henkel AG & Co KGaA

- 3M

- Illinois Tool Works Inc

- Arkema Group

- Huntsman International LLC

- DuPont

- Dow

- H B Fuller Company

- Sika AG

- AVERY DENNISON CORPORATION

Key Developments in North America Automotive Adhesives & Sealants Market Industry

- April 2022: ITW Performance Polymers launched Plexus MA8105, a new adhesive offering fast room-temperature curing, excellent mechanical properties, and broad adhesion capabilities.

- February 2022: Arkema Group finalized the acquisition of Ashland's Performance Adhesives business, a recognized leader in high-performance adhesives in the United States.

- January 2022: DuPont Interconnect Solutions announced the completion of an expansion project at its Circleville, Ohio, manufacturing site, aimed at increasing the production of Kapton® polyimide film and Pyralux® flexible circuit materials to meet rising global demand across various industries, including automotive.

Strategic Outlook for North America Automotive Adhesives & Sealants Market Market

The strategic outlook for the North America Automotive Adhesives & Sealants Market is exceptionally promising, driven by continuous innovation and the transformative shifts within the automotive sector. The escalating demand for electric vehicles is a significant growth catalyst, necessitating advanced adhesive solutions for battery integration, thermal management, and structural integrity. The ongoing trend towards lightweighting vehicles for improved efficiency and range will further boost the adoption of structural adhesives. Industry players are strategically focusing on developing sustainable and eco-friendly adhesive formulations to meet evolving environmental regulations and consumer preferences. Mergers and acquisitions are anticipated to play a crucial role in consolidating market share, acquiring new technologies, and expanding geographical reach. The integration of smart technologies and advanced manufacturing processes within the automotive industry will also create new opportunities for specialized adhesives and sealants with enhanced functionalities.

North America Automotive Adhesives & Sealants Market Segmentation

-

1. Resin

- 1.1. Acrylic

- 1.2. Cyanoacrylate

- 1.3. Epoxy

- 1.4. Polyurethane

- 1.5. Silicone

- 1.6. VAE/EVA

- 1.7. Other Resins

-

2. Technology

- 2.1. Hot Melt

- 2.2. Reactive

- 2.3. Sealants

- 2.4. Solvent-borne

- 2.5. UV Cured Adhesives

- 2.6. Water-borne

North America Automotive Adhesives & Sealants Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

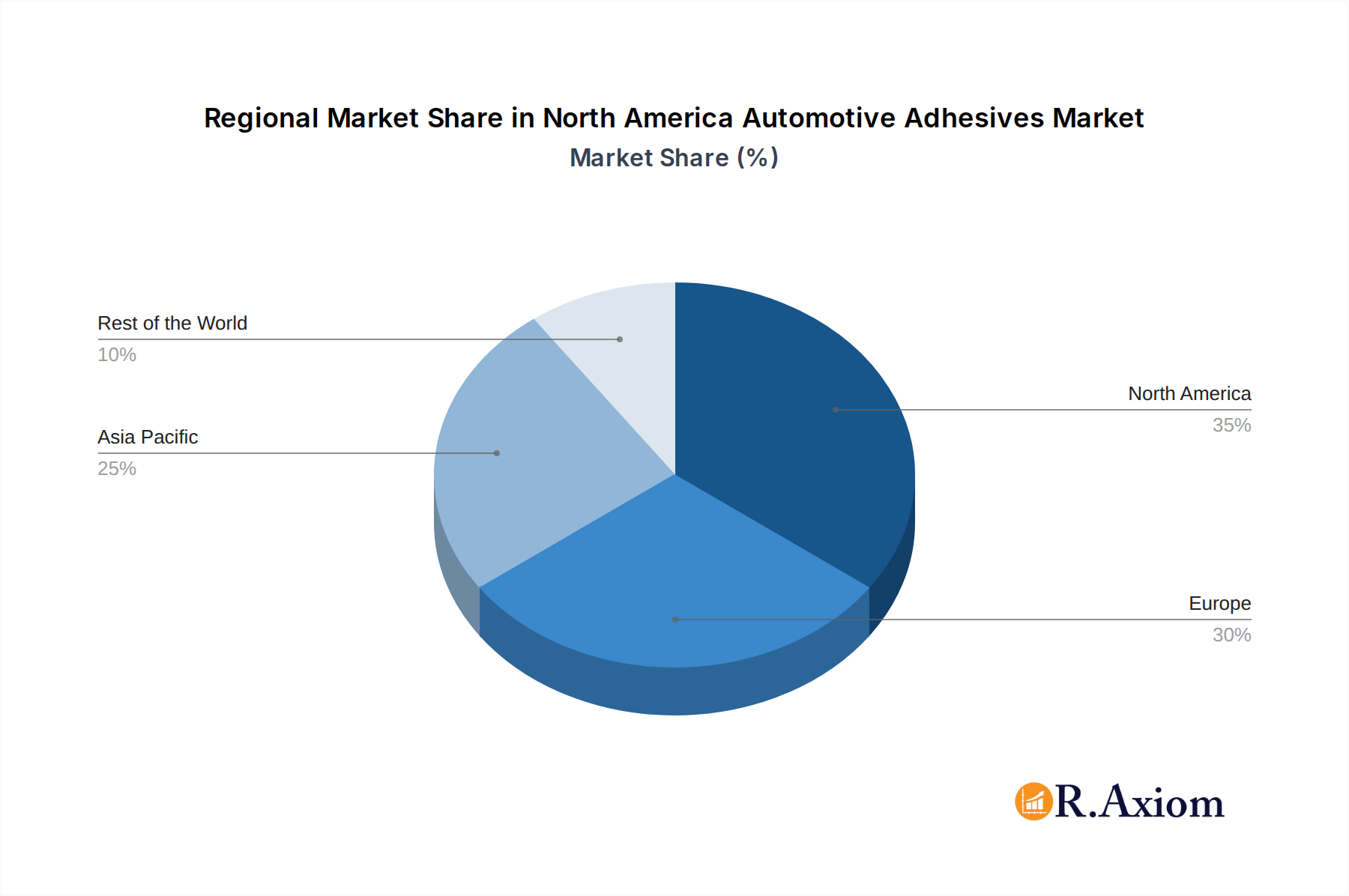

North America Automotive Adhesives & Sealants Market Regional Market Share

Geographic Coverage of North America Automotive Adhesives & Sealants Market

North America Automotive Adhesives & Sealants Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Acrylic

- 5.1.2. Cyanoacrylate

- 5.1.3. Epoxy

- 5.1.4. Polyurethane

- 5.1.5. Silicone

- 5.1.6. VAE/EVA

- 5.1.7. Other Resins

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Hot Melt

- 5.2.2. Reactive

- 5.2.3. Sealants

- 5.2.4. Solvent-borne

- 5.2.5. UV Cured Adhesives

- 5.2.6. Water-borne

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. North America Automotive Adhesives & Sealants Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 6.1.1. Acrylic

- 6.1.2. Cyanoacrylate

- 6.1.3. Epoxy

- 6.1.4. Polyurethane

- 6.1.5. Silicone

- 6.1.6. VAE/EVA

- 6.1.7. Other Resins

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Hot Melt

- 6.2.2. Reactive

- 6.2.3. Sealants

- 6.2.4. Solvent-borne

- 6.2.5. UV Cured Adhesives

- 6.2.6. Water-borne

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Henkel AG & Co KGaA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 3M

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Illinois Tool Works Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Arkema Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Huntsman International LLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 DuPont

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Dow

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 H B Fuller Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sika A

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 AVERY DENNISON CORPORATION

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Henkel AG & Co KGaA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Automotive Adhesives & Sealants Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Automotive Adhesives & Sealants Market Share (%) by Company 2025

List of Tables

- Table 1: North America Automotive Adhesives & Sealants Market Revenue billion Forecast, by Resin 2020 & 2033

- Table 2: North America Automotive Adhesives & Sealants Market Revenue billion Forecast, by Technology 2020 & 2033

- Table 3: North America Automotive Adhesives & Sealants Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: North America Automotive Adhesives & Sealants Market Revenue billion Forecast, by Resin 2020 & 2033

- Table 5: North America Automotive Adhesives & Sealants Market Revenue billion Forecast, by Technology 2020 & 2033

- Table 6: North America Automotive Adhesives & Sealants Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States North America Automotive Adhesives & Sealants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Automotive Adhesives & Sealants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Automotive Adhesives & Sealants Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Adhesives & Sealants Market?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the North America Automotive Adhesives & Sealants Market?

Key companies in the market include Henkel AG & Co KGaA, 3M, Illinois Tool Works Inc, Arkema Group, Huntsman International LLC, DuPont, Dow, H B Fuller Company, Sika A, AVERY DENNISON CORPORATION.

3. What are the main segments of the North America Automotive Adhesives & Sealants Market?

The market segments include Resin, Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 77.08 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand from the Construction Industry in Saudi Arabia; Other Drivers.

6. What are the notable trends driving market growth?

Growing trend of 'bonding instead of welding' to significantly contribute to the demand for automotive adhesives.

7. Are there any restraints impacting market growth?

; Impact of COVID-19 Pandemic on Global Economy.

8. Can you provide examples of recent developments in the market?

April 2022: ITW Performance Polymers launched Plexus MA8105 as its newest adhesive with fast room-temperature curing, excellent mechanical properties, and a broad range of adhesion.February 2022: Arkema Group completed the acquisition of Ashland's Performance Adhesives business. Ashland is a world leader in high-performance adhesives in the United States.January 2022: DuPont Interconnect Solutions, a business within the Electronics & Industrial segment, announced the completion of the expansion project at its Circleville, Ohio, manufacturing site. This completion is expected to expand the production of Kapton® polyimide film and Pyralux® flexible circuit materials to meet the growing global demand in the automotive, consumer electronics, telecom, specialized industrial, and defense industries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Adhesives & Sealants Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Adhesives & Sealants Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Adhesives & Sealants Market?

To stay informed about further developments, trends, and reports in the North America Automotive Adhesives & Sealants Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence