Key Insights

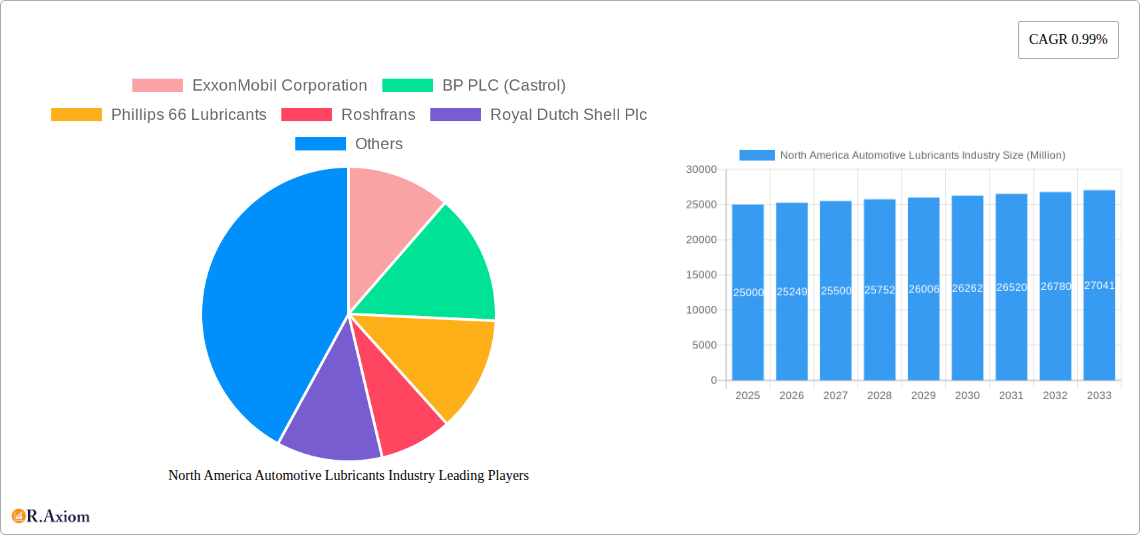

The North American automotive lubricants market, valued at approximately $25 billion in 2025, is projected to experience steady growth, driven by increasing vehicle ownership, particularly in the passenger vehicle segment, and the expanding commercial fleet in the region. The market's Compound Annual Growth Rate (CAGR) of 0.99% from 2019-2024 suggests a relatively stable, mature market. However, several factors will influence future growth. The rising adoption of fuel-efficient vehicles and electric vehicles (EVs) presents a significant challenge, as the demand for traditional lubricants will likely decrease. Conversely, the growth of hybrid vehicles introduces new lubricant needs, creating opportunities for specialized products. Furthermore, stringent environmental regulations concerning lubricant composition and disposal are prompting manufacturers to invest in research and development of sustainable and eco-friendly lubricants. This includes bio-based lubricants and lubricants designed to improve fuel efficiency, contributing to a more sustainable automotive sector. The market is segmented by vehicle type (commercial vehicles, motorcycles, passenger vehicles) and product type (engine oils, greases, hydraulic fluids, transmission & gear oils), with engine oils currently holding the largest market share. Key players like ExxonMobil, BP, Shell, and Chevron dominate the market, leveraging their established distribution networks and strong brand recognition. Competition is intensifying with the emergence of smaller, specialized lubricant manufacturers focusing on niche segments, such as high-performance lubricants and environmentally friendly alternatives.

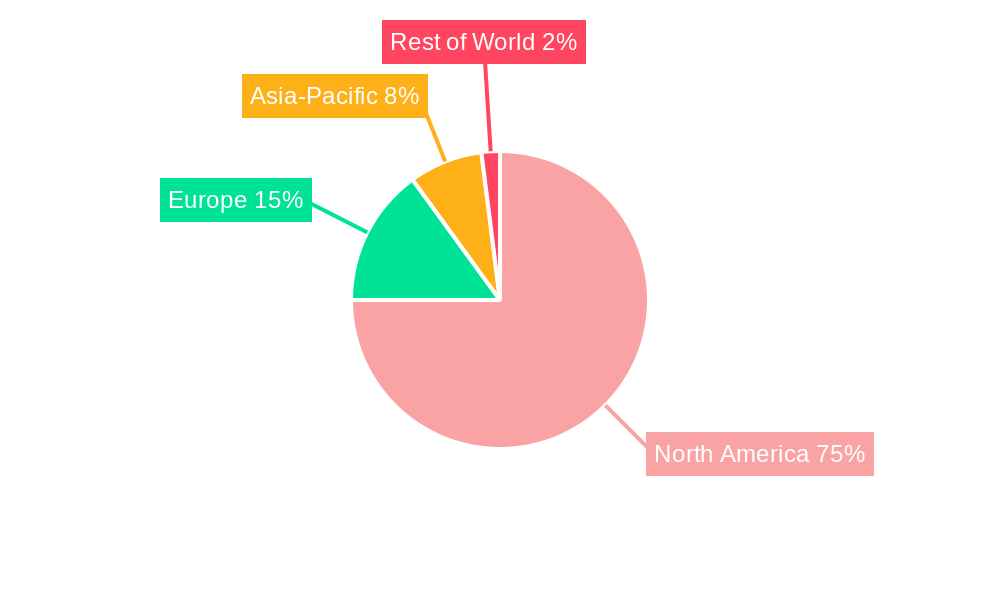

The geographic distribution within North America shows the United States holding the largest market share due to its large automotive sector and higher vehicle density. Canada and Mexico exhibit promising growth potential driven by infrastructure development and the expanding automotive industry in these countries. The forecast period (2025-2033) will likely see continued consolidation among major players, increased focus on product innovation, and a gradual shift toward sustainable and eco-friendly lubricant solutions. Maintaining robust supply chains and effectively navigating evolving environmental regulations will be crucial for success in this competitive market.

North America Automotive Lubricants Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the North America automotive lubricants industry, covering the period 2019-2033. With a base year of 2025 and a forecast period extending to 2033, this study offers invaluable insights for industry stakeholders, investors, and businesses seeking to navigate this dynamic market. The report leverages extensive data analysis, including market sizing, segmentation, competitive landscape, and future growth projections, all expressed in Millions.

North America Automotive Lubricants Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the North American automotive lubricants market, examining market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and M&A activities. The market is characterized by a moderately concentrated structure with key players holding significant market share. ExxonMobil, BP (Castrol), Shell, and Chevron collectively account for approximately xx% of the market, indicating a high level of consolidation. However, smaller players like Valvoline and AMSOIL are also significant contributors, focusing on niche segments or specialized products.

- Market Share: ExxonMobil holds approximately xx% market share, followed by BP (Castrol) at xx%, Shell at xx%, and Chevron at xx%. The remaining share is distributed among other players, including Phillips 66, TotalEnergies, and smaller independent players.

- Innovation Drivers: Stringent emission regulations, the rising demand for fuel-efficient vehicles, and growing focus on environmental sustainability are pushing innovation towards low-viscosity oils and eco-friendly formulations.

- Regulatory Frameworks: Regulations concerning lubricant composition, disposal, and environmental impact play a crucial role in shaping industry practices and influencing product development. Compliance costs are a key challenge for many players.

- Product Substitutes: The emergence of electric and hybrid vehicles presents a potential threat, as they require different types of lubricants or reduced lubricant volumes. The market is adapting to this trend by developing specialized lubricants for electric vehicles.

- End-User Trends: The preference for longer drain intervals and higher-performance lubricants is increasing. Consumers are also increasingly aware of the environmental impact of lubricants and are demanding sustainable options.

- M&A Activities: The industry has witnessed several mergers and acquisitions in recent years, driven by the desire to expand market reach, access new technologies, and achieve economies of scale. While precise deal values are commercially sensitive, significant activity has focused on bolstering distribution networks and strengthening technology portfolios. For example, the xx Million deal between [Company A] and [Company B] in [Year] is notable.

North America Automotive Lubricants Industry Industry Trends & Insights

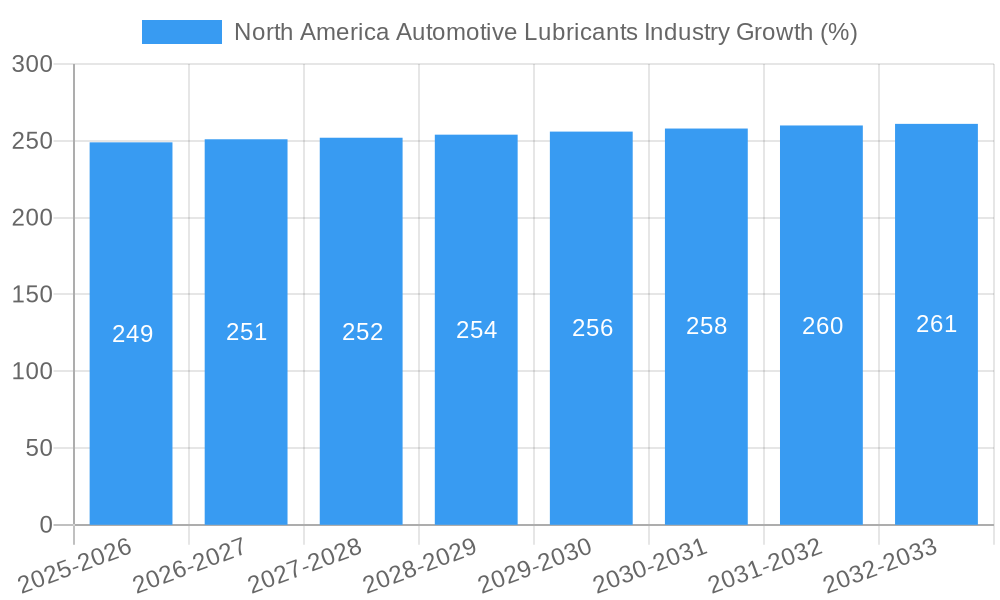

The North American automotive lubricants market is experiencing steady growth driven by factors such as the increasing number of vehicles on the road, rising demand from the commercial vehicle sector, and continuous advancements in lubricant technology. The market witnessed a CAGR of xx% during the historical period (2019-2024) and is projected to grow at a CAGR of xx% during the forecast period (2025-2033).

Several key trends are shaping the industry's trajectory:

- Market Growth Drivers: The expansion of the automotive industry, especially in the commercial vehicle segment, is a major driver. Rising disposable incomes and infrastructure development are further fueling demand.

- Technological Disruptions: Advancements in lubricant formulation, particularly in low-viscosity and synthetic oils, are enhancing engine performance and efficiency. The adoption of additive technologies that enhance fuel economy and reduce emissions is also on the rise. The market penetration of fully synthetic oils is increasing rapidly, reaching approximately xx% in 2024 and expected to reach xx% by 2033.

- Consumer Preferences: Consumers are increasingly prioritizing performance, longer drain intervals, and environmentally friendly options. This is driving the demand for high-performance synthetic lubricants and eco-friendly formulations.

- Competitive Dynamics: The market is characterized by intense competition among major players, leading to price wars and a focus on product differentiation and innovation. The entry of new players specializing in niche segments also adds to the competitive pressure.

Dominant Markets & Segments in North America Automotive Lubricants Industry

The United States remains the dominant market in North America, accounting for approximately xx% of the total market volume in 2024. However, Canada and Mexico are also exhibiting significant growth, driven by their respective automotive sectors. The passenger vehicle segment currently holds the largest market share by vehicle type, but commercial vehicles are displaying higher growth rates. Within product types, engine oils dominate, accounting for over xx% of the market, although the demand for specialized lubricants such as greases and transmission fluids is also expanding.

- By Vehicle Type:

- Passenger Vehicles: Dominated by the large consumer base and high vehicle density in the US. Growth is linked to new vehicle sales and aftermarket replacements.

- Commercial Vehicles: Strong growth driven by the increase in freight transportation and logistics, infrastructure projects, and stricter emission norms.

- Motorcycles: A smaller segment, but with growing demand from leisure activities and rising affordability.

- By Product Type:

- Engine Oils: The largest segment due to their necessity for all vehicle types, with the continued adoption of advanced formulations and the demand for longer drain intervals.

- Greases: Essential for various automotive components, with growth driven by advancements in grease technology and increasing application in commercial vehicles.

- Hydraulic Fluids: Used in power steering and other hydraulic systems. Market growth is tied to new vehicle production and the aftermarket.

- Transmission & Gear Oils: Crucial for smooth transmission operation. Growth is driven by increasing demand from automatic transmission vehicles.

- By Country:

- United States: Largest market, driven by high vehicle ownership rates, robust automotive manufacturing, and a well-established aftermarket.

- Canada: Moderate growth, influenced by factors like economic conditions and government policies related to automotive manufacturing and fuel efficiency.

- Mexico: Relatively high growth rate driven by foreign direct investment in the automotive industry, and increasing vehicle production for export.

- Rest of North America: A smaller segment with moderate growth potential, driven mainly by the growth of the automotive sector in these countries.

North America Automotive Lubricants Industry Product Developments

The industry is witnessing significant innovation in lubricant technology. This includes the development of low-viscosity engine oils to improve fuel efficiency, synthetic lubricants offering enhanced performance and durability, and bio-based lubricants focused on environmental sustainability. These innovations aim to meet the changing demands of modern vehicles and stricter emission regulations. The introduction of lubricants tailored for electric vehicles and hybrid electric vehicles is also gaining traction, addressing the specific needs of this rapidly growing market segment.

Report Scope & Segmentation Analysis

This report segments the North American automotive lubricants market by vehicle type (passenger vehicles, commercial vehicles, motorcycles), product type (engine oils, greases, hydraulic fluids, transmission & gear oils), and country (United States, Canada, Mexico, Rest of North America). Growth projections for each segment are provided, along with detailed analysis of market size, competitive dynamics, and key drivers for each segment. The market size for each segment is predicted for both the base year (2025) and the forecast period (2025-2033), enabling a comprehensive understanding of the market dynamics across various segments.

Key Drivers of North America Automotive Lubricants Industry Growth

The growth of the North American automotive lubricants industry is driven by several key factors:

- Rising Vehicle Sales: Increasing demand for personal and commercial vehicles, especially in developing regions within North America.

- Stringent Emission Regulations: Governments' push for stricter emission standards is driving the development and adoption of more fuel-efficient and environmentally friendly lubricants.

- Technological Advancements: Continuous innovation in lubricant formulations, resulting in higher-performance, longer-lasting, and more environmentally friendly products.

- Economic Growth: Positive economic growth in the region boosts consumer spending and the demand for automobiles.

Challenges in the North America Automotive Lubricants Industry Sector

The North American automotive lubricants industry faces several challenges:

- Fluctuating Crude Oil Prices: Volatility in crude oil prices directly impacts the cost of production and profitability.

- Environmental Regulations: Meeting increasingly stringent environmental regulations requires significant investments in research and development, as well as compliance costs.

- Intense Competition: The presence of many established players and new entrants creates intense competition, leading to price pressures and a need for continuous product differentiation.

- Supply Chain Disruptions: Global supply chain disruptions can impact the availability of raw materials and hinder production. These disruptions have resulted in an estimated xx Million loss of revenue for several companies in the past two years.

Emerging Opportunities in North America Automotive Lubricants Industry

The automotive lubricants market presents several emerging opportunities:

- Growth of Electric Vehicles: The transition to electric vehicles presents opportunities for developing specialized lubricants for electric vehicle components.

- Bio-based Lubricants: Growing consumer interest in sustainable products is driving demand for bio-based lubricants.

- Advanced Additive Technology: The incorporation of advanced additives for enhanced performance and efficiency is an area of significant growth.

- Digitalization of the Supply Chain: Improved supply chain management through digital technologies can improve efficiency and reduce costs.

Leading Players in the North America Automotive Lubricants Industry Market

- ExxonMobil Corporation

- BP PLC (Castrol)

- Phillips 66 Lubricants

- Roshfrans

- Royal Dutch Shell Plc

- Chevron Corporation

- TotalEnergies

- HollyFrontier (PetroCanada lubricants)

- Valvoline Inc

- AMSOIL Inc

Key Developments in North America Automotive Lubricants Industry Industry

- July 2021: Mighty Distributing System (Mighty Auto Parts) partnered with Total Specialties USA to distribute Quartz Ineo and Quartz 9000 lubricants. This expanded TotalEnergies' distribution network in the North American aftermarket.

- October 2021: Valvoline and Cummins extended their collaboration agreement for another five years, strengthening Valvoline's position in the heavy-duty diesel engine oil market.

- January 2022: ExxonMobil reorganized its business into three lines: Upstream Company, Product Solutions, and Low Carbon Solutions, reflecting a strategic shift toward low-carbon technologies. This reorganization signals ExxonMobil’s commitment to adapting to changing market demands.

Strategic Outlook for North America Automotive Lubricants Industry Market

The North American automotive lubricants market is poised for continued growth, driven by increasing vehicle ownership, stricter emission regulations, and technological innovations. The shift towards electric vehicles presents both challenges and opportunities, requiring companies to adapt their product portfolios and invest in research and development to cater to the evolving needs of the automotive industry. The focus on sustainability and environmental responsibility will further shape market trends, creating a demand for eco-friendly and high-performance lubricants. The overall outlook for the industry is positive, with significant growth potential in the coming years.

North America Automotive Lubricants Industry Segmentation

-

1. Vehicle Type

- 1.1. Commercial Vehicles

- 1.2. Motorcycles

- 1.3. Passenger Vehicles

-

2. Product Type

- 2.1. Engine Oils

- 2.2. Greases

- 2.3. Hydraulic Fluids

- 2.4. Transmission & Gear Oils

North America Automotive Lubricants Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Automotive Lubricants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 0.99% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Automotive Production and Sales; Increasing Adoption of High-performance Lubricants

- 3.3. Market Restrains

- 3.3.1. Extended Drain Intervals; Modest Impact of Electric Vehicles (EVs) in the Future

- 3.4. Market Trends

- 3.4.1. Largest Segment By Vehicle Type

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Automotive Lubricants Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Commercial Vehicles

- 5.1.2. Motorcycles

- 5.1.3. Passenger Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Engine Oils

- 5.2.2. Greases

- 5.2.3. Hydraulic Fluids

- 5.2.4. Transmission & Gear Oils

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. United States North America Automotive Lubricants Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Automotive Lubricants Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Automotive Lubricants Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Automotive Lubricants Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 ExxonMobil Corporation

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 BP PLC (Castrol)

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Phillips 66 Lubricants

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Roshfrans

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Royal Dutch Shell Plc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Chevron Corporation

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 TotalEnergies

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 HollyFrontier (PetroCanada lubricants)

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Valvoline Inc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 AMSOIL Inc

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 ExxonMobil Corporation

List of Figures

- Figure 1: North America Automotive Lubricants Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Automotive Lubricants Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Automotive Lubricants Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Automotive Lubricants Industry Volume Billion Forecast, by Region 2019 & 2032

- Table 3: North America Automotive Lubricants Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 4: North America Automotive Lubricants Industry Volume Billion Forecast, by Vehicle Type 2019 & 2032

- Table 5: North America Automotive Lubricants Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 6: North America Automotive Lubricants Industry Volume Billion Forecast, by Product Type 2019 & 2032

- Table 7: North America Automotive Lubricants Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: North America Automotive Lubricants Industry Volume Billion Forecast, by Region 2019 & 2032

- Table 9: North America Automotive Lubricants Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: North America Automotive Lubricants Industry Volume Billion Forecast, by Country 2019 & 2032

- Table 11: United States North America Automotive Lubricants Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United States North America Automotive Lubricants Industry Volume (Billion) Forecast, by Application 2019 & 2032

- Table 13: Canada North America Automotive Lubricants Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Automotive Lubricants Industry Volume (Billion) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Automotive Lubricants Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Mexico North America Automotive Lubricants Industry Volume (Billion) Forecast, by Application 2019 & 2032

- Table 17: Rest of North America North America Automotive Lubricants Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Rest of North America North America Automotive Lubricants Industry Volume (Billion) Forecast, by Application 2019 & 2032

- Table 19: North America Automotive Lubricants Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 20: North America Automotive Lubricants Industry Volume Billion Forecast, by Vehicle Type 2019 & 2032

- Table 21: North America Automotive Lubricants Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 22: North America Automotive Lubricants Industry Volume Billion Forecast, by Product Type 2019 & 2032

- Table 23: North America Automotive Lubricants Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: North America Automotive Lubricants Industry Volume Billion Forecast, by Country 2019 & 2032

- Table 25: United States North America Automotive Lubricants Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: United States North America Automotive Lubricants Industry Volume (Billion) Forecast, by Application 2019 & 2032

- Table 27: Canada North America Automotive Lubricants Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Canada North America Automotive Lubricants Industry Volume (Billion) Forecast, by Application 2019 & 2032

- Table 29: Mexico North America Automotive Lubricants Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Mexico North America Automotive Lubricants Industry Volume (Billion) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Lubricants Industry?

The projected CAGR is approximately 0.99%.

2. Which companies are prominent players in the North America Automotive Lubricants Industry?

Key companies in the market include ExxonMobil Corporation, BP PLC (Castrol), Phillips 66 Lubricants, Roshfrans, Royal Dutch Shell Plc, Chevron Corporation, TotalEnergies, HollyFrontier (PetroCanada lubricants), Valvoline Inc, AMSOIL Inc.

3. What are the main segments of the North America Automotive Lubricants Industry?

The market segments include Vehicle Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Automotive Production and Sales; Increasing Adoption of High-performance Lubricants.

6. What are the notable trends driving market growth?

Largest Segment By Vehicle Type : <span style="font-family: 'regular_bold';color:#0e7db3;">Passenger Vehicles</span>.

7. Are there any restraints impacting market growth?

Extended Drain Intervals; Modest Impact of Electric Vehicles (EVs) in the Future.

8. Can you provide examples of recent developments in the market?

January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.October 2021: Valvoline and Cummins extended their long-standing marketing and technology collaboration agreement for another five years. Cummins will endorse and promote Valvoline's Premium Blue engine oil for its heavy-duty diesel engines and generators and will distribute Valvoline products through its global distribution networks.July 2021: Mighty Distributing System (Mighty Auto Parts), a pioneer in automotive aftermarket goods and services, announced a new relationship with Total Specialties USA. It would target the Quartz Ineo and Quartz 9000 sub-ranges, geared for light automobiles and meet European OEMs' most stringent criteria.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Lubricants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Lubricants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Lubricants Industry?

To stay informed about further developments, trends, and reports in the North America Automotive Lubricants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence