Key Insights

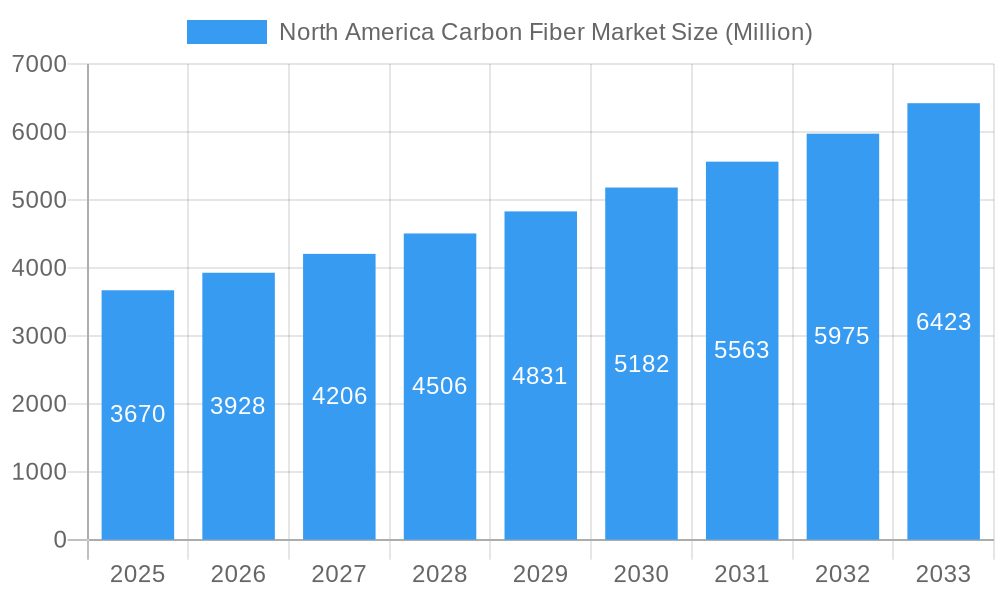

The North America Carbon Fiber Market is poised for significant expansion, projected to reach an estimated $3.67 billion in 2025 with a robust Compound Annual Growth Rate (CAGR) of 7.04% through 2033. This growth is largely fueled by the escalating demand for lightweight, high-strength materials across pivotal industries. Key drivers include the aerospace and defense sector's continuous pursuit of fuel efficiency and enhanced performance, alongside the burgeoning automotive industry's shift towards electric vehicles (EVs) where weight reduction is paramount for extending battery range. Furthermore, the expanding renewable energy sector, particularly in wind turbine blade manufacturing, and the increasing adoption of composite materials in construction and infrastructure projects are significant contributors. Advancements in carbon fiber production technologies, leading to cost reductions and improved material properties, are also propelling market growth.

North America Carbon Fiber Market Market Size (In Billion)

The market is segmented by raw material, with Polyacrylonitrile (PAN) remaining the dominant precursor due to its superior performance characteristics. Both virgin fiber (VCF) and recycled fiber (RCF) are gaining traction, with RCF adoption increasing as sustainability initiatives gain momentum and recycling technologies mature. Applications span high-performance textiles, advanced composite materials for structural components, specialized microelectrodes in electronics, and catalytic converters in automotive applications. While opportunities abound, the market faces restraints such as the high initial cost of carbon fiber production and complex recycling processes, which can hinder widespread adoption, especially in cost-sensitive applications. However, the persistent innovation and strategic investments by leading players are expected to mitigate these challenges, ensuring a dynamic and upward trajectory for the North America Carbon Fiber Market.

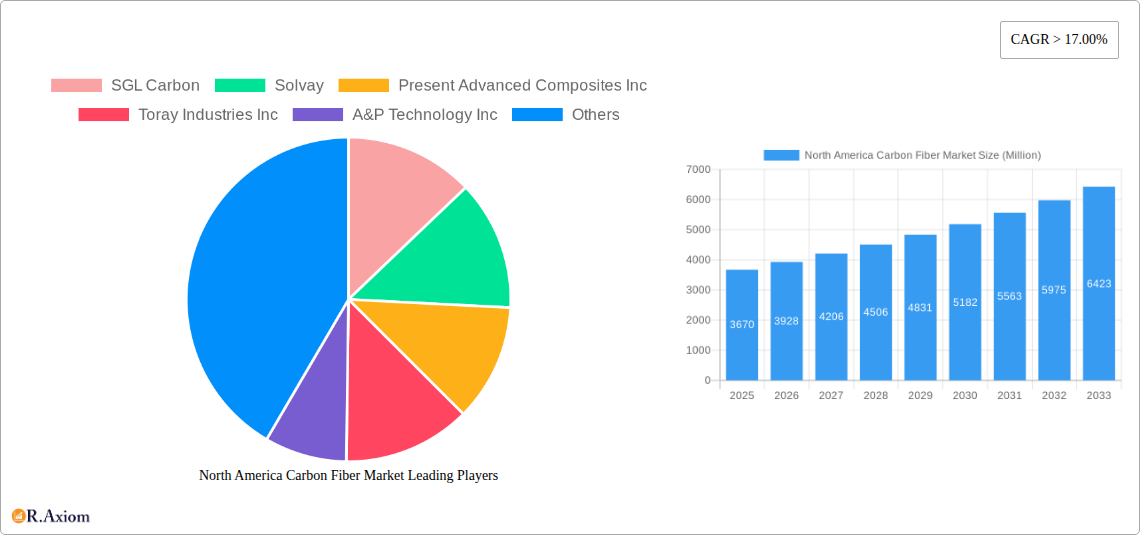

North America Carbon Fiber Market Company Market Share

North America Carbon Fiber Market Market Concentration & Innovation

The North America carbon fiber market, estimated to be valued at approximately $5.5 billion in 2025, exhibits a moderately concentrated landscape driven by significant investments in R&D and a surge in technological advancements. Innovation is primarily fueled by the demand for lightweight, high-strength materials across diverse end-user industries. Key innovation drivers include the development of novel precursor materials, enhanced manufacturing processes for both virgin and recycled carbon fiber, and the creation of advanced composite materials tailored for specific applications. Regulatory frameworks, particularly those promoting sustainability and emissions reduction in the automotive and aerospace sectors, indirectly stimulate innovation by encouraging the adoption of lighter materials. Product substitutes, such as advanced aluminum alloys and high-strength steel, remain a consideration, but the superior strength-to-weight ratio of carbon fiber continues to offer a distinct competitive advantage. End-user trends, especially the burgeoning electric vehicle (EV) market and the expansion of renewable energy infrastructure, are critical innovation catalysts. Mergers and acquisitions (M&A) activities, while not extensively documented with precise deal values, are likely to play a role in market consolidation and the diffusion of innovative technologies. Companies like SGL Carbon and Solvay actively invest in expanding their production capacities and developing new grades of carbon fiber to meet evolving market needs, indicating a strategic focus on capturing market share through technological leadership.

North America Carbon Fiber Market Industry Trends & Insights

The North America carbon fiber market is poised for robust growth, projected to reach a valuation exceeding $10.0 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 6.5% between 2025 and 2033. This expansion is primarily propelled by the escalating demand for lightweight, high-performance materials across a spectrum of industries, notably automotive, aerospace, and renewable energy. The automotive sector, in particular, is witnessing a significant shift towards carbon fiber composites to enhance fuel efficiency and enable the design of more aerodynamic electric vehicles. Stringent environmental regulations and government incentives promoting reduced emissions are further accelerating the adoption of carbon fiber solutions. In the aerospace industry, the continuous pursuit of lighter and stronger aircraft components for improved performance and fuel economy remains a dominant trend. The alternative energy sector, especially wind energy, is a growing consumer of carbon fiber for the manufacturing of larger and more efficient turbine blades. Technological disruptions, including advancements in additive manufacturing for carbon fiber composites and the development of cost-effective recycling processes for carbon fiber waste, are poised to redefine market dynamics. The increasing availability of recycled carbon fiber (RCF) is making carbon fiber more accessible and sustainable, broadening its market penetration. Consumer preferences are increasingly leaning towards products that offer enhanced performance, durability, and sustainability, aligning perfectly with the inherent qualities of carbon fiber. Competitive dynamics are characterized by intense R&D efforts, strategic collaborations between material suppliers and end-users, and a focus on expanding production capacities to meet growing demand. Major players are investing heavily in innovation to develop differentiated products and secure long-term supply agreements.

Dominant Markets & Segments in North America Carbon Fiber Market

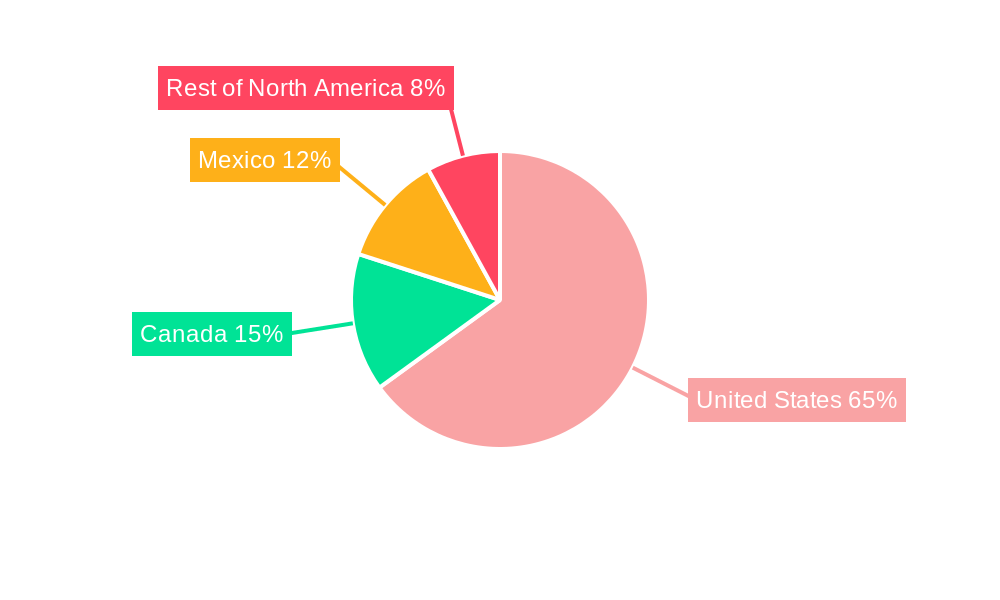

The North America carbon fiber market's dominance is intricately linked to the economic prowess and industrial landscape of its constituent regions, with the United States emerging as the undisputed leader, accounting for a substantial portion of market share. This preeminence is driven by its advanced manufacturing capabilities, significant presence of key end-user industries like aerospace and automotive, and robust research and development infrastructure.

Raw Material Dominance:

- Polyacrylonitrile (PAN) reigns supreme as the dominant raw material for carbon fiber production in North America. Its superior properties and established manufacturing processes make it the preferred precursor, especially for high-performance applications. The strong demand from the aerospace and automotive sectors for Virgin Fiber (VCF) further solidifies PAN's leading position.

Type Dominance:

- Virgin Fiber (VCF) continues to hold the largest market share due to its unparalleled performance characteristics, which are critical for demanding applications. However, Recycled Fiber (RCF) is experiencing a rapid growth trajectory, driven by sustainability initiatives and the development of advanced recycling technologies, making it a significant emerging segment.

Application Dominance:

- Composite Materials represent the largest application segment, as carbon fiber is predominantly used to create high-performance composite structures. The versatility of these composites allows for their application across a multitude of industries.

End-user Industry Dominance:

- Aerospace and Defense has historically been and continues to be a dominant end-user industry, demanding lightweight and high-strength materials for aircraft and defense systems.

- Automotive is rapidly gaining ground and is projected to become a dominant segment in the coming years, driven by the electrification trend and the need for weight reduction in vehicles.

- Alternative Energy, particularly wind energy, is a significant and growing contributor to market demand, with carbon fiber playing a crucial role in the manufacturing of wind turbine blades.

Geographical Dominance:

- United States: The sheer scale of its manufacturing base, coupled with substantial investments in aerospace, automotive, and renewable energy, positions the United States as the most dominant geographical market within North America.

- Canada: While smaller than the US, Canada exhibits strong growth in sectors like aerospace and automotive, contributing significantly to the market.

- Mexico: Its burgeoning automotive manufacturing sector and strategic location make Mexico an increasingly important market for carbon fiber.

- Rest of North America: This segment encompasses smaller markets with specialized demand, contributing to the overall growth but with less individual market impact compared to the leading nations.

North America Carbon Fiber Market Product Developments

Product development in the North America carbon fiber market is characterized by a relentless pursuit of enhanced performance, cost-effectiveness, and sustainability. Innovations are focused on developing carbon fibers with higher tensile strength and modulus, improved temperature resistance, and better fatigue performance. The introduction of larger tow size fibers, such as the SIGRAFIL 50k carbon fiber by SGL Carbon, signifies a trend towards increased process efficiency and higher material throughput for manufacturers in the wind and automotive industries. Collaborations, like the one between Hexcel Corporation and Archer Aviation Inc., highlight the development of high-performance materials specifically tailored for emerging applications like electric vertical take-off and landing (eVTOL) aircraft. Furthermore, advancements in recycled carbon fiber technologies, exemplified by Vartega's patented chemical-based recycling process, are crucial for addressing sustainability concerns and expanding the market's reach into cost-sensitive applications. These developments collectively aim to drive broader adoption of carbon fiber by improving its manufacturing economics and environmental footprint.

Report Scope & Segmentation Analysis

This comprehensive report delves into the North America carbon fiber market, meticulously segmented to provide actionable insights. The study encompasses the entire value chain, from raw materials to end-user applications and geographical distribution.

Raw Material Segmentation: The market is analyzed based on Polyacrylonitrile (PAN), Petroleum Pitch, and Rayon. PAN is expected to dominate due to its widespread use in high-performance fibers. Petroleum pitch and rayon, while currently smaller segments, offer niche applications and potential for growth.

Type Segmentation: The report distinguishes between Virgin Fiber (VCF) and Recycled Fiber (RCF). VCF is projected to maintain its dominance owing to superior performance, while RCF is anticipated to witness significant growth driven by sustainability initiatives and cost advantages.

Application Segmentation: Key applications analyzed include Composite Materials, Textiles, Microelectrodes, and Catalysis. Composite materials are expected to remain the largest application, with notable growth anticipated in textiles and microelectronics due to their unique conductive and lightweight properties.

End-user Industry Segmentation: The market is segmented into Aerospace and Defense, Alternative Energy, Automotive, Construction and Infrastructure, Sporting Goods, and Other End-user Industries (Marine and Maritime). Aerospace and Defense and Automotive are projected to be the leading segments, with significant growth potential also seen in Alternative Energy and Construction.

Geography Segmentation: The report provides an in-depth analysis of the United States, Canada, Mexico, and the Rest of North America. The United States is anticipated to lead in market size and growth, followed by Canada and Mexico, driven by their respective industrial strengths.

Key Drivers of North America Carbon Fiber Market Growth

The North America carbon fiber market is propelled by a confluence of powerful drivers. The relentless demand for lightweight materials to enhance fuel efficiency and reduce emissions across the automotive and aerospace sectors is paramount. Government regulations and incentives promoting sustainability further bolster this trend. Technological advancements in manufacturing processes, including improved precursor technologies and efficient recycling methods, are making carbon fiber more accessible and cost-effective. The rapid growth of the electric vehicle (EV) market necessitates lighter vehicle structures to maximize range, making carbon fiber composites an attractive solution. Expansion in the renewable energy sector, particularly for wind turbine blades, is another significant growth catalyst. Furthermore, increasing investments in infrastructure development and the growing demand for high-performance sporting goods contribute to market expansion.

Challenges in the North America Carbon Fiber Market Sector

Despite its robust growth trajectory, the North America carbon fiber market faces several challenges. The high cost of production, particularly for virgin carbon fiber, remains a significant barrier to wider adoption in cost-sensitive applications. Complex manufacturing processes and the need for specialized equipment contribute to this cost. Supply chain disruptions, including the availability and price volatility of precursor materials like PAN, can impact production and pricing. Developing standardized recycling processes for carbon fiber waste that consistently yield high-quality material is an ongoing challenge. Furthermore, the availability of competitive substitutes, such as advanced aluminum alloys and high-strength steels, presents a persistent challenge, especially in applications where the full performance benefits of carbon fiber may not be critical. Regulatory hurdles related to the use of composite materials in certain applications and the need for specialized training for engineers and technicians also pose limitations.

Emerging Opportunities in North America Carbon Fiber Market

The North America carbon fiber market is brimming with emerging opportunities. The burgeoning electric vertical take-off and landing (eVTOL) aircraft market presents a significant new frontier, demanding lightweight and strong materials for sustainable air mobility solutions. Advancements in additive manufacturing (3D printing) with carbon fiber composites are opening up possibilities for rapid prototyping and the creation of complex, customized parts. The growing emphasis on circular economy principles is driving innovation in carbon fiber recycling, creating opportunities for companies to develop and scale up cost-effective RCF solutions. Expanding applications in the construction and infrastructure sector, such as the use of carbon fiber reinforced polymers (CFRPs) for bridge reinforcement and seismic retrofitting, offer substantial growth potential. The increasing adoption of carbon fiber in medical devices, due to its biocompatibility and strength, also represents a promising emerging market.

Leading Players in the North America Carbon Fiber Market Market

- SGL Carbon

- Solvay

- Toray Industries Inc.

- Hexcel Corporation

- TEIJIN LIMITED

- Mitsubishi Chemical Carbon Fiber and Composites Inc.

- DowAksa

- Hyosung Advanced Materials

- Formosa M Co Ltd

- Present Advanced Composites Inc

- A&P Technology Inc.

- Vartega Inc.

Key Developments in North America Carbon Fiber Market Industry

- March 2023: SGL Carbon launched SIGRAFIL 50k carbon fiber. This majorly used in the wind and automotive industries, among others. It has high levels of strength of 4.9 GPa and elongation of 2.0 %. The advantages of SIGRAFIL 50k fiber types are increased process efficiency, higher material throughput, faster process times, and less set-up effort.

- April 2022: Hexcel Corporation and Archer Aviation Inc. announced their collaboration to supply high-performance carbon fiber material that would be used to manufacture Archer's production aircraft.

- January 2022: Vartega, a US-based company, announced the employment of a new technology for the recycling of carbon fiber waste for the management of carbon fiber waste in the country. The company will be using a patented chemical-based process to rescue carbon fiber waste from an eternity in the landfill.

Strategic Outlook for North America Carbon Fiber Market Market

The strategic outlook for the North America carbon fiber market is exceptionally bright, fueled by a persistent global drive for performance, efficiency, and sustainability. Key growth catalysts include the accelerating adoption of electric vehicles, the ongoing expansion of renewable energy infrastructure, and the continued innovation within the aerospace sector. Investments in advanced manufacturing technologies and the development of more cost-effective and sustainable production methods, particularly through the expansion of recycled carbon fiber capabilities, will be crucial for unlocking new market segments and capturing a larger share. Strategic partnerships between material suppliers and end-users will continue to shape product development and market penetration. Emerging applications in areas like additive manufacturing and advanced construction solutions will offer significant future growth potential, solidifying carbon fiber's position as a critical material for innovation and progress across diverse industries in North America.

North America Carbon Fiber Market Segmentation

-

1. Raw Material

- 1.1. Polyacrtlonitrile (PAN)

- 1.2. Petroleum Pitch and Rayon

-

2. Type

- 2.1. Virgin Fiber (VCF)

- 2.2. Recycled Fiber (RCF)

-

3. Application

- 3.1. Composite Materials

- 3.2. Textiles

- 3.3. Microelectrodes

- 3.4. Catalysis

-

4. End-user Industry

- 4.1. Aerospace and Defense

- 4.2. Alternative Energy

- 4.3. Automotive

- 4.4. Construction and Infrastructure

- 4.5. Sporting Goods

- 4.6. Other End-user Industries (Marine and Maritime)

-

5. Geography

- 5.1. United States

- 5.2. Canada

- 5.3. Mexico

- 5.4. Rest of North America

North America Carbon Fiber Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

North America Carbon Fiber Market Regional Market Share

Geographic Coverage of North America Carbon Fiber Market

North America Carbon Fiber Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 5.1.1. Polyacrtlonitrile (PAN)

- 5.1.2. Petroleum Pitch and Rayon

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Virgin Fiber (VCF)

- 5.2.2. Recycled Fiber (RCF)

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Composite Materials

- 5.3.2. Textiles

- 5.3.3. Microelectrodes

- 5.3.4. Catalysis

- 5.4. Market Analysis, Insights and Forecast - by End-user Industry

- 5.4.1. Aerospace and Defense

- 5.4.2. Alternative Energy

- 5.4.3. Automotive

- 5.4.4. Construction and Infrastructure

- 5.4.5. Sporting Goods

- 5.4.6. Other End-user Industries (Marine and Maritime)

- 5.5. Market Analysis, Insights and Forecast - by Geography

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.5.4. Rest of North America

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. United States

- 5.6.2. Canada

- 5.6.3. Mexico

- 5.6.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 6. North America Carbon Fiber Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 6.1.1. Polyacrtlonitrile (PAN)

- 6.1.2. Petroleum Pitch and Rayon

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Virgin Fiber (VCF)

- 6.2.2. Recycled Fiber (RCF)

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Composite Materials

- 6.3.2. Textiles

- 6.3.3. Microelectrodes

- 6.3.4. Catalysis

- 6.4. Market Analysis, Insights and Forecast - by End-user Industry

- 6.4.1. Aerospace and Defense

- 6.4.2. Alternative Energy

- 6.4.3. Automotive

- 6.4.4. Construction and Infrastructure

- 6.4.5. Sporting Goods

- 6.4.6. Other End-user Industries (Marine and Maritime)

- 6.5. Market Analysis, Insights and Forecast - by Geography

- 6.5.1. United States

- 6.5.2. Canada

- 6.5.3. Mexico

- 6.5.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 7. United States North America Carbon Fiber Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 7.1.1. Polyacrtlonitrile (PAN)

- 7.1.2. Petroleum Pitch and Rayon

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Virgin Fiber (VCF)

- 7.2.2. Recycled Fiber (RCF)

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Composite Materials

- 7.3.2. Textiles

- 7.3.3. Microelectrodes

- 7.3.4. Catalysis

- 7.4. Market Analysis, Insights and Forecast - by End-user Industry

- 7.4.1. Aerospace and Defense

- 7.4.2. Alternative Energy

- 7.4.3. Automotive

- 7.4.4. Construction and Infrastructure

- 7.4.5. Sporting Goods

- 7.4.6. Other End-user Industries (Marine and Maritime)

- 7.5. Market Analysis, Insights and Forecast - by Geography

- 7.5.1. United States

- 7.5.2. Canada

- 7.5.3. Mexico

- 7.5.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Raw Material

- 8. Canada North America Carbon Fiber Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 8.1.1. Polyacrtlonitrile (PAN)

- 8.1.2. Petroleum Pitch and Rayon

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Virgin Fiber (VCF)

- 8.2.2. Recycled Fiber (RCF)

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Composite Materials

- 8.3.2. Textiles

- 8.3.3. Microelectrodes

- 8.3.4. Catalysis

- 8.4. Market Analysis, Insights and Forecast - by End-user Industry

- 8.4.1. Aerospace and Defense

- 8.4.2. Alternative Energy

- 8.4.3. Automotive

- 8.4.4. Construction and Infrastructure

- 8.4.5. Sporting Goods

- 8.4.6. Other End-user Industries (Marine and Maritime)

- 8.5. Market Analysis, Insights and Forecast - by Geography

- 8.5.1. United States

- 8.5.2. Canada

- 8.5.3. Mexico

- 8.5.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Raw Material

- 9. Mexico North America Carbon Fiber Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 9.1.1. Polyacrtlonitrile (PAN)

- 9.1.2. Petroleum Pitch and Rayon

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Virgin Fiber (VCF)

- 9.2.2. Recycled Fiber (RCF)

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Composite Materials

- 9.3.2. Textiles

- 9.3.3. Microelectrodes

- 9.3.4. Catalysis

- 9.4. Market Analysis, Insights and Forecast - by End-user Industry

- 9.4.1. Aerospace and Defense

- 9.4.2. Alternative Energy

- 9.4.3. Automotive

- 9.4.4. Construction and Infrastructure

- 9.4.5. Sporting Goods

- 9.4.6. Other End-user Industries (Marine and Maritime)

- 9.5. Market Analysis, Insights and Forecast - by Geography

- 9.5.1. United States

- 9.5.2. Canada

- 9.5.3. Mexico

- 9.5.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Raw Material

- 10. Rest of North America North America Carbon Fiber Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 10.1.1. Polyacrtlonitrile (PAN)

- 10.1.2. Petroleum Pitch and Rayon

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Virgin Fiber (VCF)

- 10.2.2. Recycled Fiber (RCF)

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Composite Materials

- 10.3.2. Textiles

- 10.3.3. Microelectrodes

- 10.3.4. Catalysis

- 10.4. Market Analysis, Insights and Forecast - by End-user Industry

- 10.4.1. Aerospace and Defense

- 10.4.2. Alternative Energy

- 10.4.3. Automotive

- 10.4.4. Construction and Infrastructure

- 10.4.5. Sporting Goods

- 10.4.6. Other End-user Industries (Marine and Maritime)

- 10.5. Market Analysis, Insights and Forecast - by Geography

- 10.5.1. United States

- 10.5.2. Canada

- 10.5.3. Mexico

- 10.5.4. Rest of North America

- 10.1. Market Analysis, Insights and Forecast - by Raw Material

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 SGL Carbon

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Solvay

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Present Advanced Composites Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Toray Industries Inc

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 A&P Technology Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Formosa M Co Ltd

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 DowAksa

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Hyosung Advanced Materials

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Mitsubishi Chemical Carbon Fiber and Composites Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Hexcel Corporation

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 TEIJIN LIMITED

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Vartega Inc *List Not Exhaustive

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 SGL Carbon

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: North America Carbon Fiber Market Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: North America Carbon Fiber Market Share (%) by Company 2025

List of Tables

- Table 1: North America Carbon Fiber Market Revenue undefined Forecast, by Raw Material 2020 & 2033

- Table 2: North America Carbon Fiber Market Volume kilotons Forecast, by Raw Material 2020 & 2033

- Table 3: North America Carbon Fiber Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: North America Carbon Fiber Market Volume kilotons Forecast, by Type 2020 & 2033

- Table 5: North America Carbon Fiber Market Revenue undefined Forecast, by Application 2020 & 2033

- Table 6: North America Carbon Fiber Market Volume kilotons Forecast, by Application 2020 & 2033

- Table 7: North America Carbon Fiber Market Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 8: North America Carbon Fiber Market Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 9: North America Carbon Fiber Market Revenue undefined Forecast, by Geography 2020 & 2033

- Table 10: North America Carbon Fiber Market Volume kilotons Forecast, by Geography 2020 & 2033

- Table 11: North America Carbon Fiber Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 12: North America Carbon Fiber Market Volume kilotons Forecast, by Region 2020 & 2033

- Table 13: North America Carbon Fiber Market Revenue undefined Forecast, by Raw Material 2020 & 2033

- Table 14: North America Carbon Fiber Market Volume kilotons Forecast, by Raw Material 2020 & 2033

- Table 15: North America Carbon Fiber Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 16: North America Carbon Fiber Market Volume kilotons Forecast, by Type 2020 & 2033

- Table 17: North America Carbon Fiber Market Revenue undefined Forecast, by Application 2020 & 2033

- Table 18: North America Carbon Fiber Market Volume kilotons Forecast, by Application 2020 & 2033

- Table 19: North America Carbon Fiber Market Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 20: North America Carbon Fiber Market Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 21: North America Carbon Fiber Market Revenue undefined Forecast, by Geography 2020 & 2033

- Table 22: North America Carbon Fiber Market Volume kilotons Forecast, by Geography 2020 & 2033

- Table 23: North America Carbon Fiber Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: North America Carbon Fiber Market Volume kilotons Forecast, by Country 2020 & 2033

- Table 25: North America Carbon Fiber Market Revenue undefined Forecast, by Raw Material 2020 & 2033

- Table 26: North America Carbon Fiber Market Volume kilotons Forecast, by Raw Material 2020 & 2033

- Table 27: North America Carbon Fiber Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 28: North America Carbon Fiber Market Volume kilotons Forecast, by Type 2020 & 2033

- Table 29: North America Carbon Fiber Market Revenue undefined Forecast, by Application 2020 & 2033

- Table 30: North America Carbon Fiber Market Volume kilotons Forecast, by Application 2020 & 2033

- Table 31: North America Carbon Fiber Market Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 32: North America Carbon Fiber Market Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 33: North America Carbon Fiber Market Revenue undefined Forecast, by Geography 2020 & 2033

- Table 34: North America Carbon Fiber Market Volume kilotons Forecast, by Geography 2020 & 2033

- Table 35: North America Carbon Fiber Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: North America Carbon Fiber Market Volume kilotons Forecast, by Country 2020 & 2033

- Table 37: North America Carbon Fiber Market Revenue undefined Forecast, by Raw Material 2020 & 2033

- Table 38: North America Carbon Fiber Market Volume kilotons Forecast, by Raw Material 2020 & 2033

- Table 39: North America Carbon Fiber Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 40: North America Carbon Fiber Market Volume kilotons Forecast, by Type 2020 & 2033

- Table 41: North America Carbon Fiber Market Revenue undefined Forecast, by Application 2020 & 2033

- Table 42: North America Carbon Fiber Market Volume kilotons Forecast, by Application 2020 & 2033

- Table 43: North America Carbon Fiber Market Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 44: North America Carbon Fiber Market Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 45: North America Carbon Fiber Market Revenue undefined Forecast, by Geography 2020 & 2033

- Table 46: North America Carbon Fiber Market Volume kilotons Forecast, by Geography 2020 & 2033

- Table 47: North America Carbon Fiber Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 48: North America Carbon Fiber Market Volume kilotons Forecast, by Country 2020 & 2033

- Table 49: North America Carbon Fiber Market Revenue undefined Forecast, by Raw Material 2020 & 2033

- Table 50: North America Carbon Fiber Market Volume kilotons Forecast, by Raw Material 2020 & 2033

- Table 51: North America Carbon Fiber Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 52: North America Carbon Fiber Market Volume kilotons Forecast, by Type 2020 & 2033

- Table 53: North America Carbon Fiber Market Revenue undefined Forecast, by Application 2020 & 2033

- Table 54: North America Carbon Fiber Market Volume kilotons Forecast, by Application 2020 & 2033

- Table 55: North America Carbon Fiber Market Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 56: North America Carbon Fiber Market Volume kilotons Forecast, by End-user Industry 2020 & 2033

- Table 57: North America Carbon Fiber Market Revenue undefined Forecast, by Geography 2020 & 2033

- Table 58: North America Carbon Fiber Market Volume kilotons Forecast, by Geography 2020 & 2033

- Table 59: North America Carbon Fiber Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: North America Carbon Fiber Market Volume kilotons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Carbon Fiber Market?

The projected CAGR is approximately 7.04%.

2. Which companies are prominent players in the North America Carbon Fiber Market?

Key companies in the market include SGL Carbon, Solvay, Present Advanced Composites Inc, Toray Industries Inc, A&P Technology Inc, Formosa M Co Ltd, DowAksa, Hyosung Advanced Materials, Mitsubishi Chemical Carbon Fiber and Composites Inc, Hexcel Corporation, TEIJIN LIMITED, Vartega Inc *List Not Exhaustive.

3. What are the main segments of the North America Carbon Fiber Market?

The market segments include Raw Material, Type, Application, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Fuel-efficient and Lightweight Vehicles; Accelerating Usage in the Aerospace and Defense Sector; Increasing Usage in Renewable Energy.

6. What are the notable trends driving market growth?

Aerospace and Defense Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

High R&D Investments; Other Restraints.

8. Can you provide examples of recent developments in the market?

March 2023: SGL Carbon launched SIGRAFIL 50k carbon fiber. This is majorly used in the wind and automotive industries, among others. It has high levels of strength of 4.9 GPa and elongation of 2.0 %. The advantages of SIGRAFIL 50k fiber types are increased process efficiency, higher material throughput, faster process times, and less set-up effort.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in kilotons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Carbon Fiber Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Carbon Fiber Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Carbon Fiber Market?

To stay informed about further developments, trends, and reports in the North America Carbon Fiber Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence