Key Insights

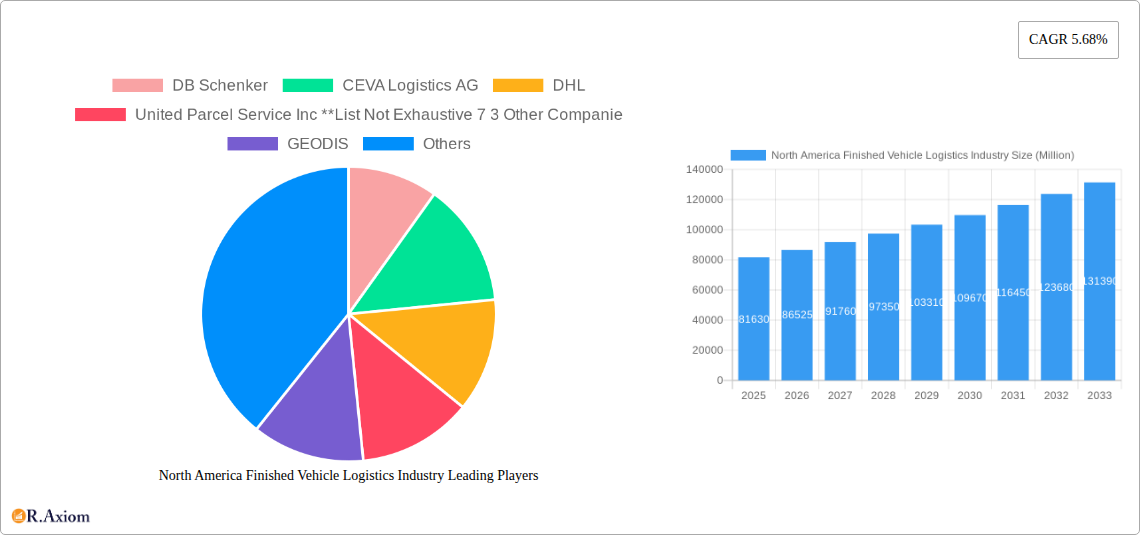

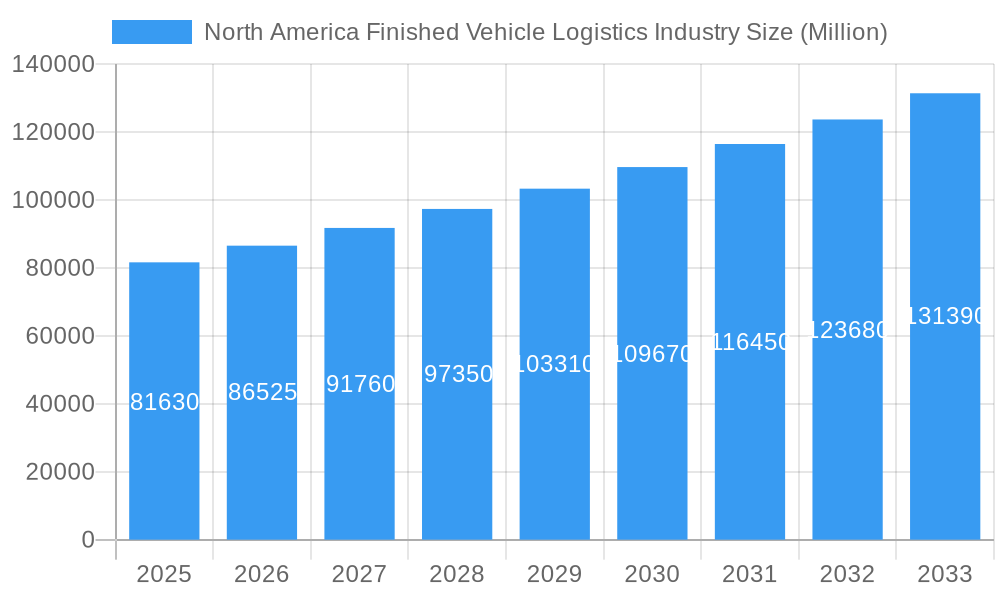

The North American finished vehicle logistics market, valued at $81.63 billion in 2025, is projected to experience robust growth, driven by a Compound Annual Growth Rate (CAGR) of 5.68% from 2025 to 2033. This expansion is fueled by several key factors. The increasing production and sales of vehicles, particularly in the electric vehicle (EV) segment, necessitate efficient and specialized logistics solutions. Furthermore, the growth of e-commerce in automotive parts and accessories indirectly contributes to the demand for robust finished vehicle logistics. The expansion of automotive manufacturing facilities across North America, along with the rise of just-in-time inventory management strategies, further propels market growth. Infrastructure improvements focused on supporting larger and heavier vehicle transportation also play a significant role. However, challenges remain, including fluctuations in fuel prices, geopolitical uncertainties affecting supply chains, and the need for enhanced cybersecurity measures within logistics operations. These factors can impact profitability and efficiency. The market is segmented by service (transportation, warehousing, distribution and inventory management, and other services), vehicle type (finished vehicles, auto components, and other types), and geography (United States, Canada, and Mexico). Major players like DB Schenker, CEVA Logistics, DHL, and UPS are actively shaping the market landscape through strategic partnerships, technological advancements, and expansion efforts. The competitive nature of the market requires companies to continuously innovate and offer specialized services to meet the evolving needs of the automotive industry.

North America Finished Vehicle Logistics Industry Market Size (In Billion)

The North American region, specifically the United States, Canada, and Mexico, represents a significant share of the global finished vehicle logistics market. Growth within this region is expected to be predominantly driven by the expansion of automotive manufacturing hubs and the increasing demand for efficient transportation solutions catering to the diverse needs of OEMs (Original Equipment Manufacturers) and dealerships. The development of sustainable and environmentally friendly transportation methods, coupled with advancements in supply chain technology, are expected to become increasingly important in the years to come. Companies are focusing on improving their efficiency through route optimization, real-time tracking, and predictive analytics, further contributing to the market's positive outlook. The integration of technology, including AI and IoT (Internet of Things) solutions, is transforming the industry, leading to enhanced visibility, reduced operational costs, and improved overall supply chain resilience. This technological progress will be a key driver of sustained growth in the coming years.

North America Finished Vehicle Logistics Industry Company Market Share

This comprehensive report provides an in-depth analysis of the North America Finished Vehicle Logistics industry, offering invaluable insights for stakeholders, investors, and industry professionals. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report meticulously examines market trends, competitive dynamics, and future growth potential. The analysis incorporates data from the historical period (2019-2024) and leverages detailed segmentation across services, vehicle types, and geographical regions.

North America Finished Vehicle Logistics Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the North American finished vehicle logistics market, examining market concentration, innovation drivers, regulatory influences, and market dynamics. The market is characterized by a moderately concentrated structure, with key players such as DB Schenker, CEVA Logistics AG, DHL, United Parcel Service Inc., GEODIS, Nippon Express Co Ltd, XPO Logistics Inc, KUEHNE + NAGEL International AG, DSV, and Ryder System Inc. holding significant market share. However, several smaller players also contribute to the overall market dynamics. The exact market share for each player is unavailable and estimated at xx% for now.

The industry exhibits significant innovation driven by the need for enhanced efficiency, sustainability, and technological integration. Regulatory frameworks, including environmental regulations and trade agreements, significantly shape industry practices. Product substitutes, such as alternative transportation modes and technology-driven solutions, continuously challenge the established order. The increasing demand for electric vehicles and the associated logistical requirements further fuel innovation. Mergers and acquisitions (M&A) activity has been moderate over the past years, with total deal values estimated at xx Million USD (2019-2024). The average deal value is xx Million USD. This activity is expected to increase given the current market dynamics and industry growth projection. End-user trends towards just-in-time delivery and increased transparency in the supply chain are reshaping logistical operations.

North America Finished Vehicle Logistics Industry Industry Trends & Insights

The North America finished vehicle logistics market is experiencing robust growth, driven by a multitude of factors. The CAGR for the period 2025-2033 is projected to be xx%, reflecting the consistent expansion of the automotive industry and the increasing complexity of vehicle transportation and distribution. Market penetration of advanced logistics technologies, such as telematics and IoT, is growing at xx% annually. Technological disruptions, particularly in areas such as automation, data analytics, and AI-powered optimization, are transforming operational efficiency and cost structures. Consumer preferences for faster delivery times and enhanced visibility into the supply chain are placing increased pressure on logistics providers to adopt innovative solutions. Competitive dynamics are characterized by intense rivalry among established players and the emergence of new entrants leveraging technological advancements and disruptive business models. This is causing a price war, and lowering profit margins.

Dominant Markets & Segments in North America Finished Vehicle Logistics Industry

The United States constitutes the largest market within North America, accounting for approximately xx% of the total market value. Its well-established automotive industry, extensive infrastructure, and robust economic activity drive demand for finished vehicle logistics services.

By Country:

- United States: Dominant due to a large automotive manufacturing base, extensive infrastructure, and high economic activity.

- Mexico: Growing rapidly due to increasing automotive production and proximity to the US market.

- Canada: A significant but smaller market compared to the US, driven by its automotive industry and proximity to the US.

By Service:

- Transportation: Remains the largest segment, owing to the significant volume of vehicle movement.

- Warehousing: Growing steadily as manufacturers and retailers prioritize efficient inventory management.

- Distribution and Inventory Management: Expanding due to the need for optimized supply chain solutions.

- Other Services: Includes value-added services such as customs brokerage and insurance.

By Type:

- Finished Vehicles: The dominant segment, representing the bulk of logistical activity.

- Auto Components: A significant segment, with demand driven by the automotive supply chain.

- Other Types: Includes specialized vehicles and related equipment.

Key drivers in each segment include favorable government policies, infrastructure investments, and technological advancements.

North America Finished Vehicle Logistics Industry Product Developments

Recent product innovations focus on enhancing efficiency, transparency, and sustainability. This includes the integration of IoT sensors for real-time tracking, AI-powered route optimization software, and the use of alternative fuels to reduce carbon emissions. These developments address industry demands for improved supply chain visibility, cost reduction, and environmental responsibility, enhancing the competitiveness of logistics providers. The market fit is strong, aligning with industry trends towards digitization, efficiency, and sustainability.

Report Scope & Segmentation Analysis

This report segments the North American finished vehicle logistics market by service (Transportation, Warehousing, Distribution and Inventory Management, Other Services), vehicle type (Finished Vehicle, Auto Components, Other types), and country (United States, Canada, Mexico). Each segment’s market size and growth projections are analyzed, along with the competitive landscape. The Transportation segment exhibits the highest growth, driven by the burgeoning automotive sector. The Finished Vehicle type segment dominates due to the core nature of finished vehicle logistics. The US market remains the largest, followed by Mexico, experiencing significant growth due to its expanding automotive manufacturing base.

Key Drivers of North America Finished Vehicle Logistics Industry Growth

Several factors fuel the growth of the North American finished vehicle logistics industry. Firstly, the ongoing expansion of the automotive industry creates sustained demand for efficient vehicle transportation and distribution services. Secondly, the increasing adoption of just-in-time manufacturing strategies necessitates sophisticated logistics solutions. Thirdly, government initiatives promoting infrastructure development and technological innovation further stimulate industry growth. Finally, the rise of e-commerce and omnichannel distribution models adds to the demand for advanced logistics capabilities.

Challenges in the North America Finished Vehicle Logistics Industry Sector

The industry faces challenges, including fluctuating fuel prices impacting operational costs (estimated to increase costs by xx% in the next 5 years), stringent environmental regulations requiring compliance investment (estimated at xx Million USD annually), and intense competition among logistics providers. Supply chain disruptions, such as those witnessed recently, can significantly impact operational efficiency and profitability. These factors necessitate strategic adaptation and innovation to maintain competitiveness and profitability.

Emerging Opportunities in North America Finished Vehicle Logistics Industry

Emerging opportunities lie in the adoption of advanced technologies like AI, blockchain, and autonomous vehicles to enhance efficiency and optimize operations. The growing demand for sustainable logistics solutions presents opportunities for providers offering eco-friendly transportation options. Expansion into new markets, such as emerging economies and developing regions within North America, also provides significant growth potential. Moreover, the increasing focus on last-mile delivery solutions provides opportunities to create niche services.

Leading Players in the North America Finished Vehicle Logistics Industry Market

- DB Schenker

- CEVA Logistics AG

- DHL

- United Parcel Service Inc

- GEODIS

- Nippon Express Co Ltd

- XPO Logistics Inc

- KUEHNE + NAGEL International AG

- DSV

- Ryder System Inc

Key Developments in North America Finished Vehicle Logistics Industry Industry

- December 2023: The US Department of Energy's Advanced Energy Manufacturing and Recycling Grant Programme invested USD 250 Million to support clean energy supply chains and EV production, impacting logistics efficiency.

- May 2023: Bolloré Logistics opened a new automotive competence center in Mexico, enhancing its service offerings for automotive manufacturers and suppliers.

Strategic Outlook for North America Finished Vehicle Logistics Industry Market

The North American finished vehicle logistics market is poised for continued growth, driven by technological advancements, increasing automotive production, and evolving consumer demands. Opportunities for innovation, expansion, and strategic partnerships abound. The focus on sustainability, efficiency, and technological integration will shape future market dynamics. The market is expected to continue to consolidate, with larger players acquiring smaller ones and increasing their market share.

North America Finished Vehicle Logistics Industry Segmentation

-

1. Service

- 1.1. Transportation

- 1.2. Warehousing, Distribution and Inventory Management

- 1.3. Other Services

-

2. Type

- 2.1. Finished Vehicle

- 2.2. Auto Components

- 2.3. Other types

North America Finished Vehicle Logistics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Finished Vehicle Logistics Industry Regional Market Share

Geographic Coverage of North America Finished Vehicle Logistics Industry

North America Finished Vehicle Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.68% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Transportation

- 5.1.2. Warehousing, Distribution and Inventory Management

- 5.1.3. Other Services

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Finished Vehicle

- 5.2.2. Auto Components

- 5.2.3. Other types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. North America Finished Vehicle Logistics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Transportation

- 6.1.2. Warehousing, Distribution and Inventory Management

- 6.1.3. Other Services

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Finished Vehicle

- 6.2.2. Auto Components

- 6.2.3. Other types

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CEVA Logistics AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DHL

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 United Parcel Service Inc **List Not Exhaustive 7 3 Other Companie

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 GEODIS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Nippon Express Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 XPO Logistics Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 KUEHNE + NAGEL International AG

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 DSV

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Ryder System Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Finished Vehicle Logistics Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Finished Vehicle Logistics Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Finished Vehicle Logistics Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 2: North America Finished Vehicle Logistics Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 3: North America Finished Vehicle Logistics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: North America Finished Vehicle Logistics Industry Revenue Million Forecast, by Service 2020 & 2033

- Table 5: North America Finished Vehicle Logistics Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: North America Finished Vehicle Logistics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States North America Finished Vehicle Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Finished Vehicle Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Finished Vehicle Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Finished Vehicle Logistics Industry?

The projected CAGR is approximately 5.68%.

2. Which companies are prominent players in the North America Finished Vehicle Logistics Industry?

Key companies in the market include DB Schenker, CEVA Logistics AG, DHL, United Parcel Service Inc **List Not Exhaustive 7 3 Other Companie, GEODIS, Nippon Express Co Ltd, XPO Logistics Inc, KUEHNE + NAGEL International AG, DSV, Ryder System Inc.

3. What are the main segments of the North America Finished Vehicle Logistics Industry?

The market segments include Service, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 81.63 Million as of 2022.

5. What are some drivers contributing to market growth?

Environmental Concerns and Regulations; Technological Advancements in Automotive Technology.

6. What are the notable trends driving market growth?

Demand for Light Vehicle Production.

7. Are there any restraints impacting market growth?

Economic Uncertainty.

8. Can you provide examples of recent developments in the market?

December 2023: Government departments in the United States coordinated a wide range of funding initiatives for clean energy and circular economy to support the production of electric vehicles and batteries and improve logistics efficiency. To establish clean energy supply chains in locations affected by the closure of power plants or coal mines, the Department of Energy's Advanced Energy Manufacturing and Recycling Grant Programme will invest USD 250 million.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Finished Vehicle Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Finished Vehicle Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Finished Vehicle Logistics Industry?

To stay informed about further developments, trends, and reports in the North America Finished Vehicle Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence