Key Insights

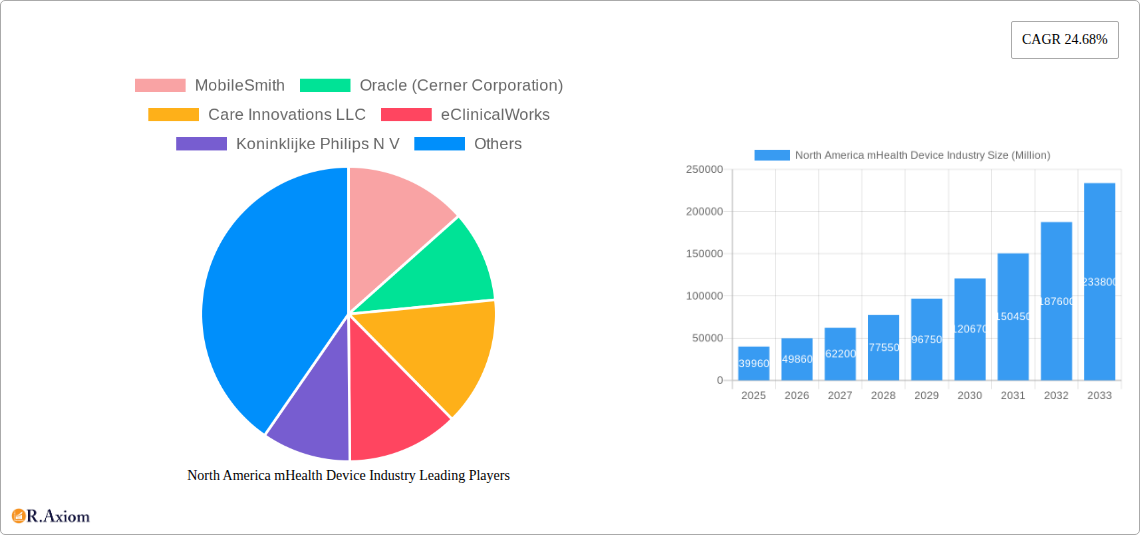

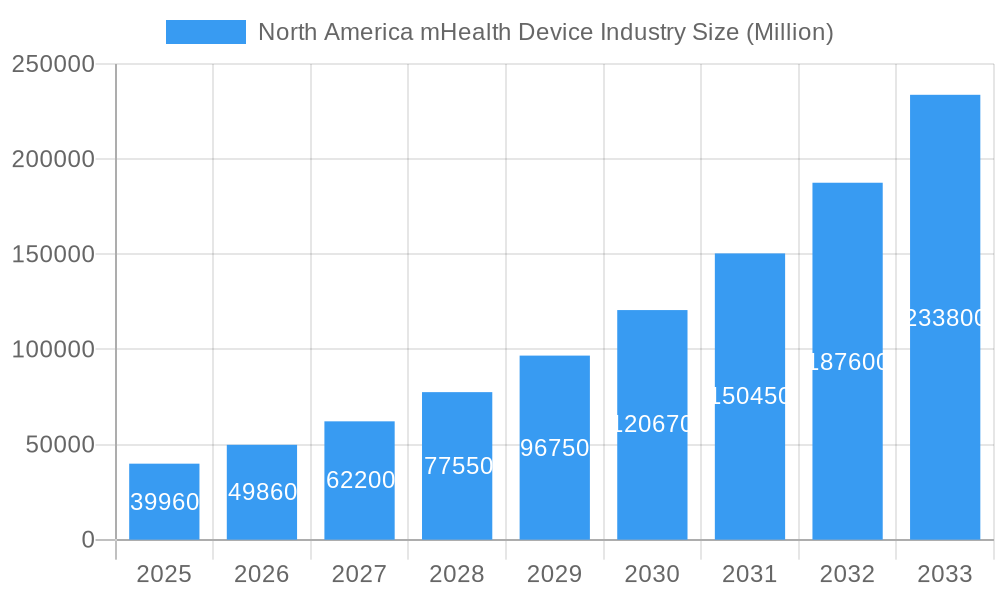

The North American mHealth device market is poised for substantial expansion, projected to reach USD 39.96 billion in 2025, with an impressive Compound Annual Growth Rate (CAGR) of 24.68% anticipated throughout the forecast period of 2025-2033. This robust growth is primarily fueled by an increasing prevalence of chronic diseases, a growing elderly population demanding continuous health monitoring, and the accelerating adoption of remote patient monitoring (RPM) solutions. The integration of advanced technologies like AI and IoT into mHealth devices is further enhancing their capabilities, enabling more personalized and proactive healthcare management. Furthermore, favorable government initiatives supporting digital health adoption and increasing consumer awareness regarding preventative healthcare are significant drivers. The market is witnessing a surge in demand for solutions that offer convenience, efficiency, and improved patient outcomes, positioning mHealth devices as indispensable tools in modern healthcare ecosystems.

North America mHealth Device Industry Market Size (In Billion)

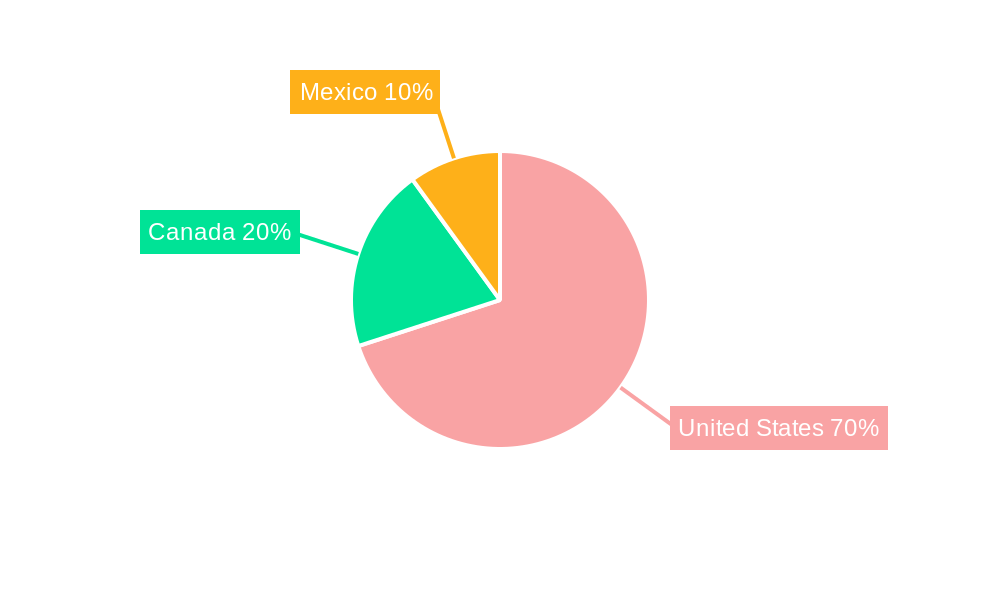

The market segmentation reveals a dynamic landscape with diverse service and device types contributing to its growth. Treatment services, encompassing independent aging solutions and chronic disease management, are gaining significant traction. Diagnostic and monitoring services, particularly remote patient monitoring devices and telemedicine solutions, are at the forefront of this revolution, offering continuous data collection and timely interventions. The widespread availability of connected devices like blood glucose monitors, cardiac monitors, and wearable health trackers is democratizing access to health data. Key stakeholders, including mobile operators, healthcare providers, and application content players, are actively collaborating to build a comprehensive mHealth ecosystem. Geographically, the United States is expected to dominate the market due to its advanced healthcare infrastructure, high disposable incomes, and early adoption of technological innovations, followed by Canada and Mexico, which are also witnessing a steady increase in mHealth device penetration.

North America mHealth Device Industry Company Market Share

This in-depth report provides a definitive analysis of the North America mHealth Device Industry, exploring its current landscape, historical performance, and projected trajectory through 2033. Delving into market concentration, innovation, key trends, dominant segments, product developments, and strategic outlooks, this report offers actionable insights for industry stakeholders including mobile operators, healthcare providers, application/content players, and device manufacturers. Leveraging high-traffic keywords, this report is optimized for search visibility, ensuring it reaches key decision-makers seeking to navigate and capitalize on this rapidly evolving market. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year, and the forecast period extending from 2025 to 2033, drawing from historical data from 2019 to 2024.

North America mHealth Device Industry Market Concentration & Innovation

The North America mHealth Device Industry exhibits a dynamic market concentration, characterized by a blend of established giants and agile innovators. Key players are actively investing in research and development, driving significant product innovation across various segments. Regulatory frameworks, such as those governed by the FDA, play a crucial role in shaping the market, ensuring product safety and efficacy, but also introducing compliance complexities. The threat of product substitutes is growing, with advancements in wearable technology and integrated healthcare platforms constantly emerging. End-user trends are increasingly focused on personalized health management, preventative care, and remote patient monitoring, fueling demand for sophisticated mHealth solutions. Mergers and acquisitions (M&A) activities are a significant feature, with deal values reaching hundreds of millions of dollars as companies seek to consolidate market share, acquire new technologies, and expand their service offerings. For instance, recent M&A activities indicate a strategic consolidation aimed at leveraging cross-platform synergies.

- Key Innovation Drivers:

- Advancements in sensor technology for more accurate data collection.

- Integration of Artificial Intelligence (AI) and Machine Learning (ML) for predictive analytics and personalized insights.

- Development of user-friendly interfaces and intuitive mobile applications.

- Increased focus on interoperability and data security protocols.

- Regulatory Landscape:

- FDA oversight for medical devices and software as a medical device (SaMD).

- HIPAA compliance for data privacy and security in the United States.

- Ongoing evolution of digital health regulations.

- M&A Activities:

- Strategic acquisitions to gain market share and technological expertise.

- Investments in startups developing novel mHealth solutions.

- Estimated M&A deal values in the range of $50 Million to $500 Million.

North America mHealth Device Industry Industry Trends & Insights

The North America mHealth Device Industry is experiencing robust growth, driven by a confluence of technological advancements, evolving consumer health consciousness, and increasing healthcare provider adoption. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 15-20% during the forecast period. Key growth drivers include the rising prevalence of chronic diseases, the growing demand for convenient and accessible healthcare services, and the increasing penetration of smartphones and wearable devices. Technological disruptions, such as the integration of 5G connectivity for faster data transmission and the development of advanced biosensors, are further accelerating market expansion. Consumer preferences are shifting towards proactive health management, with individuals seeking tools to monitor their well-being, manage chronic conditions, and engage in preventative care. The competitive dynamics are intensifying, with established healthcare technology companies, mobile device manufacturers, and innovative startups vying for market dominance. The market penetration of mHealth solutions is steadily increasing across all demographics, signifying a fundamental shift in how healthcare is delivered and consumed. The increasing adoption of remote patient monitoring devices, for example, is transforming chronic disease management and post-acute care, allowing for continuous patient oversight and timely interventions. This shift is further supported by advancements in telemedicine solutions, enabling remote consultations and diagnoses, thereby reducing the burden on physical healthcare facilities and improving patient access, especially in rural or underserved areas. The integration of wellness and fitness solutions into comprehensive mHealth platforms is also gaining traction, appealing to a broader consumer base interested in holistic health management.

Dominant Markets & Segments in North America mHealth Device Industry

The United States stands as the dominant market within the North America mHealth Device Industry, accounting for a substantial market share exceeding 75%. This dominance is attributed to its advanced healthcare infrastructure, high disposable income, significant investment in healthcare technology, and a large, tech-savvy population. Canada and Mexico follow, with their respective markets showing promising growth potential driven by increasing digital health adoption and government initiatives to improve healthcare accessibility.

Within Service Type, Monitoring Services are the largest and fastest-growing segment, encompassing Remote Patient Monitoring Devices, Medical , Telemedicine Solutions, and Post Acute Care Services. The demand for continuous patient oversight, particularly for chronic disease management and elder care, fuels this segment's growth.

- Key Drivers for Monitoring Services:

- Aging population and increasing need for independent living solutions.

- Rising prevalence of chronic conditions like diabetes, cardiovascular diseases, and respiratory illnesses.

- Healthcare provider focus on reducing hospital readmissions and improving patient outcomes.

- Reimbursement policies supporting remote patient monitoring.

Treatment Services, particularly Chronic Disease Management and Independent Aging Solutions, represent significant sub-segments, demonstrating strong growth as mHealth solutions become integral to long-term care and proactive health management. Diagnostic Services are also poised for expansion as mHealth devices integrate advanced diagnostic capabilities. Wellness and Fitness Solutions, while a more consumer-centric segment, continue to grow with increased awareness of preventative health.

In terms of Device Type, Remote Patient Monitoring Devices and Cardiac Monitors are leading segments, reflecting the critical need for continuous health surveillance. Blood Glucose Monitors remain essential for diabetes management. Respiratory Monitors are seeing increased demand due to the prevalence of respiratory conditions. Body and Temperature Monitors are becoming ubiquitous with consumer wearables.

The Stake Holder landscape is dominated by Healthcare Providers, who are increasingly integrating mHealth solutions into their clinical workflows to enhance patient care, improve efficiency, and reduce costs. Mobile Operators are crucial enablers, providing the necessary connectivity and platforms. Application/Content Players are vital in developing user-centric software that delivers value to patients and providers.

North America mHealth Device Industry Product Developments

Product innovation in the North America mHealth Device Industry is characterized by the development of more sophisticated, integrated, and user-friendly devices and applications. Companies are focusing on miniaturization, enhanced sensor accuracy, and improved battery life for wearable devices. The integration of AI and ML algorithms is enabling predictive diagnostics and personalized treatment recommendations. Applications are becoming more comprehensive, offering features like medication reminders, remote consultation capabilities, and seamless data sharing with healthcare providers. Competitive advantages are being gained through superior data analytics, robust security features, and effective integration with existing healthcare systems. The focus is on creating solutions that not only monitor health but also actively contribute to improved patient outcomes and proactive health management.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North America mHealth Device Industry, segmented by Service Type, Device Type, Stake Holder, and Geography.

- Service Type: This includes Treatment Services (Independent Aging Solutions, Chronic Disease Management), Diagnostic Services, Monitoring Services (Remote Patient Monitoring Devices, Medical , Telemedicine Solutions, Post Acute Care Services), Wellness and Fitness Solutions, and Other Services. Growth projections for Monitoring Services are robust, with an estimated market size of over $10 Billion by 2033, driven by increasing adoption in chronic disease management.

- Device Type: Key segments analyzed include Blood Glucose Monitors, Cardiac Monitors, Hemodynamic Monitors, Neurological Monitors, Respiratory Monitors, Body and Temperature Monitors, and Remote Patient Monitoring Devices. The Remote Patient Monitoring Devices segment is expected to witness a CAGR of over 18% during the forecast period.

- Stake Holder: The analysis covers Mobile Operators, Healthcare Providers, and Application/Content Players, with Healthcare Providers being the largest segment by market share and adoption rate.

- Geography: The report focuses on the United States, Canada, and Mexico, with the United States dominating the market due to its advanced healthcare ecosystem and higher adoption rates of digital health technologies.

Key Drivers of North America mHealth Device Industry Growth

The North America mHealth Device Industry is propelled by several key drivers. The escalating burden of chronic diseases necessitates continuous monitoring and proactive management, which mHealth devices effectively address. The rapid advancement in mobile technology, including the proliferation of smartphones and the increasing adoption of wearable devices, provides a robust platform for mHealth solutions. Supportive government initiatives and favorable reimbursement policies for telehealth and remote patient monitoring are also significant growth catalysts. Furthermore, a growing consumer awareness and demand for personalized, convenient, and accessible healthcare services are pushing individuals to embrace mHealth technologies for self-management and preventative care. The expansion of 5G networks promises to enhance the speed and reliability of data transmission, enabling more sophisticated real-time monitoring and telemedicine applications.

Challenges in the North America mHealth Device Industry Sector

Despite its strong growth potential, the North America mHealth Device Industry faces several challenges. Regulatory hurdles, including the complex approval processes for medical devices and the evolving landscape of data privacy regulations like HIPAA, can slow down innovation and market entry. Ensuring robust data security and patient privacy is paramount and requires continuous investment and vigilance against cyber threats. Interoperability issues between different mHealth devices, applications, and existing electronic health record (EHR) systems can hinder seamless data integration and workflow efficiency. High initial costs associated with advanced mHealth devices and the need for continuous technological upgrades can be a barrier for some healthcare providers and consumers. Moreover, the digital divide, particularly in rural or lower-income communities, can limit access to mHealth solutions, creating disparities in healthcare delivery.

Emerging Opportunities in North America mHealth Device Industry

Emerging opportunities in the North America mHealth Device Industry are vast and varied. The growing demand for personalized medicine presents a significant opportunity for mHealth devices that can collect and analyze granular patient data for tailored treatment plans. The expansion of the aging population fuels the need for independent living solutions and remote care technologies. The integration of AI and machine learning into mHealth platforms offers opportunities for predictive analytics, early disease detection, and personalized health coaching. The increasing focus on mental health and behavioral wellness is creating a market for mHealth applications designed to support emotional well-being and provide remote therapeutic interventions. Furthermore, the ongoing advancements in biosensor technology are paving the way for the development of non-invasive and highly accurate diagnostic tools that can be integrated into consumer devices. Partnerships between technology companies and healthcare organizations are crucial for leveraging these opportunities and driving widespread adoption.

Leading Players in the North America mHealth Device Industry Market

- MobileSmith

- Oracle (Cerner Corporation)

- Care Innovations LLC

- eClinicalWorks

- Koninklijke Philips N V

- Cisco Systems Inc

- Veradigm (Allscripts Healthcare LLC)

- Medtronic PLC

- Boston Scientific Corporation

- Telus Health

- AT&T Inc

- Apple Inc

- Samsung Healthcare Solutions

Key Developments in North America mHealth Device Industry Industry

- July 2022: AmerisourceBergen launched DTx Connect, a fully integrated ordering, dispensing, and fulfillment platform designed to facilitate patient access to physician-ordered digital therapeutics and diagnostics. DTx, a fast-expanding subset of digital health, utilizes software to offer clinical interventions directly to patients for the treatment, management, or prevention of various illnesses and disorders, including diabetes and behavioral health issues.

- May 2022: The University of Virginia (UVA) Health developed a smartphone application named HOPE (Heal, Overcome, Persist, Endure), aimed at providing patients with accessible and effective remote care.

Strategic Outlook for North America mHealth Device Industry Market

The strategic outlook for the North America mHealth Device Industry is exceptionally positive, driven by sustained innovation and increasing market acceptance. Future growth will be catalyzed by the deeper integration of mHealth solutions into mainstream healthcare ecosystems, facilitated by stronger interoperability standards and supportive regulatory environments. The expansion of AI-driven predictive analytics and personalized health insights will empower both patients and providers with more actionable information. The growing emphasis on preventative care and chronic disease management will continue to fuel demand for remote monitoring and telemedicine services. Strategic collaborations between technology developers, healthcare providers, and payers will be crucial for scaling successful mHealth models and ensuring equitable access. The industry is poised for continued disruption and growth, offering significant opportunities for companies that can deliver value-driven, secure, and user-centric mHealth solutions.

North America mHealth Device Industry Segmentation

-

1. Service Type

-

1.1. Treatment Services

- 1.1.1. Independent Aging Solutions

- 1.1.2. Chronic Disease Management

- 1.2. Diagnostic Services

-

1.3. Monitoring Services

- 1.3.1. Remote Patient Monitoring Devices

- 1.3.2. Medical

- 1.3.3. Telemedicine Solutions

- 1.3.4. Post Acute Care Services

- 1.4. Wellness and Fitness Solutions

- 1.5. Other Services

-

1.1. Treatment Services

-

2. Device Type

- 2.1. Blood Glucose Monitors

- 2.2. Cardiac Monitors

- 2.3. Hemodynamic Monitors

- 2.4. Neurological Monitors

- 2.5. Respiratory Monitors

- 2.6. Body and Temperature Monitors

- 2.7. Remote Patient Monitoring Devices

- 2.8. Other Device Types

-

3. Stake Holder

- 3.1. Mobile Operators

- 3.2. Healthcare Providers

- 3.3. Application/Content Players

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Mexico

North America mHealth Device Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America mHealth Device Industry Regional Market Share

Geographic Coverage of North America mHealth Device Industry

North America mHealth Device Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.68% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Treatment Services

- 5.1.1.1. Independent Aging Solutions

- 5.1.1.2. Chronic Disease Management

- 5.1.2. Diagnostic Services

- 5.1.3. Monitoring Services

- 5.1.3.1. Remote Patient Monitoring Devices

- 5.1.3.2. Medical

- 5.1.3.3. Telemedicine Solutions

- 5.1.3.4. Post Acute Care Services

- 5.1.4. Wellness and Fitness Solutions

- 5.1.5. Other Services

- 5.1.1. Treatment Services

- 5.2. Market Analysis, Insights and Forecast - by Device Type

- 5.2.1. Blood Glucose Monitors

- 5.2.2. Cardiac Monitors

- 5.2.3. Hemodynamic Monitors

- 5.2.4. Neurological Monitors

- 5.2.5. Respiratory Monitors

- 5.2.6. Body and Temperature Monitors

- 5.2.7. Remote Patient Monitoring Devices

- 5.2.8. Other Device Types

- 5.3. Market Analysis, Insights and Forecast - by Stake Holder

- 5.3.1. Mobile Operators

- 5.3.2. Healthcare Providers

- 5.3.3. Application/Content Players

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. North America mHealth Device Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Treatment Services

- 6.1.1.1. Independent Aging Solutions

- 6.1.1.2. Chronic Disease Management

- 6.1.2. Diagnostic Services

- 6.1.3. Monitoring Services

- 6.1.3.1. Remote Patient Monitoring Devices

- 6.1.3.2. Medical

- 6.1.3.3. Telemedicine Solutions

- 6.1.3.4. Post Acute Care Services

- 6.1.4. Wellness and Fitness Solutions

- 6.1.5. Other Services

- 6.1.1. Treatment Services

- 6.2. Market Analysis, Insights and Forecast - by Device Type

- 6.2.1. Blood Glucose Monitors

- 6.2.2. Cardiac Monitors

- 6.2.3. Hemodynamic Monitors

- 6.2.4. Neurological Monitors

- 6.2.5. Respiratory Monitors

- 6.2.6. Body and Temperature Monitors

- 6.2.7. Remote Patient Monitoring Devices

- 6.2.8. Other Device Types

- 6.3. Market Analysis, Insights and Forecast - by Stake Holder

- 6.3.1. Mobile Operators

- 6.3.2. Healthcare Providers

- 6.3.3. Application/Content Players

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. United States North America mHealth Device Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Treatment Services

- 7.1.1.1. Independent Aging Solutions

- 7.1.1.2. Chronic Disease Management

- 7.1.2. Diagnostic Services

- 7.1.3. Monitoring Services

- 7.1.3.1. Remote Patient Monitoring Devices

- 7.1.3.2. Medical

- 7.1.3.3. Telemedicine Solutions

- 7.1.3.4. Post Acute Care Services

- 7.1.4. Wellness and Fitness Solutions

- 7.1.5. Other Services

- 7.1.1. Treatment Services

- 7.2. Market Analysis, Insights and Forecast - by Device Type

- 7.2.1. Blood Glucose Monitors

- 7.2.2. Cardiac Monitors

- 7.2.3. Hemodynamic Monitors

- 7.2.4. Neurological Monitors

- 7.2.5. Respiratory Monitors

- 7.2.6. Body and Temperature Monitors

- 7.2.7. Remote Patient Monitoring Devices

- 7.2.8. Other Device Types

- 7.3. Market Analysis, Insights and Forecast - by Stake Holder

- 7.3.1. Mobile Operators

- 7.3.2. Healthcare Providers

- 7.3.3. Application/Content Players

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. Canada North America mHealth Device Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Treatment Services

- 8.1.1.1. Independent Aging Solutions

- 8.1.1.2. Chronic Disease Management

- 8.1.2. Diagnostic Services

- 8.1.3. Monitoring Services

- 8.1.3.1. Remote Patient Monitoring Devices

- 8.1.3.2. Medical

- 8.1.3.3. Telemedicine Solutions

- 8.1.3.4. Post Acute Care Services

- 8.1.4. Wellness and Fitness Solutions

- 8.1.5. Other Services

- 8.1.1. Treatment Services

- 8.2. Market Analysis, Insights and Forecast - by Device Type

- 8.2.1. Blood Glucose Monitors

- 8.2.2. Cardiac Monitors

- 8.2.3. Hemodynamic Monitors

- 8.2.4. Neurological Monitors

- 8.2.5. Respiratory Monitors

- 8.2.6. Body and Temperature Monitors

- 8.2.7. Remote Patient Monitoring Devices

- 8.2.8. Other Device Types

- 8.3. Market Analysis, Insights and Forecast - by Stake Holder

- 8.3.1. Mobile Operators

- 8.3.2. Healthcare Providers

- 8.3.3. Application/Content Players

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Mexico North America mHealth Device Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 9.1.1. Treatment Services

- 9.1.1.1. Independent Aging Solutions

- 9.1.1.2. Chronic Disease Management

- 9.1.2. Diagnostic Services

- 9.1.3. Monitoring Services

- 9.1.3.1. Remote Patient Monitoring Devices

- 9.1.3.2. Medical

- 9.1.3.3. Telemedicine Solutions

- 9.1.3.4. Post Acute Care Services

- 9.1.4. Wellness and Fitness Solutions

- 9.1.5. Other Services

- 9.1.1. Treatment Services

- 9.2. Market Analysis, Insights and Forecast - by Device Type

- 9.2.1. Blood Glucose Monitors

- 9.2.2. Cardiac Monitors

- 9.2.3. Hemodynamic Monitors

- 9.2.4. Neurological Monitors

- 9.2.5. Respiratory Monitors

- 9.2.6. Body and Temperature Monitors

- 9.2.7. Remote Patient Monitoring Devices

- 9.2.8. Other Device Types

- 9.3. Market Analysis, Insights and Forecast - by Stake Holder

- 9.3.1. Mobile Operators

- 9.3.2. Healthcare Providers

- 9.3.3. Application/Content Players

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. United States

- 9.4.2. Canada

- 9.4.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 MobileSmith

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Oracle (Cerner Corporation)

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Care Innovations LLC

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 eClinicalWorks

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Koninklijke Philips N V

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Cisco Systems Inc

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Veradigm (Allscripts Healthcare LLC)

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Medtronic PLC

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Boston Scientific Corporation

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Telus Health

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 AT&T Inc

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Apple Inc

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.13 Samsung Healthcare Solutions

- 10.1.13.1. Company Overview

- 10.1.13.2. Products

- 10.1.13.3. Company Financials

- 10.1.13.4. SWOT Analysis

- 10.1.1 MobileSmith

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America mHealth Device Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America mHealth Device Industry Share (%) by Company 2025

List of Tables

- Table 1: North America mHealth Device Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 2: North America mHealth Device Industry Volume K Unit Forecast, by Service Type 2020 & 2033

- Table 3: North America mHealth Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 4: North America mHealth Device Industry Volume K Unit Forecast, by Device Type 2020 & 2033

- Table 5: North America mHealth Device Industry Revenue Million Forecast, by Stake Holder 2020 & 2033

- Table 6: North America mHealth Device Industry Volume K Unit Forecast, by Stake Holder 2020 & 2033

- Table 7: North America mHealth Device Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: North America mHealth Device Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 9: North America mHealth Device Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 10: North America mHealth Device Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: North America mHealth Device Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 12: North America mHealth Device Industry Volume K Unit Forecast, by Service Type 2020 & 2033

- Table 13: North America mHealth Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 14: North America mHealth Device Industry Volume K Unit Forecast, by Device Type 2020 & 2033

- Table 15: North America mHealth Device Industry Revenue Million Forecast, by Stake Holder 2020 & 2033

- Table 16: North America mHealth Device Industry Volume K Unit Forecast, by Stake Holder 2020 & 2033

- Table 17: North America mHealth Device Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: North America mHealth Device Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 19: North America mHealth Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: North America mHealth Device Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 21: North America mHealth Device Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 22: North America mHealth Device Industry Volume K Unit Forecast, by Service Type 2020 & 2033

- Table 23: North America mHealth Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 24: North America mHealth Device Industry Volume K Unit Forecast, by Device Type 2020 & 2033

- Table 25: North America mHealth Device Industry Revenue Million Forecast, by Stake Holder 2020 & 2033

- Table 26: North America mHealth Device Industry Volume K Unit Forecast, by Stake Holder 2020 & 2033

- Table 27: North America mHealth Device Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 28: North America mHealth Device Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 29: North America mHealth Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: North America mHealth Device Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: North America mHealth Device Industry Revenue Million Forecast, by Service Type 2020 & 2033

- Table 32: North America mHealth Device Industry Volume K Unit Forecast, by Service Type 2020 & 2033

- Table 33: North America mHealth Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 34: North America mHealth Device Industry Volume K Unit Forecast, by Device Type 2020 & 2033

- Table 35: North America mHealth Device Industry Revenue Million Forecast, by Stake Holder 2020 & 2033

- Table 36: North America mHealth Device Industry Volume K Unit Forecast, by Stake Holder 2020 & 2033

- Table 37: North America mHealth Device Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 38: North America mHealth Device Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 39: North America mHealth Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: North America mHealth Device Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America mHealth Device Industry?

The projected CAGR is approximately 24.68%.

2. Which companies are prominent players in the North America mHealth Device Industry?

Key companies in the market include MobileSmith, Oracle (Cerner Corporation), Care Innovations LLC, eClinicalWorks, Koninklijke Philips N V, Cisco Systems Inc, Veradigm (Allscripts Healthcare LLC), Medtronic PLC, Boston Scientific Corporation, Telus Health, AT&T Inc, Apple Inc, Samsung Healthcare Solutions.

3. What are the main segments of the North America mHealth Device Industry?

The market segments include Service Type, Device Type, Stake Holder, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 39.96 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Use of Smart Consumer Devices for Varied Applications; Increasing Investments in Personalized Medicine and Patient Centric Approach; Increasing Awareness and Demand for Point of Care Diagnosis and Treatment.

6. What are the notable trends driving market growth?

Remote Patient Monitoring Devices are Estimated to Hold a Significant Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Data Privacy Issues.

8. Can you provide examples of recent developments in the market?

July 2022: AmerisourceBergen launched DTx Connect, a fully integrated ordering, dispensing, and fulfillment platform that aims to facilitate patient access to physician-ordered digital therapeutics and diagnostics DTx, a fast-expanding subset of digital health, uses software to offer clinical interventions to patients directly to treat, manage, or prevent a wide range of illnesses and disorders, such as diabetes and behavioral health issues.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America mHealth Device Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America mHealth Device Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America mHealth Device Industry?

To stay informed about further developments, trends, and reports in the North America mHealth Device Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence