Key Insights

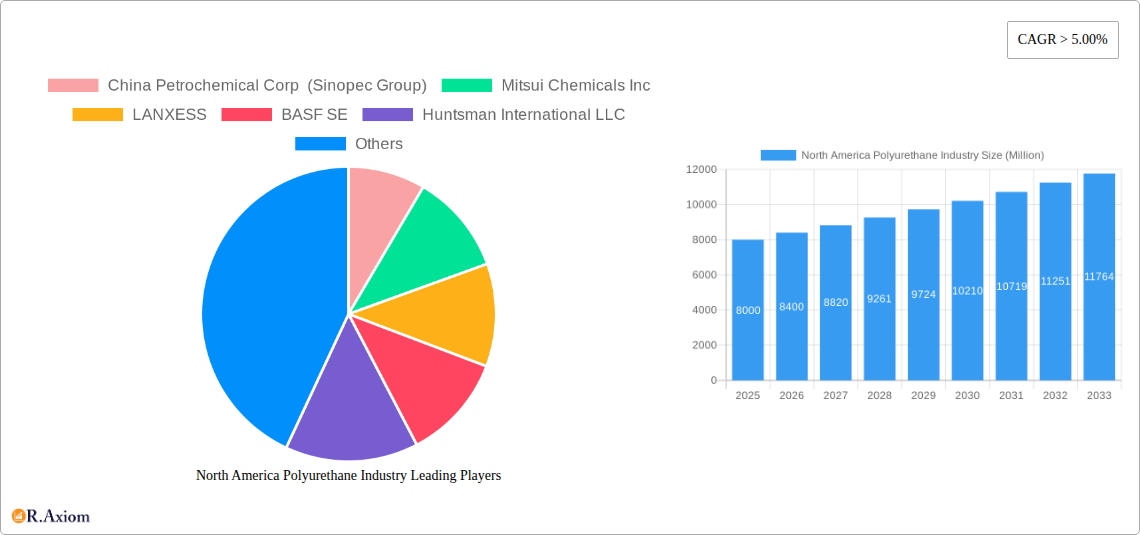

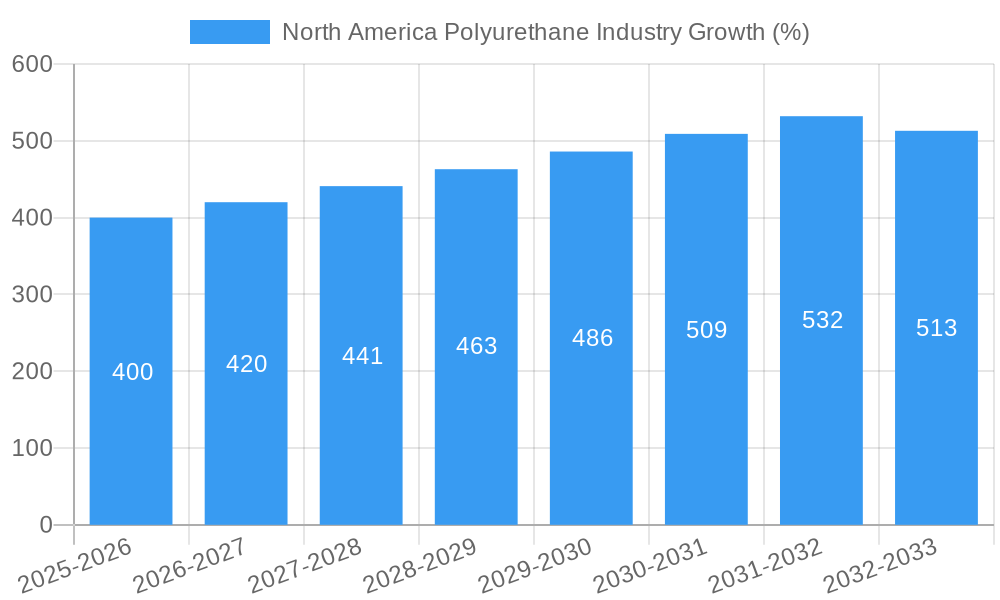

The North American polyurethane market, valued at approximately $8 billion in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 5% from 2025 to 2033. This expansion is driven by several key factors. The burgeoning construction sector, fueled by infrastructure development and residential construction, significantly boosts demand for polyurethane foams in insulation and building materials. Simultaneously, the automotive and transportation industries' increasing adoption of lightweight and high-performance polyurethane components, such as dashboards and seat cushions, contributes to market growth. Furthermore, the expanding electronics and appliances market requires polyurethane for cushioning, insulation, and sealing applications. While raw material price fluctuations and environmental concerns regarding polyurethane production present challenges, ongoing innovation in sustainable polyurethane formulations and recycling technologies are mitigating these restraints. The flexible foam segment, encompassing coatings, adhesives, sealants, and binders, shows particularly strong growth potential, driven by its versatility across various applications. Within the end-user industries, furniture and interiors consistently demonstrate high demand for polyurethane-based foams, reflecting consumer preferences for comfort and durability. Competition among major players like BASF, Dow, and Huntsman, alongside regional manufacturers, fosters innovation and price competitiveness.

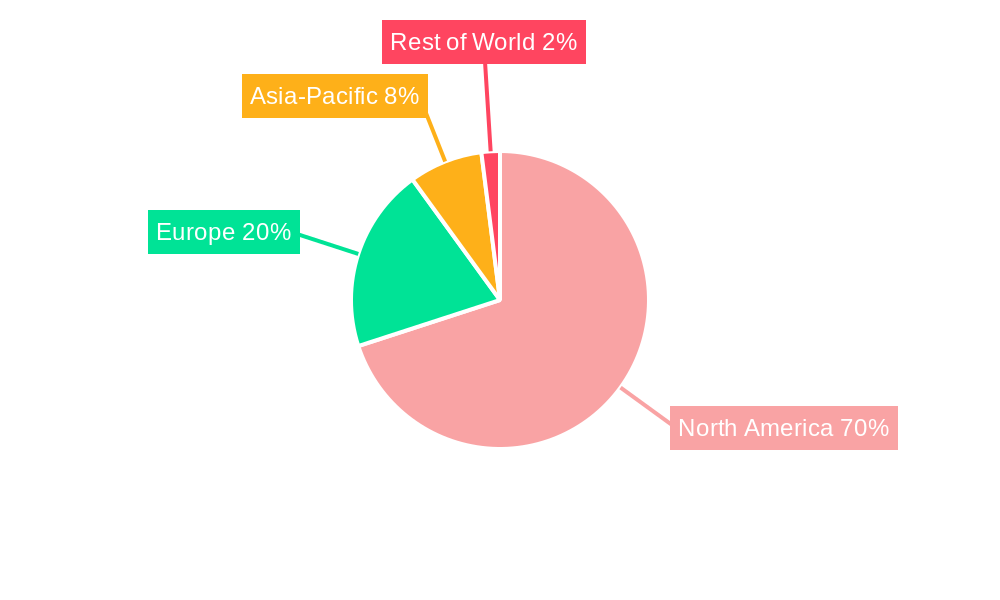

Looking ahead, the North American polyurethane market will experience sustained growth, albeit with a potential moderation in the CAGR towards the latter half of the forecast period (2030-2033) due to predicted market saturation in certain segments. Continued growth in sustainable and high-performance polyurethane applications will be pivotal in maintaining the market's upward trajectory. Regional variations exist, with the United States dominating the North American market due to its significant manufacturing base and robust construction and automotive sectors. Canada and Mexico will experience moderate growth, propelled by increasing industrialization and infrastructure investments. However, government regulations targeting environmentally harmful substances and the development of bio-based polyurethane alternatives are likely to reshape the market landscape in the coming years, favoring companies with a strong focus on sustainability and innovation.

North America Polyurethane Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North America polyurethane industry, covering market size, segmentation, growth drivers, challenges, and future opportunities. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report offers actionable insights for industry stakeholders, including manufacturers, suppliers, distributors, and investors.

North America Polyurethane Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the North America polyurethane industry, examining market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and M&A activities. The industry is characterized by a moderately concentrated market structure, with key players holding significant market share. For instance, BASF SE and Dow collectively hold an estimated xx% of the market (2025). However, the presence of several smaller players fosters competition.

- Market Concentration: The Herfindahl-Hirschman Index (HHI) is estimated at xx in 2025, indicating a moderately concentrated market.

- Innovation Drivers: Growing demand for high-performance materials in automotive and construction sectors drives innovation in polyurethane chemistry, leading to the development of sustainable and high-performance products.

- Regulatory Framework: Stringent environmental regulations regarding VOC emissions and the use of hazardous chemicals are shaping product development and manufacturing processes.

- Product Substitutes: Competition from alternative materials, such as bio-based polymers, is increasing, necessitating continuous innovation and cost optimization within the polyurethane industry.

- End-User Trends: The increasing focus on energy efficiency and lightweight designs in the automotive and construction sectors is fueling demand for specific polyurethane formulations.

- M&A Activities: The industry has witnessed several significant M&A activities in recent years, valued at approximately $xx Million in the period 2019-2024, driven by companies’ strategies to expand their product portfolios and market reach. These deals primarily involved acquisitions of smaller specialized firms with unique technologies.

North America Polyurethane Industry Industry Trends & Insights

The North America polyurethane industry is witnessing robust growth, driven by the increasing demand across various end-use sectors. The market is expected to exhibit a CAGR of xx% during the forecast period (2025-2033), reaching a projected value of $xx Million by 2033. Key factors driving this growth include rising construction activities, increasing automotive production, and the growing popularity of polyurethane-based furniture and appliances. Technological advancements, such as the development of bio-based polyurethanes and improved manufacturing processes, are further enhancing the market's growth trajectory. The market penetration of high-performance polyurethanes, particularly in the automotive and aerospace sectors, is also significant, exceeding xx% in 2025. However, fluctuating raw material prices and intensifying competition pose challenges to sustained growth. Consumer preference shifts towards eco-friendly and sustainable products also influence the market, driving innovation in bio-based and recycled polyurethane materials. Competitive dynamics are intense, with major players focusing on product differentiation, cost reduction, and technological advancements to maintain market share.

Dominant Markets & Segments in North America Polyurethane Industry

The building and construction sector is the dominant end-user industry for polyurethanes in North America, accounting for an estimated xx% of the total market value in 2025. This dominance is driven by the extensive use of polyurethane foams in insulation, roofing, and other building applications. The flexible foam segment holds a significant share within the applications market, predominantly used in furniture and bedding. The coatings, adhesives, sealants, and binders segment also shows significant growth potential, largely attributed to rising demand in various industrial applications.

Key Drivers for Building and Construction Dominance:

- Robust infrastructure development programs.

- Stringent energy efficiency regulations.

- Growing demand for sustainable building materials.

- Increased investments in residential and commercial construction.

Dominance Analysis: The strong growth in the building and construction sector, coupled with the increasing use of polyurethane in insulation and other applications, solidifies its position as the leading segment. The automotive and transportation segment also demonstrates considerable growth, fueled by the demand for lightweight and high-performance materials.

North America Polyurethane Industry Product Developments

Recent innovations focus on developing sustainable and high-performance polyurethanes. This includes bio-based polyurethanes derived from renewable resources and recycled polyurethane foams offering environmentally friendly alternatives. These new materials aim to address concerns about the environmental impact of traditional polyurethane production while enhancing properties such as durability and thermal efficiency. The market fit is excellent, driven by growing consumer demand for sustainable products and stringent environmental regulations. Technological trends lean towards incorporating recycled content and utilizing renewable feedstocks.

Report Scope & Segmentation Analysis

This report segments the North America polyurethane market by application (foams, flexible foams, coatings, adhesives, sealants, and binders, elastomers, other applications) and end-user industry (furniture and interiors, building and construction, electronics and appliances, automotive and transportation, packaging, other end-user industries). Each segment’s growth projections, market size, and competitive dynamics are analyzed. The building and construction segment is expected to witness the fastest growth, driven by robust infrastructure development. The automotive and transportation segment exhibits significant growth due to increasing demand for lightweight and energy-efficient vehicles. The flexible foam segment benefits from the growth in the furniture and bedding industries.

Key Drivers of North America Polyurethane Industry Growth

Growth is fueled by several factors: increasing construction activities, particularly in infrastructure projects and residential buildings; rising demand from the automotive industry for lightweight and high-performance materials; and the growth in furniture and bedding manufacturing. Government initiatives promoting energy efficiency and sustainable building practices are also significant drivers. Technological advancements, particularly in sustainable and high-performance polyurethane formulations, enhance market growth.

Challenges in the North America Polyurethane Industry Sector

The industry faces challenges such as fluctuating raw material prices, especially isocyanates and polyols, impacting production costs and profitability. Supply chain disruptions, amplified by geopolitical events, pose logistical and cost-related obstacles. Intense competition from established players and the emergence of new entrants pressure margins. Environmental regulations regarding VOC emissions necessitate continuous innovation in cleaner production processes.

Emerging Opportunities in North America Polyurethane Industry

Emerging opportunities exist in developing bio-based and recycled polyurethanes, catering to the growing demand for sustainable materials. The expanding construction sector in developing economies presents significant market expansion potential. Innovation in high-performance polyurethane formulations for niche applications like aerospace and medical devices offers growth prospects. Exploring new applications of polyurethane in energy-efficient technologies, such as insulation and renewable energy systems, provides future opportunities.

Leading Players in the North America Polyurethane Industry Market

- China Petrochemical Corp (Sinopec Group)

- Mitsui Chemicals Inc

- LANXESS

- BASF SE

- Huntsman International LLC

- Fujian Southeast Electrochemical Co Ltd

- Dow

- Covestro AG

- Tosoh Corporation

- Perstorp

Key Developments in North America Polyurethane Industry Industry

- 2023 Q2: BASF SE announced a significant investment in expanding its polyurethane production capacity in North America.

- 2022 Q4: Covestro AG launched a new line of bio-based polyurethanes.

- 2021 Q3: Huntsman International LLC acquired a smaller polyurethane manufacturer, expanding its market share. (Further details on specific acquisitions and launches require additional research for accurate year and month).

Strategic Outlook for North America Polyurethane Industry Market

The North America polyurethane industry is poised for continued growth, driven by strong demand from key sectors and ongoing innovations in sustainable and high-performance materials. The increasing focus on energy efficiency and the development of novel applications will shape future market dynamics. Companies that successfully adapt to evolving consumer preferences and regulatory landscapes while investing in research and development will be best positioned to capture future market opportunities. The market’s long-term potential remains robust, offering promising prospects for both established players and new entrants.

North America Polyurethane Industry Segmentation

-

1. Application

- 1.1. Foams

- 1.2. Coatings

- 1.3. Adhesives, Sealants, and Binders

- 1.4. Elastomers

- 1.5. Other Applications

-

2. End-user Industry

- 2.1. Furniture and Interiors

- 2.2. Building and Construction

- 2.3. Electronics and Appliances

- 2.4. Automotive and Transportation

- 2.5. Packaging

- 2.6. Other End-user Industries

-

3. Geography

- 3.1. United States

- 3.2. Mexico

- 3.3. Canada

- 3.4. Rest of North America

North America Polyurethane Industry Segmentation By Geography

- 1. United States

- 2. Mexico

- 3. Canada

- 4. Rest of North America

North America Polyurethane Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Increasing Use of Durable Plastics in Construction; Increasing Emphasis on Recycling

- 3.3. Market Restrains

- 3.3.1. ; Volatile Raw Material Prices; Competition from Polystyrene and Polypropylene Foam

- 3.4. Market Trends

- 3.4.1. Foams Application is Expected to Hold the Largest Share of the Application Segment

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Foams

- 5.1.2. Coatings

- 5.1.3. Adhesives, Sealants, and Binders

- 5.1.4. Elastomers

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Furniture and Interiors

- 5.2.2. Building and Construction

- 5.2.3. Electronics and Appliances

- 5.2.4. Automotive and Transportation

- 5.2.5. Packaging

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Mexico

- 5.3.3. Canada

- 5.3.4. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Mexico

- 5.4.3. Canada

- 5.4.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. United States North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Foams

- 6.1.2. Coatings

- 6.1.3. Adhesives, Sealants, and Binders

- 6.1.4. Elastomers

- 6.1.5. Other Applications

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Furniture and Interiors

- 6.2.2. Building and Construction

- 6.2.3. Electronics and Appliances

- 6.2.4. Automotive and Transportation

- 6.2.5. Packaging

- 6.2.6. Other End-user Industries

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Mexico

- 6.3.3. Canada

- 6.3.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Mexico North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Foams

- 7.1.2. Coatings

- 7.1.3. Adhesives, Sealants, and Binders

- 7.1.4. Elastomers

- 7.1.5. Other Applications

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Furniture and Interiors

- 7.2.2. Building and Construction

- 7.2.3. Electronics and Appliances

- 7.2.4. Automotive and Transportation

- 7.2.5. Packaging

- 7.2.6. Other End-user Industries

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Mexico

- 7.3.3. Canada

- 7.3.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Canada North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Foams

- 8.1.2. Coatings

- 8.1.3. Adhesives, Sealants, and Binders

- 8.1.4. Elastomers

- 8.1.5. Other Applications

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Furniture and Interiors

- 8.2.2. Building and Construction

- 8.2.3. Electronics and Appliances

- 8.2.4. Automotive and Transportation

- 8.2.5. Packaging

- 8.2.6. Other End-user Industries

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Mexico

- 8.3.3. Canada

- 8.3.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Rest of North America North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Foams

- 9.1.2. Coatings

- 9.1.3. Adhesives, Sealants, and Binders

- 9.1.4. Elastomers

- 9.1.5. Other Applications

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Furniture and Interiors

- 9.2.2. Building and Construction

- 9.2.3. Electronics and Appliances

- 9.2.4. Automotive and Transportation

- 9.2.5. Packaging

- 9.2.6. Other End-user Industries

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Mexico

- 9.3.3. Canada

- 9.3.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. United States North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 11. Canada North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 12. Mexico North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 13. Rest of North America North America Polyurethane Industry Analysis, Insights and Forecast, 2019-2031

- 14. Competitive Analysis

- 14.1. Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 China Petrochemical Corp (Sinopec Group)

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Mitsui Chemicals Inc

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 LANXESS

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 BASF SE

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Huntsman International LLC

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Fujian Southeast Electrochemical Co Ltd

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Dow

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Covestro AG

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Tosoh Corporation

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Perstorp

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.1 China Petrochemical Corp (Sinopec Group)

List of Figures

- Figure 1: North America Polyurethane Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Polyurethane Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Polyurethane Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Region 2019 & 2032

- Table 3: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 5: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 6: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 7: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 9: North America Polyurethane Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Region 2019 & 2032

- Table 11: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 13: United States North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: United States North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 15: Canada North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Mexico North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 19: Rest of North America North America Polyurethane Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of North America North America Polyurethane Industry Volume (kilograms per cubic meter) Forecast, by Application 2019 & 2032

- Table 21: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 22: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 23: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 24: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 25: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 27: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 29: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 30: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 31: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 32: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 33: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 34: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 35: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 36: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 37: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 38: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 39: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 40: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 41: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 42: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 43: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 44: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

- Table 45: North America Polyurethane Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 46: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Application 2019 & 2032

- Table 47: North America Polyurethane Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 48: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by End-user Industry 2019 & 2032

- Table 49: North America Polyurethane Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 50: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Geography 2019 & 2032

- Table 51: North America Polyurethane Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 52: North America Polyurethane Industry Volume kilograms per cubic meter Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Polyurethane Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the North America Polyurethane Industry?

Key companies in the market include China Petrochemical Corp (Sinopec Group), Mitsui Chemicals Inc, LANXESS, BASF SE, Huntsman International LLC, Fujian Southeast Electrochemical Co Ltd, Dow, Covestro AG, Tosoh Corporation, Perstorp.

3. What are the main segments of the North America Polyurethane Industry?

The market segments include Application, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Use of Durable Plastics in Construction; Increasing Emphasis on Recycling.

6. What are the notable trends driving market growth?

Foams Application is Expected to Hold the Largest Share of the Application Segment.

7. Are there any restraints impacting market growth?

; Volatile Raw Material Prices; Competition from Polystyrene and Polypropylene Foam.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in kilograms per cubic meter.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Polyurethane Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Polyurethane Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Polyurethane Industry?

To stay informed about further developments, trends, and reports in the North America Polyurethane Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence