Key Insights

The North America structural steel fabrication market, valued at approximately $179.04 billion in 2025, is projected to experience robust growth. This expansion is driven by a compound annual growth rate (CAGR) of 9% from 2025 to 2033. Key growth drivers include the expanding construction sector, particularly in infrastructure development (roads, bridges, public transportation) and commercial real estate, which significantly boosts demand for steel fabrication. Furthermore, the increasing need for sustainable and resilient infrastructure promotes the adoption of advanced fabrication techniques, enhancing structural integrity and longevity. Government initiatives focused on infrastructure modernization and urban renewal projects across the US and Canada also support market growth. Technological advancements in automated welding and cutting systems improve efficiency and reduce production costs, increasing market competitiveness.

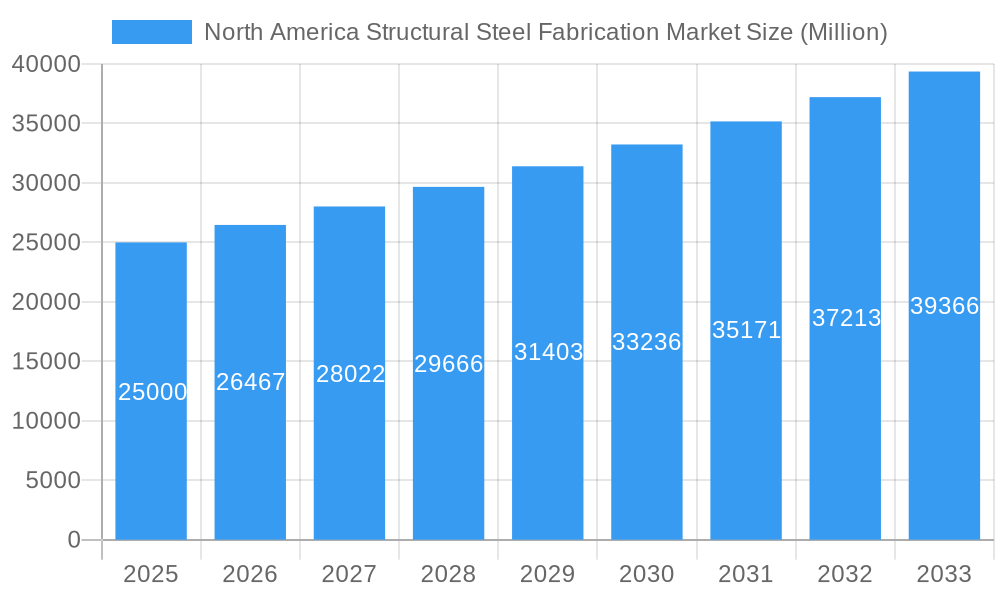

North America Structural Steel Fabrication Market Market Size (In Billion)

Challenges include fluctuating steel prices due to global supply chain dynamics and raw material availability. Skilled labor shortages in fabrication can constrain production capacity and increase labor costs. However, ongoing worker training and automation efforts are mitigating these effects. The competitive landscape features multinational corporations and regional players. Established companies like Valmont Industries Inc. and Cornerstone Building Brands Inc. hold significant market share, while smaller firms specialize in niche applications. The market is segmented by diverse applications, including infrastructure, high-rise buildings, and industrial structures. The forecast period (2025-2033) anticipates continued expansion driven by ongoing infrastructure investment and technological improvements.

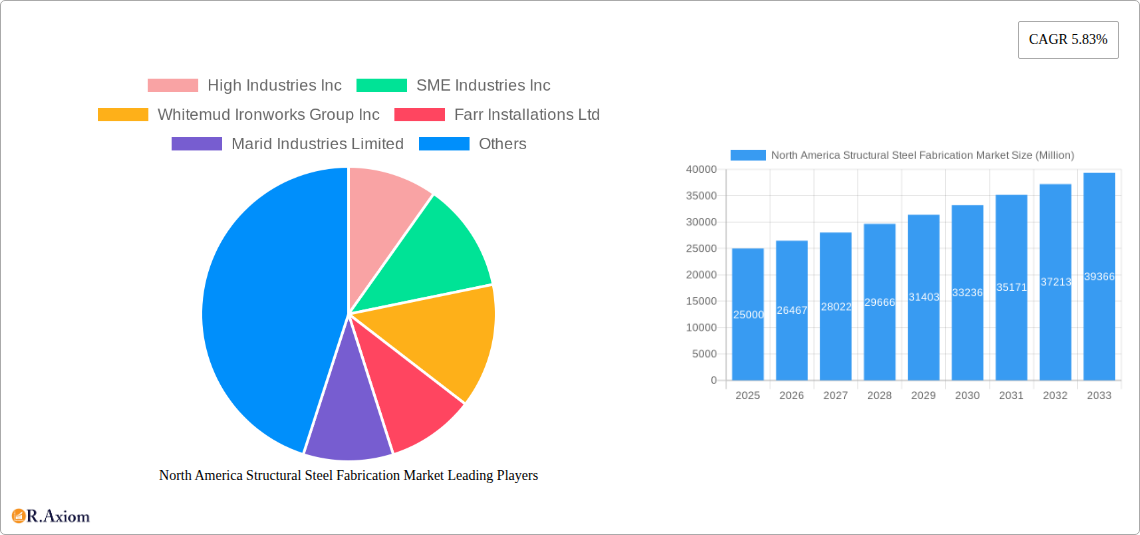

North America Structural Steel Fabrication Market Company Market Share

North America Structural Steel Fabrication Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North America Structural Steel Fabrication market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with 2025 as the base year, this report meticulously examines market dynamics, growth drivers, challenges, and future opportunities. The study incorporates detailed segmentation analysis, competitive landscapes, and key industry developments, equipping readers with actionable intelligence to navigate this dynamic market.

North America Structural Steel Fabrication Market Market Concentration & Innovation

The North America structural steel fabrication market exhibits a moderately concentrated structure, with a few large players holding significant market share. Precise market share data for individual companies is proprietary and not publicly disclosed; however, analysis suggests that the top five players collectively control approximately xx% of the market, while numerous smaller, regional fabricators account for the remaining share. This concentration is largely influenced by economies of scale, technological advancements, and access to capital. Innovation within the sector focuses on optimizing fabrication processes, enhancing material properties (e.g., higher-strength steels), and leveraging advanced technologies such as Building Information Modeling (BIM) and automation. Regulatory frameworks, including building codes and safety standards, strongly influence design and fabrication practices. Substitute materials like concrete and composite materials pose some competitive pressure but remain largely niche applications compared to structural steel. End-user trends favoring sustainable and efficient construction methods fuel innovation in lighter, more sustainable steel fabrication techniques. Mergers and acquisitions (M&A) activity is a prominent feature, with recent transactions impacting market consolidation and influencing technological capabilities. For example, several significant acquisitions have occurred in the recent past, involving deal values ranging from xx Million to xx Million, further shaping the market landscape.

North America Structural Steel Fabrication Market Industry Trends & Insights

The North America structural steel fabrication market is on a significant upward trajectory, projected to expand at a robust Compound Annual Growth Rate (CAGR) of approximately 5.5% to 6.5% during the forecast period (2025-2033). This accelerated growth is primarily fueled by substantial investments in infrastructure revitalization and expansion across the continent. Key sectors driving this demand include the transportation industry (highways, bridges, airports, and rail), the burgeoning energy sector (including renewable energy infrastructure like wind farms and solar installations), and the resilient commercial construction segment (offices, retail spaces, and entertainment venues). Furthermore, the market is experiencing a transformative shift with the increasing adoption of advanced fabrication technologies. Innovations such as high-precision laser cutting, automated robotic welding, and sophisticated CNC machining are revolutionizing the industry by significantly boosting production efficiency, elevating fabrication accuracy, and driving down operational labor costs. A growing emphasis on sustainable construction practices is also shaping market dynamics, leading to an increased demand for high-performance, durable steels and the implementation of environmentally conscious fabrication processes. Evolving consumer preferences for aesthetically pleasing, architecturally innovative, and structurally sound buildings are compelling fabricators to embrace cutting-edge design methodologies and sophisticated fabrication solutions. The competitive landscape is characterized by a dynamic interplay of intense price competition, especially among smaller and regional fabricators. However, leading players are strategically differentiating themselves by leveraging their advanced technological capabilities, offering specialized value-added services, and optimizing their supply chain management to ensure reliability and cost-effectiveness.

Dominant Markets & Segments in North America Structural Steel Fabrication Market

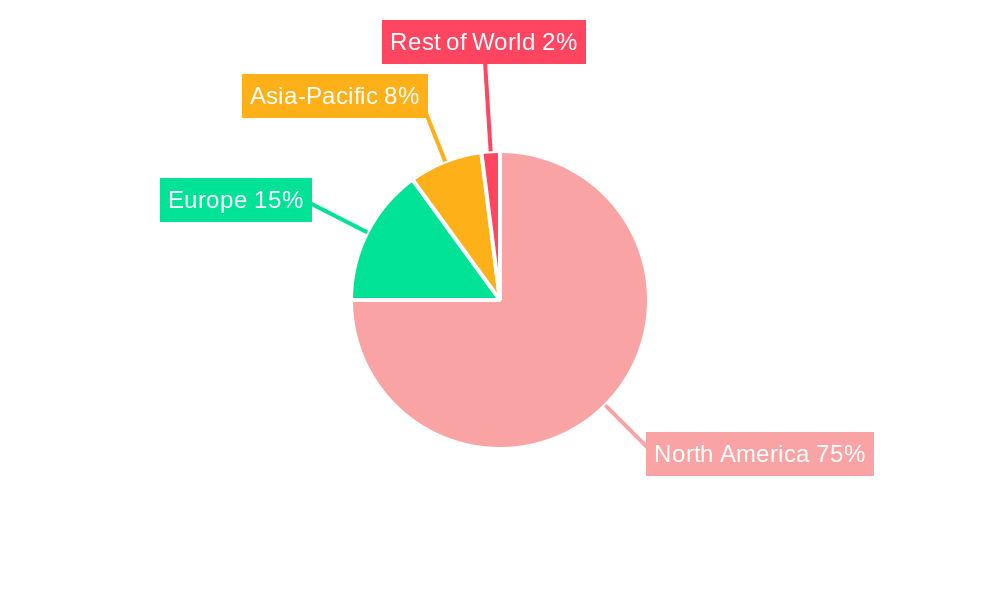

The United States unequivocally leads the North American structural steel fabrication market, commanding an estimated share of over 70% to 75% of the total market value. This pronounced dominance is a direct consequence of the nation's exceptionally robust and diverse construction industry, its ongoing commitment to large-scale infrastructure development projects, and historically favorable economic conditions that foster consistent investment. Canada represents a significant, albeit smaller, market with a notable share. The growth of the Mexican market is also noteworthy, driven by its expanding industrial and infrastructure sectors.

Key Drivers of US Market Dominance:

- Thriving Construction Ecosystem: Sustained and substantial investment from both private enterprises and public entities across a broad spectrum of construction projects, from residential developments to large commercial complexes and industrial facilities.

- Expansive Infrastructure Investment Agenda: Significant and ongoing federal, state, and local government funding allocated towards the modernization and expansion of vital infrastructure, including highways, bridges, public transportation networks, and energy grids.

- Conducive Economic Environment: Generally stable and predictable macroeconomic conditions that historically encourage robust business activity and consumer confidence, thereby stimulating demand for construction and related services.

Detailed Dominance Analysis: The sheer scale and consistent growth momentum of the US market are underpinned by persistent demand from a wide array of sectors, including commercial real estate, residential housing, and industrial manufacturing. Complementing this, proactive government initiatives aimed at bolstering infrastructure development further solidify its position. The substantial size and inherent diversity of the US market enable larger-scale fabricators to achieve significant economies of scale, thereby establishing a pronounced competitive advantage over smaller, more localized players.

North America Structural Steel Fabrication Market Product Developments

Recent product innovations center on high-strength low-alloy (HSLA) steels, which offer superior strength-to-weight ratios, reducing material costs and enhancing structural performance. Advanced fabrication techniques, like automated welding and laser cutting, improve precision and speed. These advancements enhance cost-effectiveness, sustainability, and the overall quality of fabricated structures, providing significant competitive advantages for companies embracing these technologies. Market fit for these innovations is driven by the construction industry's need for efficient, durable, and cost-effective solutions.

Report Scope & Segmentation Analysis

This report segments the North America structural steel fabrication market by several key factors, including product type (beams, columns, plates, etc.), end-use industry (construction, infrastructure, energy, etc.), and region (United States and Canada). Each segment is analyzed to determine growth potential, market size, and competitive dynamics. Growth projections vary significantly across segments, depending on industry-specific trends and the impact of economic factors. For instance, the infrastructure segment is expected to show strong growth driven by government investment, whereas the commercial sector may experience fluctuating growth, influenced by macroeconomic conditions. Competitive landscapes also differ across these segments, with some featuring higher levels of competition than others.

Key Drivers of North America Structural Steel Fabrication Market Growth

The North American structural steel fabrication market is propelled by a confluence of powerful growth catalysts. Foremost among these is the vigorous implementation of widespread infrastructure development programs across the continent. These initiatives encompass ambitious projects such as highway network expansions, critical bridge replacements, the construction of new public transportation systems, and extensive energy sector developments, all of which generate substantial and sustained demand for fabricated steel structures. Concurrently, the market benefits from the continued and steady expansion of both commercial and residential construction activities. This sustained building momentum directly translates into increased demand for structural steel. Moreover, the industry is undergoing a technological renaissance. Advancements in steel fabrication processes, including the integration of automation, sophisticated design software (BIM), and enhanced welding techniques, are significantly boosting operational efficiency, improving precision, and ultimately reducing overall project costs, thereby encouraging wider adoption of structural steel as a preferred building material.

Challenges in the North America Structural Steel Fabrication Market Sector

The North America structural steel fabrication market faces several challenges. Fluctuations in steel prices due to global supply chain disruptions and raw material cost volatility significantly impact profitability. Increased labor costs and skilled labor shortages also constrain the industry's capacity. Furthermore, stringent environmental regulations add to the operational costs, putting pressure on margins. These challenges result in an estimated xx% decrease in profit margins for some firms in the past year.

Emerging Opportunities in North America Structural Steel Fabrication Market

The North American structural steel fabrication market is ripe with emerging opportunities poised to shape its future. The growing global imperative for sustainability is fueling a demand for green steel fabrication techniques, the use of recycled steel content, and the development of high-performance, longer-lasting steel products. Furthermore, the groundbreaking advancements in additive manufacturing, commonly known as 3D printing, present a revolutionary potential for fabricating intricate and complex steel structures with unprecedented design flexibility and material optimization. Strategic expansion into burgeoning market segments, such as the development of renewable energy infrastructure (wind turbines, solar panel mounting systems) and the rapidly growing modular construction sector, offers significant avenues for sustained growth and market penetration.

Leading Players in the North America Structural Steel Fabrication Market Market

- High Industries Inc

- SME Industries Inc

- Whitemud Ironworks Group Inc

- Farr Installations Ltd

- Marid Industries Limited

- Postensados y Disenos de Estructuras SA de CV

- Gimsa Division Industrial SA de CV

- B & H Structures Co Ltd

- Fabricado de Acero Estructural SA

- Metalurgica Industrial y Construccion SA

- Valmont Industries Inc

- Cornerstone Building Brands Inc

- DBM Global

- Groupe Canam Inc

- Sabre Industries Inc

Key Developments in North America Structural Steel Fabrication Market Industry

- June 2022: BM Group, a prominent player based in Vancouver, significantly expanded its market reach and comprehensive service offerings through the strategic acquisition of LE Steel Fabricators Ltd.

- April 2022: Terex Corporation bolstered its manufacturing capabilities and enhanced its competitive standing within the heavy equipment sector by successfully acquiring Steelweld, a specialized steel fabrication company.

- Ongoing: Increased investment by major fabricators in advanced robotic welding and automated cutting systems to improve efficiency and precision.

- Focus on Sustainability: Growing trend towards utilizing recycled steel content and implementing energy-efficient fabrication processes to align with environmental regulations and client demands.

- BIM Integration: Widespread adoption of Building Information Modeling (BIM) for enhanced project planning, design coordination, and fabrication accuracy, leading to reduced errors and waste.

Strategic Outlook for North America Structural Steel Fabrication Market Market

The North America structural steel fabrication market is poised for sustained growth over the forecast period. Continued infrastructure investment, coupled with technological advancements and the increasing adoption of sustainable building practices, presents significant opportunities. Companies that embrace innovation, optimize their supply chains, and adapt to evolving market dynamics are well-positioned to capitalize on this growth.

North America Structural Steel Fabrication Market Segmentation

-

1. End-user Industry

- 1.1. Manufacturing

- 1.2. Power and Energy

- 1.3. Construction

- 1.4. Oil and Gas

- 1.5. Other End-user Industries

-

2. Product Type

- 2.1. Heavy Sectional Steel

- 2.2. Light Sectional Steel

- 2.3. Other Product Types

North America Structural Steel Fabrication Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Structural Steel Fabrication Market Regional Market Share

Geographic Coverage of North America Structural Steel Fabrication Market

North America Structural Steel Fabrication Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 5.1.1. Manufacturing

- 5.1.2. Power and Energy

- 5.1.3. Construction

- 5.1.4. Oil and Gas

- 5.1.5. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Heavy Sectional Steel

- 5.2.2. Light Sectional Steel

- 5.2.3. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6. North America Structural Steel Fabrication Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6.1.1. Manufacturing

- 6.1.2. Power and Energy

- 6.1.3. Construction

- 6.1.4. Oil and Gas

- 6.1.5. Other End-user Industries

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Heavy Sectional Steel

- 6.2.2. Light Sectional Steel

- 6.2.3. Other Product Types

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 High Industries Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 SME Industries Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Whitemud Ironworks Group Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Farr Installations Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Marid Industries Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Postensados y Disenos de Estructuras SA de CV

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Gimsa Division Industrial SA de CV

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 B & H Structures Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Fabricado de Acero Estructural SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Metalurgica Industrial y Construccion SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Valmont Industries Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Cornerstone Building Brands Inc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 DBM Global

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Groupe Canam Inc

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Sabre Industries Inc

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 High Industries Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Structural Steel Fabrication Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Structural Steel Fabrication Market Share (%) by Company 2025

List of Tables

- Table 1: North America Structural Steel Fabrication Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 2: North America Structural Steel Fabrication Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: North America Structural Steel Fabrication Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: North America Structural Steel Fabrication Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 5: North America Structural Steel Fabrication Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: North America Structural Steel Fabrication Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States North America Structural Steel Fabrication Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Structural Steel Fabrication Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Structural Steel Fabrication Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Structural Steel Fabrication Market?

The projected CAGR is approximately 9%.

2. Which companies are prominent players in the North America Structural Steel Fabrication Market?

Key companies in the market include High Industries Inc, SME Industries Inc, Whitemud Ironworks Group Inc, Farr Installations Ltd, Marid Industries Limited, Postensados y Disenos de Estructuras SA de CV, Gimsa Division Industrial SA de CV, B & H Structures Co Ltd, Fabricado de Acero Estructural SA, Metalurgica Industrial y Construccion SA, Valmont Industries Inc, Cornerstone Building Brands Inc, DBM Global, Groupe Canam Inc, Sabre Industries Inc.

3. What are the main segments of the North America Structural Steel Fabrication Market?

The market segments include End-user Industry, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 179.04 billion as of 2022.

5. What are some drivers contributing to market growth?

3.; Rapid Growth In the Infrastructure Sector3.; Increased Demand for Steel Products.

6. What are the notable trends driving market growth?

Increased Use of Blockchain. Internet of Things. and Industry 5.0.

7. Are there any restraints impacting market growth?

3.; Rapid Growth In the Infrastructure Sector3.; Increased Demand for Steel Products.

8. Can you provide examples of recent developments in the market?

Jun 2022: Vancouver-based BM Group acquired LE Steel Fabricators Ltd. This acquisition will give them the opportunity to enter an existing sector from a different angle while carrying out more substantial repair and restoration operations. Additionally, BM Group's clients benefit from cost reductions, efficiency, and other advantages as a result of its strong financial position and varied portfolio of companies.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Structural Steel Fabrication Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Structural Steel Fabrication Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Structural Steel Fabrication Market?

To stay informed about further developments, trends, and reports in the North America Structural Steel Fabrication Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence