Key Insights

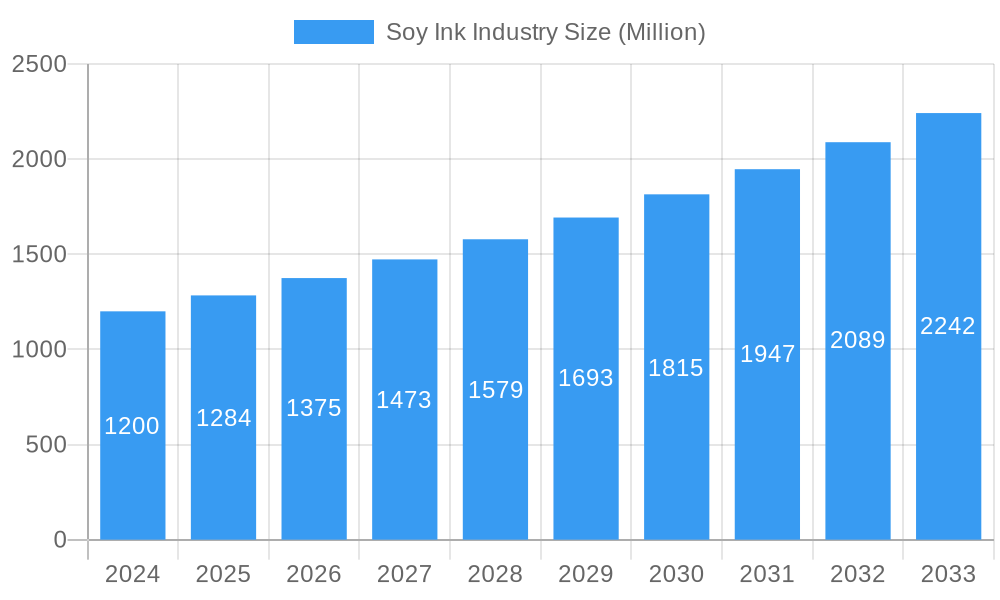

The global soy ink market is poised for substantial growth, projected to reach approximately $1.2 billion in 2024 and expand at a compelling Compound Annual Growth Rate (CAGR) of 7.5% through 2033. This robust expansion is fueled by a growing consumer and regulatory demand for environmentally friendly printing solutions, positioning soy-based inks as a prime alternative to traditional petroleum-based inks. The inherent sustainability of soy ink, derived from renewable resources, significantly reduces volatile organic compound (VOC) emissions, contributing to improved air quality and a healthier printing environment. This ecological advantage is a key driver, particularly within the label and packaging sector, where brands are increasingly prioritizing sustainable materials to enhance their corporate social responsibility profiles and appeal to environmentally conscious consumers. Furthermore, advancements in soy ink formulations are continuously improving their performance characteristics, including faster drying times, enhanced color vibrancy, and broader substrate compatibility, thereby broadening their applicability across diverse printing segments.

Soy Ink Industry Market Size (In Billion)

The market's trajectory is further bolstered by emerging trends such as the increasing adoption of digital printing technologies, which can seamlessly integrate with soy-based inks, and a rising emphasis on circular economy principles within the printing industry. While the market benefits from these positive drivers, it also faces certain challenges, including the initial cost of soy inks which can sometimes be higher than conventional alternatives, and the need for specialized printing equipment or adjustments for optimal performance in some applications. However, the long-term benefits of reduced environmental impact and potential cost savings through improved efficiency and waste reduction are expected to outweigh these initial considerations. Key regions like Asia Pacific, driven by strong manufacturing bases and growing environmental awareness, and North America, with its established focus on sustainable practices, are expected to be significant contributors to market expansion. Companies are actively investing in research and development to overcome existing limitations and unlock the full potential of soy inks across a wider range of commercial and publication printing applications, solidifying its position as a critical component of a more sustainable printing future.

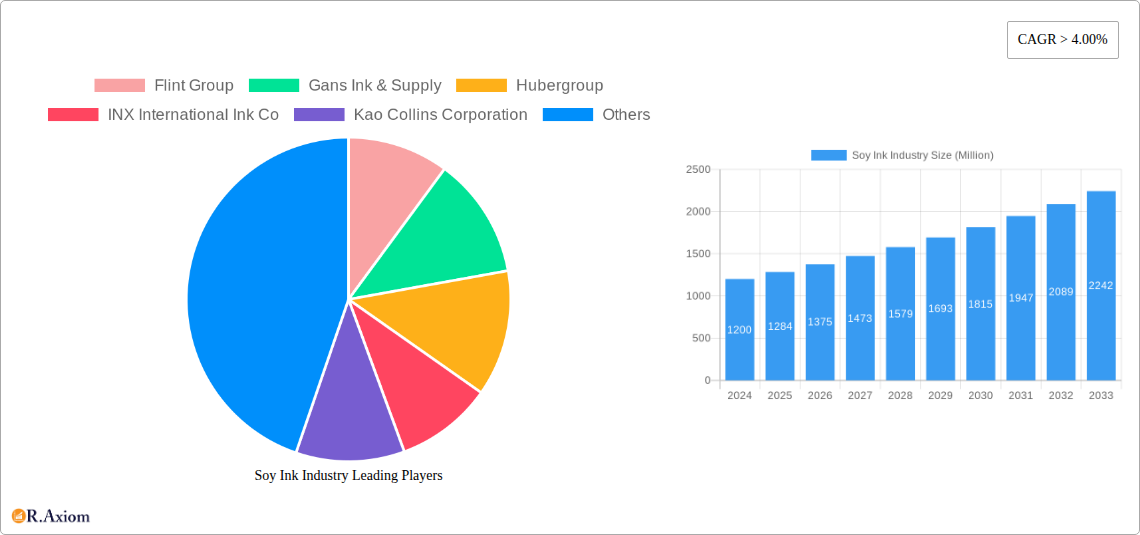

Soy Ink Industry Company Market Share

This comprehensive Soy Ink Industry report delivers an in-depth analysis of the global market, providing actionable intelligence for stakeholders. Covering the historical period 2019–2024, base and estimated year 2025, and a robust forecast period from 2025–2033, the report meticulously examines market dynamics, growth drivers, segmentation, competitive landscapes, and future opportunities. With an anticipated market size of over 2 billion by the end of the forecast period, this study is crucial for businesses navigating the evolving soy ink landscape, including flint ink, soy-based ink, and UV ink applications in label and packaging, commercial printing, and publication sectors.

Soy Ink Industry Market Concentration & Innovation

The Soy Ink Industry exhibits a moderate market concentration, with a few major players holding significant market share, estimated to be upwards of 60% combined. Innovation remains a key differentiator, driven by increasing demand for sustainable and eco-friendly printing solutions. Regulatory frameworks, particularly those promoting VOC reduction and bio-based materials, are compelling manufacturers to invest in R&D for low-VOC and high-bio-renewable content inks. Product substitutes, such as water-based inks and other vegetable-oil-based inks, present a competitive challenge, necessitating continuous product development and cost optimization. End-user trends are increasingly leaning towards environmentally conscious choices, boosting the adoption of soy inks in sectors like food packaging and publications. Merger and acquisition (M&A) activities are also observed, with deal values ranging from tens of millions to hundreds of millions, indicating a strategic consolidation to enhance market reach and technological capabilities. Key innovation drivers include enhanced printability, improved color vibrancy, faster drying times, and reduced environmental impact, all contributing to the growth of the soy ink market, projected to reach over 5 billion in value by 2033.

Soy Ink Industry Industry Trends & Insights

The Soy Ink Industry is poised for significant growth, driven by a confluence of factors including escalating environmental consciousness, stringent government regulations on volatile organic compounds (VOCs), and the inherent benefits of soy-based inks such as renewability and biodegradability. The global market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033, reaching a market size estimated to surpass 7 billion. Technological advancements play a pivotal role, with ongoing research and development focused on improving ink performance, expanding application versatility, and reducing production costs. For instance, advancements in soy oil processing and additive formulations are leading to inks with enhanced rub resistance, faster curing times, and superior color fidelity, making them increasingly competitive with traditional petroleum-based inks. Consumer preferences are a powerful catalyst; brands are actively seeking sustainable packaging solutions to appeal to eco-conscious consumers, thereby creating substantial demand for soy inks, particularly in the label and packaging segment. Market penetration of soy inks, currently estimated at over 40% in specific applications, is expected to rise as awareness and performance benefits become more widely recognized. The competitive dynamics are intensifying, with established ink manufacturers and new entrants alike vying for market share by offering innovative, sustainable, and cost-effective solutions. The shift towards a circular economy further amplifies the appeal of soy inks, aligning with industry-wide sustainability goals and consumer expectations for environmentally responsible products. This trend is further supported by the development of specialized soy inks for digital printing technologies, opening up new avenues for market expansion. The increasing adoption of eco-friendly printing practices across various industries, from commercial printing to niche applications, underscores the robust growth trajectory of the soy ink market.

Dominant Markets & Segments in Soy Ink Industry

The Label and Packaging segment is the undisputed leader within the Soy Ink Industry, accounting for an estimated over 55% of the global market share. This dominance is fueled by a confluence of factors, including stringent regulations promoting sustainable packaging, increasing consumer demand for eco-friendly products, and the critical need for safe and compliant inks in food and beverage packaging. Key drivers for this segment's leadership include:

- Growing E-commerce and Retail Expansion: The surge in online retail and the expansion of global supply chains necessitate robust and visually appealing packaging, creating a continuous demand for high-quality printing inks.

- Regulatory Mandates for Sustainability: Governments worldwide are implementing stricter environmental regulations, pushing brands to adopt greener printing solutions, with soy inks being a prime candidate due to their bio-renewable nature and reduced VOC emissions.

- Brand Differentiation and Consumer Perception: Companies are increasingly leveraging sustainable packaging to enhance brand image and connect with environmentally conscious consumers, making soy inks a strategic choice for differentiation.

- Versatility in Printing Technologies: Soy inks are compatible with a wide array of printing technologies commonly used in packaging, such as flexography and gravure, further cementing their position.

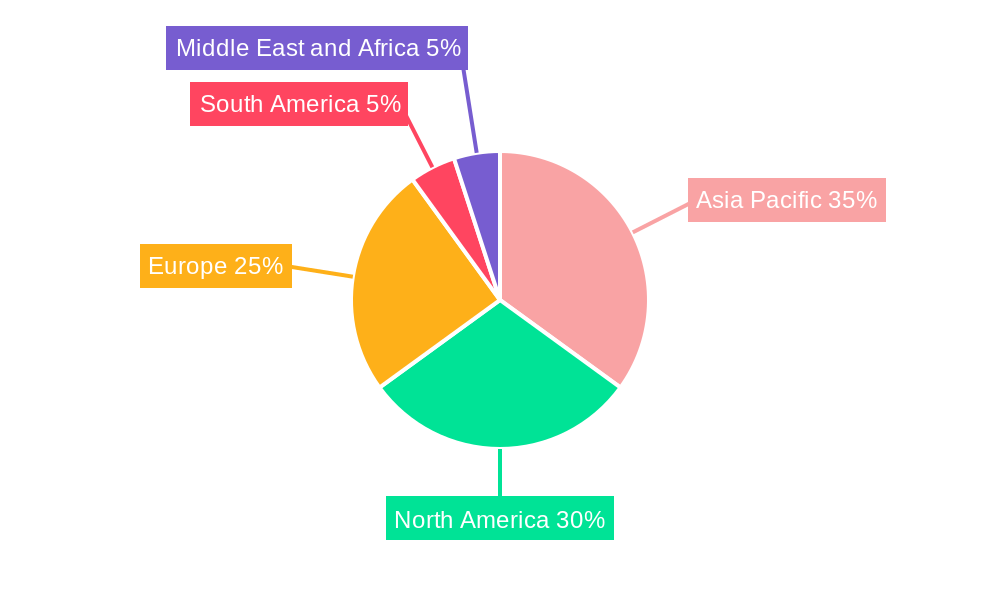

Geographically, North America and Europe currently represent the dominant markets for soy inks, driven by mature regulatory environments and a strong consumer focus on sustainability. However, the Asia-Pacific region is experiencing rapid growth, propelled by burgeoning manufacturing sectors, increasing environmental awareness, and government initiatives promoting green manufacturing practices. Within the Type segmentation, Soy-based Ink naturally holds the largest share, being the core product. However, advancements in UV Ink technology, including UV-curable soy-based inks, are gaining significant traction due to their fast drying times and enhanced durability, especially in the Label and Packaging application. The Commercial Printing segment, while historically significant, is seeing a slower growth rate compared to packaging, with a gradual shift towards digital printing solutions. The Publication segment is also undergoing transformation, with the rise of digital media impacting traditional print volumes. Nevertheless, soy inks find application here for their eco-friendly profile, especially for magazines and catalogs with a sustainability focus. The overall market size for soy ink is projected to reach over 6 billion by 2033, with the Label and Packaging application leading this expansion.

Soy Ink Industry Product Developments

The Soy Ink Industry is characterized by continuous product innovation aimed at enhancing performance and sustainability. Recent developments focus on improving ink formulations for faster drying times, better adhesion on diverse substrates, and increased resistance to smudging and fading. The integration of bio-renewable content is a paramount trend, with manufacturers actively developing UV offset ink series featuring high bio-renewable content for paper and board applications, aligning with circular economy principles. These innovations offer competitive advantages by meeting evolving environmental standards and consumer preferences for greener products, thereby securing market share in environmentally conscious sectors like label and packaging.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Soy Ink Industry across key segments. The Type segmentation includes Flint Ink, Soy-based Ink, UV Ink, and Other Types, each contributing to the overall market dynamics with varying growth trajectories and adoption rates. The Application segmentation is granularly analyzed, covering Label and Packaging, Commercial Printing, Publication, and Other Applications. Projections indicate that Label and Packaging will continue to dominate, driven by sustainability demands. Soy-based Ink is expected to maintain its lead in the Type segment, while UV Ink formulations are poised for significant growth due to their advanced performance characteristics. The market size for each segment is projected to exceed 1 billion individually by 2033, reflecting the expanding adoption of soy ink technologies.

Key Drivers of Soy Ink Industry Growth

The growth of the Soy Ink Industry is primarily propelled by robust environmental consciousness and increasingly stringent government regulations mandating the reduction of VOC emissions and the adoption of sustainable materials. The inherent biodegradability and renewability of soy-based inks make them an attractive alternative to petroleum-based inks, aligning with global sustainability goals and the principles of the circular economy. Furthermore, advancements in ink technology are leading to improved performance characteristics, such as enhanced color vibrancy, faster drying times, and superior print quality, thereby expanding their applicability across various printing sectors, including food-grade packaging. The growing demand from end-users for eco-friendly products and packaging solutions further incentivizes manufacturers to invest in and promote soy ink products, solidifying their market position. The market is projected to reach over 3 billion in value by 2028.

Challenges in the Soy Ink Industry Sector

Despite its promising growth, the Soy Ink Industry faces several challenges. The primary restraint is the often higher cost of soy-based inks compared to conventional petroleum-based alternatives, which can be a deterrent for price-sensitive customers. Supply chain volatility for raw materials, such as soybean oil, can also impact production costs and availability. While performance has improved, some niche applications may still experience limitations in terms of specific properties like extreme durability or rapid curing compared to specialized synthetic inks. Regulatory hurdles related to food contact compliance and certification processes can also add complexity and time to market for certain applications. Furthermore, intense competition from other eco-friendly ink alternatives and established petroleum-based ink manufacturers necessitates continuous innovation and strategic market positioning. The market is estimated to be valued at over 1 billion in 2024.

Emerging Opportunities in Soy Ink Industry

Emerging opportunities within the Soy Ink Industry are abundant, particularly in the development of advanced bio-renewable inks with superior performance characteristics. The increasing global focus on sustainable packaging solutions for the food and beverage industry presents a significant growth avenue, as does the potential for wider adoption in the textile and electronics printing sectors. Innovations in digital printing technologies are creating new demand for specialized soy-based inks, opening up markets for customized and on-demand printing. Furthermore, the growing emphasis on the circular economy and waste reduction is driving demand for biodegradable and compostable inks, further enhancing the market potential of soy-based formulations. The expansion of emerging economies and their increasing adoption of environmental regulations will also contribute significantly to market growth, projected to reach over 8 billion by 2033.

Leading Players in the Soy Ink Industry Market

Flint Group Gans Ink & Supply Hubergroup INX International Ink Co Kao Collins Corporation Siegwerk Druckfarben AG & Co KGaA Omya AG Sun Chemical Synthotex Chemicals Pvt Ltd Toyo Ink America LLC

Key Developments in Soy Ink Industry Industry

- May 2022: Siegwerk launched a new UV offset ink series with high bio-renewable content for paper and board applications. With its new SICURA Litho Pack ECO series, Siegwerk added another sustainable ink solution with a high share of bio-renewable content. This is expected to help the company further expand its offering in line with the circular economy.

- May 2022: Flint Group officially announced the launch of its Kryoset Flint ink series, a groundbreaking development that enables the production of heat-set quality products within the conventional heat-set process without the need for the drying process.

Strategic Outlook for Soy Ink Industry Market

The strategic outlook for the Soy Ink Industry is overwhelmingly positive, driven by the persistent global shift towards sustainability and environmentally conscious practices. Continued investment in research and development will be crucial for overcoming cost barriers and enhancing product performance to compete effectively with traditional inks. The expanding regulatory landscape favoring eco-friendly solutions, coupled with growing consumer demand for sustainable products, will continue to fuel market growth. Strategic partnerships and collaborations, particularly in the supply chain and with end-users, will be vital for market penetration and for adapting to evolving industry needs. The integration of soy inks into emerging printing technologies, such as digital and 3D printing, presents significant future opportunities. The market is projected to achieve a valuation of over 9 billion by 2033, underscoring its robust growth potential.

Soy Ink Industry Segmentation

-

1. Type

- 1.1. Flint Ink

- 1.2. Soy-based Ink

- 1.3. UV Ink

- 1.4. Other Types

-

2. Application

- 2.1. Label and Packaging

- 2.2. Commercial Printing

- 2.3. Publication

- 2.4. Other Applications

Soy Ink Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Soy Ink Industry Regional Market Share

Geographic Coverage of Soy Ink Industry

Soy Ink Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Flint Ink

- 5.1.2. Soy-based Ink

- 5.1.3. UV Ink

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Label and Packaging

- 5.2.2. Commercial Printing

- 5.2.3. Publication

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Soy Ink Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Flint Ink

- 6.1.2. Soy-based Ink

- 6.1.3. UV Ink

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Label and Packaging

- 6.2.2. Commercial Printing

- 6.2.3. Publication

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Asia Pacific Soy Ink Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Flint Ink

- 7.1.2. Soy-based Ink

- 7.1.3. UV Ink

- 7.1.4. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Label and Packaging

- 7.2.2. Commercial Printing

- 7.2.3. Publication

- 7.2.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. North America Soy Ink Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Flint Ink

- 8.1.2. Soy-based Ink

- 8.1.3. UV Ink

- 8.1.4. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Label and Packaging

- 8.2.2. Commercial Printing

- 8.2.3. Publication

- 8.2.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Soy Ink Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Flint Ink

- 9.1.2. Soy-based Ink

- 9.1.3. UV Ink

- 9.1.4. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Label and Packaging

- 9.2.2. Commercial Printing

- 9.2.3. Publication

- 9.2.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Soy Ink Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Flint Ink

- 10.1.2. Soy-based Ink

- 10.1.3. UV Ink

- 10.1.4. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Label and Packaging

- 10.2.2. Commercial Printing

- 10.2.3. Publication

- 10.2.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Soy Ink Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Flint Ink

- 11.1.2. Soy-based Ink

- 11.1.3. UV Ink

- 11.1.4. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Label and Packaging

- 11.2.2. Commercial Printing

- 11.2.3. Publication

- 11.2.4. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Flint Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Gans Ink & Supply

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hubergroup

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 INX International Ink Co

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Kao Collins Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Siegwerk Druckfarben AG & Co KGaA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Omya AG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sun Chemical

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Synthotex Chemicals Pvt Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Toyo Ink America LLC *List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Flint Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Soy Ink Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Soy Ink Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: Asia Pacific Soy Ink Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific Soy Ink Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: Asia Pacific Soy Ink Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Soy Ink Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Soy Ink Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Soy Ink Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: North America Soy Ink Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Soy Ink Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: North America Soy Ink Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: North America Soy Ink Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Soy Ink Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Soy Ink Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe Soy Ink Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Soy Ink Industry Revenue (billion), by Application 2025 & 2033

- Figure 17: Europe Soy Ink Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe Soy Ink Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Soy Ink Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Soy Ink Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: South America Soy Ink Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Soy Ink Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: South America Soy Ink Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: South America Soy Ink Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Soy Ink Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Soy Ink Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Soy Ink Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Soy Ink Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Middle East and Africa Soy Ink Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Soy Ink Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Soy Ink Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Soy Ink Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Soy Ink Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Soy Ink Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Soy Ink Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Soy Ink Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Soy Ink Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Soy Ink Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global Soy Ink Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Soy Ink Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Soy Ink Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 19: Global Soy Ink Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Soy Ink Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: France Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Soy Ink Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 27: Global Soy Ink Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Global Soy Ink Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Soy Ink Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 33: Global Soy Ink Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 34: Global Soy Ink Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Soy Ink Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Soy Ink Industry?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Soy Ink Industry?

Key companies in the market include Flint Group, Gans Ink & Supply, Hubergroup, INX International Ink Co, Kao Collins Corporation, Siegwerk Druckfarben AG & Co KGaA, Omya AG, Sun Chemical, Synthotex Chemicals Pvt Ltd, Toyo Ink America LLC *List Not Exhaustive.

3. What are the main segments of the Soy Ink Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Growth in Demand from Packaging Industry; Growing Concerns Related to VOC Emissions from Conventional Ink Printing Solutions.

6. What are the notable trends driving market growth?

Growth in Demand from Packaging Industry.

7. Are there any restraints impacting market growth?

Growth in Demand from Packaging Industry; Growing Concerns Related to VOC Emissions from Conventional Ink Printing Solutions.

8. Can you provide examples of recent developments in the market?

May 11, 2022: Siegwerk launched a new UV offset ink series with high bio-renewable content for paper and board applications. With its new SICURA Litho Pack ECO series, Siegwerk added another sustainable ink solution with a high share of bio-renewable content. This is expected to help the company further expand its offering in line with the circular economy.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Soy Ink Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Soy Ink Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Soy Ink Industry?

To stay informed about further developments, trends, and reports in the Soy Ink Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence