Key Insights

The United Kingdom's nuclear power sector is set for substantial growth, projecting a CAGR of 8.5%. This expansion is propelled by the nation's commitment to decarbonization objectives and the rising demand for stable, low-carbon energy. The market, valued at an estimated 54.8 billion as of 2025, is significantly influenced by government policies promoting new nuclear construction and the refurbishment of existing plants. Key growth factors include the necessity to phase out aging fossil fuel infrastructure, bolster energy security, and achieve ambitious net-zero emission targets. The focus on advanced reactor technologies and nuclear power's strategic position in the UK's energy framework further stimulate market development. Investments are anticipated in projects for infrastructure modernization and the exploration of innovative reactor types, such as High-temperature Gas-cooled Reactors and Liquid Metal Fast Breeder Reactors, designed for enhanced efficiency and safety.

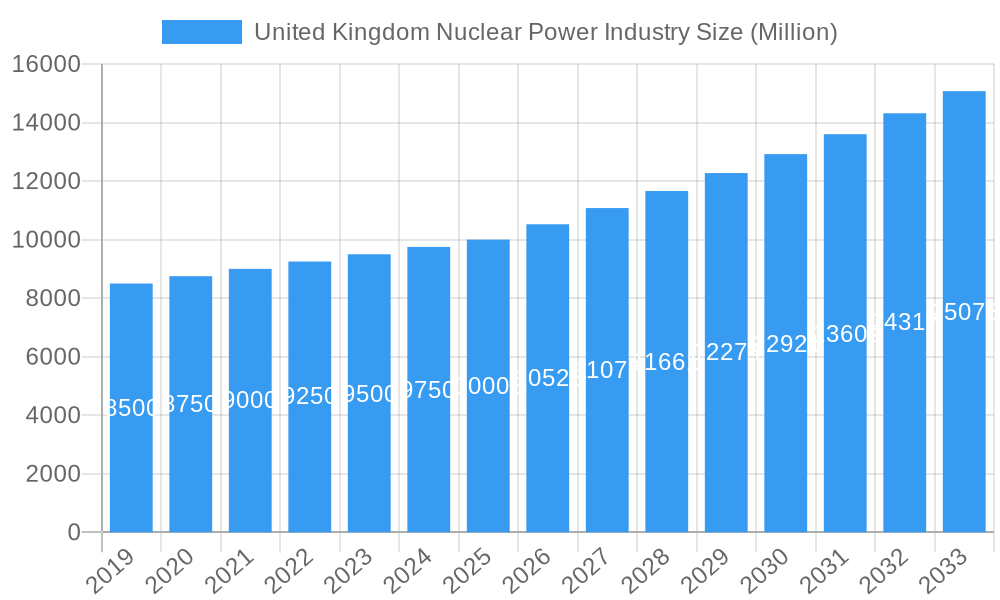

United Kingdom Nuclear Power Industry Market Size (In Billion)

The UK nuclear power market features a variety of reactor types and applications. Pressurized Water Reactors (PWRs) and Boiling Water Reactors (BWRs) currently lead commercial power generation, with increasing interest in advanced designs. The capacity segment is dominated by large-scale reactors exceeding 1000 MW, essential for baseload electricity. However, opportunities are also expanding in prototype and research reactors for technological advancement and specialized energy requirements. Leading companies such as Aecom, Orano Group, SNC-Lavalin Group, Bechtel, and Fluor Corporation are actively engaged in projects, highlighting a competitive yet collaborative industry landscape. While high capital costs and public perception present challenges, innovative financing and improved safety measures are being implemented to ensure sustained growth and solidify nuclear energy's vital role in the UK's future power generation.

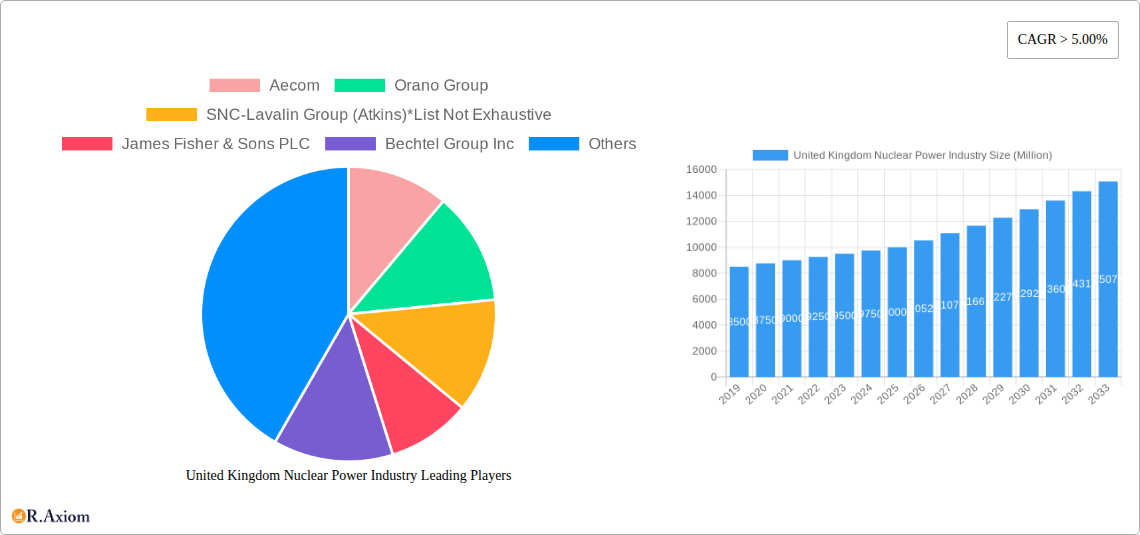

United Kingdom Nuclear Power Industry Company Market Share

United Kingdom Nuclear Power Industry Market Concentration & Innovation

The United Kingdom nuclear power industry is characterized by moderate market concentration, with a few key players dominating the large-scale reactor construction and operation segments. Innovation is a critical driver, fueled by substantial R&D investments aimed at enhancing reactor safety, efficiency, and the development of advanced nuclear technologies like Small Modular Reactors (SMRs). Regulatory frameworks, spearheaded by bodies such as the Office for Nuclear Regulation (ONR), play a pivotal role in shaping the industry's trajectory, ensuring stringent safety and security standards. The threat of product substitutes, primarily renewable energy sources and fossil fuels, necessitates continuous advancements in nuclear technology to maintain competitiveness. End-user trends are increasingly leaning towards low-carbon energy solutions and energy security, bolstering the demand for nuclear power. Mergers and acquisitions (M&A) activity, while not as frequent as in more mature industries, are strategically important for consolidating expertise and securing large-scale project financing. For instance, significant M&A deals in the global nuclear sector, though not specific to the UK, indicate potential for consolidation and investment. The market share of existing nuclear power plants is substantial, contributing a significant portion of the UK's baseload electricity.

- Market Share of Existing Nuclear Capacity: xx Million Megawatts (MW)

- Estimated M&A Deal Value (Global Nuclear Sector): xx Million USD

- Innovation Focus Areas: SMRs, advanced fuel cycles, decommissioning technologies, passive safety systems.

- Key Regulatory Bodies: Office for Nuclear Regulation (ONR), Department for Energy Security and Net Zero.

United Kingdom Nuclear Power Industry Industry Trends & Insights

The United Kingdom nuclear power industry is poised for significant growth and transformation over the forecast period of 2025–2033, driven by a confluence of factors including the urgent need for decarbonization, enhanced energy security, and technological advancements. The industry is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 5-7% during this period, reflecting the strategic importance placed on nuclear energy within the UK's net-zero ambitions. Technological disruptions are a key theme, with the development and potential deployment of Small Modular Reactors (SMRs) promising to revolutionize the nuclear landscape by offering more flexible, scalable, and potentially cost-effective solutions compared to traditional large-scale power plants. Consumer preferences are increasingly shifting towards reliable and sustainable energy sources, and nuclear power, with its low-carbon footprint and consistent energy generation, is well-positioned to meet these demands. Competitive dynamics within the industry are evolving, with a focus on global collaboration for expertise and supply chain resilience. The market penetration of nuclear energy in the UK's overall energy mix is projected to increase as new projects come online and existing plants are maintained or repowered where feasible. The historical performance from 2019-2024 has seen continued operation of existing fleet and planning for future investments, laying the groundwork for the projected growth. The base year of 2025 will be a critical juncture, marking the commencement of accelerated development and investment in new nuclear capacity.

- Projected CAGR (2025-2033): 5-7%

- Current Nuclear Share in UK Energy Mix: Approximately 16%

- Future Nuclear Share Projection (2033): xx%

- Key Growth Enablers: Government support, private investment, climate targets, energy independence goals.

Dominant Markets & Segments in United Kingdom Nuclear Power Industry

Within the United Kingdom nuclear power industry, the Commercial Power Reactor segment, particularly those with capacities Above 1000 MW, is currently the dominant market force. These large-scale plants provide the bulk of the nuclear-generated electricity, underpinning the UK's baseload power needs. The Pressurized Water Reactor (PWR) type remains the most prevalent technology globally and within the UK's existing fleet, offering a proven and reliable method for electricity generation. The future, however, shows significant promise for segments like Prototype Power Reactor and Research Reactor, especially with the burgeoning interest in Small Modular Reactors (SMRs) which, while varying in capacity (potentially below 100 MW to 100-1000 MW), represent a significant area of innovation and future deployment. The application of nuclear technology extends beyond commercial power generation, with ongoing research and development in areas that could influence future reactor designs and applications.

- Dominant Reactor Type: Pressurized Water Reactor (PWR)

- Dominant Application: Commercial Power Reactor

- Dominant Capacity Segment: Above 1000 MW

- Key Drivers for Dominance:

- Economic Policies: Government incentives and long-term energy strategy supporting large-scale nuclear projects.

- Infrastructure: Established grid connections and skilled workforce for large-scale operations.

- Energy Security: The strategic imperative to maintain a diverse and reliable energy supply.

- Decarbonization Targets: The need for consistent, low-carbon electricity to meet climate goals.

The analysis also highlights the growing importance of High-temperature Gas-cooled Reactor (HTGR) and Liquid Metal Fast Breeder Reactor (LMFBR) research, which, while not currently dominant in commercial deployment, represent future potential for advanced applications. The Pressurized Heavy Water Reactor (PHWR) and Boiling Water Reactor (BWR) types, though present in global portfolios, have a less significant footprint in the current UK large-scale new build pipeline, but remain relevant in existing operations and decommissioning contexts. Other Reactor Types, encompassing novel designs and research prototypes, are crucial for fostering innovation and exploring niche applications or next-generation technologies. The Below 100 MW and 100-1000 MW capacity segments are poised for significant expansion with the advent of SMRs, which could cater to a wider range of energy demands and industrial applications, thereby diversifying the market.

United Kingdom Nuclear Power Industry Product Developments

Product developments in the UK nuclear power industry are largely centered on enhancing the safety, efficiency, and economic viability of nuclear energy. The most significant innovation is the advancement of Small Modular Reactors (SMRs), which promise a more flexible and scalable approach to nuclear power generation. Companies are actively developing SMR designs that offer shorter construction times, reduced upfront costs, and enhanced safety features, including passive cooling systems. These developments are not only aimed at electricity generation but also explore applications in industrial heat, hydrogen production, and desalination. The competitive advantage of these new designs lies in their adaptability to various geographical locations and their potential to revitalize nuclear energy's appeal as a clean and reliable power source.

- Key Innovation: Small Modular Reactors (SMRs)

- Application Focus: Electricity generation, industrial heat, hydrogen production.

- Competitive Advantages: Scalability, reduced cost, faster deployment, enhanced safety.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the United Kingdom Nuclear Power Industry, segmenting the market across various Reactor Types, Applications, and Capacity levels. The Reactor Types analyzed include Pressurized Water Reactor (PWR), Pressurized Heavy Water Reactor (PHWR), Boiling Water Reactor (BWR), High-temperature Gas-cooled Reactor (HTGR), and Liquid Metal Fast Breeder Reactor (LMFBR), alongside Other Reactor Types representing emerging technologies. Applications are categorized into Commercial Power Reactor, Prototype Power Reactor, and Research Reactor. Capacity segments cover Below 100 MW, 100-1000 MW, and Above 1000 MW. Growth projections and market sizes will be detailed for each segment, alongside an analysis of competitive dynamics and key drivers influencing their development within the study period of 2019–2033.

- Reactor Types: PWR, PHWR, BWR, HTGR, LMFBR, Other.

- Applications: Commercial, Prototype, Research.

- Capacity: Below 100 MW, 100-1000 MW, Above 1000 MW.

Each segment's analysis will include a granular look at its current market size, projected growth trajectory, and the specific factors contributing to its dominance or potential growth. For instance, the Commercial Power Reactor segment, particularly those exceeding 1000 MW capacity, is expected to maintain its leading position in terms of contribution to the energy mix, driven by existing infrastructure and long-term contracts. However, the Prototype and Research Reactor segments, especially those related to SMR development, are poised for significant expansion, driven by governmental support and private investment in next-generation nuclear technologies. The competitive dynamics will be examined in terms of technology providers, project developers, and the role of regulatory approvals in shaping market entry and expansion.

Key Drivers of United Kingdom Nuclear Power Industry Growth

The growth of the United Kingdom nuclear power industry is propelled by a multifaceted set of drivers. Foremost among these is the urgent imperative to meet stringent net-zero emissions targets, for which nuclear power's low-carbon baseload generation is indispensable. Secondly, energy security concerns, amplified by geopolitical instability, are driving a renewed focus on domestic, reliable energy sources. Thirdly, significant government support and policy initiatives, including subsidies, tax incentives, and clear regulatory pathways for new nuclear projects, are crucial enablers. Finally, technological innovation, particularly in the development of SMRs, is opening up new avenues for deployment and addressing cost and siting challenges associated with traditional large-scale reactors.

- Net-Zero Emissions Targets: Critical for decarbonizing the electricity grid.

- Energy Security: Reducing reliance on volatile international fossil fuel markets.

- Government Support: Favorable policies and regulatory frameworks.

- Technological Advancements: SMR development and advanced reactor designs.

Challenges in the United Kingdom Nuclear Power Industry Sector

Despite its growth potential, the UK nuclear power industry faces substantial challenges. High upfront capital costs and long construction lead times for large-scale projects remain significant barriers to investment. Regulatory hurdles and complex approval processes can lead to project delays and cost overruns. Public perception and safety concerns, though diminishing with advancements, still require careful management. Supply chain limitations and the availability of skilled labor for specialized nuclear tasks can also pose constraints. Furthermore, competition from rapidly evolving renewable energy technologies and the associated cost reductions present a constant challenge to nuclear's economic competitiveness.

- High Capital Costs & Long Construction Times: Major investment deterrents.

- Regulatory Complexity: Potential for delays and cost escalations.

- Public Perception: Ongoing need for transparent communication on safety.

- Supply Chain & Workforce: Ensuring adequate capacity and expertise.

Emerging Opportunities in United Kingdom Nuclear Power Industry

The United Kingdom nuclear power industry is ripe with emerging opportunities, particularly driven by the global push for decarbonization and energy independence. The most prominent opportunity lies in the development and deployment of Small Modular Reactors (SMRs), which offer greater flexibility, affordability, and suitability for a wider range of applications, including industrial processes and remote communities. There is also significant potential in advanced nuclear fuels and waste management technologies, aiming to improve efficiency and reduce the long-term environmental impact of nuclear energy. Furthermore, the decommissioning of existing nuclear sites presents opportunities for specialized service providers and innovative de-risking technologies. The integration of nuclear power with other low-carbon sources for a robust, hybrid energy system also represents a growing area of focus.

- SMR Deployment: A key growth frontier for flexible and cost-effective nuclear power.

- Advanced Fuels & Waste Management: Enhancing sustainability and efficiency.

- Decommissioning Services: A substantial long-term market.

- Hybrid Energy Systems: Nuclear's role in integrated clean energy solutions.

Leading Players in the United Kingdom Nuclear Power Industry Market

- Aecom

- Orano Group

- SNC-Lavalin Group (Atkins)

- James Fisher & Sons PLC

- Bechtel Group Inc

- Fluor Corporation

- Babcock International Group PLC

- Studsvik AB

Key Developments in United Kingdom Nuclear Power Industry Industry

- November 2022: Rolls-Royce's nuclear power division identified four abandoned sites in Britain for the construction of a new fleet of microreactors, owned by the Nuclear Decommissioning Authority (NDA) in England and Wales. This development signifies a significant step towards the deployment of advanced nuclear technology for localized power generation.

- October 2022: The Welsh government and the British Nuclear Decommissioning Authority (NDA) agreed to collaborate on establishing a small-scale nuclear power facility in Trawsfynydd, North Wales. This collaboration will facilitate the sharing of site-specific information by the NDA, align decommissioning plans with the new nuclear project, and support Cwmni Egino in stakeholder engagement and socio-economic development.

Strategic Outlook for United Kingdom Nuclear Power Industry Market

The strategic outlook for the United Kingdom nuclear power industry is robust, fueled by a national commitment to achieving net-zero emissions and enhancing energy security. The continued investment in and development of advanced nuclear technologies, particularly SMRs, will be a primary growth catalyst, promising more adaptable and economically viable nuclear solutions. Government policies are expected to remain supportive, providing a stable regulatory environment and potential financial incentives for new projects. The industry is also poised to benefit from increased global collaboration, sharing of best practices, and advancements in supply chain resilience. The successful integration of nuclear power into the UK's future energy mix will depend on navigating regulatory challenges, maintaining public trust, and effectively leveraging technological innovation to meet the evolving demands of the energy landscape.

- Future Growth Catalysts: SMR deployment, government backing, energy security demands, technological innovation.

- Market Potential: Significant contribution to a decarbonized and secure energy future.

- Key Focus Areas: Advanced reactor technologies, regulatory efficiency, stakeholder engagement.

United Kingdom Nuclear Power Industry Segmentation

-

1. Reactor Type

- 1.1. Pressurized Water Reactor

- 1.2. Pressurized Heavy Water Reactor

- 1.3. Boiling Water Reactor

- 1.4. High-temperature Gas-cooled Reactor

- 1.5. Liquid Metal Fast Breeder Reactor

- 1.6. Other Reactor Types

-

2. Application

- 2.1. Commercial Power Reactor

- 2.2. Prototype Power Reactor

- 2.3. Research Reactor

-

3. Capacity

- 3.1. Below 100 MW

- 3.2. 100-1000 MW

- 3.3. Above 1000 MW

United Kingdom Nuclear Power Industry Segmentation By Geography

- 1. United Kingdom

United Kingdom Nuclear Power Industry Regional Market Share

Geographic Coverage of United Kingdom Nuclear Power Industry

United Kingdom Nuclear Power Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Reactor Type

- 5.1.1. Pressurized Water Reactor

- 5.1.2. Pressurized Heavy Water Reactor

- 5.1.3. Boiling Water Reactor

- 5.1.4. High-temperature Gas-cooled Reactor

- 5.1.5. Liquid Metal Fast Breeder Reactor

- 5.1.6. Other Reactor Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Commercial Power Reactor

- 5.2.2. Prototype Power Reactor

- 5.2.3. Research Reactor

- 5.3. Market Analysis, Insights and Forecast - by Capacity

- 5.3.1. Below 100 MW

- 5.3.2. 100-1000 MW

- 5.3.3. Above 1000 MW

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Reactor Type

- 6. United Kingdom Nuclear Power Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Reactor Type

- 6.1.1. Pressurized Water Reactor

- 6.1.2. Pressurized Heavy Water Reactor

- 6.1.3. Boiling Water Reactor

- 6.1.4. High-temperature Gas-cooled Reactor

- 6.1.5. Liquid Metal Fast Breeder Reactor

- 6.1.6. Other Reactor Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Commercial Power Reactor

- 6.2.2. Prototype Power Reactor

- 6.2.3. Research Reactor

- 6.3. Market Analysis, Insights and Forecast - by Capacity

- 6.3.1. Below 100 MW

- 6.3.2. 100-1000 MW

- 6.3.3. Above 1000 MW

- 6.1. Market Analysis, Insights and Forecast - by Reactor Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Aecom

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Orano Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 SNC-Lavalin Group (Atkins)*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 James Fisher & Sons PLC

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bechtel Group Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Fluor Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Babcock International Group PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Studsvik AB

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Aecom

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom Nuclear Power Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: United Kingdom Nuclear Power Industry Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Reactor Type 2020 & 2033

- Table 2: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 4: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Reactor Type 2020 & 2033

- Table 6: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 8: United Kingdom Nuclear Power Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Nuclear Power Industry?

The projected CAGR is approximately 8.5%.

2. Which companies are prominent players in the United Kingdom Nuclear Power Industry?

Key companies in the market include Aecom, Orano Group, SNC-Lavalin Group (Atkins)*List Not Exhaustive, James Fisher & Sons PLC, Bechtel Group Inc, Fluor Corporation, Babcock International Group PLC, Studsvik AB.

3. What are the main segments of the United Kingdom Nuclear Power Industry?

The market segments include Reactor Type, Application, Capacity.

4. Can you provide details about the market size?

The market size is estimated to be USD 54.8 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Presence of Strict Government Regulations to Control Air Pollution.

6. What are the notable trends driving market growth?

Commercial Power Reactor Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Renewable Energy.

8. Can you provide examples of recent developments in the market?

In November 2022, The nuclear power division of Rolls-Royce selected four abandoned sites in Britain to construct a new fleet of microreactors. The Nuclear Decommissioning Authority, which manages some of Britain's first nuclear facilities, owns the four locations in England and Wales.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Nuclear Power Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Nuclear Power Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Nuclear Power Industry?

To stay informed about further developments, trends, and reports in the United Kingdom Nuclear Power Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence