Key Insights

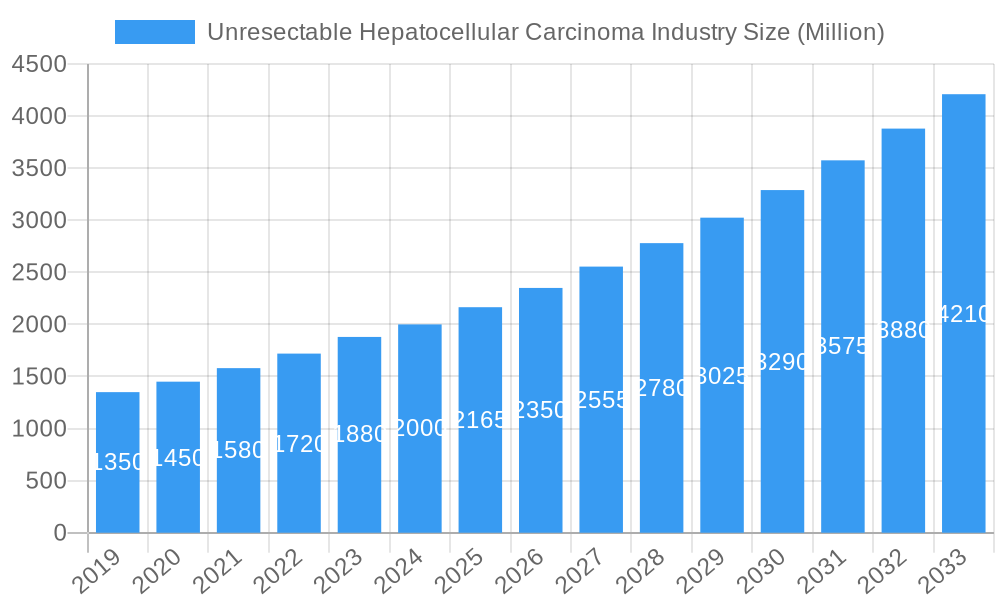

The Unresectable Hepatocellular Carcinoma (HCC) market is poised for significant expansion, projected to reach an estimated $2.01 billion by 2025. This robust growth trajectory is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 8.84%, indicating a dynamic and evolving treatment landscape. The market's expansion is primarily driven by the increasing global incidence of liver cancer, a growing patient population ineligible for surgical intervention, and advancements in therapeutic modalities. Key drivers include the rising prevalence of chronic liver diseases like hepatitis B and C, coupled with an increase in non-alcoholic fatty liver disease (NAFLD) and alcoholic liver disease, all recognized risk factors for HCC. Furthermore, the development and adoption of novel treatment options, such as molecularly targeted therapies and immunotherapies, are significantly contributing to improved patient outcomes and market growth. These innovative treatments offer new hope for patients with unresectable tumors, expanding treatment options beyond traditional chemotherapy.

Unresectable Hepatocellular Carcinoma Industry Market Size (In Billion)

The competitive landscape is characterized by the presence of major pharmaceutical giants and emerging biopharmaceutical companies actively engaged in research and development. The market is segmented into key treatment areas, with chemotherapy, molecularly targeted therapy, and immunotherapy representing the dominant segments. Molecularly targeted therapy and immunotherapy are expected to witness particularly strong growth due to their increasing efficacy and targeted action. Hospitals and cancer centers are the primary end-users, reflecting the sophisticated medical infrastructure required for advanced HCC treatment. Geographically, North America and Europe currently dominate the market, driven by higher healthcare expenditure and earlier adoption of advanced therapies. However, the Asia Pacific region is anticipated to exhibit the fastest growth in the coming years, fueled by a rising cancer burden, increasing healthcare investments, and a growing awareness of advanced treatment options. Restrains such as the high cost of novel therapies and the need for specialized diagnostic tools are being mitigated by increasing healthcare accessibility and evolving reimbursement policies.

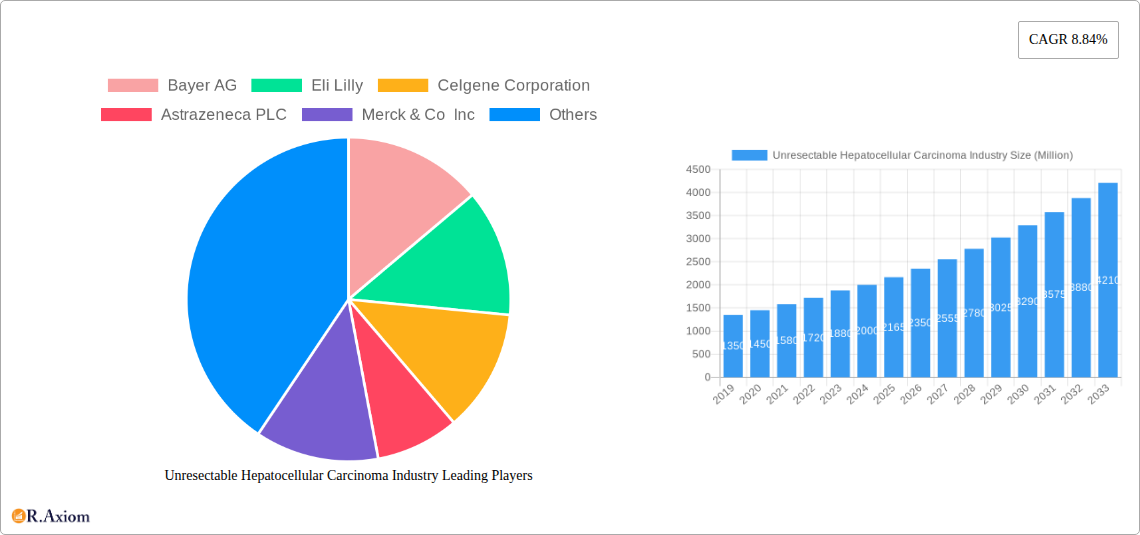

Unresectable Hepatocellular Carcinoma Industry Company Market Share

Here is an SEO-optimized, detailed report description for the Unresectable Hepatocellular Carcinoma Industry, designed for immediate use without modification:

Unresectable Hepatocellular Carcinoma Industry Market Concentration & Innovation

The Unresectable Hepatocellular Carcinoma (uHCC) industry is characterized by a dynamic market concentration, with key players such as Bayer AG, Eli Lilly, Celgene Corporation, Astrazeneca PLC, Merck & Co Inc, F Hoffmann-La Roche Ltd, Bristol-Myers-Squibb Company, Chugai Pharmaceutical Co Ltd, BeiGene, Eisai Co Ltd, Pharmaxis, and Pfizer Inc driving innovation. Innovation in uHCC treatment is largely propelled by advancements in immunotherapy and molecularly targeted therapies, leading to novel treatment regimens and improved patient outcomes. Regulatory frameworks, particularly those from the FDA and EMA, play a crucial role in market entry and drug approval, influencing the pace of innovation and market access. Product substitutes, while currently limited in the advanced uHCC space, are being explored through research into alternative therapies and combination approaches. End-user trends indicate a growing preference for specialized cancer centers equipped to handle complex oncology treatments, alongside a continued reliance on major hospitals. Mergers and acquisitions (M&A) activity, with estimated deal values in the hundreds of millions, signifies a consolidation trend as larger pharmaceutical companies seek to expand their portfolios in lucrative oncology segments. The market share of leading immunotherapy drugs is projected to reach XX% by 2033, reflecting the increasing adoption of these novel treatment modalities.

Unresectable Hepatocellular Carcinoma Industry Industry Trends & Insights

The Unresectable Hepatocellular Carcinoma (uHCC) industry is poised for substantial growth, driven by an increasing global incidence of liver cancer and advancements in therapeutic interventions. The Compound Annual Growth Rate (CAGR) for the uHCC market is estimated at approximately XX% during the forecast period of 2025–2033. This robust growth is underpinned by several key factors, including a rising prevalence of underlying conditions such as hepatitis B and C, cirrhosis, and non-alcoholic fatty liver disease, which are primary risk factors for hepatocellular carcinoma. Furthermore, the aging global population contributes to a higher incidence of chronic diseases, including liver cancer. Technological disruptions are revolutionizing uHCC treatment paradigms. The development and widespread adoption of immunotherapies, such as checkpoint inhibitors, have significantly improved progression-free survival and overall survival rates for patients with unresectable disease, transforming it from a largely palliative setting to one with potential for long-term disease control. Molecularly targeted therapies are also gaining traction, offering more precise treatment options with potentially fewer systemic side effects compared to traditional chemotherapy. Consumer preferences are shifting towards personalized medicine and treatment options that offer a better quality of life. Patients and their oncologists are increasingly seeking treatments that not only extend survival but also minimize debilitating side effects. This demand fuels research into novel drug combinations and biomarkers to identify patients most likely to benefit from specific therapies. Competitive dynamics within the uHCC market are intense, with major pharmaceutical companies investing heavily in R&D to secure a leading position. The market penetration of advanced therapies is expected to climb from XX% in 2025 to an estimated XX% by 2033, reflecting the increasing accessibility and efficacy of these treatments. The market landscape is a complex interplay of established pharmaceutical giants and emerging biotechnology firms, all vying for a share of this critical therapeutic area. The total market size is projected to reach over $XX Billion by 2033, a testament to the unmet need and the potential for innovative solutions.

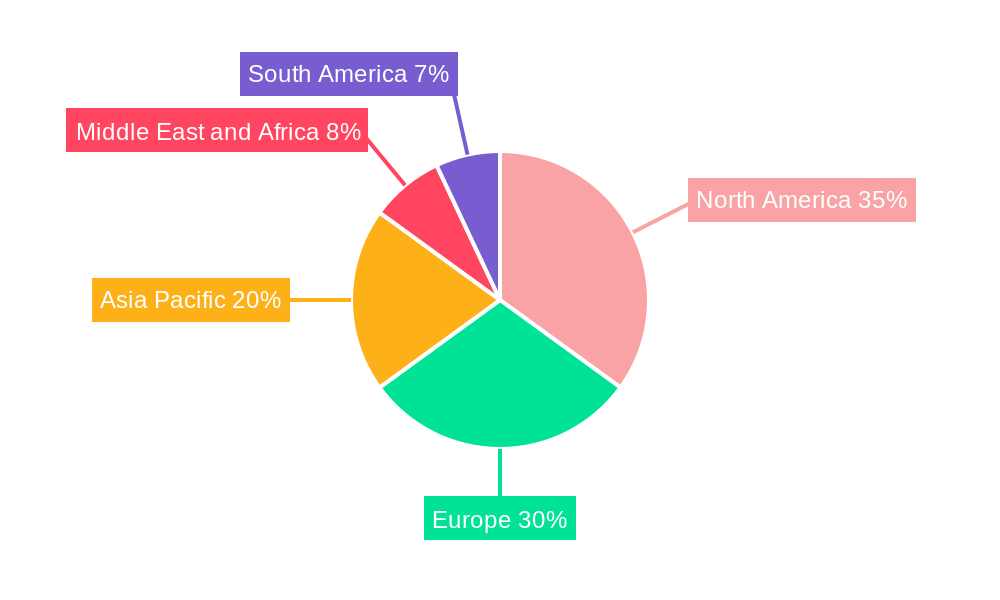

Dominant Markets & Segments in Unresectable Hepatocellular Carcinoma Industry

The Unresectable Hepatocellular Carcinoma (uHCC) market exhibits significant regional and segmental dominance, driven by a confluence of factors including healthcare infrastructure, economic development, and disease prevalence.

Dominant Region: North America, specifically the United States, currently dominates the uHCC market due to its advanced healthcare system, high disposable incomes, robust research and development infrastructure, and a well-established reimbursement framework for novel therapies. The presence of leading cancer research institutions and a high concentration of oncologists specializing in liver cancer further contribute to this dominance.

Key Drivers of Regional Dominance:

- Advanced Healthcare Infrastructure: Superior access to cutting-edge diagnostic tools and treatment facilities.

- High R&D Investment: Significant funding for clinical trials and drug development, fostering innovation.

- Favorable Reimbursement Policies: Comprehensive insurance coverage and payment models that support the adoption of expensive, innovative therapies.

- High Disease Incidence & Awareness: Increasing awareness of liver cancer risk factors and early detection initiatives.

Dominant Segments:

Treatment: Immunotherapy Immunotherapy currently holds the dominant position within the treatment segment of the uHCC market. This dominance is attributed to its proven efficacy in improving patient survival rates and its potential for durable responses. The development of immune checkpoint inhibitors has revolutionized uHCC treatment, offering a new lease on life for many patients with advanced disease. The market penetration of immunotherapy is expected to continue its upward trajectory, driven by ongoing clinical trials exploring new combinations and expanded indications.

- Key Drivers of Immunotherapy Dominance:

- Significant Efficacy Improvements: Demonstrated improvements in overall survival and progression-free survival compared to older treatment modalities.

- Durable Responses: Potential for long-lasting disease control in a subset of patients.

- Growing Clinical Evidence: Continuous influx of data from clinical trials supporting its use.

- Market Exclusivity: Prominent market share held by leading immunotherapy drugs.

- Key Drivers of Immunotherapy Dominance:

End User: Hospitals Hospitals, particularly academic medical centers and large tertiary care facilities, represent the dominant end-user segment. These institutions are equipped with the necessary infrastructure, specialized medical personnel, and patient volume to administer complex uHCC treatments, including immunotherapy and targeted therapies. They serve as primary hubs for diagnosis, treatment initiation, and ongoing patient management.

- Key Drivers of Hospital Dominance:

- Comprehensive Care Capabilities: Ability to provide multidisciplinary care, including surgery, medical oncology, radiation oncology, and supportive care.

- Access to Advanced Technology: Availability of cutting-edge diagnostic imaging, treatment delivery systems, and clinical trial participation.

- Specialized Expertise: Concentration of oncologists, hepatologists, and specialized nursing staff.

- Patient Flow: High volume of liver cancer patients seeking treatment.

- Key Drivers of Hospital Dominance:

While Molecularly Targeted Therapy is a rapidly growing segment, and Chemotherapy remains a foundational treatment, Immunotherapy's transformative impact and Hospitals' comprehensive care capabilities position them as the leading segments in the current uHCC market landscape.

Unresectable Hepatocellular Carcinoma Industry Product Developments

The Unresectable Hepatocellular Carcinoma (uHCC) industry is witnessing a surge in product developments, primarily focused on enhancing therapeutic efficacy and expanding treatment options. Innovations in immunotherapy, such as novel checkpoint inhibitors and combination therapies, are at the forefront, offering improved patient outcomes and longer survival rates. Molecularly targeted therapies are also evolving, with a focus on agents that target specific genetic mutations and signaling pathways implicated in HCC development. These advancements aim to provide more personalized treatment approaches, leading to better tolerability and efficacy. The competitive advantage of these new products lies in their ability to address unmet medical needs in a complex disease setting, offering hope for patients with previously limited therapeutic options.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the Unresectable Hepatocellular Carcinoma (uHCC) industry, segmented across key treatment modalities and end-user categories.

Treatment Segmentation: The market is analyzed based on Chemotherapy, Molecularly Targeted Therapy, Immunotherapy, and Other Treatments. Each segment's market size, growth projections, and competitive dynamics are detailed. Immunotherapy is currently the leading segment, with significant growth anticipated. Molecularly Targeted Therapy is also experiencing rapid expansion.

End-User Segmentation: The analysis covers Hospitals, Cancer Centers, and Other End Users. Hospitals represent the largest end-user segment due to their comprehensive healthcare infrastructure and patient volume. Cancer Centers are also significant contributors, specializing in advanced oncology care.

Key Drivers of Unresectable Hepatocellular Carcinoma Industry Growth

The growth of the Unresectable Hepatocellular Carcinoma (uHCC) industry is propelled by several interconnected factors. Technologically, the rapid advancements in immunotherapy, including the development of immune checkpoint inhibitors and novel combination strategies, have fundamentally changed treatment paradigms and improved patient survival. Molecularly targeted therapies, designed to inhibit specific cancer-driving pathways, are also expanding the therapeutic arsenal. Economically, increasing healthcare expenditure globally, particularly in emerging markets, and robust investment in oncology R&D by major pharmaceutical companies fuel innovation and market expansion. Regulatory factors, such as expedited approval pathways for breakthrough therapies and favorable reimbursement policies for innovative cancer treatments, further accelerate market penetration. The rising global incidence of liver cancer, driven by factors like increasing rates of obesity, viral hepatitis, and alcohol consumption, creates a growing patient pool, thus underpinning market demand.

Challenges in the Unresectable Hepatocellular Carcinoma Industry Sector

Despite significant advancements, the Unresectable Hepatocellular Carcinoma (uHCC) industry faces several challenges. High treatment costs associated with novel immunotherapies and targeted therapies pose a significant barrier to access, particularly in resource-limited regions, impacting market penetration. Regulatory hurdles and lengthy approval processes for new drugs, although streamlined for breakthrough therapies, can still delay market entry. The complexity of HCC, including its multifactorial etiology and heterogeneity, presents challenges in identifying optimal treatment strategies for all patient subsets, leading to varying treatment responses. Furthermore, the competitive landscape is increasingly crowded, with multiple players vying for market share, which can intensify pricing pressures and necessitate substantial R&D investment to maintain a competitive edge. Supply chain disruptions and manufacturing complexities for biologics and targeted therapies can also impact market availability.

Emerging Opportunities in Unresectable Hepatocellular Carcinoma Industry

Emerging opportunities in the Unresectable Hepatocellular Carcinoma (uHCC) industry are significant and diverse. The development of next-generation immunotherapies, including personalized cancer vaccines and novel combination regimens, holds immense potential for further improving patient outcomes. Biomarker discovery and the advancement of precision medicine are creating opportunities for more targeted and effective treatments, identifying patient populations most likely to respond to specific therapies. Expansion into emerging markets, with their growing healthcare infrastructure and increasing awareness of liver cancer, presents a substantial growth avenue. Furthermore, research into combination therapies that synergistically target HCC through multiple pathways, alongside advancements in early detection and non-invasive diagnostic tools, offer opportunities to transform the management of unresectable HCC and improve overall patient prognosis. The exploration of the gut microbiome's role in HCC treatment response also represents a novel area for therapeutic intervention.

Leading Players in the Unresectable Hepatocellular Carcinoma Industry Market

- Bayer AG

- Eli Lilly

- Celgene Corporation

- Astrazeneca PLC

- Merck & Co Inc

- F Hoffmann-La Roche Ltd

- Bristol-Myers-Squibb Company

- Chugai Pharmaceutical Co Ltd

- BeiGene

- Eisai Co Ltd

- Pharmaxis

- Pfizer Inc

Key Developments in Unresectable Hepatocellular Carcinoma Industry Industry

- 2023 October: Launch of novel combination immunotherapy regimen demonstrating significant progression-free survival benefits in first-line treatment.

- 2024 March: FDA approval of a new molecularly targeted therapy for patients with specific genetic mutations in unresectable HCC.

- 2024 June: Bristol-Myers-Squibb Company announced promising Phase III trial results for an expanded indication of its immunotherapy in a broader HCC patient population.

- 2024 August: Bayer AG reported positive outcomes from a study investigating a novel dual-acting agent for unresectable HCC.

- 2025 January: Merck & Co Inc initiated a global Phase III trial for its established immunotherapy in combination with a novel tyrosine kinase inhibitor.

Strategic Outlook for Unresectable Hepatocellular Carcinoma Industry Market

The strategic outlook for the Unresectable Hepatocellular Carcinoma (uHCC) market is exceptionally promising, driven by continuous innovation and a growing unmet medical need. The sustained investment in immunotherapy and molecularly targeted therapy research by leading pharmaceutical companies, including Bayer AG, Eli Lilly, and Merck & Co Inc, will continue to yield novel treatment options with enhanced efficacy and improved patient tolerability. Expansion into emerging markets presents a significant growth catalyst, as healthcare infrastructure and awareness surrounding liver cancer improve. The increasing focus on personalized medicine, guided by advanced biomarker identification, will enable more precise and effective treatment strategies, maximizing therapeutic benefits and minimizing adverse events. Strategic collaborations and potential mergers and acquisitions among key players are anticipated to further consolidate the market and accelerate the development and commercialization of innovative therapies, ultimately transforming the uHCC treatment landscape.

Unresectable Hepatocellular Carcinoma Industry Segmentation

-

1. Treatment

- 1.1. Chemotherapy

- 1.2. Molecularly Targeted Therapy

- 1.3. Immunotherapy

- 1.4. Other Treatments

-

2. End User

- 2.1. Hospitals

- 2.2. Cancer Centers

- 2.3. Other End Users

Unresectable Hepatocellular Carcinoma Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Unresectable Hepatocellular Carcinoma Industry Regional Market Share

Geographic Coverage of Unresectable Hepatocellular Carcinoma Industry

Unresectable Hepatocellular Carcinoma Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.84% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Treatment

- 5.1.1. Chemotherapy

- 5.1.2. Molecularly Targeted Therapy

- 5.1.3. Immunotherapy

- 5.1.4. Other Treatments

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Cancer Centers

- 5.2.3. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Treatment

- 6. Global Unresectable Hepatocellular Carcinoma Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Treatment

- 6.1.1. Chemotherapy

- 6.1.2. Molecularly Targeted Therapy

- 6.1.3. Immunotherapy

- 6.1.4. Other Treatments

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Cancer Centers

- 6.2.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Treatment

- 7. North America Unresectable Hepatocellular Carcinoma Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Treatment

- 7.1.1. Chemotherapy

- 7.1.2. Molecularly Targeted Therapy

- 7.1.3. Immunotherapy

- 7.1.4. Other Treatments

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Cancer Centers

- 7.2.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Treatment

- 8. Europe Unresectable Hepatocellular Carcinoma Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Treatment

- 8.1.1. Chemotherapy

- 8.1.2. Molecularly Targeted Therapy

- 8.1.3. Immunotherapy

- 8.1.4. Other Treatments

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Cancer Centers

- 8.2.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Treatment

- 9. Asia Pacific Unresectable Hepatocellular Carcinoma Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Treatment

- 9.1.1. Chemotherapy

- 9.1.2. Molecularly Targeted Therapy

- 9.1.3. Immunotherapy

- 9.1.4. Other Treatments

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Cancer Centers

- 9.2.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Treatment

- 10. Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Treatment

- 10.1.1. Chemotherapy

- 10.1.2. Molecularly Targeted Therapy

- 10.1.3. Immunotherapy

- 10.1.4. Other Treatments

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Cancer Centers

- 10.2.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Treatment

- 11. South America Unresectable Hepatocellular Carcinoma Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Treatment

- 11.1.1. Chemotherapy

- 11.1.2. Molecularly Targeted Therapy

- 11.1.3. Immunotherapy

- 11.1.4. Other Treatments

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals

- 11.2.2. Cancer Centers

- 11.2.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Treatment

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bayer AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Eli Lilly

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Celgene Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Astrazeneca PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Merck & Co Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 F Hoffmann-La Roche Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bristol-Myers-Squibb Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Chugai Pharmaceutical Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 BeiGene

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Eisai Co Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Pharmaxis

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Pfizer Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Bayer AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Unresectable Hepatocellular Carcinoma Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Unresectable Hepatocellular Carcinoma Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Treatment 2025 & 2033

- Figure 4: North America Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Treatment 2025 & 2033

- Figure 5: North America Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Treatment 2025 & 2033

- Figure 6: North America Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Treatment 2025 & 2033

- Figure 7: North America Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by End User 2025 & 2033

- Figure 8: North America Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by End User 2025 & 2033

- Figure 9: North America Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by End User 2025 & 2033

- Figure 11: North America Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Treatment 2025 & 2033

- Figure 16: Europe Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Treatment 2025 & 2033

- Figure 17: Europe Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Treatment 2025 & 2033

- Figure 18: Europe Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Treatment 2025 & 2033

- Figure 19: Europe Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by End User 2025 & 2033

- Figure 20: Europe Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by End User 2025 & 2033

- Figure 21: Europe Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by End User 2025 & 2033

- Figure 22: Europe Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by End User 2025 & 2033

- Figure 23: Europe Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Treatment 2025 & 2033

- Figure 28: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Treatment 2025 & 2033

- Figure 29: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Treatment 2025 & 2033

- Figure 30: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Treatment 2025 & 2033

- Figure 31: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by End User 2025 & 2033

- Figure 32: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by End User 2025 & 2033

- Figure 33: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by End User 2025 & 2033

- Figure 34: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by End User 2025 & 2033

- Figure 35: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Treatment 2025 & 2033

- Figure 40: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Treatment 2025 & 2033

- Figure 41: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Treatment 2025 & 2033

- Figure 42: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Treatment 2025 & 2033

- Figure 43: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by End User 2025 & 2033

- Figure 44: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by End User 2025 & 2033

- Figure 45: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by End User 2025 & 2033

- Figure 46: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by End User 2025 & 2033

- Figure 47: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Treatment 2025 & 2033

- Figure 52: South America Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Treatment 2025 & 2033

- Figure 53: South America Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Treatment 2025 & 2033

- Figure 54: South America Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Treatment 2025 & 2033

- Figure 55: South America Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by End User 2025 & 2033

- Figure 56: South America Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by End User 2025 & 2033

- Figure 57: South America Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by End User 2025 & 2033

- Figure 58: South America Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by End User 2025 & 2033

- Figure 59: South America Unresectable Hepatocellular Carcinoma Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: South America Unresectable Hepatocellular Carcinoma Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America Unresectable Hepatocellular Carcinoma Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America Unresectable Hepatocellular Carcinoma Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Treatment 2020 & 2033

- Table 2: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 3: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 5: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Treatment 2020 & 2033

- Table 8: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 9: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 11: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Treatment 2020 & 2033

- Table 20: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 21: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 22: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 23: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Germany Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: France Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Italy Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Italy Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Spain Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Spain Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Treatment 2020 & 2033

- Table 38: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 39: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 40: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 41: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: China Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: China Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Japan Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Japan Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: India Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Australia Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Australia Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: South Korea Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: South Korea Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Treatment 2020 & 2033

- Table 56: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 57: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 58: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 59: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: GCC Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: GCC Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: South Africa Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: South Africa Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: Rest of Middle East and Africa Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Treatment 2020 & 2033

- Table 68: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Treatment 2020 & 2033

- Table 69: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 70: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 71: Global Unresectable Hepatocellular Carcinoma Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 72: Global Unresectable Hepatocellular Carcinoma Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 73: Brazil Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Brazil Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Argentina Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Argentina Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Rest of South America Unresectable Hepatocellular Carcinoma Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: Rest of South America Unresectable Hepatocellular Carcinoma Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Unresectable Hepatocellular Carcinoma Industry?

The projected CAGR is approximately 8.84%.

2. Which companies are prominent players in the Unresectable Hepatocellular Carcinoma Industry?

Key companies in the market include Bayer AG, Eli Lilly, Celgene Corporation, Astrazeneca PLC, Merck & Co Inc, F Hoffmann-La Roche Ltd, Bristol-Myers-Squibb Company, Chugai Pharmaceutical Co Ltd, BeiGene, Eisai Co Ltd, Pharmaxis, Pfizer Inc.

3. What are the main segments of the Unresectable Hepatocellular Carcinoma Industry?

The market segments include Treatment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.01 Million as of 2022.

5. What are some drivers contributing to market growth?

High Incidence Rate of Liver Carcinoma; Advancement in New Treatment Options.

6. What are the notable trends driving market growth?

Chemotherapy Holds Significant Share in the Unresectable Hepatocellular Carcinoma Market.

7. Are there any restraints impacting market growth?

Less Diagnosis and Poor Efficacy of Current Therapeutic Agents.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Unresectable Hepatocellular Carcinoma Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Unresectable Hepatocellular Carcinoma Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Unresectable Hepatocellular Carcinoma Industry?

To stay informed about further developments, trends, and reports in the Unresectable Hepatocellular Carcinoma Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence