Key Insights

The Asia Pacific private banking market is experiencing robust growth, driven by a burgeoning high-net-worth individual (HNWI) population, increasing wealth concentration, and a rising demand for sophisticated wealth management solutions. The market's Compound Annual Growth Rate (CAGR) exceeding 8% from 2019 to 2024 indicates a strong upward trajectory. Key drivers include the region's expanding economies, particularly in China, India, and Southeast Asia, coupled with favorable government policies promoting financial inclusion and wealth creation. Furthermore, the increasing adoption of digital banking technologies and the growing preference for personalized financial advice contribute significantly to market expansion. This growth is segmented across various service offerings, including investment management, wealth planning, and trust and estate services. Leading players such as UBS, Credit Suisse, and HSBC are aggressively expanding their presence in the region, leveraging their global expertise and local partnerships to capture market share. Competitive pressures are intensifying, prompting banks to innovate with technologically advanced platforms and differentiated service offerings to cater to the evolving needs of sophisticated clients.

However, challenges remain. Geopolitical uncertainties, regulatory changes, and fluctuations in global financial markets pose risks to market stability. The increasing competition from fintech companies offering innovative and cost-effective solutions also necessitates adaptation and innovation from traditional private banks. Despite these challenges, the long-term outlook for the Asia Pacific private banking market remains positive, with the continued growth of the HNWI population and the ongoing demand for comprehensive wealth management services expected to fuel market expansion throughout the forecast period (2025-2033). The market is estimated to reach a significant size by 2033, based on the projected CAGR. Further segmentation within the market will likely emerge, reflecting the varied needs of HNWIs across different countries and demographics.

Asia Pacific Private Banking Market: A Comprehensive Report (2019-2033)

This comprehensive report provides a detailed analysis of the Asia Pacific private banking market, covering the period 2019-2033. With a focus on market concentration, innovation, key trends, and future growth prospects, this report is an essential resource for industry stakeholders, investors, and strategic decision-makers. The report utilizes data from the historical period (2019-2024), base year (2025), and estimated year (2025) to forecast market trends through 2033.

Asia Pacific Private Banking Market Concentration & Innovation

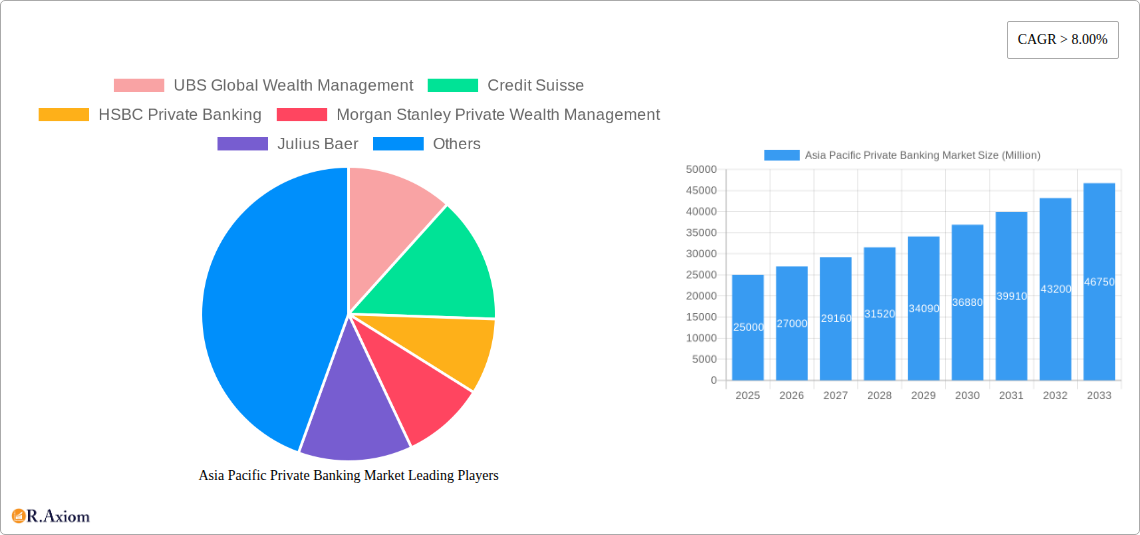

This section analyzes the competitive landscape of the Asia Pacific private banking market, examining market concentration, innovation drivers, regulatory frameworks, and M&A activities. The market is characterized by a high degree of concentration, with a few major players holding significant market share. Key players include UBS Global Wealth Management, Credit Suisse, HSBC Private Banking, Morgan Stanley Private Wealth Management, Julius Baer, J P Morgan Private Bank, Bank of Singapore, Goldman Sachs Private Wealth Management, Citi Bank, and DBS. This list is not exhaustive.

Market Concentration: The top five players collectively hold an estimated xx% market share in 2025, indicating a relatively concentrated market. However, the emergence of fintech companies and digital banks is gradually increasing competition.

Innovation Drivers: Technological advancements, evolving customer preferences, and increasing regulatory scrutiny are driving innovation within the sector. This includes the adoption of digital platforms, AI-powered solutions, and personalized wealth management services.

Regulatory Frameworks: Stringent regulatory frameworks, particularly regarding data privacy and anti-money laundering (AML), are shaping the market landscape. Compliance costs and the need for robust cybersecurity measures are key challenges for private banks.

Product Substitutes: The rise of robo-advisors and other digital wealth management platforms present a degree of substitutability for traditional private banking services, particularly for less affluent clients.

End-User Trends: A growing demand for personalized, digitally enabled, and sustainable investment solutions is reshaping client expectations. High-net-worth individuals (HNWIs) are increasingly seeking sophisticated wealth planning services, including estate planning and philanthropic advice.

M&A Activities: The Asia Pacific private banking market has witnessed several significant mergers and acquisitions (M&A) deals in recent years, with deal values exceeding xx Million in the period 2019-2024. These activities are driven by a desire to expand market reach, enhance product offerings, and achieve synergies.

Asia Pacific Private Banking Market Industry Trends & Insights

The Asia Pacific private banking market is experiencing robust growth, driven by a number of factors. The region's expanding HNWIs population, rising disposable incomes, and increasing awareness of wealth management products are key growth drivers. Technological advancements are also significantly impacting the industry, fostering innovation and efficiency.

Market Growth Drivers: The burgeoning HNWIs population in several key markets, such as China, India, and Singapore, is a primary driver. Economic growth in the region is fueling the expansion of private wealth, while favourable government policies are promoting investment in the financial sector. The increasing demand for wealth management services, including investment advisory, portfolio management, and estate planning is further boosting market growth.

Technological Disruptions: The adoption of fintech solutions, including robo-advisors, digital platforms, and AI-driven analytics, is revolutionizing the private banking experience. This is enabling greater efficiency, personalized service, and improved client engagement.

Consumer Preferences: Clients are increasingly seeking personalized wealth management strategies that align with their unique financial goals and risk tolerance. There is also a growing demand for sustainable and responsible investment solutions.

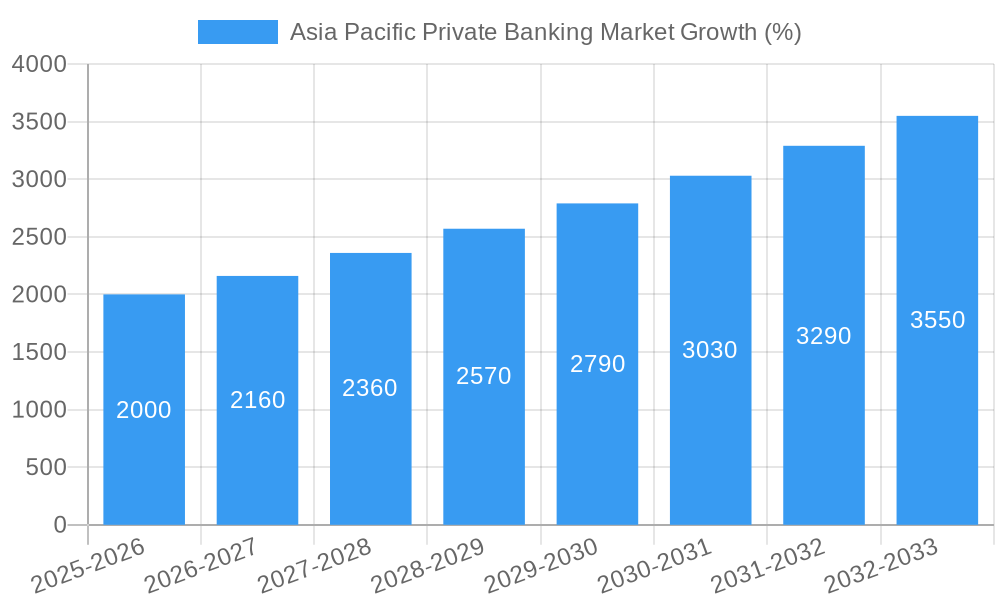

Competitive Dynamics: The market is characterized by intense competition among both traditional private banks and emerging fintech players. Banks are striving to differentiate themselves through innovative product offerings, advanced technology, and superior client service. The projected compound annual growth rate (CAGR) for the Asia Pacific private banking market during the forecast period (2025-2033) is estimated at xx%. Market penetration is expected to reach xx% by 2033.

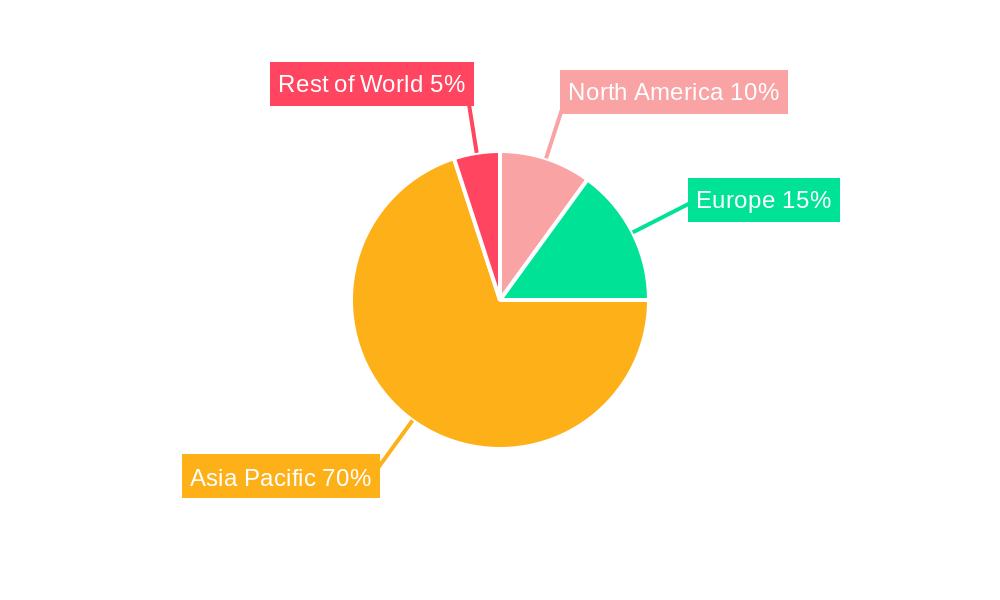

Dominant Markets & Segments in Asia Pacific Private Banking Market

This section identifies the leading markets and segments within the Asia Pacific private banking market. While specific data is unavailable, Hong Kong, Singapore, and mainland China are among the dominant markets due to robust economic growth and the concentration of HNWIs in these locations.

Key Drivers in Dominant Markets:

- Hong Kong: Established financial hub with strong regulatory frameworks and a deep pool of financial professionals.

- Singapore: Strategic geographical location, favorable tax policies, and pro-business environment.

- Mainland China: Rapid economic growth, increasing HNWIs population, and government initiatives to develop the domestic financial sector.

The analysis reveals that these markets are characterized by a high concentration of wealth, advanced financial infrastructure, and favorable regulatory environments. Detailed dominance analysis would further explore specific market share, growth rates, and competitive landscapes within each region.

Asia Pacific Private Banking Market Product Developments

Recent years have witnessed significant product innovation within the Asia Pacific private banking sector. Banks are increasingly leveraging technology to enhance client engagement, personalize service, and optimize investment strategies. The integration of artificial intelligence (AI) and big data analytics is enabling the development of sophisticated investment solutions and personalized financial planning tools. The rise of digital platforms is making wealth management services more accessible and convenient, expanding the reach of private banks to a broader clientele. The growing focus on sustainable and ESG (Environmental, Social, and Governance) investing reflects changing client preferences and the importance of socially responsible investing.

Report Scope & Segmentation Analysis

This report segments the Asia Pacific private banking market based on several key parameters, including client type (HNWIs, ultra-high-net-worth individuals (UHNWIs)), product type (wealth planning, investment management, trust services), and service channel (digital platforms, private banking branches). Each segment displays diverse growth projections, market sizes, and competitive dynamics. The report provides detailed analysis of each segment, highlighting growth drivers, key players, and competitive pressures.

Key Drivers of Asia Pacific Private Banking Market Growth

The Asia Pacific private banking market is poised for substantial growth driven by a confluence of factors. The burgeoning HNWIs population, fueled by rapid economic growth across the region, is a key driver. Increasing disposable incomes are enabling more individuals to accumulate significant wealth and seek professional wealth management services. Favourable government policies aimed at promoting financial sector development and attracting foreign investment also contribute. Finally, technological advancements, such as digital platforms and AI-driven solutions, are transforming the delivery of private banking services and expanding market reach.

Challenges in the Asia Pacific Private Banking Market Sector

Despite promising growth prospects, the Asia Pacific private banking market faces several challenges. Stringent regulatory compliance requirements, including AML and KYC (Know Your Customer) regulations, increase operational costs and complexity. Cybersecurity threats pose a significant risk to data security and operational continuity. Intense competition from both established private banks and emerging fintech players pressures profit margins and necessitates continuous innovation to maintain a competitive edge. Geopolitical instability and economic volatility in certain regions can also dampen market growth.

Emerging Opportunities in Asia Pacific Private Banking Market

The Asia Pacific private banking sector presents numerous emerging opportunities. The expansion of the HNWIs population in emerging markets presents significant growth potential. The increasing adoption of digital technologies offers opportunities for innovative service delivery and enhanced client engagement. The growing focus on sustainable and responsible investments creates demand for specialized products and services. Furthermore, developing innovative solutions to meet the unique financial needs of specific demographic segments presents a fertile ground for differentiation and expansion within the market.

Leading Players in the Asia Pacific Private Banking Market Market

- UBS Global Wealth Management

- Credit Suisse

- HSBC Private Banking

- Morgan Stanley Private Wealth Management

- Julius Baer

- J P Morgan Private Bank

- Bank of Singapore

- Goldman Sachs Private Wealth Management

- Citi Bank

- DBS

- List Not Exhaustive

Key Developments in Asia Pacific Private Banking Market Industry

November 2022: SBC Global Private Banking launched its discretionary digital platform (DPM) in Asia, becoming the first bank in the region to offer this service on a mobile app. This signifies a significant shift towards digitalization in the private banking sector.

February 2023: GXS, a digital bank majority-owned by Grab, expanded its services. Its innovative approach to showcasing interest accrual on deposits highlights a focus on transparency and user-friendly digital banking. The offering of high-interest time deposits (3.48%) compared to regular savings accounts (0.08%) demonstrates a competitive strategy focused on attracting customers with attractive deposit rates.

Strategic Outlook for Asia Pacific Private Banking Market Market

The Asia Pacific private banking market is poised for continued growth, driven by the region's robust economic expansion, burgeoning HNWIs population, and technological advancements. Opportunities exist in expanding into underserved markets, developing innovative digital solutions, and offering specialized wealth management products tailored to specific client needs. Banks that effectively leverage technology, embrace sustainability, and deliver personalized service will be best positioned to capture market share and drive future growth.

Asia Pacific Private Banking Market Segmentation

-

1. Type

- 1.1. Asset Management Service

- 1.2. Insurance Service

- 1.3. Trust Service

- 1.4. Tax Consulting

- 1.5. Real Estate Consulting

-

2. Application

- 2.1. Personal

- 2.2. Enterprise

Asia Pacific Private Banking Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Private Banking Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 8.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Rising Insurance Business in Asia Pacific

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Asia Pacific Private Banking Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Asset Management Service

- 5.1.2. Insurance Service

- 5.1.3. Trust Service

- 5.1.4. Tax Consulting

- 5.1.5. Real Estate Consulting

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Personal

- 5.2.2. Enterprise

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 UBS Global Wealth Management

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Credit Suisse

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 HSBC Private Banking

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Morgan Stanley Private Wealth Management

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Julius Baer

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 J P Morgan Private Bank

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Bank of Singapore

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Goldman Sachs Private Wealth Management

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Citi Bank

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 DBS**List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 UBS Global Wealth Management

List of Figures

- Figure 1: Asia Pacific Private Banking Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Asia Pacific Private Banking Market Share (%) by Company 2024

List of Tables

- Table 1: Asia Pacific Private Banking Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Asia Pacific Private Banking Market Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Asia Pacific Private Banking Market Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Asia Pacific Private Banking Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Asia Pacific Private Banking Market Revenue Million Forecast, by Type 2019 & 2032

- Table 6: Asia Pacific Private Banking Market Revenue Million Forecast, by Application 2019 & 2032

- Table 7: Asia Pacific Private Banking Market Revenue Million Forecast, by Country 2019 & 2032

- Table 8: China Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Japan Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: South Korea Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: India Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Australia Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: New Zealand Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Indonesia Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Malaysia Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Singapore Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Thailand Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Vietnam Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Philippines Asia Pacific Private Banking Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Private Banking Market?

The projected CAGR is approximately > 8.00%.

2. Which companies are prominent players in the Asia Pacific Private Banking Market?

Key companies in the market include UBS Global Wealth Management, Credit Suisse, HSBC Private Banking, Morgan Stanley Private Wealth Management, Julius Baer, J P Morgan Private Bank, Bank of Singapore, Goldman Sachs Private Wealth Management, Citi Bank, DBS**List Not Exhaustive.

3. What are the main segments of the Asia Pacific Private Banking Market?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Rising Insurance Business in Asia Pacific.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

February 2023: GXS, a digital bank majority owned by Grab, operator of Southeast Asia's ubiquitous super app, expanded services since opening in September. GXS's app hardly looks like a banking app. The app updates GXS account holders with daily reports on how much interest their deposits have accrued. While a regular savings account offers 0.08% interest, time deposits, opened for specific purposes such as travel or layaway purchases, earn 3.48%.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Private Banking Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Private Banking Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Private Banking Market?

To stay informed about further developments, trends, and reports in the Asia Pacific Private Banking Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence