Key Insights

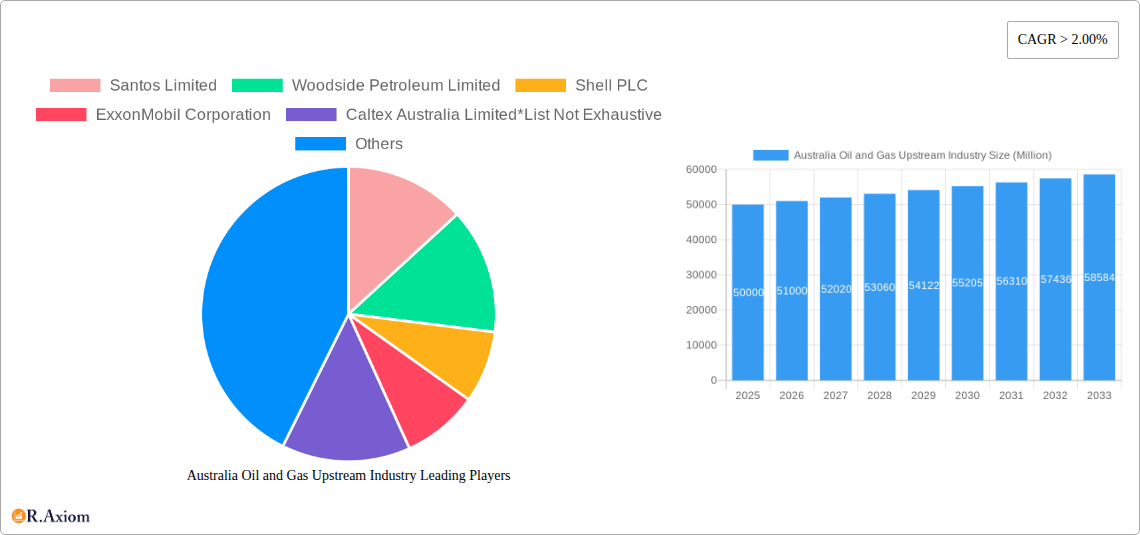

The Australian oil and gas upstream industry, encompassing exploration, development, and production, is a significant contributor to the nation's economy. While precise market size figures for 2019-2024 are unavailable, the provided data indicates a market valued at (let's assume) $XX million in 2025, experiencing a Compound Annual Growth Rate (CAGR) exceeding 2.00%. This positive growth trajectory is fueled by several factors. Firstly, consistent global demand for energy resources, particularly natural gas, continues to underpin investment and production within the sector. Secondly, advancements in offshore exploration technologies and efficient extraction methods are unlocking previously inaccessible reserves, contributing to output. Furthermore, government policies promoting domestic energy security and strategic investment in infrastructure development are encouraging expansion. However, the industry faces challenges, including fluctuating global energy prices and increasing pressure to adopt sustainable practices to mitigate environmental impacts. The segmentation of the market into onshore and offshore operations, along with oil and gas products, reveals differing growth dynamics. Onshore operations may experience slower growth due to land access constraints and regulatory hurdles, while offshore exploration might exhibit faster growth due to technological advancements. Key players like Santos Limited, Woodside Petroleum Limited, and international giants like Shell and ExxonMobil, are actively shaping the market landscape through strategic acquisitions, technological innovation, and exploration efforts. The competitive landscape is marked by both domestic and international entities, reflecting the significant global interest in Australia's energy resources.

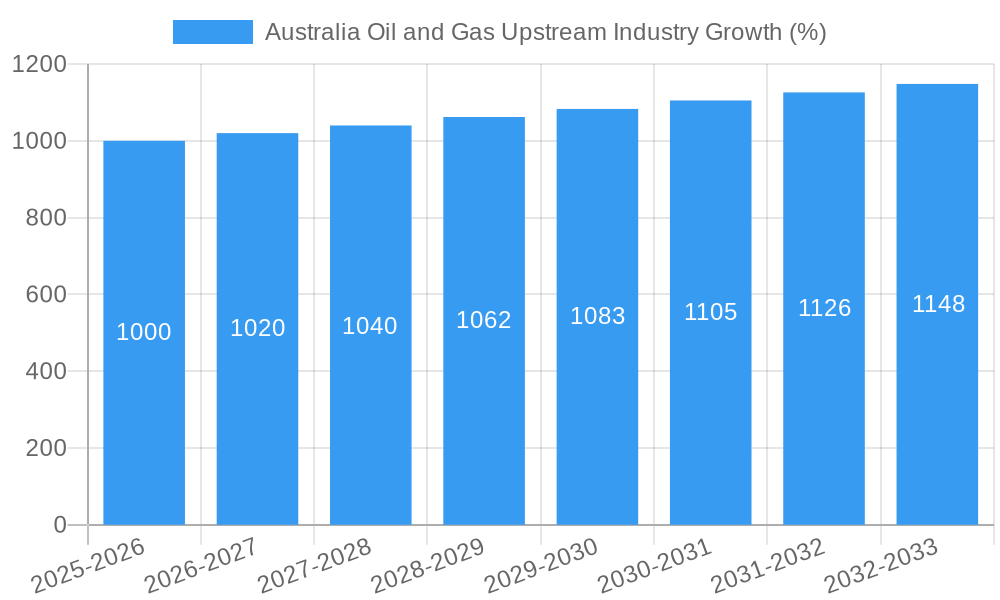

The forecast period (2025-2033) projects continued growth, albeit potentially at a moderated rate. While the specific CAGR beyond 2025 is not given, a conservative estimate, given industry trends and global energy forecasts, suggests a sustainable but potentially slightly decreasing growth rate in the latter half of the forecast period. This moderation could stem from increased regulatory scrutiny on environmental concerns and potential shifts towards renewable energy sources. The ongoing balance between global energy needs, environmental considerations, and investment strategies will be key determinants of the Australian oil and gas upstream industry's trajectory in the coming years. Companies will need to adapt their strategies to navigate these competing forces, with a focus on sustainability, efficiency, and responsible resource management.

This comprehensive report provides a detailed analysis of the Australian oil and gas upstream industry, covering market dynamics, key players, technological advancements, and future growth prospects. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The report offers actionable insights for industry stakeholders, investors, and policymakers.

Australia Oil and Gas Upstream Industry Market Concentration & Innovation

This section analyzes the competitive landscape, innovation drivers, regulatory environment, and market dynamics within the Australian oil and gas upstream sector. The historical period (2019-2024) reveals a moderately concentrated market, with several major players holding significant market share. Santos Limited, Woodside Petroleum Limited, and BHP Group PLC consistently rank among the top players. However, the market share distribution is dynamic, influenced by M&A activity and exploration successes.

Market Concentration Metrics (2024):

- Top 3 players' combined market share: xx%

- Average deal value (M&A, 2019-2024): $xx Million

Innovation Drivers:

- Government incentives for renewable energy integration and carbon capture technologies.

- Growing demand for advanced digital technologies in exploration, production, and operations.

- Focus on enhancing operational efficiency and safety through automation and AI.

Regulatory Framework & Product Substitutes:

The Australian regulatory framework significantly impacts industry operations, emphasizing environmental protection and safety standards. The increasing focus on renewable energy sources presents a challenge in terms of market share and long-term investment strategies. There is a limited number of direct substitutes for oil and gas in certain applications, which provides some stability despite the growing renewable energy sector.

End-User Trends & M&A Activities:

The Australian oil and gas upstream industry's end-users largely include domestic and international energy companies, power generation plants, and industrial consumers. Recent M&A activities have involved significant transactions, driven by consolidation, portfolio diversification, and technological advancements. The strategic alliances reflect increasing collaboration within the industry to address operational challenges and ensure long-term sustainability.

Australia Oil and Gas Upstream Industry Industry Trends & Insights

The Australian oil and gas upstream industry experienced xx% CAGR during 2019-2024 and is projected to grow at xx% CAGR from 2025-2033. Market growth is driven by increasing global energy demand, particularly in Asia, and domestic consumption in Australia, despite increasing investment in renewable energy alternatives. Technological disruptions such as advancements in subsea production and digitalization are driving efficiency gains and reducing operational costs. This includes the adoption of AI and machine learning to enhance safety, improve forecasting, and optimize extraction processes. Consumer preferences are shifting towards cleaner energy sources, placing increasing pressure on oil and gas companies to adopt sustainable practices and reduce their carbon footprint. The competitive dynamics are shaped by a combination of established players, new entrants focusing on innovative technologies and smaller companies specializing in niche areas. These factors create a dynamic market landscape characterized by both competition and collaboration, with companies continually seeking to adapt and innovate to maintain their competitiveness.

Dominant Markets & Segments in Australia Oil and Gas Upstream Industry

The Australian oil and gas upstream industry is geographically diversified, with significant activities in both onshore and offshore areas across different states. However, the offshore segment currently holds a dominant market share due to significant reserves and established infrastructure.

Leading Segments:

- Offshore: Dominated by large-scale projects, leveraging advanced technologies and requiring high capital investment. Key drivers include substantial proven reserves, favorable regulatory frameworks, access to global markets, and established export infrastructure.

- Onshore: Characterized by smaller-scale operations, with a focus on cost-efficiency and sustainable practices. Drivers include proximity to processing facilities, lower infrastructure costs and the opportunity to leverage emerging technologies for improved efficiency.

Key Regional Drivers:

- Western Australia: Rich in offshore oil and gas reserves, well-developed infrastructure, and strategic location for Asian exports.

- Queensland: Significant onshore gas resources, increasing exploration activity, and expanding LNG export capabilities.

- Northern Territory: Large untapped resources and emerging opportunities, facing both potential benefits and substantial environmental concerns.

The dominance of Offshore and Western Australia stems from the presence of large-scale projects and reserves, mature infrastructure, and government incentives promoting exploration and production.

Australia Oil and Gas Upstream Industry Product Developments

Recent product innovations focus on improving efficiency, safety, and environmental performance. This includes advanced subsea compression technology, enhancing the extraction of gas from deepwater fields. Improved drilling techniques, enhanced oil recovery methods, and the integration of AI-powered monitoring systems are also significant developments contributing to a more sustainable and efficient oil and gas industry. These innovations aim to maximize resource recovery, reduce operational costs, and mitigate environmental impact.

Report Scope & Segmentation Analysis

This report segments the Australian oil and gas upstream market based on Product (Oil and Gas) and Location of Deployment (Onshore and Offshore).

Product:

- Oil: The oil segment is projected to witness moderate growth driven by consistent global demand and domestic consumption. Market competition is characterized by established players with significant market share.

- Gas: The gas segment demonstrates stronger growth potential driven by increasing domestic and export demand, particularly LNG. The market displays a mixture of both established players and newer companies focusing on innovative exploration and production techniques.

Location of Deployment:

- Onshore: The onshore segment offers opportunities for smaller companies to participate and is experiencing growth fueled by investments in advanced technologies and the focus on cleaner energy solutions. Competitive dynamics are more fragmented with a variety of players.

- Offshore: The offshore segment dominates the market with large-scale projects and considerable capital investments. Competition is higher among established companies which possess significant resources.

Key Drivers of Australia Oil and Gas Upstream Industry Growth

Several factors drive the growth of the Australian oil and gas upstream industry. These include sustained global demand for energy, significant reserves, supportive government policies encouraging exploration and development, and technological advancements enhancing efficiency and productivity. Moreover, strategic investments in infrastructure, particularly LNG export facilities, are contributing to market expansion.

Challenges in the Australia Oil and Gas Upstream Industry Sector

The Australian oil and gas upstream industry faces challenges including fluctuating global oil and gas prices, stringent environmental regulations necessitating high operational costs, and increased scrutiny from environmental groups. Supply chain disruptions and skilled labor shortages also impede growth. Additionally, the increasing focus on transitioning to renewable energy poses a long-term challenge.

Emerging Opportunities in Australia Oil and Gas Upstream Industry

Emerging opportunities include the development of carbon capture and storage technologies, investment in renewable gas sources such as biomethane, and exploration of untapped resources in frontier regions. The integration of digital technologies and AI in exploration and production offers further scope for innovation and efficiency gains.

Leading Players in the Australia Oil and Gas Upstream Industry Market

- Santos Limited

- Woodside Petroleum Limited

- Shell PLC

- ExxonMobil Corporation

- Caltex Australia Limited

- BHP Group PLC

- Origin Energy Limited

- Chevron Corporation

- BP PLC

- Total Energies SE

Key Developments in Australia Oil and Gas Upstream Industry Industry

- September 2021: Wood and NERA partnered to develop the Augmented Machine Vision Solution (AMVS), an advanced AI technology for inspecting subsea oil and gas infrastructure, improving speed, accuracy, and safety.

- August 2021: Chevron awarded a USD 6 billion contract to Worley for the Jansz-lo Compression project in Western Australia, utilizing advanced subsea compression technology to supply natural gas.

Strategic Outlook for Australia Oil and Gas Upstream Industry Market

The Australian oil and gas upstream industry is poised for continued growth, driven by global energy demand and technological advancements. However, a strategic focus on sustainability, technological innovation, and efficient resource management will be crucial for long-term success. Companies that successfully navigate the challenges of climate change concerns and regulatory pressures will be best positioned to capitalize on future opportunities.

Australia Oil and Gas Upstream Industry Segmentation

- 1. Onshore

- 2. Offshore

Australia Oil and Gas Upstream Industry Segmentation By Geography

- 1. Australia

Australia Oil and Gas Upstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 2.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Modernization and Upgrades of Existing Military Aircraft Fleets4.; Increasing Defense Budgets

- 3.3. Market Restrains

- 3.3.1. 4.; Shift Toward Unmanned Aircraft

- 3.4. Market Trends

- 3.4.1. Offshore Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Oil and Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 5.2. Market Analysis, Insights and Forecast - by Offshore

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Santos Limited

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Woodside Petroleum Limited

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Shell PLC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 ExxonMobil Corporation

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Caltex Australia Limited*List Not Exhaustive

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 BHP Group PLC

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Origin Energy Limited

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Chevron Corporation

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 BP PLC

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Total Energies SE

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Santos Limited

List of Figures

- Figure 1: Australia Oil and Gas Upstream Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Australia Oil and Gas Upstream Industry Share (%) by Company 2024

List of Tables

- Table 1: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Onshore 2019 & 2032

- Table 3: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Offshore 2019 & 2032

- Table 4: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Onshore 2019 & 2032

- Table 7: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Offshore 2019 & 2032

- Table 8: Australia Oil and Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Oil and Gas Upstream Industry?

The projected CAGR is approximately > 2.00%.

2. Which companies are prominent players in the Australia Oil and Gas Upstream Industry?

Key companies in the market include Santos Limited, Woodside Petroleum Limited, Shell PLC, ExxonMobil Corporation, Caltex Australia Limited*List Not Exhaustive, BHP Group PLC, Origin Energy Limited, Chevron Corporation, BP PLC, Total Energies SE.

3. What are the main segments of the Australia Oil and Gas Upstream Industry?

The market segments include Onshore, Offshore.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Modernization and Upgrades of Existing Military Aircraft Fleets4.; Increasing Defense Budgets.

6. What are the notable trends driving market growth?

Offshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Shift Toward Unmanned Aircraft.

8. Can you provide examples of recent developments in the market?

In September 2021, a partnership between Wood and National Energy Resources Australia (NERA) developed an advanced AI technology known as Augmented Machine Vision Solution (AMVS). This technology is expected to assist in inspecting industrial equipment, especially subsea oil and gas infrastructure. This new innovative solution improves speed and accuracy and reduces human risk. It also has the potential to be executed in various industries to enhance reliability and reduce inspection costs.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Oil and Gas Upstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Oil and Gas Upstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Oil and Gas Upstream Industry?

To stay informed about further developments, trends, and reports in the Australia Oil and Gas Upstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence