Key Insights

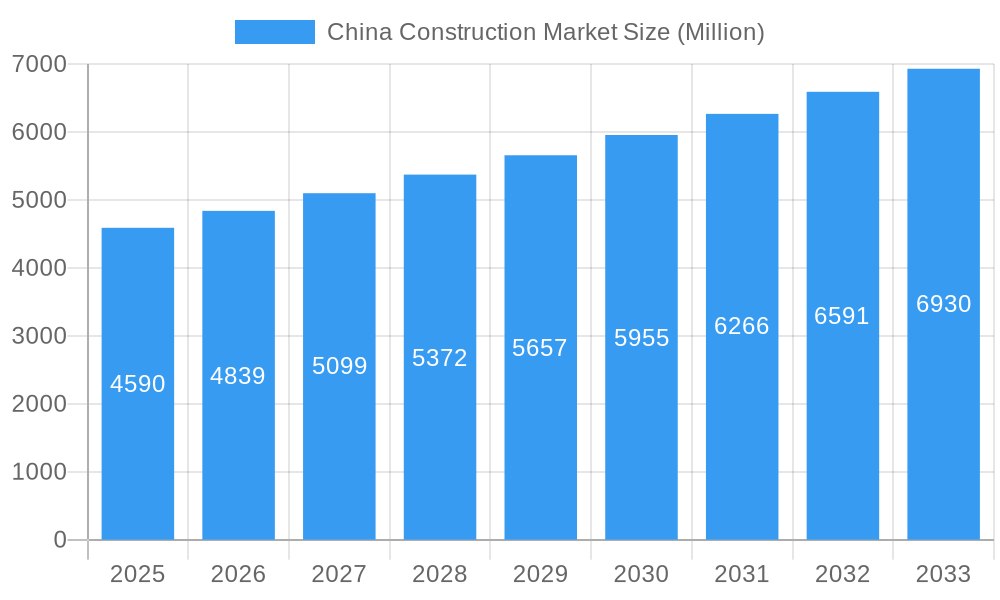

The China construction market, valued at $4.59 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 5.07% from 2025 to 2033. This expansion is driven by several key factors. Firstly, significant government investments in infrastructure projects, particularly within transportation (high-speed rail, roads, and ports) and energy & utilities (renewable energy installations and grid modernization), are fueling demand. Secondly, rapid urbanization and a burgeoning middle class are driving residential and commercial construction activity. The rising need for modern, sustainable buildings further contributes to this growth. However, challenges exist. Fluctuations in raw material prices, particularly steel and cement, coupled with potential labor shortages and environmental regulations, could act as restraints on market expansion. The market is segmented by sector, with residential, commercial, industrial, infrastructure (transportation), and energy & utilities representing significant components. Key players include state-owned enterprises such as China State Construction Engineering, China Communications Construction Company, and China Railway Group, along with several other prominent players in the construction sector. These companies are strategically positioned to benefit from the ongoing infrastructure development and urbanization initiatives. The forecast period suggests continued, albeit moderated, growth, with potential for acceleration depending on government policy and economic conditions.

China Construction Market Market Size (In Billion)

The competitive landscape is dominated by large, integrated state-owned enterprises, reflecting the significant role of the government in infrastructure development. These companies possess considerable financial resources and experience in large-scale projects. However, the market also sees the emergence of specialized private companies focusing on niche segments like green building technologies and sustainable infrastructure solutions. These companies leverage innovation to compete and cater to the growing demand for environmentally friendly construction practices. Competition is likely to intensify as private companies seek to capture a larger share of the market. The market's future growth trajectory will depend on a balance between government investment, economic stability, and the successful implementation of sustainable and efficient construction practices.

China Construction Market Company Market Share

China Construction Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the China construction market, covering market size, segmentation, key players, growth drivers, challenges, and future opportunities. The study period spans 2019-2033, with 2025 as the base and estimated year. The forecast period is 2025-2033, and the historical period covers 2019-2024. This report is invaluable for industry stakeholders, investors, and businesses seeking to understand and navigate the dynamic landscape of the Chinese construction sector.

China Construction Market Market Concentration & Innovation

The Chinese construction market exhibits a high degree of concentration, with a few large state-owned enterprises (SOEs) dominating the landscape. These companies often hold significant market share in specific segments. However, a growing number of private companies are emerging, increasing competition and fostering innovation. The market is characterized by a complex interplay of factors including government regulations, technological advancements, and fluctuating demand across various sectors.

Key Metrics & Observations:

- Market Concentration: The top 5 companies account for approximately xx% of the total market revenue (2024 estimate). This concentration is expected to remain significant throughout the forecast period, though competitive pressures from smaller players will likely increase.

- M&A Activity: The value of M&A deals in the construction sector has fluctuated in recent years. In 2024, the total value reached approximately $xx Million, reflecting a slowdown in larger-scale acquisitions.

- Innovation Drivers: Government initiatives promoting green building technologies, infrastructure development, and technological advancements in construction methods are key innovation drivers. The adoption of Building Information Modeling (BIM) and other digital technologies is also rapidly accelerating.

- Regulatory Frameworks: Stringent building codes and environmental regulations significantly influence the construction sector. Compliance costs and the need for sustainable practices impact both the operational costs and innovation in construction technologies and materials.

- Product Substitutes: The emergence of prefabricated construction methods and alternative building materials presents new competitive pressures. While traditional methods still dominate, the market share of substitutes is expected to gradually increase.

- End-User Trends: Growing urbanization and rising disposable incomes are driving demand for high-quality residential and commercial spaces. Increasing government spending on infrastructure projects further stimulates the construction market's growth.

China Construction Market Industry Trends & Insights

The China construction market is experiencing robust growth fueled by sustained government investment in infrastructure, rapid urbanization, and the increasing demand for housing and commercial spaces. Technological advancements, such as BIM and prefabrication, are transforming construction practices, enhancing efficiency and productivity. However, the sector faces challenges like rising material costs, skilled labor shortages, and stringent environmental regulations.

- Market Growth Drivers: Government policies promoting infrastructure development, urbanization, and housing initiatives are major drivers. The Belt and Road Initiative continues to create substantial opportunities for Chinese construction firms internationally.

- Technological Disruptions: The adoption of advanced technologies like BIM, 3D printing, and robotics is increasing efficiency and reducing construction times. This leads to improved project management, cost optimization, and better quality control.

- Consumer Preferences: Increased demand for sustainable and eco-friendly buildings, smart homes, and technologically advanced infrastructure projects is shaping market trends. Consumers are becoming increasingly aware of environmental impacts and sustainable development goals.

- Competitive Dynamics: The market is highly competitive, with both SOEs and private companies vying for market share. The landscape is characterized by significant consolidation and strategic alliances aimed at expanding capabilities and market presence. The market growth rate (CAGR) from 2025 to 2033 is estimated to be xx%. Market penetration of innovative technologies like BIM is growing rapidly and is expected to reach xx% by 2033.

Dominant Markets & Segments in China Construction Market

The Chinese construction market is vast and diverse, with significant variations across different regions and sectors. While precise dominance cannot be easily quantified without specific data, certain regions and segments consistently display higher activity and growth.

- Leading Regions: Provinces with rapid urbanization and strong economic growth generally show higher construction activity. Tier 1 cities like Beijing, Shanghai, Guangzhou, and Shenzhen consistently have the highest demand for new construction.

- Dominant Sectors:

- Infrastructure (Transportation): This sector receives substantial government investment, making it consistently among the largest market segments. High-speed rail projects, road networks, and urban transit systems drive growth.

- Residential: Growing urbanization and a rising middle class fuel strong demand for residential construction. This sector is expected to remain a key market driver for the foreseeable future.

- Commercial: Growth in this sector mirrors overall economic development and the expansion of the service industry. Office buildings, shopping malls, and other commercial spaces are major components.

- Industrial: Demand for industrial construction is tied to manufacturing and industrial production, demonstrating cyclical patterns.

- Energy and Utilities: This sector involves large-scale projects, typically driven by government policy and the need for expanding energy capacity and improving infrastructure.

Key Drivers of Dominance:

- Government Policies: Infrastructure spending, housing policies, and other economic strategies are influential in determining market dominance.

- Economic Growth: Regional economic strength significantly correlates with construction activity.

- Urbanization: Areas experiencing rapid urbanization exhibit higher demand for housing and infrastructure projects.

China Construction Market Product Developments

The Chinese construction market witnesses continuous product innovation focused on efficiency, sustainability, and cost-effectiveness. Prefabricated construction methods are gaining traction, alongside the use of advanced materials like high-strength concrete and sustainable building materials. Technological integration is a key trend, with Building Information Modeling (BIM) becoming increasingly prevalent, offering improved design, planning, and project management capabilities. The development of smart building technologies integrates Internet of Things (IoT) capabilities, energy efficiency features, and automated systems into building projects, enhancing operational efficiency and building value.

Report Scope & Segmentation Analysis

This report segments the China construction market by sector: Residential, Commercial, Industrial, Infrastructure (Transportation), and Energy and Utilities. Each segment is analyzed based on market size, growth projections, and competitive dynamics.

- Residential: This segment is characterized by high demand, driven by urbanization and a growing middle class, resulting in xx Million in 2025.

- Commercial: This segment shows strong growth, driven by economic expansion and increasing investment in commercial real estate, expected to reach xx Million by 2025.

- Industrial: Growth in this segment reflects the manufacturing and industrial activity with xx Million market size in 2025.

- Infrastructure (Transportation): Significant government investment drives substantial growth in this segment, with a market size estimated at xx Million in 2025.

- Energy and Utilities: This segment is driven by energy demand and infrastructure development, reaching xx Million in 2025.

Key Drivers of China Construction Market Growth

Several factors contribute to the China construction market's growth:

- Government Investment: Substantial government spending on infrastructure development and housing programs fuels market expansion.

- Urbanization: Rapid urbanization drives demand for new housing, commercial spaces, and infrastructure.

- Economic Growth: Overall economic expansion positively impacts construction activity.

- Technological Advancements: The adoption of innovative construction technologies increases efficiency and reduces costs.

Challenges in the China Construction Market Sector

The sector faces various challenges:

- Rising Material Costs: Fluctuations in material prices impact project costs and profitability.

- Skilled Labor Shortages: A shortage of skilled labor limits project completion and increases costs.

- Stringent Regulations: Strict environmental and building codes increase compliance costs and complexity.

- Supply Chain Disruptions: Occasional supply chain disruptions can delay projects and affect overall costs.

Emerging Opportunities in China Construction Market

Several opportunities exist:

- Green Building Technologies: The growing demand for sustainable buildings opens opportunities for eco-friendly construction.

- Smart City Initiatives: Smart city development drives demand for advanced infrastructure and technologies.

- Prefabricated Construction: Prefabricated construction offers efficiency and cost advantages, creating opportunities for growth.

- Technological Integration: The increasing use of BIM and other technologies improves efficiency and project management.

Leading Players in the China Construction Market Market

- China National Chemical Engineering

- China Metallurgical Group

- China State Construction Engineering China State Construction Engineering

- China Communications Construction Company China Communications Construction Company

- China Railway Group

- China Railway Construction

- China Energy Engineering Corporation

- Shanghai Construction Group

- China Petroleum Engineering Corporation

- Power Construction Corporation of China

Key Developments in China Construction Market Industry

- December 2023: Two Chinese construction projects received Awards of Merit from Engineering News-Record (ENR): The Lamu Port Berth 1-3 Project (Airport and Port category) and the Peljesac Bridge (Bridge and Tunnel category). This recognition enhances the global reputation of Chinese construction firms.

- July 2023: The Shaoxing Metro Line 2, constructed by CRCC, opened, marking a significant advancement in automated and driverless subway systems in China. This boosts Shaoxing's infrastructure and supports the Hangzhou Asian Games.

Strategic Outlook for China Construction Market Market

The future of the China construction market looks promising, driven by sustained government investment, urbanization, and technological advancements. The focus on green building technologies and smart city initiatives will create new opportunities for growth and innovation. The increasing integration of technology and the emphasis on sustainable practices will shape the future of the sector, demanding a robust and adaptable approach from market players.

China Construction Market Segmentation

-

1. Sector

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

- 1.4. Infrastruture (Transportation)

- 1.5. Energy and Utilities

China Construction Market Segmentation By Geography

- 1. China

China Construction Market Regional Market Share

Geographic Coverage of China Construction Market

China Construction Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.07% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.1.4. Infrastruture (Transportation)

- 5.1.5. Energy and Utilities

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. China

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. China Construction Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Residential

- 6.1.2. Commercial

- 6.1.3. Industrial

- 6.1.4. Infrastruture (Transportation)

- 6.1.5. Energy and Utilities

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China National Chemical Engineering

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 China Metallurgical Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 China State Construction Engineering

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 China Communications Construction Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 China Railway Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 China Railway Construction

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 China Energy Engineering Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Shanghai Construction Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 China Petroleum Engineering Corporation**List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Power Construction Corporation of China

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 China National Chemical Engineering

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Construction Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Construction Market Share (%) by Company 2025

List of Tables

- Table 1: China Construction Market Revenue Million Forecast, by Sector 2020 & 2033

- Table 2: China Construction Market Revenue Million Forecast, by Region 2020 & 2033

- Table 3: China Construction Market Revenue Million Forecast, by Sector 2020 & 2033

- Table 4: China Construction Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Construction Market?

The projected CAGR is approximately 5.07%.

2. Which companies are prominent players in the China Construction Market?

Key companies in the market include China National Chemical Engineering, China Metallurgical Group, China State Construction Engineering, China Communications Construction Company, China Railway Group, China Railway Construction, China Energy Engineering Corporation, Shanghai Construction Group, China Petroleum Engineering Corporation**List Not Exhaustive, Power Construction Corporation of China.

3. What are the main segments of the China Construction Market?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.59 Million as of 2022.

5. What are some drivers contributing to market growth?

Government Infrastructure Spending; Urbanization and Increasing Disposable Incomes.

6. What are the notable trends driving market growth?

Increase in Output value of China Construction Industry.

7. Are there any restraints impacting market growth?

Oversupply in the Real Estate; Labor Shortages.

8. Can you provide examples of recent developments in the market?

December 2023: Recently, "Engineering News-Record" (ENR), one of the world's most authoritative academic journals in engineering and construction, announced the winners of the 2023 Global Best Projects Awards. I received awards for two projects. The Lamu Port Berth 1-3 Project was honored with the Award of Merit in the Airport and Port category, while the Peljesac Bridge and its access roads in Croatia received the Award of Merit in the Bridge and Tunnel category.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Construction Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Construction Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Construction Market?

To stay informed about further developments, trends, and reports in the China Construction Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence