Key Insights

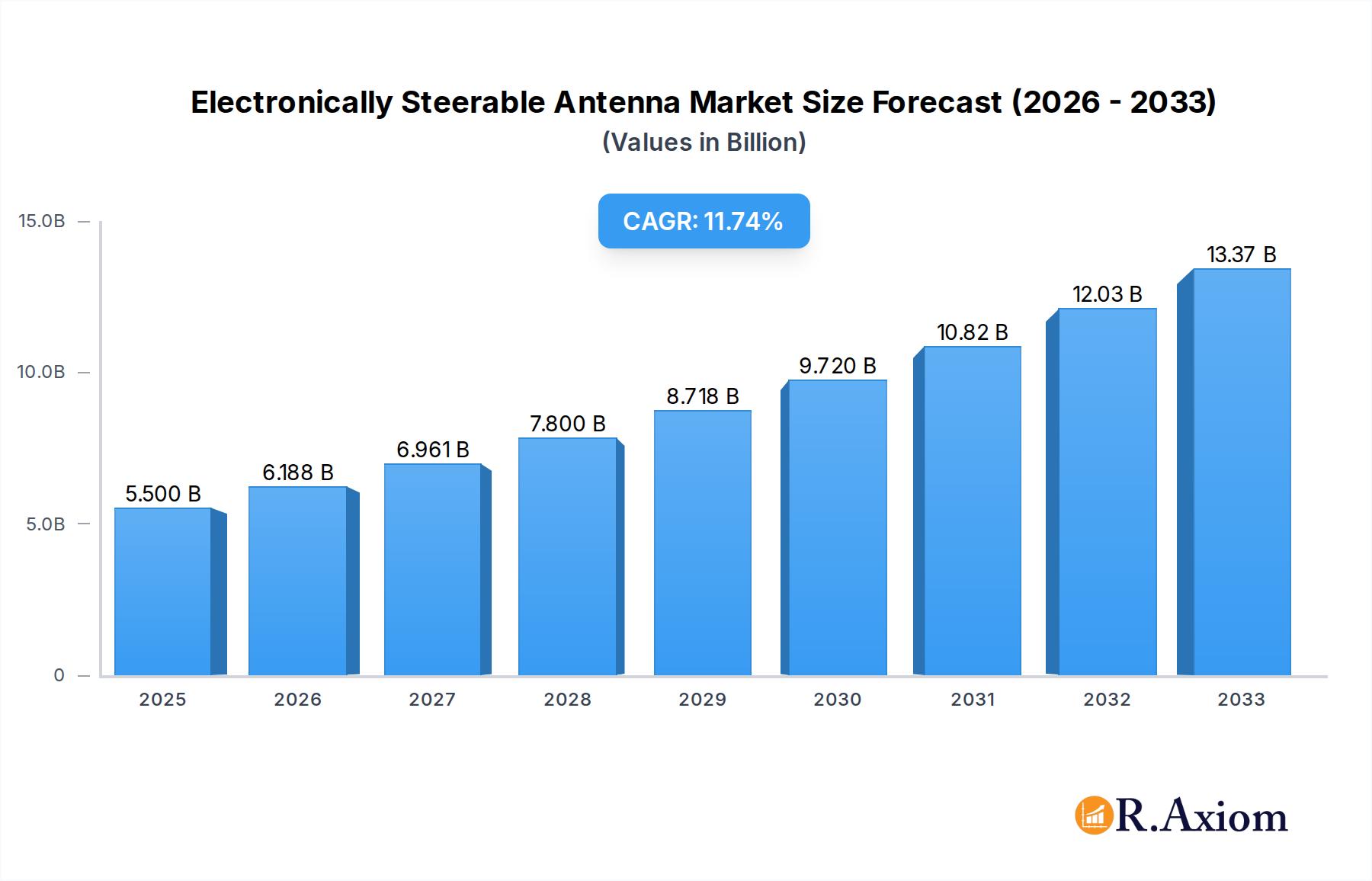

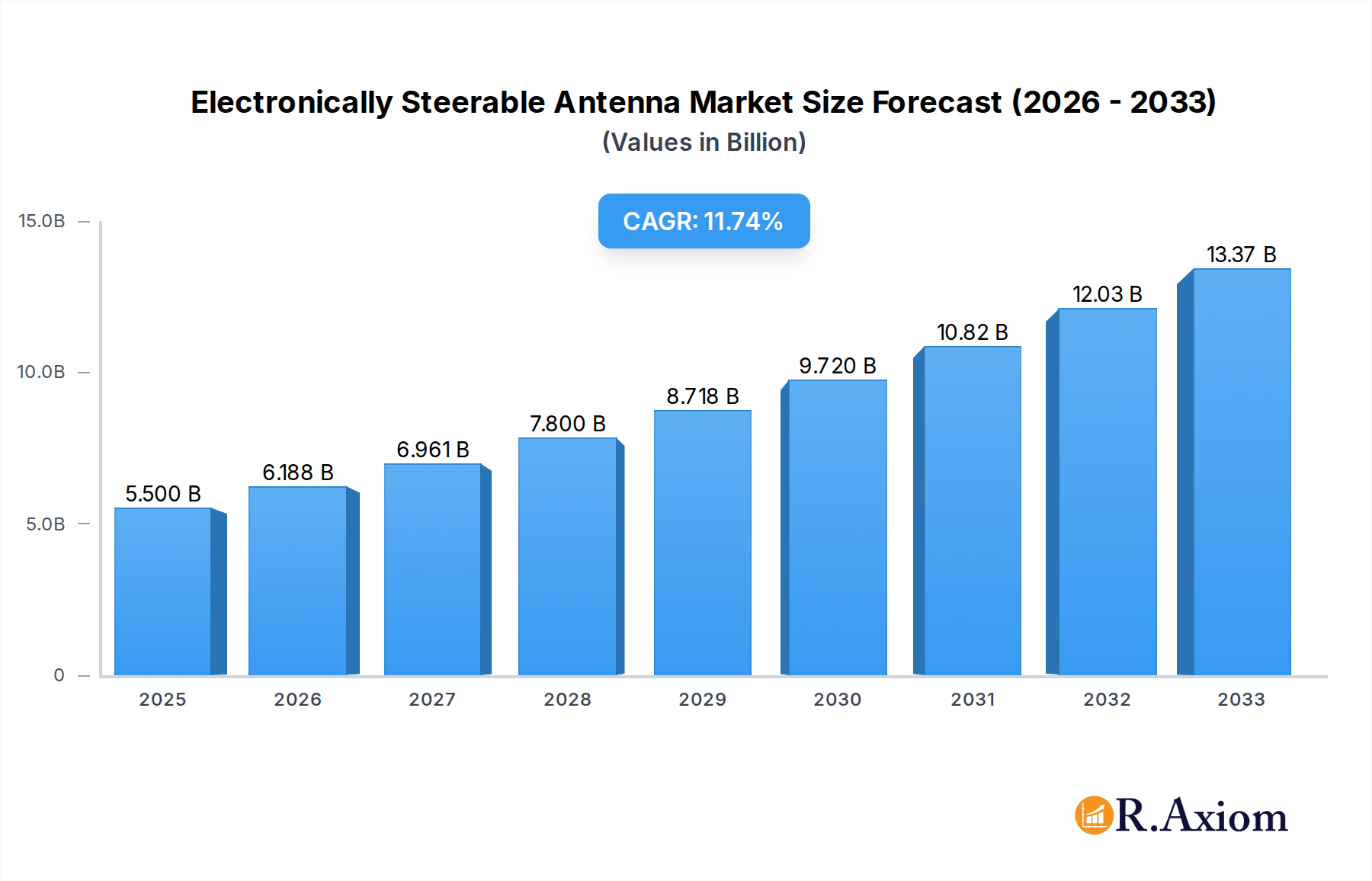

The Electronically Steerable Antenna (ESA) market is poised for significant expansion, projected to reach $5,500 million by 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 12.5% during the forecast period of 2025-2033. This surge is driven by critical advancements in satellite communications, where ESAs are becoming indispensable for high-throughput connectivity and rapid beam steering. The escalating demand for seamless global internet access, particularly in underserved regions, is a primary catalyst. Furthermore, the burgeoning aerospace and defense sectors are heavily investing in advanced radar systems and secure communication networks, both of which are key consumers of ESA technology. The proliferation of Low Earth Orbit (LEO) satellites, enabling faster data transmission and lower latency, further amplifies the need for agile and efficient antennas like those offered by ESA solutions.

Electronically Steerable Antenna Market Size (In Billion)

Key trends shaping this dynamic market include the increasing adoption of phased array antennas due to their superior performance and miniaturization capabilities, enabling integration into a wider range of platforms. The development of multi-beam antennas is also gaining traction, allowing for simultaneous communication with multiple satellites or ground stations, thereby enhancing spectral efficiency and network capacity. While the market is characterized by substantial growth, certain restraints such as the high initial cost of advanced ESA systems and the complexity of integration can pose challenges. However, continuous technological innovation and economies of scale are expected to mitigate these concerns over time. Emerging applications in the automotive sector, particularly for autonomous driving and vehicle-to-everything (V2X) communication, represent a nascent but promising area for ESA market penetration. Geographically, North America and Asia Pacific are expected to lead in market share, fueled by strong governmental investments in defense, telecommunications infrastructure upgrades, and the rapid expansion of satellite constellations.

Electronically Steerable Antenna Company Market Share

The Electronically Steerable Antenna (ESA) market exhibits a moderate level of concentration, with a mix of established aerospace and defense contractors, innovative startups, and specialized component manufacturers. Key players like Kymeta, ThinKom, and Hanwha Systems Co., Ltd. are actively investing in R&D, driving innovation in areas such as flat-panel ESAs, software-defined antennas, and multi-band capabilities. This innovation is fueled by the increasing demand for seamless connectivity in satellite communications and the growing adoption of advanced radar systems. Regulatory frameworks, particularly concerning spectrum allocation and export controls for advanced antenna technologies, play a significant role in shaping market dynamics. Product substitutes, such as traditional mechanically steered antennas, still hold a considerable market share but are gradually being displaced by the superior performance and agility of ESAs. End-user trends are heavily influenced by the need for robust, real-time data transmission in sectors like maritime, aviation, and defense. Mergers and acquisition (M&A) activities, with reported deal values in the tens of millions, are likely to increase as larger companies seek to acquire cutting-edge ESA technologies and expand their market reach. The market share of leading ESA providers is estimated to be in the range of 5% to 15%, with significant fragmentation in specialized application segments.

Electronically Steerable Antenna Industry Trends & Insights

The global Electronically Steerable Antenna (ESA) market is poised for substantial growth, driven by a confluence of technological advancements, evolving communication needs, and expanding application horizons. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 18-22% during the forecast period of 2025–2033, signifying a robust expansion trajectory. This growth is underpinned by several key market drivers. The burgeoning demand for high-bandwidth, always-on connectivity across various sectors, including satellite communications, wireless communications, and radar, is a primary catalyst. The proliferation of Low Earth Orbit (LEO) satellite constellations by companies like SpaceX and OneWeb is significantly boosting the adoption of ESAs, enabling faster and more reliable satellite internet services. Furthermore, the increasing sophistication of defense systems, requiring advanced radar capabilities for target tracking, surveillance, and electronic warfare, is another major growth engine.

Technological disruptions are at the forefront of this market evolution. The miniaturization and cost reduction of phased array antenna technology are making ESAs more accessible and economically viable for a broader range of applications. Advances in materials science, semiconductor technology, and antenna design are leading to lighter, more power-efficient, and higher-performance ESAs. Software-defined networking (SDN) and artificial intelligence (AI) are increasingly being integrated into ESA systems, enabling dynamic beamforming, intelligent interference mitigation, and adaptive signal processing, thereby enhancing overall system efficiency and flexibility.

Consumer preferences are shifting towards seamless and ubiquitous connectivity. In the enterprise sector, businesses are seeking reliable communication solutions for remote operations, fleet management, and IoT deployments. For consumers, the expectation of high-speed internet access, even in remote or mobile environments, is driving the demand for ESAs in applications such as in-flight connectivity and maritime broadband. The competitive dynamics within the ESA market are intensifying. While established players are leveraging their expertise and market presence, new entrants are challenging the status quo with disruptive technologies and innovative business models. Strategic partnerships and collaborations between antenna manufacturers, satellite operators, and system integrators are becoming crucial for market penetration and fostering ecosystem development. The market penetration of ESAs is expected to grow significantly, moving from niche applications to mainstream adoption in various communication and sensing domains. The estimated market size for ESAs is projected to reach several tens of billions of dollars by 2033, with substantial investment expected in research, development, and manufacturing capabilities.

Dominant Markets & Segments in Electronically Steerable Antenna

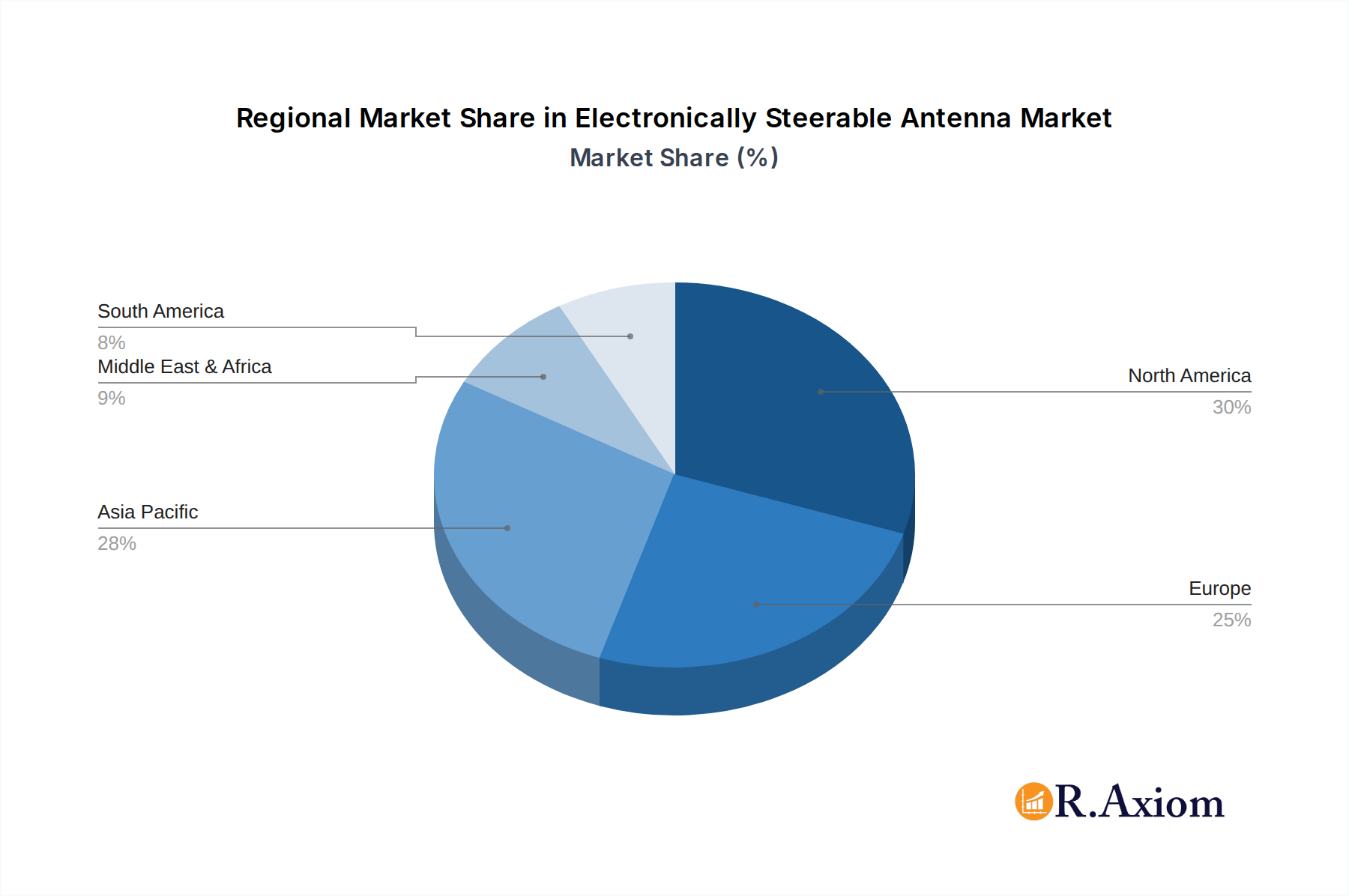

The Electronically Steerable Antenna (ESA) market is characterized by the dominance of specific regions and application segments, driven by strong economic policies, robust infrastructure development, and critical end-user demands.

Region/Country Dominance:

- North America (United States and Canada): This region stands out as a dominant market due to substantial government investment in defense and space programs, particularly in radar technology and satellite communications. The presence of major aerospace and defense contractors, coupled with a thriving startup ecosystem focused on innovative ESA solutions, further solidifies North America's leading position. Economic policies supporting technological advancement and high adoption rates of cutting-edge communication systems contribute significantly.

Application Dominance:

- Satellite Communications: This segment is the current leader and is projected to maintain its dominance throughout the forecast period.

- Key Drivers: The exponential growth of LEO satellite constellations for broadband internet (e.g., Starlink, OneWeb) requires agile and rapidly steerable antennas for continuous tracking. Maritime and aviation sectors are increasingly adopting satellite broadband for passenger and operational connectivity, necessitating flat-panel and low-profile ESAs. The expansion of global mobile satellite services (MSS) also fuels demand.

- Radar Communications: This segment is experiencing rapid growth and is expected to become a significant contributor to overall market expansion.

- Key Drivers: Modernization of defense systems, including airborne early warning and control (AEW&C) systems, ground-based surveillance, and electronic warfare, relies heavily on advanced phased array radar technology. The automotive industry's interest in radar for advanced driver-assistance systems (ADAS) and autonomous driving, while currently nascent for ESAs, represents a substantial future growth avenue.

- Wireless Communications: While not as dominant as satellite communications currently, this segment is poised for significant growth.

- Key Drivers: The deployment of 5G and future 6G networks will benefit from beamforming capabilities offered by ESAs for enhanced spectral efficiency and coverage in dense urban areas. Fixed wireless access (FWA) solutions utilizing ESAs for last-mile connectivity in underserved regions are also gaining traction.

Type Dominance:

- Phased Array Antenna: This type of ESA is currently the most prevalent and drives significant market demand.

- Key Drivers: The inherent advantages of electronic beam steering, rapid scanning, and multi-beam capabilities make phased array antennas ideal for both satellite tracking and advanced radar applications. Innovations in solid-state power amplifiers and digital beamforming are continuously improving their performance and reducing costs, making them a preferred choice across various applications.

- Multiple Beam Antenna: This is a sub-category of phased array antennas that offers specialized advantages.

- Key Drivers: The ability to simultaneously communicate with multiple satellites or ground stations is critical for high-throughput satellite systems and complex communication networks. This capability is crucial for efficient spectrum utilization and increased data throughput, making it a growing area of interest.

The economic policies in countries like the United States and its allies, prioritizing defense modernization and space exploration, coupled with significant private sector investments in satellite and wireless infrastructure, are the primary factors behind the dominance of North America and the aforementioned segments. The increasing deployment of satellite constellations and the ever-growing need for advanced radar capabilities are expected to sustain this dominance in the foreseeable future, with strong growth anticipated in emerging markets as well.

Electronically Steerable Antenna Product Developments

Recent product developments in the Electronically Steerable Antenna (ESA) market are characterized by a strong focus on enhanced performance, reduced form factors, and expanded frequency capabilities. Innovations include the introduction of ultra-low profile flat-panel ESAs designed for seamless integration into vehicles and aircraft, offering improved aerodynamic efficiency and reduced visual impact. Advanced phased array antennas are now incorporating digital beamforming technologies, enabling greater flexibility, adaptability, and intelligent signal processing. Furthermore, there's a growing trend towards multi-band and multi-orbit compatible ESAs, allowing users to seamlessly switch between different satellite constellations (LEO, MEO, GEO) and terrestrial wireless networks. These developments are driven by the increasing demand for ubiquitous, high-bandwidth connectivity in diverse environments, providing competitive advantages through superior agility, faster beam switching, and more efficient spectrum utilization.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the global Electronically Steerable Antenna (ESA) market, covering the period from 2019 to 2033, with a base year of 2025. The market is segmented based on Application, Type, and Region.

Application Segments:

- Satellite Communications: This segment encompasses applications such as broadband internet access, mobile satellite services, earth observation, and telecommunications. The market size is projected to reach an estimated $25,000 million by 2033, with a significant CAGR.

- Wireless Communications: This segment includes 5G/6G infrastructure, fixed wireless access, and enterprise connectivity solutions. Expected market size by 2033 is approximately $15,000 million, with robust growth driven by network densification.

- Radar Communications: This segment covers defense radar systems, automotive radar, weather radar, and air traffic control. Estimated market size by 2033 is around $20,000 million, fueled by defense modernization and autonomous vehicle development.

- Astronomical Study: This niche segment involves radio telescopes and other scientific instruments. While smaller in market size, estimated at $1,000 million by 2033, it showcases the diverse applications of ESA technology.

- Others: This includes emerging applications and specialized industrial uses, with an estimated market size of $5,000 million by 2033.

Type Segments:

- Phased Array Antenna: This dominant type is expected to hold the largest market share, driven by its inherent advantages. Projected market share is over 60% of the total ESA market.

- Multiple Beam Antenna: This segment, often a sub-category of phased array, focuses on simultaneous multi-target or multi-user communication. Estimated market share is around 25%.

- Others: This includes novel or less prevalent ESA designs. Estimated market share is approximately 15%.

Key Drivers of Electronically Steerable Antenna Growth

The growth of the Electronically Steerable Antenna (ESA) market is primarily propelled by several interconnected factors. Technologically, the advancement and cost reduction of phased array antenna technology, including innovations in digital beamforming and metamaterials, are making ESAs more competitive and accessible. Economically, the increasing demand for high-bandwidth, reliable connectivity across sectors like satellite communications (driven by LEO constellations), wireless communications (5G/6G expansion), and defense (advanced radar systems) provides a strong market pull. Regulatory frameworks, particularly concerning spectrum allocation for satellite services and defense applications, are also enabling wider adoption. Furthermore, the growing integration of AI and machine learning into ESA systems for optimized performance and adaptive capabilities is a significant growth catalyst.

Challenges in the Electronically Steerable Antenna Sector

Despite its promising growth trajectory, the Electronically Steerable Antenna (ESA) sector faces several challenges. Regulatory hurdles, particularly in obtaining spectrum licenses and navigating export controls for advanced defense-related technologies, can slow down market penetration. Supply chain issues, such as the availability of specialized components like Gallium Nitride (GaN) semiconductor devices and advanced electronic components, can lead to production delays and increased costs, potentially impacting market growth by an estimated 5-10%. Competitive pressures from established players and the high initial R&D and manufacturing costs associated with cutting-edge ESA development can also present significant barriers to entry for new companies. Furthermore, the need for specialized technical expertise for installation and maintenance can limit adoption in certain less developed markets.

Emerging Opportunities in Electronically Steerable Antenna

The Electronically Steerable Antenna (ESA) market is rife with emerging opportunities. The rapid expansion of Low Earth Orbit (LEO) satellite constellations presents a massive opportunity for ESAs in providing global broadband internet access. The burgeoning adoption of autonomous vehicles and advanced driver-assistance systems (ADAS) is creating a significant demand for automotive-grade ESAs for radar applications. The integration of ESAs into Internet of Things (IoT) devices for enhanced connectivity in remote or challenging environments is another promising avenue. Furthermore, the development of software-defined and AI-enabled ESAs offers opportunities for highly adaptable and intelligent communication and sensing solutions, opening doors for new applications in smart cities, industrial automation, and advanced surveillance.

Leading Players in the Electronically Steerable Antenna Market

- Fujikura

- ET Industries

- Kymeta

- ReliaSat

- Starwin

- ThinKom

- PPM Systems

- Vialite Communications

- Hanwha Systems Co., Ltd.

- Tracxn

Key Developments in Electronically Steerable Antenna Industry

- 2023/07: Kymeta announces a new generation of flat-panel antennas with enhanced performance for maritime and land-based connectivity.

- 2023/05: Hanwha Systems Co., Ltd. showcases advanced phased array antenna technology for next-generation military applications.

- 2022/11: ThinKom Solutions receives significant investment to scale production of its high-performance airborne ESAs.

- 2022/09: Starwin introduces compact and power-efficient ESAs for mobile satellite terminals.

- 2021/04: Vialite Communications highlights its breakthroughs in optical fiber integration for ESA systems, enabling longer reach and higher bandwidth.

- 2020/12: Fujikura demonstrates innovative materials for lighter and more durable ESA components.

- 2019/06: ET Industries announces a strategic partnership to develop advanced radar antenna systems.

Strategic Outlook for Electronically Steerable Antenna Market

The strategic outlook for the Electronically Steerable Antenna (ESA) market remains exceptionally positive, characterized by continuous innovation and expanding application frontiers. The sustained growth of satellite constellations and the increasing demand for high-speed connectivity in diverse environments will continue to be major growth catalysts. Strategic collaborations between ESA manufacturers, satellite operators, and end-users will be crucial for developing tailored solutions and accelerating market adoption. Investments in advanced manufacturing capabilities and R&D for next-generation technologies, such as artificial intelligence-driven beamforming and integrated multi-band/multi-orbit functionalities, will be key differentiators. Emerging markets and applications, particularly in the automotive and IoT sectors, represent significant untapped potential for future growth. The market is poised for sustained expansion, driven by its critical role in enabling the future of global communication and sensing.

Electronically Steerable Antenna Segmentation

-

1. Application

- 1.1. Satellite Communications

- 1.2. Wireless Communications

- 1.3. Radar Communications

- 1.4. Astronomical Study

- 1.5. Others

-

2. Type

- 2.1. Phased Array Antenna

- 2.2. Multiple Beam Antenna

- 2.3. Others

Electronically Steerable Antenna Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Electronically Steerable Antenna Regional Market Share

Geographic Coverage of Electronically Steerable Antenna

Electronically Steerable Antenna REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Electronically Steerable Antenna Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Satellite Communications

- 5.1.2. Wireless Communications

- 5.1.3. Radar Communications

- 5.1.4. Astronomical Study

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Phased Array Antenna

- 5.2.2. Multiple Beam Antenna

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Electronically Steerable Antenna Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Satellite Communications

- 6.1.2. Wireless Communications

- 6.1.3. Radar Communications

- 6.1.4. Astronomical Study

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Phased Array Antenna

- 6.2.2. Multiple Beam Antenna

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Electronically Steerable Antenna Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Satellite Communications

- 7.1.2. Wireless Communications

- 7.1.3. Radar Communications

- 7.1.4. Astronomical Study

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Phased Array Antenna

- 7.2.2. Multiple Beam Antenna

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Electronically Steerable Antenna Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Satellite Communications

- 8.1.2. Wireless Communications

- 8.1.3. Radar Communications

- 8.1.4. Astronomical Study

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Phased Array Antenna

- 8.2.2. Multiple Beam Antenna

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Electronically Steerable Antenna Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Satellite Communications

- 9.1.2. Wireless Communications

- 9.1.3. Radar Communications

- 9.1.4. Astronomical Study

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Phased Array Antenna

- 9.2.2. Multiple Beam Antenna

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Electronically Steerable Antenna Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Satellite Communications

- 10.1.2. Wireless Communications

- 10.1.3. Radar Communications

- 10.1.4. Astronomical Study

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Phased Array Antenna

- 10.2.2. Multiple Beam Antenna

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Fujikura

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 ET Industries

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Kymeta

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ReliaSat

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Starwin

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ThinKom

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 PPM Systems

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Vialite Communications

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hanwha Systems Co. Ltd.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tracxn

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Fujikura

List of Figures

- Figure 1: Global Electronically Steerable Antenna Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Electronically Steerable Antenna Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Electronically Steerable Antenna Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Electronically Steerable Antenna Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Electronically Steerable Antenna Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Electronically Steerable Antenna Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Electronically Steerable Antenna Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Electronically Steerable Antenna Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Electronically Steerable Antenna Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Electronically Steerable Antenna Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Electronically Steerable Antenna Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Electronically Steerable Antenna Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Electronically Steerable Antenna Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Electronically Steerable Antenna Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Electronically Steerable Antenna Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Electronically Steerable Antenna Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Electronically Steerable Antenna Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Electronically Steerable Antenna Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Electronically Steerable Antenna Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Electronically Steerable Antenna Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Electronically Steerable Antenna Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Electronically Steerable Antenna Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Electronically Steerable Antenna Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Electronically Steerable Antenna Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Electronically Steerable Antenna Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Electronically Steerable Antenna Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Electronically Steerable Antenna Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Electronically Steerable Antenna Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Electronically Steerable Antenna Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Electronically Steerable Antenna Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Electronically Steerable Antenna Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Electronically Steerable Antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Electronically Steerable Antenna Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Electronically Steerable Antenna Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Electronically Steerable Antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Electronically Steerable Antenna Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Electronically Steerable Antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Electronically Steerable Antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Electronically Steerable Antenna Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Electronically Steerable Antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Electronically Steerable Antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Electronically Steerable Antenna Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Electronically Steerable Antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Electronically Steerable Antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Electronically Steerable Antenna Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Electronically Steerable Antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Electronically Steerable Antenna Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Electronically Steerable Antenna Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Electronically Steerable Antenna Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Electronically Steerable Antenna Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronically Steerable Antenna?

The projected CAGR is approximately 12.5%.

2. Which companies are prominent players in the Electronically Steerable Antenna?

Key companies in the market include Fujikura, ET Industries, Kymeta, ReliaSat, Starwin, ThinKom, PPM Systems, Vialite Communications, Hanwha Systems Co., Ltd., Tracxn.

3. What are the main segments of the Electronically Steerable Antenna?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electronically Steerable Antenna," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electronically Steerable Antenna report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electronically Steerable Antenna?

To stay informed about further developments, trends, and reports in the Electronically Steerable Antenna, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence