Key Insights

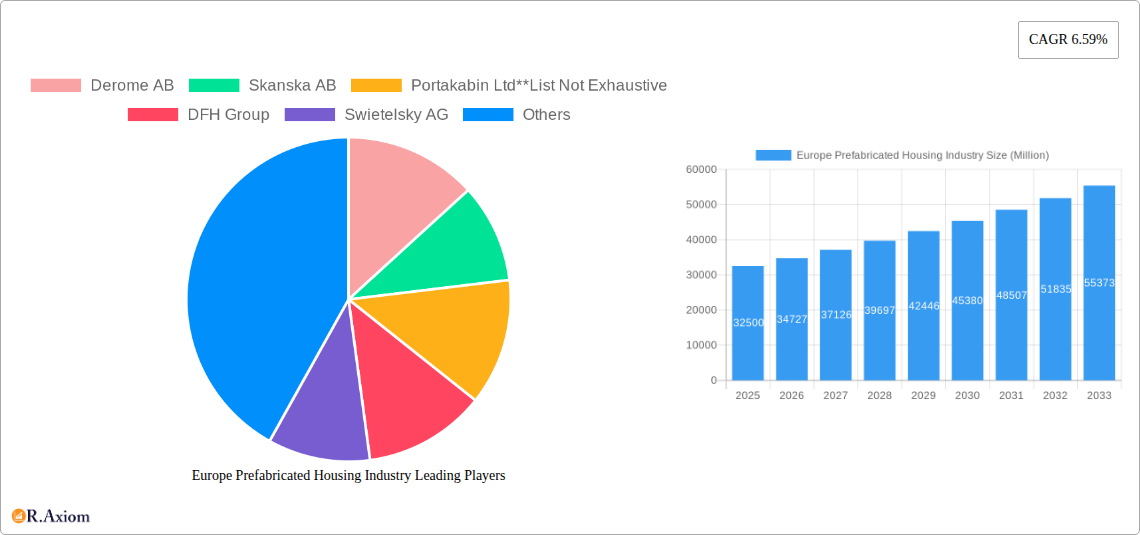

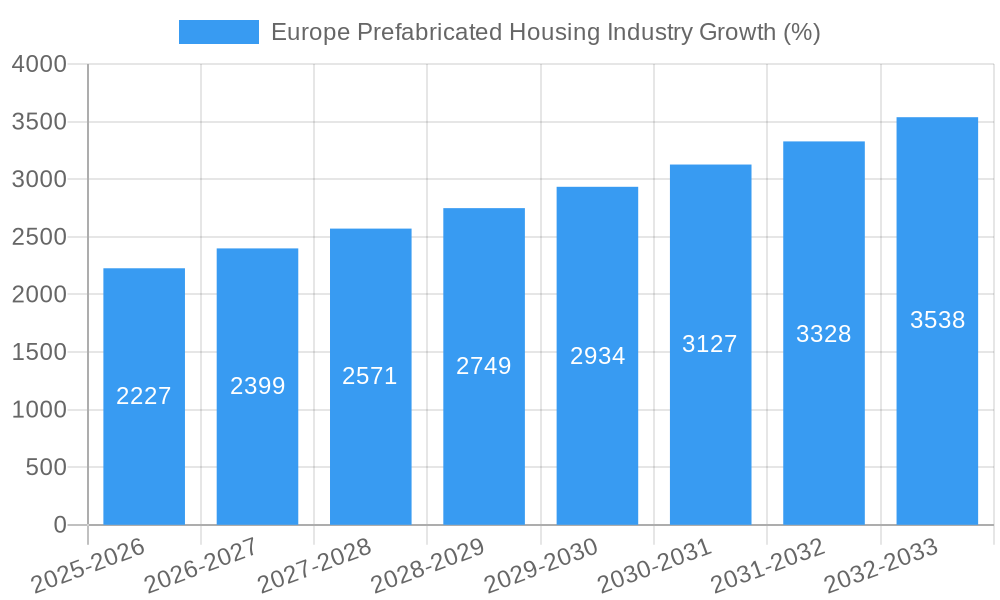

The European prefabricated housing market, valued at €32.5 billion in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 6.59% from 2025 to 2033. This expansion is driven by several key factors. Increasing urbanization and population density across major European nations like Germany, the UK, and France are creating a significant demand for efficient and cost-effective housing solutions. Prefabricated housing offers a faster construction timeline compared to traditional methods, addressing the urgent need for affordable housing in rapidly growing urban areas. Furthermore, stringent environmental regulations and a growing focus on sustainable construction practices are fueling the adoption of prefabricated buildings, known for their reduced environmental impact and optimized resource utilization. The market segmentation reveals a strong preference for single-family units, although multi-family projects are also gaining traction, particularly in densely populated urban centers. Leading companies like Derome AB, Skanska AB, and Portakabin Ltd are driving innovation and expanding their market share through technological advancements and strategic partnerships. However, challenges remain, including overcoming potential consumer perceptions regarding the quality and aesthetics of prefabricated homes, and navigating complex building codes and regulations across diverse European markets.

The growth trajectory of the European prefabricated housing market is expected to remain positive throughout the forecast period. Factors such as government initiatives promoting sustainable housing and technological advancements in prefabrication techniques will contribute to this growth. Germany, the UK, and France are anticipated to remain the largest markets within Europe, owing to their high population density and robust construction sectors. However, other countries within the region are also showing increasing interest in adopting prefabricated housing, potentially leading to a more geographically diverse market in the coming years. The continued expansion of the industry will likely involve further consolidation among market players, increased investment in research and development, and a heightened focus on integrating smart home technology and sustainable building materials to cater to evolving consumer preferences.

Europe Prefabricated Housing Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the European prefabricated housing industry, encompassing market size, segmentation, key players, growth drivers, challenges, and future opportunities. The study period covers 2019-2033, with 2025 as the base and estimated year. The forecast period spans 2025-2033, while the historical period analyzed is 2019-2024. This report is crucial for industry stakeholders, investors, and anyone seeking to understand this rapidly evolving sector.

Europe Prefabricated Housing Industry Market Concentration & Innovation

The European prefabricated housing market exhibits a moderately concentrated landscape, with several large players holding significant market share. While precise market share figures for individual companies are proprietary, leading players such as Skanska AB, Derome AB, and Portakabin Ltd contribute substantially to the overall market volume. Smaller, specialized firms cater to niche segments, creating a diverse yet competitive ecosystem. Innovation is driven by several factors including:

- Technological advancements: 3D printing, automation, and the adoption of sustainable building materials are reshaping the industry.

- Government regulations: Stringent environmental standards and building codes are prompting manufacturers to adopt more eco-friendly construction methods.

- Consumer preferences: Increasing demand for energy-efficient, affordable, and customizable housing is fueling innovation.

- M&A Activity: Consolidation through mergers and acquisitions (M&A) is likely to increase, driven by companies seeking to expand their market reach and technological capabilities. While precise M&A deal values are not publicly available for all transactions in this sector, we estimate the total value of such deals in the past five years to be around xx Million.

Product substitutes include traditional construction methods, however, the prefabricated housing sector offers advantages in terms of speed, cost-efficiency, and quality control, making it a competitive alternative. End-user trends point towards a growing preference for sustainable and customizable housing solutions, impacting product development and market segmentation.

Europe Prefabricated Housing Industry Industry Trends & Insights

The European prefabricated housing market is experiencing robust growth, driven by several factors. The industry’s Compound Annual Growth Rate (CAGR) during the historical period (2019-2024) is estimated at xx%, and is projected to reach xx% during the forecast period (2025-2033). Key drivers include:

- Rising housing demand: Population growth and urbanization are increasing the need for affordable housing across Europe.

- Shorter construction times: Prefabrication significantly reduces construction time compared to traditional methods, leading to faster project completion.

- Cost-effectiveness: Prefabricated housing can be more cost-effective than traditional construction, especially for large-scale projects.

- Improved energy efficiency: Modern prefabricated homes often incorporate energy-efficient features, reducing operating costs for homeowners.

- Technological advancements: Innovations in materials, design, and manufacturing processes are constantly improving the quality and appeal of prefabricated homes.

Market penetration of prefabricated housing varies across European countries, with higher adoption rates observed in countries with robust regulatory frameworks and supportive government policies. Competitive dynamics are shaped by the interplay between established players and new entrants, with a growing emphasis on innovation and sustainability.

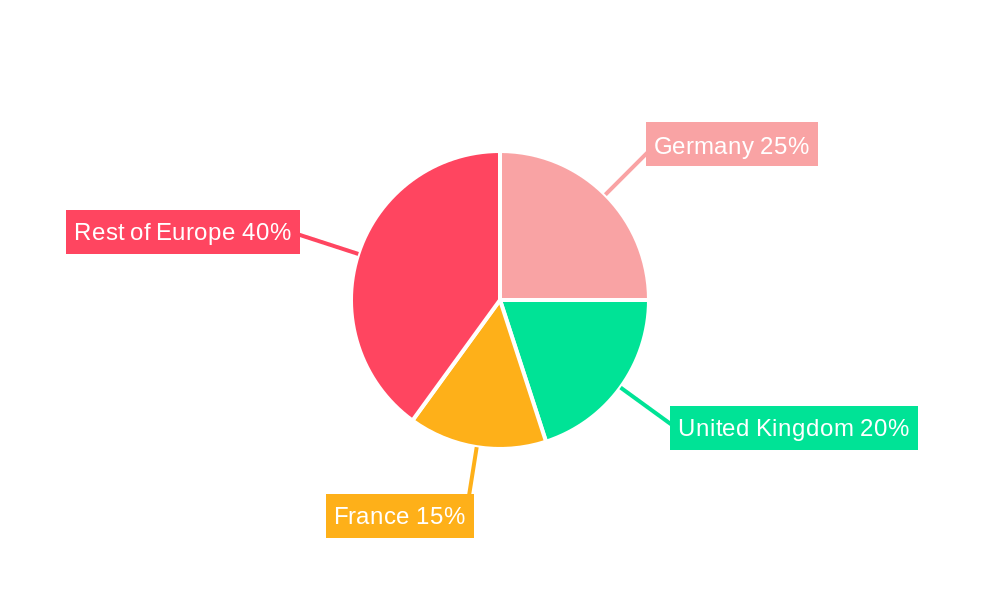

Dominant Markets & Segments in Europe Prefabricated Housing Industry

The German, United Kingdom, and French markets represent the largest segments within the European prefabricated housing industry. Germany's substantial housing shortage and supportive government initiatives make it a dominant market. The UK benefits from a strong construction sector and substantial investments in infrastructure projects. France, while showing considerable growth, lags slightly behind Germany and the UK due to xx. The "Rest of Europe" segment encompasses countries with varying levels of market maturity and growth potential.

Key Drivers by Country:

- Germany: Government targets for new housing construction (400,000 units annually), supportive regulatory frameworks, and strong industrial infrastructure.

- United Kingdom: High housing demand, robust construction sector, and investment in infrastructure projects.

- France: Growing awareness of the benefits of prefabrication, ongoing urbanization, and government initiatives promoting sustainable construction.

- Rest of Europe: Varied growth rates depending on individual country's economic conditions, housing policies, and market maturity.

By Type:

The multi-family segment is currently showing faster growth than the single-family segment, driven by the need for affordable high-density housing solutions in urban areas. However, the single-family segment continues to hold significant market share, driven by an increase in demand for suburban properties.

Europe Prefabricated Housing Industry Product Developments

The European prefabricated housing industry is witnessing significant product innovation, with manufacturers introducing energy-efficient designs, smart home integrations, and customizable options. Technological advancements in materials science, 3D printing, and robotics are transforming the manufacturing process, improving both speed and quality of construction. The focus is shifting towards sustainable and eco-friendly construction materials, leading to improved environmental performance and reduced carbon footprints. Modular designs and off-site construction techniques contribute to shortened construction timelines, reducing project costs and risks.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the European prefabricated housing market, segmented by type (single-family and multi-family) and geography (Germany, United Kingdom, France, and Rest of Europe). Growth projections vary by segment, reflecting differences in market dynamics and demand. Germany’s market is expected to experience the highest growth due to government policies, while the UK market will show consistent growth due to high housing demand and robust construction activity. The single-family segment is projected to demonstrate steady growth driven by consumer preference, while multi-family housing is estimated to exhibit higher growth potential due to the increase in urbanization. Competitive dynamics differ across each segment and geographical area, reflecting variations in market maturity, concentration, and technological adoption. Market sizes for each segment are provided in the full report with precise values estimated in Millions.

Key Drivers of Europe Prefabricated Housing Industry Growth

Several factors are fueling the growth of the European prefabricated housing industry. These include: increasing urbanization and population growth driving demand for affordable housing; government initiatives promoting sustainable and efficient construction; cost-effectiveness and speed advantages of prefabrication over traditional methods; and technological advancements like 3D printing, automation, and modular design enhancing efficiency and quality. Favorable economic conditions in many European countries further support the industry's expansion.

Challenges in the Europe Prefabricated Housing Industry Sector

Despite the growth prospects, the industry faces several challenges. These include: regulatory hurdles and obtaining necessary approvals; supply chain disruptions and material cost fluctuations; skills gaps in the workforce impacting productivity; competition from established construction companies; and consumer perceptions regarding the quality and aesthetic appeal of prefabricated housing. These challenges can impact overall project timelines and profitability, necessitating proactive strategies for mitigation.

Emerging Opportunities in Europe Prefabricated Housing Industry

Significant opportunities exist in expanding prefabricated housing into underserved markets, developing innovative sustainable materials and design solutions, integrating smart technologies, and capitalizing on government incentives for green building. The growing demand for customizable and affordable housing solutions offers significant potential, especially in urban areas. Further investments in technology and talent development will be critical to achieving sustained growth.

Leading Players in the Europe Prefabricated Housing Industry Market

- Derome AB

- Skanska AB

- Portakabin Ltd

- DFH Group

- Swietelsky AG

- Bouygues Batiment International

- Wolf Holding GmbH

- Peab AB

- Containex

- Laing O'Rourke

Key Developments in Europe Prefabricated Housing Industry Industry

- January 2023: TopHat launched Europe's largest modular housing site in the UK, a 650,000 sq. ft plant capable of producing a home per hour, creating 1,000 new jobs. This significantly increases production capacity and emphasizes the UK's commitment to sustainable construction.

- March 2023: HAUBNER GROUP and SEMODU AG announced plans to build Europe's most advanced modular housing production facility in Germany, aligning with the government's goal of 400,000 new units annually. This signals a major technological advancement in the sector and strengthens Germany's position as a leader in prefabricated housing.

Strategic Outlook for Europe Prefabricated Housing Industry Market

The European prefabricated housing market is poised for continued expansion, driven by strong demand, technological innovation, and supportive government policies. The industry's focus on sustainability, affordability, and speed of construction will attract further investment and drive market growth. Addressing challenges related to supply chains, skills shortages, and consumer perceptions will be crucial for realizing the industry's full potential. Companies investing in automation, sustainable materials, and innovative designs are well-positioned to capitalize on emerging opportunities and achieve significant market share growth in the coming years.

Europe Prefabricated Housing Industry Segmentation

-

1. Type

- 1.1. Single-family

- 1.2. Multi-family

Europe Prefabricated Housing Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Prefabricated Housing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.59% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Huge Demand for Prefabricated Housing Driving the Market; Huge Demand for Multi-family Houses Driving Market Growth

- 3.3. Market Restrains

- 3.3.1. Lack of Awareness of Prefabricated Market; Lack of Standardization and Regulation in the Prefabricated Buildings Industry

- 3.4. Market Trends

- 3.4.1. Huge Demand for Multi-family Houses Driving Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Single-family

- 5.1.2. Multi-family

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Prefabricated Housing Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Derome AB

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Skanska AB

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Portakabin Ltd**List Not Exhaustive

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 DFH Group

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Swietelsky AG

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Bouygues Batiment International

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Wolf Holding GmbH

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Peab AB

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Containex

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Laing O'Rourke

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Derome AB

List of Figures

- Figure 1: Europe Prefabricated Housing Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Prefabricated Housing Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Prefabricated Housing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Prefabricated Housing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Europe Prefabricated Housing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Europe Prefabricated Housing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Germany Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: France Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Italy Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: United Kingdom Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Netherlands Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Sweden Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Rest of Europe Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Europe Prefabricated Housing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 13: Europe Prefabricated Housing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: United Kingdom Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Germany Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: France Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Italy Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Spain Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Netherlands Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Belgium Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Sweden Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Norway Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Poland Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Denmark Europe Prefabricated Housing Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Prefabricated Housing Industry?

The projected CAGR is approximately 6.59%.

2. Which companies are prominent players in the Europe Prefabricated Housing Industry?

Key companies in the market include Derome AB, Skanska AB, Portakabin Ltd**List Not Exhaustive, DFH Group, Swietelsky AG, Bouygues Batiment International, Wolf Holding GmbH, Peab AB, Containex, Laing O'Rourke.

3. What are the main segments of the Europe Prefabricated Housing Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.5 Million as of 2022.

5. What are some drivers contributing to market growth?

Huge Demand for Prefabricated Housing Driving the Market; Huge Demand for Multi-family Houses Driving Market Growth.

6. What are the notable trends driving market growth?

Huge Demand for Multi-family Houses Driving Market Growth.

7. Are there any restraints impacting market growth?

Lack of Awareness of Prefabricated Market; Lack of Standardization and Regulation in the Prefabricated Buildings Industry.

8. Can you provide examples of recent developments in the market?

March 2023: HAUBNER GROUP and SEMODU AG proposed constructing Europe's most advanced production facility for modular housing to meet the German government's target of constructing 400,000 units annually. HAUBNER GROUP's current production facility in Neumarkt in der Oberpfalz will construct a production facility with a maximum floor area of 40,000 sq. m. A production line for modules focused on the manufacturing procedures used in the automotive industry will be constructed at this location. It aims to establish a technological foundation for the next industrialization stage of home development.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Prefabricated Housing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Prefabricated Housing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Prefabricated Housing Industry?

To stay informed about further developments, trends, and reports in the Europe Prefabricated Housing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence