Key Insights

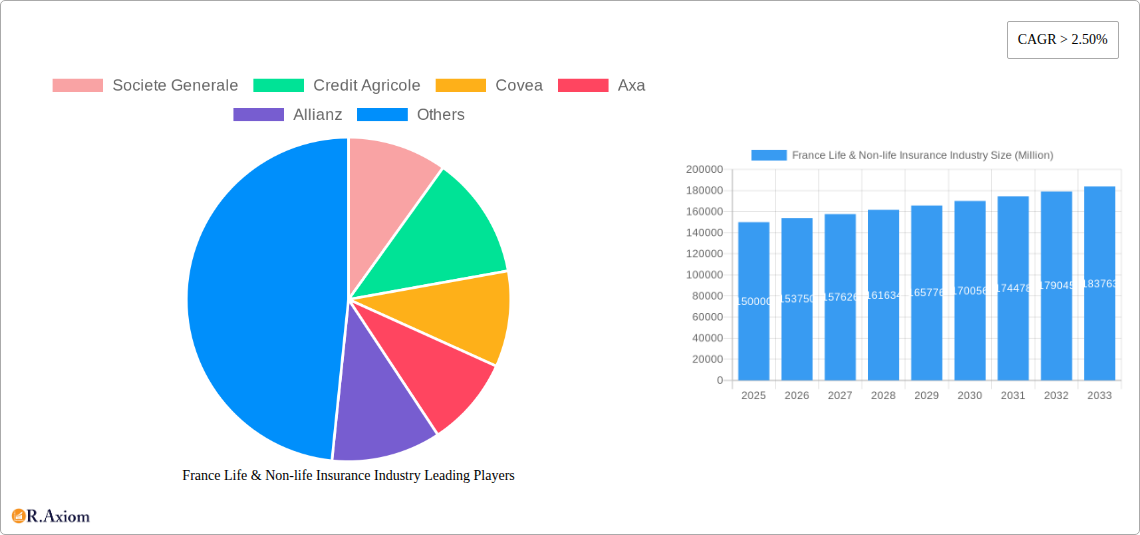

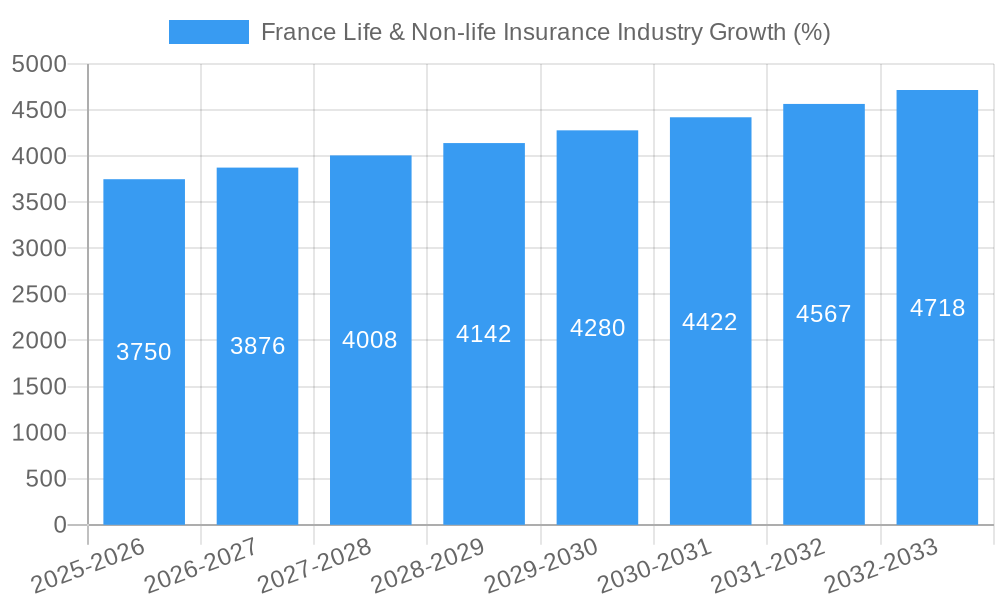

The French Life & Non-life Insurance market, valued at approximately €150 billion in 2025, exhibits robust growth potential, projected to expand at a compound annual growth rate (CAGR) exceeding 2.5% from 2025 to 2033. This growth is fueled by several key factors. Increasing awareness of the importance of financial security and risk mitigation, especially amongst a growing middle class, drives demand for both life and non-life insurance products. Furthermore, favorable government policies supporting the insurance sector and the ongoing digital transformation of the industry, with increased adoption of online platforms and InsurTech solutions, contribute to market expansion. Competition within the market remains intense, with established players like Société Générale, Crédit Agricole, and AXA vying for market share alongside smaller, more agile insurers. However, potential regulatory changes and economic fluctuations present challenges to sustained growth. The market is segmented by product type (life, health, auto, home, etc.), distribution channels (online, agents, brokers), and geographical regions within France. Specific regional data would require further research.

The forecast period of 2025-2033 indicates continued expansion, driven by factors such as a rising aging population necessitating increased life insurance coverage and evolving consumer preferences for customized insurance solutions. The dominance of established players suggests a potential need for innovation and differentiation to capture market share. Maintaining profitability amidst competitive pressures and evolving consumer demands requires insurers to adapt to these trends with technological innovation and diversified product offerings. This will likely lead to a higher concentration among leading players and more mergers and acquisitions activity.

France Life & Non-life Insurance Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the France Life & Non-life Insurance industry, covering market dynamics, competitive landscape, and future growth prospects from 2019 to 2033. The study period spans the historical period (2019-2024), the base year (2025), and the forecast period (2025-2033), offering a complete picture of this crucial sector. This report is essential for insurers, investors, and stakeholders seeking actionable insights into this dynamic market.

France Life & Non-life Insurance Industry Market Concentration & Innovation

The French life and non-life insurance market exhibits a high degree of concentration, with a few major players dominating the landscape. Key players such as AXA, Allianz, Societe Generale, Credit Agricole, and Covea collectively hold a significant market share (estimated at xx%), leaving smaller players to compete for the remaining portion. The market share of individual companies fluctuates annually based on product innovation, mergers & acquisitions (M&A), and regulatory changes. Recent M&A activity has been moderate, with deal values totaling approximately xx Million in 2024. Innovation is primarily driven by technological advancements, including digitalization and data analytics, used to improve customer experience, streamline operations, and develop innovative insurance products. The regulatory framework, while relatively stable, continues to evolve, impacting product offerings and operational procedures. Consumer trends towards personalized and digital-first services present both opportunities and challenges for established players.

- Key Players: AXA, Allianz, Societe Generale, Credit Agricole, Covea, La banque postale, MACIF, Credit mutuel, MAIF, ACM, Caisse D'Epargne, Groupama (List Not Exhaustive)

- Market Concentration: High (estimated xx% held by top 5 players in 2024)

- M&A Deal Value (2024): xx Million

- Innovation Drivers: Digitalization, Data Analytics, Personalized Services

France Life & Non-life Insurance Industry Industry Trends & Insights

The French life and non-life insurance market is experiencing steady growth, driven by factors such as increasing penetration rates, particularly in non-life insurance, and a growing awareness of insurance needs. The market's compound annual growth rate (CAGR) during the forecast period (2025-2033) is projected to be xx%. Technological disruption is transforming the industry, with Insurtech startups challenging established players. Consumer preferences are shifting toward digital channels, personalized products, and value-for-money offerings. The competitive dynamics are characterized by both intense competition among established players and the emergence of new entrants, increasing pressure on pricing and margins. Market penetration is highest in urban areas, with rural areas lagging behind. Further growth will depend on effective regulatory changes promoting competition and fostering innovation within this space.

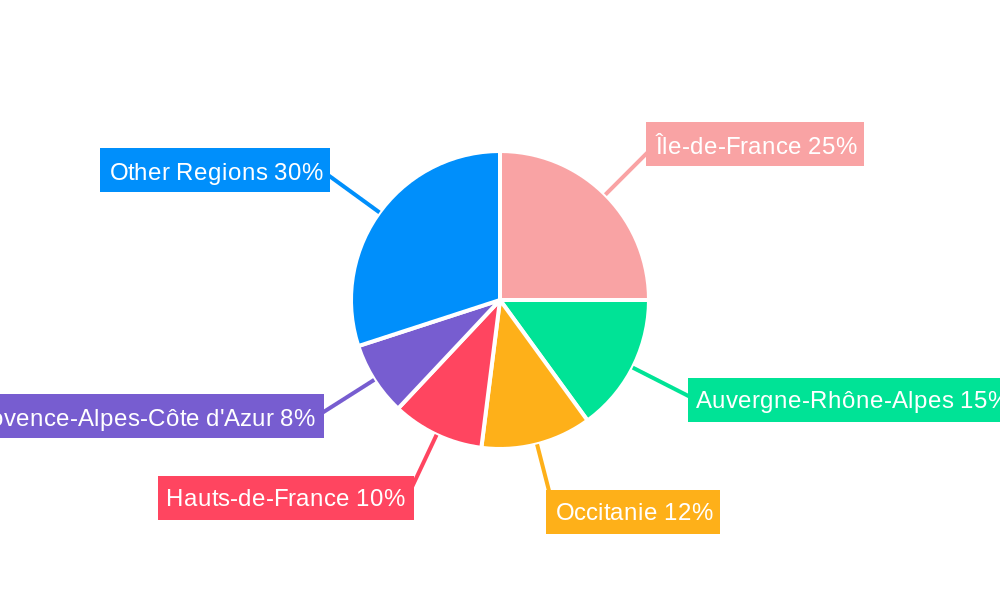

Dominant Markets & Segments in France Life & Non-life Insurance Industry

The French life and non-life insurance market is largely dominated by the urban areas of Paris and its surrounding regions, accounting for approximately xx% of the total market. This dominance is fueled by higher incomes, greater awareness of insurance products, and better access to digital channels in these regions. Other major metropolitan areas also contribute significantly to market size.

- Key Drivers of Dominance:

- Higher disposable incomes

- Increased awareness of insurance benefits

- Superior infrastructure and access to technology

- Dense population leading to higher demand

This dominance is further reinforced by the strong presence of major insurance companies and their established distribution networks within these regions. However, expanding into rural areas presents a significant opportunity for growth in the upcoming decade.

France Life & Non-life Insurance Industry Product Developments

Recent product innovations focus on digital distribution channels, personalized products, and bundled services that cater to specific customer needs. The emphasis on user-friendly interfaces and streamlined processes continues to be a key driver of new product development. Telematics and usage-based insurance models are gaining traction in the non-life sector, leveraging data analytics to personalize premiums and improve risk assessment. These products offer a competitive advantage by allowing insurers to provide more accurate and tailored coverage, better matching customer needs.

Report Scope & Segmentation Analysis

The report segments the France Life & Non-life Insurance market based on product type (life insurance, non-life insurance), distribution channel (online, offline), and customer demographics (age, income). The life insurance segment is projected to grow at a CAGR of xx% during 2025-2033, driven by increased demand for retirement savings and health insurance plans. The non-life insurance segment is expected to grow at a CAGR of xx% due to factors like rising vehicle ownership and increased awareness of property and casualty insurance. Market size for both segments is expected to exceed xx Million by 2033. The competitive dynamics vary across segments, with some areas experiencing more intense competition than others.

Key Drivers of France Life & Non-life Insurance Industry Growth

Several factors are driving growth in the French Life & Non-life insurance industry. Technological advancements, particularly in digital platforms and data analytics, are improving efficiency and customer experiences. Economic stability and rising disposable incomes are increasing insurance penetration. Favorable regulatory frameworks encouraging competition and innovation are creating a more dynamic environment. The expansion of digital channels and the growth of e-commerce are further fueling the industry’s growth.

Challenges in the France Life & Non-life Insurance Industry Sector

The industry faces significant challenges, including increasing regulatory scrutiny, the need to adapt to evolving customer expectations, and fierce competition from both established players and Insurtech startups. Furthermore, low interest rates impact investment returns for life insurers and fraudulent claims represent a significant operational burden. These factors can collectively impact profitability and long-term sustainability, resulting in a need for adaptability and innovation.

Emerging Opportunities in France Life & Non-life Insurance Industry

The sector presents several significant opportunities for growth. The expansion of Insurtech and fintech solutions offers opportunities for enhanced customer service and operational efficiency. The growing demand for specialized insurance products, such as cyber insurance and travel insurance, creates niche markets for insurers to explore. The increasing penetration of mobile devices and the adoption of digital insurance platforms create a potential for reaching new customer segments and improving customer retention.

Leading Players in the France Life & Non-life Insurance Industry Market

- Societe Generale

- Credit Agricole

- Covea

- Axa

- Allianz

- La banque postale

- MACIF

- Credit mutuel

- MAIF

- ACM

- Caisse D'Epargne

- Groupama

Key Developments in France Life & Non-life Insurance Industry Industry

- December 6, 2021: Allianz Partners and Uber partnered to provide insurance for independent drivers and couriers in France and other European countries.

- June 15, 2022: Berkshire Hathaway Specialty Insurance launched a Directors and Officers Liability policy insurance in France.

Strategic Outlook for France Life & Non-life Insurance Industry Market

The French life and non-life insurance market is poised for continued growth, driven by evolving customer needs and technological innovation. Insurers who effectively leverage digital technologies, adapt to changing consumer preferences, and navigate the regulatory landscape will be best positioned to capture market share and achieve sustainable growth. The focus on personalized products, efficient operational models, and customer-centric service will be crucial in this dynamic environment.

France Life & Non-life Insurance Industry Segmentation

-

1. Insurance type

-

1.1. Life Insurance

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non-Life Insurance

- 1.2.1. Home

- 1.2.2. Motor

- 1.2.3. Health

- 1.2.4. Rest of Non-Life Insurance

-

1.1. Life Insurance

-

2. Channel of Distribution

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Online

- 2.5. Other distribution channels

France Life & Non-life Insurance Industry Segmentation By Geography

- 1. France

France Life & Non-life Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 2.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Significant Growth Contributed by the Non-Life Insurance Sector

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. France Life & Non-life Insurance Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 5.1.1. Life Insurance

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non-Life Insurance

- 5.1.2.1. Home

- 5.1.2.2. Motor

- 5.1.2.3. Health

- 5.1.2.4. Rest of Non-Life Insurance

- 5.1.1. Life Insurance

- 5.2. Market Analysis, Insights and Forecast - by Channel of Distribution

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Online

- 5.2.5. Other distribution channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. France

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Societe Generale

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Credit Agricole

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Covea

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Axa

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Allianz

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 La banque postale

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 MACIF

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Credit mutuel

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 MAIF

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 ACM

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Caisse D'Epargne

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Groupama**List Not Exhaustive

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 Societe Generale

List of Figures

- Figure 1: France Life & Non-life Insurance Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: France Life & Non-life Insurance Industry Share (%) by Company 2024

List of Tables

- Table 1: France Life & Non-life Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: France Life & Non-life Insurance Industry Revenue Million Forecast, by Insurance type 2019 & 2032

- Table 3: France Life & Non-life Insurance Industry Revenue Million Forecast, by Channel of Distribution 2019 & 2032

- Table 4: France Life & Non-life Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: France Life & Non-life Insurance Industry Revenue Million Forecast, by Insurance type 2019 & 2032

- Table 6: France Life & Non-life Insurance Industry Revenue Million Forecast, by Channel of Distribution 2019 & 2032

- Table 7: France Life & Non-life Insurance Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Life & Non-life Insurance Industry?

The projected CAGR is approximately > 2.50%.

2. Which companies are prominent players in the France Life & Non-life Insurance Industry?

Key companies in the market include Societe Generale, Credit Agricole, Covea, Axa, Allianz, La banque postale, MACIF, Credit mutuel, MAIF, ACM, Caisse D'Epargne, Groupama**List Not Exhaustive.

3. What are the main segments of the France Life & Non-life Insurance Industry?

The market segments include Insurance type, Channel of Distribution.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Significant Growth Contributed by the Non-Life Insurance Sector.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

On June 15, 2022, Berkshire Hathaway Specialty Insurance launched a Directors and Officers Liability policy insurance in France to serve local and multinational companies. This new coverage enhances BHSI's ability to provide multinational programs and services to companies with exposure in France and throughout the company's global network, which spans 170 countries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Life & Non-life Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Life & Non-life Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Life & Non-life Insurance Industry?

To stay informed about further developments, trends, and reports in the France Life & Non-life Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence