Key Insights

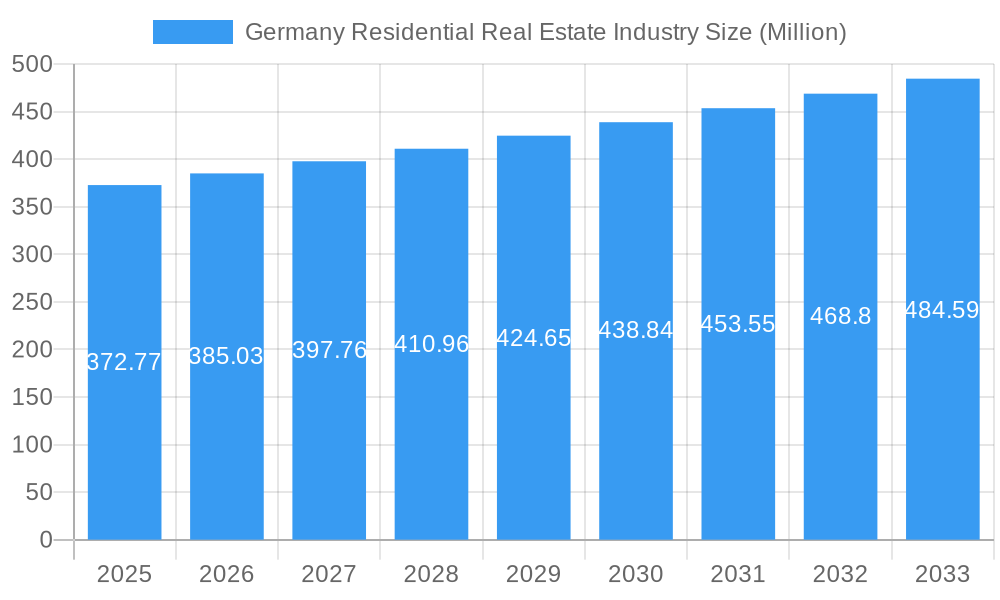

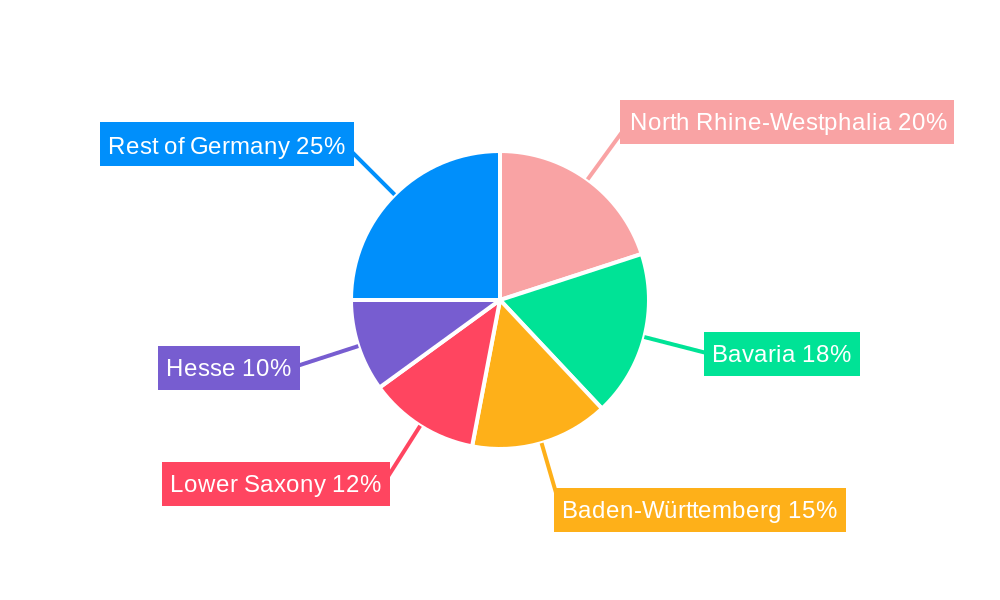

The German residential real estate market, valued at €372.77 million in 2025, exhibits robust growth potential, projected to expand at a Compound Annual Growth Rate (CAGR) exceeding 3.06% from 2025 to 2033. This growth is fueled by several key drivers. A consistently strong economy and increasing urbanization, particularly in major cities like Berlin, Munich, and Hamburg, contribute significantly to heightened demand. Furthermore, favorable government policies aimed at supporting homeownership and infrastructure development further stimulate market activity. While rising construction costs and interest rates pose some challenges, the overall positive economic outlook and persistent population growth are expected to outweigh these restraints. The market is segmented by property type (villas/landed houses and condominiums/apartments) and key cities, reflecting varying price points and demand dynamics across different geographic locations. Major players such as Vonovia SE, Deutsche Wohnen SE, and LEG Immobilien SE, along with numerous smaller regional players, shape the competitive landscape. The regions of North Rhine-Westphalia, Bavaria, Baden-Württemberg, Lower Saxony, and Hesse represent significant concentrations of market activity.

Germany Residential Real Estate Industry Market Size (In Million)

The forecast period (2025-2033) anticipates continued growth, although the pace may fluctuate slightly due to macroeconomic factors. The consistent demand, particularly in major metropolitan areas, suggests a resilient market. However, developers and investors should closely monitor interest rate fluctuations and regulatory changes that could impact market sentiment and investment decisions. Understanding the diverse segmentations – by both property type and geographic location – is crucial for strategic positioning within this dynamic market. Future growth will likely be influenced by the government's success in addressing affordability concerns and sustaining economic stability.

Germany Residential Real Estate Industry Company Market Share

Germany Residential Real Estate Industry: 2019-2033 Market Report

This comprehensive report provides an in-depth analysis of the German residential real estate industry from 2019 to 2033, offering invaluable insights for investors, developers, and industry stakeholders. The study covers market concentration, key trends, dominant segments, product developments, and future growth opportunities, encompassing a detailed examination of major players and emerging challenges. The report utilizes data from the historical period (2019-2024), the base year (2025), and projects the market's trajectory through the forecast period (2025-2033). All financial values are expressed in millions.

Germany Residential Real Estate Industry Market Concentration & Innovation

The German residential real estate market presents a dynamic landscape shaped by a blend of large, publicly listed corporations and smaller, regionally focused players. This section delves into the competitive dynamics, exploring market concentration, innovation drivers, regulatory influences, and significant industry activities. Leading players like Vonovia SE and Deutsche Wohnen SE command substantial market share, influencing overall market trends. However, smaller entities, including Wohnungsbaugenossenschaft Musikwinkel eG (WBG) and SAGA Siedlungs-Aktiengesellschaft Hamburg, maintain a significant presence, often specializing in niche markets or specific geographic areas. This diverse structure creates a complex interplay of forces driving market evolution.

- Market Concentration: While precise figures require constant updating, the top five players held an estimated X% of the market in 2025, suggesting a moderately concentrated market. This concentration is projected to evolve to Y% by 2033, driven by ongoing mergers and acquisitions (M&A) activity and potential market shifts. Further analysis of market share distribution across different property types (e.g., single-family homes vs. multi-family units) and geographic regions will provide a more granular understanding.

- Innovation Drivers: Technological advancements are profoundly impacting the sector. Smart home integration, the incorporation of sustainable building materials (e.g., timber construction, green roofs), and the adoption of energy-efficient technologies (e.g., heat pumps, solar panels) are key innovation drivers. Government initiatives focused on energy efficiency, affordable housing, and sustainable urban development significantly influence market direction and incentivize innovation. PropTech solutions, including digital platforms for property management, marketing, and financing, are transforming traditional business models.

- Regulatory Framework: Germany's stringent building codes and environmental regulations directly influence construction costs and timelines, impacting project feasibility and profitability. Rental control measures in select cities affect rental yields and investor sentiment, creating regional variations in market dynamics. Upcoming legislation and policy changes must be continually monitored for their potential impacts.

- Product Substitutes: The primary substitute for homeownership remains renting, with the choice largely determined by factors such as affordability, economic conditions, and individual lifestyle preferences. This competition influences pricing strategies and the overall demand for various property types.

- End-User Trends: Consumer preferences are increasingly focused on sustainable and energy-efficient housing, modern amenities, and convenient locations. Demand for flexible living spaces and multi-generational housing options is also growing, requiring developers to adapt their offerings to meet evolving needs. Understanding demographic shifts and changing lifestyle preferences is crucial for effective market forecasting.

- M&A Activities: The German residential real estate sector has witnessed considerable M&A activity in recent years, with deal values totaling approximately €Z Million in 2024. This consolidation trend is anticipated to continue, although potentially at a moderated pace due to macroeconomic factors and tighter financial conditions. Analyzing the types of M&A deals (e.g., horizontal vs. vertical integration) and their implications for market concentration will be essential for understanding future market structure.

Germany Residential Real Estate Industry Industry Trends & Insights

The German residential real estate market is experiencing robust growth, driven by factors such as urbanization, population growth, and increasing disposable incomes. However, challenges like rising construction costs, regulatory hurdles, and limited land availability are tempering growth. Technological disruptions, such as the adoption of PropTech solutions and innovative construction techniques, are impacting market dynamics. Consumer preferences are shifting toward sustainable, energy-efficient, and technologically advanced housing, requiring developers to adapt their offerings. Competitive dynamics are marked by consolidation, with larger companies acquiring smaller players to expand their market share.

The market is projected to experience a CAGR of xx% during the forecast period (2025-2033), reaching a market volume of €xx Million by 2033. Market penetration of green building technologies is expected to increase from xx% in 2025 to xx% by 2033.

Dominant Markets & Segments in Germany Residential Real Estate Industry

Berlin, Munich, Hamburg, and Cologne represent the most dominant markets, attracting significant investment and exhibiting higher property values and rental yields compared to the rest of Germany. The condominium and apartment segment constitutes the largest share of the market, owing to higher population density and demand in urban areas.

By Key Cities:

- Berlin: Strong population growth, robust employment market, and limited housing supply contribute to high demand.

- Munich: High demand driven by economic strength, a large influx of highly skilled workers, and a limited housing stock.

- Hamburg: Port city with strong economic activity and a growing population, resulting in steady demand for residential property.

- Cologne: Significant population and economic growth, coupled with limited housing supply, driving market activity.

- Rest of Germany: More fragmented market with varying levels of demand and growth rates across different regions.

By Type:

- Condominiums and Apartments: The dominant segment due to high population density in major cities and the preference for urban living. This segment benefits from greater accessibility to infrastructure and amenities.

- Villas and Landed Houses: A smaller but growing segment, particularly in suburban areas. Demand is driven by changing lifestyles and the desire for more space and privacy.

Germany Residential Real Estate Industry Product Developments

Recent product innovations focus on sustainable building practices, smart home technologies, and improved energy efficiency. Developers are increasingly incorporating features such as solar panels, heat pumps, and smart home automation systems to meet evolving consumer preferences. These innovations offer competitive advantages by attracting environmentally conscious buyers and enhancing property value. The market is witnessing a trend towards modular and prefabricated construction, offering cost-effectiveness and faster construction times.

Report Scope & Segmentation Analysis

This report segments the German residential real estate market by key cities (Berlin, Hamburg, Cologne, Munich, and Rest of Germany) and property type (villas and landed houses, condominiums and apartments). Each segment is analyzed in terms of market size, growth projections, and competitive dynamics.

By Key Cities: The report projects significant growth in all major cities, with Berlin and Munich leading the way due to high population growth and economic activity. The Rest of Germany segment shows steady growth, though at a slower pace.

By Type: The condominiums and apartments segment is expected to dominate the market throughout the forecast period, driven by urbanization and population growth in major cities. The villas and landed houses segment is projected to experience growth, though at a slower rate than the apartments and condominiums segment.

Key Drivers of Germany Residential Real Estate Industry Growth

Several factors fuel growth in the German residential real estate sector. These include:

- Strong economic growth: A thriving economy increases disposable incomes, bolstering demand for housing.

- Population growth and urbanization: Continued population growth and urbanization in major cities drive demand for residential properties.

- Government initiatives: Government incentives for affordable housing and sustainable building practices support market expansion.

- Technological advancements: Innovations in construction technology and smart home solutions enhance efficiency and appeal.

Challenges in the Germany Residential Real Estate Industry Sector

The German residential real estate market faces several challenges:

- High construction costs: Rising material and labor costs increase the price of new housing, potentially impacting affordability.

- Regulatory hurdles: Complex permitting processes and environmental regulations can slow down development projects.

- Limited land availability: The scarcity of land, particularly in urban areas, restricts the supply of new housing.

- Competition: Intense competition among developers and investors impacts profitability.

Emerging Opportunities in Germany Residential Real Estate Industry

Despite challenges, opportunities exist:

- Sustainable housing: Growing demand for eco-friendly homes presents significant opportunities for developers embracing green building technologies.

- Smart home integration: Integrating smart home features enhances property value and attracts tech-savvy buyers.

- Affordable housing: Government initiatives to address affordable housing shortages create opportunities for developers catering to this market segment.

Leading Players in the Germany Residential Real Estate Industry Market

- Deutsche Wohnen SE

- Wohnungsbaugenossenschaft Musikwinkel eG (WBG)

- Consus Real Estate

- Vonovia SE

- Residia Care Holding GmbH & Co

- SAGA Siedlungs-Aktiengesellschaft Hamburg

- Vivawest

- ABG Frankfurt Holding

- 6 3 Other Companies

- Degewo

- LEG Immobilien SE

Key Developments in Germany Residential Real Estate Industry Industry

- 2022 Q4: Vonovia SE and Deutsche Wohnen SE merger completed, creating one of Europe's largest residential real estate companies.

- 2023 Q1: Consus Real Estate launched a new line of sustainable apartments in Berlin.

- 2024 Q2: Government introduced new incentives for energy-efficient renovations of existing housing stock. (Further developments can be added here as they occur)

Strategic Outlook for Germany Residential Real Estate Industry Market

The German residential real estate market is poised for continued growth, driven by long-term factors such as population growth, urbanization, and economic strength. Opportunities lie in adopting sustainable building practices, integrating smart home technologies, and addressing the growing demand for affordable housing. While challenges such as construction costs and regulatory hurdles persist, the market's fundamental strength and evolving consumer preferences suggest a positive outlook for the years to come. Focusing on innovation, sustainability, and catering to diverse market needs will be crucial for success in this dynamic sector.

Germany Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Villas and Landed Houses

- 1.2. Condominiums and Apartments

-

2. Key Cities

- 2.1. Berlin

- 2.2. Hamburg

- 2.3. Cologne

- 2.4. Munich

- 2.5. Rest of Germany

Germany Residential Real Estate Industry Segmentation By Geography

- 1. Germany

Germany Residential Real Estate Industry Regional Market Share

Geographic Coverage of Germany Residential Real Estate Industry

Germany Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 3.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Strong Demand and Rising Construction Activities to Drive the Market; Rising House Prices in Germany Affecting Demand in the Market

- 3.3. Market Restrains

- 3.3.1. Weak economic environment

- 3.4. Market Trends

- 3.4.1. Strong Demand And Rising Construction Activities To Drive The Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Germany Residential Real Estate Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Villas and Landed Houses

- 5.1.2. Condominiums and Apartments

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Berlin

- 5.2.2. Hamburg

- 5.2.3. Cologne

- 5.2.4. Munich

- 5.2.5. Rest of Germany

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Deutsche Wohnen SE

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Wohnungsbaugenossenschaft Musikwinkel eG (WBG)

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Consus Real Estate

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Vonovia SE

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Residia Care Holding GmbH & Co

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 SAGA Siedlungs-Aktiengesellschaft Hamburg

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Vivawest

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 ABG Frankfurt Holding**List Not Exhaustive 6 3 Other Companie

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Degewo

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 LEG Immobilien SE

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Deutsche Wohnen SE

List of Figures

- Figure 1: Germany Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Germany Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Germany Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Germany Residential Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Germany Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Germany Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Germany Residential Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Residential Real Estate Industry?

The projected CAGR is approximately > 3.06%.

2. Which companies are prominent players in the Germany Residential Real Estate Industry?

Key companies in the market include Deutsche Wohnen SE, Wohnungsbaugenossenschaft Musikwinkel eG (WBG), Consus Real Estate, Vonovia SE, Residia Care Holding GmbH & Co, SAGA Siedlungs-Aktiengesellschaft Hamburg, Vivawest, ABG Frankfurt Holding**List Not Exhaustive 6 3 Other Companie, Degewo, LEG Immobilien SE.

3. What are the main segments of the Germany Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 372.77 Million as of 2022.

5. What are some drivers contributing to market growth?

Strong Demand and Rising Construction Activities to Drive the Market; Rising House Prices in Germany Affecting Demand in the Market.

6. What are the notable trends driving market growth?

Strong Demand And Rising Construction Activities To Drive The Market.

7. Are there any restraints impacting market growth?

Weak economic environment.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Germany Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence