Key Insights

The Japan Property & Casualty (P&C) insurance market exhibits robust growth, driven by factors such as increasing urbanization, rising awareness of insurance, and a growing middle class with higher disposable incomes. The market's compound annual growth rate (CAGR) exceeding 4.00% suggests a consistently expanding demand for property and casualty insurance products. Key drivers include government initiatives promoting insurance penetration, the escalating frequency and severity of natural disasters (like earthquakes and typhoons) necessitating comprehensive coverage, and the expanding e-commerce sector demanding robust cybersecurity and liability insurance. Significant trends include the digitalization of insurance processes, with increasing adoption of online platforms and telematics for streamlined services and risk assessment. Furthermore, the industry is seeing a shift towards customized and niche insurance products catering to the diverse needs of the Japanese population. Competitive pressures from both established players like Tokio Marine & Nichido Fire Insurance and Sompo Holdings, and newer, digitally-native insurers like Rakuten General Insurance, are fostering innovation and efficiency within the sector. While regulatory hurdles and economic uncertainties present some restraints, the overall outlook for the Japan P&C insurance market remains positive, with considerable potential for further growth in the forecast period (2025-2033).

The market segmentation, while not explicitly detailed, likely includes various categories like motor insurance, homeowners insurance, commercial property insurance, and liability insurance. The competitive landscape is characterized by a mix of large, established insurers and smaller, more specialized companies. Regional variations in risk profiles and insurance penetration rates across Japan are expected, influencing the distribution of market share. The Base year of 2025 indicates a mature market with established players and a reasonably predictable growth trajectory, further supported by the available data suggesting a stable and expanding sector. While precise market size figures aren't provided, considering a CAGR of over 4% and a study period from 2019 to 2033, coupled with the presence of numerous significant players, a substantial market size in the billions of dollars (USD) is a logical inference.

This comprehensive report provides an in-depth analysis of the Japan Property & Casualty Insurance industry, covering the period 2019-2033. It offers crucial insights into market dynamics, competitive landscapes, and future growth prospects, equipping stakeholders with actionable intelligence for strategic decision-making. The report leverages extensive data analysis, encompassing historical performance (2019-2024), a base year of 2025, and forecasts extending to 2033.

Japan Property & Casualty Insurance Industry Market Concentration & Innovation

This section analyzes the market concentration, innovation drivers, regulatory landscape, product substitutes, end-user trends, and mergers & acquisitions (M&A) activity within the Japanese property & casualty insurance sector.

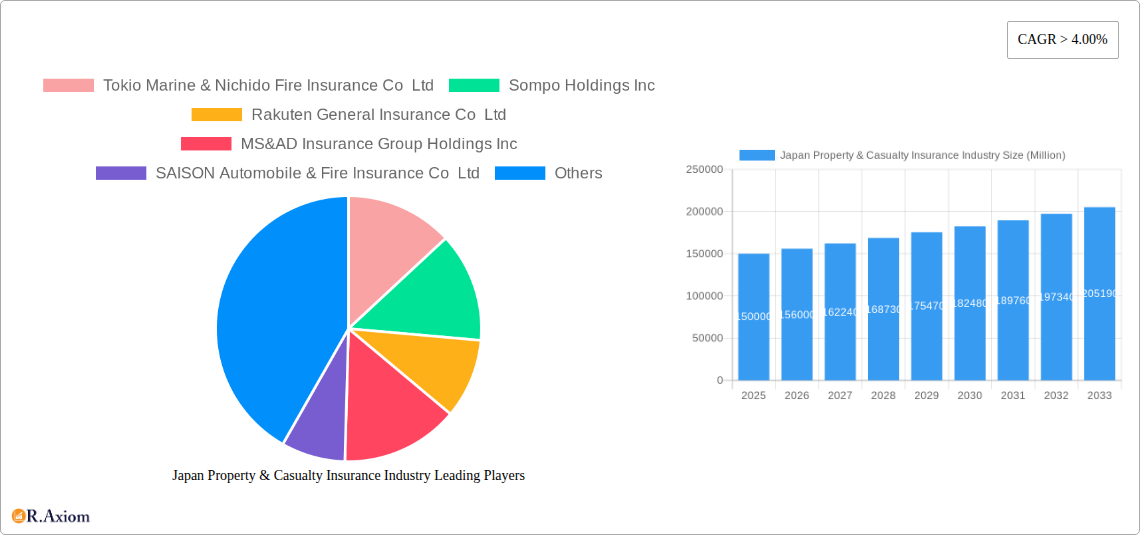

The Japanese property and casualty insurance market exhibits a high degree of concentration, with a few major players commanding significant market share. Tokio Marine & Nichido Fire Insurance Co Ltd, Sompo Holdings Inc, and MS&AD Insurance Group Holdings Inc are among the leading companies, collectively holding an estimated xx% market share in 2024. Smaller players, such as Rakuten General Insurance Co Ltd and others, compete primarily through niche offerings and specialized services.

Market Concentration Metrics (2024):

- Top 3 Players Market Share: xx%

- Top 5 Players Market Share: xx%

- Herfindahl-Hirschman Index (HHI): xx

Innovation Drivers:

- Technological advancements, particularly in data analytics and AI, are driving product innovation and process optimization.

- Growing demand for customized insurance solutions is pushing insurers to develop tailored products and services.

- Regulatory changes focused on consumer protection and market transparency are stimulating innovation in risk management and product design.

M&A Activity:

The Japanese P&C insurance sector has witnessed a moderate level of M&A activity in recent years. Deal values have ranged from xx Million to xx Million, primarily driven by consolidation efforts and expansion into new market segments. The overall deal volume has remained relatively stable, with an average of xx deals per year during the historical period.

Japan Property & Casualty Insurance Industry Industry Trends & Insights

This section delves into the key trends and insights shaping the Japanese property & casualty insurance market, encompassing market growth drivers, technological disruptions, evolving consumer preferences, and competitive dynamics.

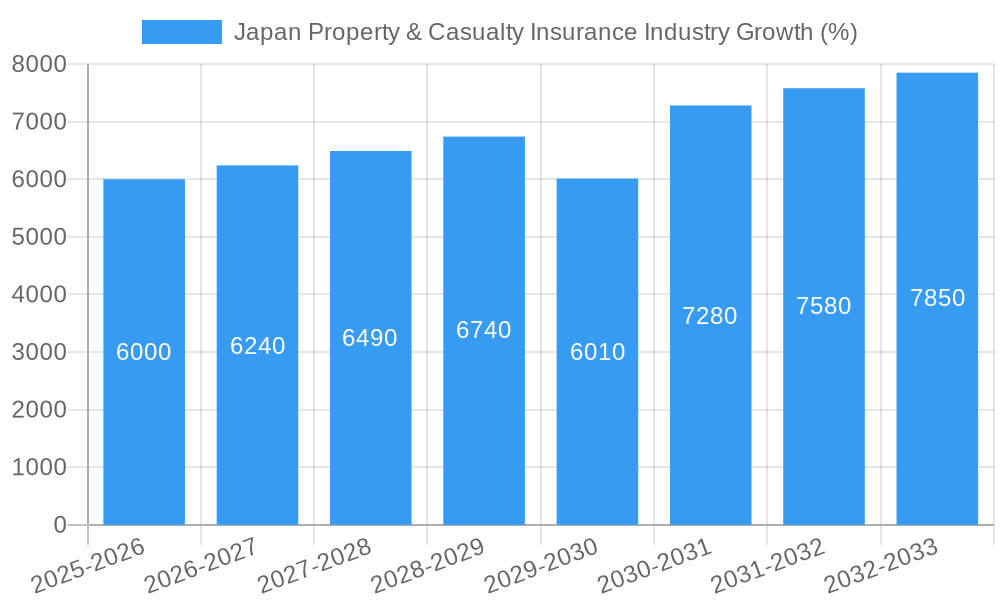

The Japanese P&C insurance market is projected to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is primarily driven by factors such as:

- Rising disposable incomes: Increased purchasing power among Japanese consumers is fueling demand for insurance products.

- Growing awareness of risk: Heightened awareness of various risks, including natural disasters and cyber threats, is driving greater insurance penetration.

- Government initiatives: Government regulations and policies promoting insurance coverage are positively influencing market growth.

- Technological advancements: The integration of Insurtech is streamlining operations, enhancing customer experience, and opening up new revenue streams.

Market penetration, measured by the percentage of the population with insurance coverage, is expected to reach xx% by 2033, compared to xx% in 2024. Increased competition is driving down premiums in some segments, while innovation is creating new, higher-margin offerings. Consumer preferences are shifting towards digital platforms and personalized insurance solutions.

Dominant Markets & Segments in Japan Property & Casualty Insurance Industry

This section highlights the leading segments within the Japanese property and casualty insurance market. The analysis focuses on key drivers of growth and competitive dynamics within each segment.

Dominant Segment: Motor Insurance

- Key Drivers: High vehicle ownership rates, stringent government regulations regarding mandatory insurance, and a growing middle class.

- Dominance Analysis: Motor insurance constitutes the largest segment of the Japanese P&C insurance market, accounting for an estimated xx% of total premiums in 2024. Intense competition among insurers drives pricing pressure and innovation in product offerings.

Other Significant Segments:

- Property Insurance: This segment is experiencing steady growth driven by rising property values and increased awareness of potential risks like natural disasters.

- Liability Insurance: Demand for liability insurance is increasing, driven by factors such as greater legal awareness and a rise in litigation.

- Health Insurance (Supplementary): While not strictly P&C, complementary health insurance is a substantial market, largely driven by an aging population and increasing medical expenses.

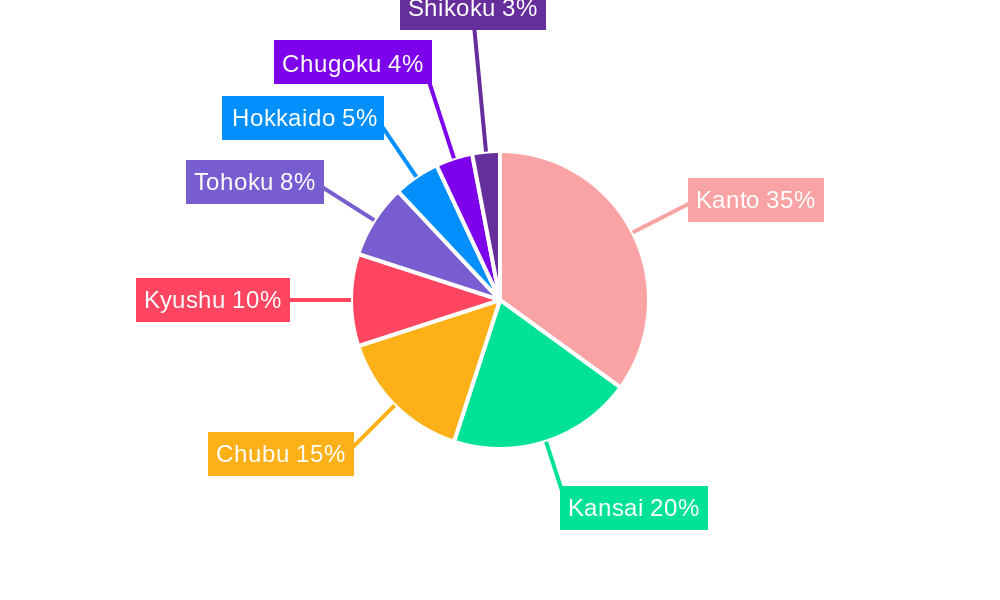

Regional Variations: Urban centers generally exhibit higher insurance penetration rates compared to rural areas.

Japan Property & Casualty Insurance Industry Product Developments

The Japanese P&C insurance industry is witnessing significant product innovations driven by technological advancements. Insurers are leveraging data analytics and AI to develop more accurate risk assessment models, personalize insurance products, and optimize pricing strategies. Telematics-based insurance, which utilizes data from connected devices to assess driving behavior, is gaining traction. The market is also seeing the rise of digital distribution channels and customized insurance solutions tailored to specific customer needs. These innovations are enhancing competitiveness and improving market fit by offering more personalized and efficient insurance products.

Report Scope & Segmentation Analysis

This report segments the Japan Property & Casualty Insurance market based on product type (Motor, Property, Liability, Others), distribution channel (Online, Offline, Bancassurance), and customer type (Individual, Corporate). Each segment's market size, growth projections, and competitive landscape are analyzed, providing a comprehensive overview of the market structure and dynamics. For example, the motor insurance segment is expected to show a CAGR of xx% over the forecast period due to increasing vehicle ownership, whereas the online distribution channel is predicted to have a xx% CAGR driven by digital adoption. The competitive landscape varies by segment, with some segments being more concentrated than others.

Key Drivers of Japan Property & Casualty Insurance Industry Growth

Several factors fuel growth in the Japanese property and casualty insurance sector. These include an increasing middle class driving higher demand for insurance products, an aging population leading to increased healthcare needs and associated insurance purchases, stringent government regulations mandating insurance coverage for certain sectors, and technological advancements allowing for innovative product offerings and enhanced customer experiences. The continued modernization of infrastructure and the nation’s focus on risk mitigation further stimulate market expansion.

Challenges in the Japan Property & Casualty Insurance Industry Sector

The Japanese P&C insurance industry faces challenges including increasing competition, particularly from new entrants utilizing innovative digital models, stringent regulatory requirements impacting profitability, and potential natural disasters impacting claims costs. These factors pose significant pressure on insurers to manage expenses, maintain profitability, and adapt to dynamic market conditions. Furthermore, the low interest rate environment complicates investment strategies for insurers. The cost of managing cyber risks also represents a growing concern.

Emerging Opportunities in Japan Property & Casualty Insurance Industry

The Japanese P&C insurance market offers several emerging opportunities. The increasing adoption of telematics offers new avenues for risk assessment and personalized pricing. Expanding into niche markets catering to specific customer segments, such as high-net-worth individuals, can yield significant growth. Leveraging advanced analytics and AI for fraud detection and risk management can improve operational efficiency and profitability. Finally, tapping into the growing demand for tailored, personalized insurance solutions that address the unique risk profiles of individual customers will unlock significant opportunities.

Leading Players in the Japan Property & Casualty Insurance Industry Market

- Tokio Marine & Nichido Fire Insurance Co Ltd

- Sompo Holdings Inc

- Rakuten General Insurance Co Ltd

- MS&AD Insurance Group Holdings Inc

- SAISON Automobile & Fire Insurance Co Ltd

- SECOM General Insurance Co Ltd

- Hitachi Capital Insurance Corporation

- Nisshin Fire & Marine Insurance Co Ltd

- Kyoei Fire & Marine Insurance Co Ltd

- Mitsui Direct General Insurance Co Ltd

List Not Exhaustive

Key Developments in Japan Property & Casualty Insurance Industry Industry

- July 2021: Sompo International Holdings Ltd launched the Sompo Women in Insurance Management (SWIM) program, aiming to develop future female leaders.

- July 2021: Sompo International Holdings Ltd expanded its Commercial Property & Casualty segment with the formation of Sompo Global Risk Solutions (GRS) Asia-Pacific in Singapore.

Strategic Outlook for Japan Property & Casualty Insurance Industry Market

The Japanese property and casualty insurance market presents a compelling long-term growth outlook. Continued economic growth, increasing risk awareness, technological advancements, and evolving consumer preferences will create a favorable environment for market expansion. Insurers who effectively adapt to changing market conditions, leverage technological innovations, and offer personalized products are well-positioned to capitalize on the substantial growth opportunities ahead. The focus on digitalization and data-driven insights will further shape the competitive landscape.

Japan Property & Casualty Insurance Industry Segmentation

-

1. Insurance Type

- 1.1. Property

- 1.2. Auto

- 1.3. Other Insurance Types

-

2. Distribution Channel

- 2.1. Direct

- 2.2. Agents

- 2.3. Banks

- 2.4. Other Distribution Channels

Japan Property & Casualty Insurance Industry Segmentation By Geography

- 1. Japan

Japan Property & Casualty Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 4.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Status of Automobile Insurance in Japan

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Japan Property & Casualty Insurance Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 5.1.1. Property

- 5.1.2. Auto

- 5.1.3. Other Insurance Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct

- 5.2.2. Agents

- 5.2.3. Banks

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Tokio Marine & Nichido Fire Insurance Co Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Sompo Holdings Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Rakuten General Insurance Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 MS&AD Insurance Group Holdings Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 SAISON Automobile & Fire Insurance Co Ltd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 SECOM General Insurance Co Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Hitachi Capital Insurance Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Nisshin Fire & Marine Insurance Co Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Kyoei Fire & Marine Insurance Co Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Mitsui Direct General Insurance Co Ltd **List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Tokio Marine & Nichido Fire Insurance Co Ltd

List of Figures

- Figure 1: Japan Property & Casualty Insurance Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Japan Property & Casualty Insurance Industry Share (%) by Company 2024

List of Tables

- Table 1: Japan Property & Casualty Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Japan Property & Casualty Insurance Industry Revenue Million Forecast, by Insurance Type 2019 & 2032

- Table 3: Japan Property & Casualty Insurance Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 4: Japan Property & Casualty Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Japan Property & Casualty Insurance Industry Revenue Million Forecast, by Insurance Type 2019 & 2032

- Table 6: Japan Property & Casualty Insurance Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 7: Japan Property & Casualty Insurance Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Property & Casualty Insurance Industry?

The projected CAGR is approximately > 4.00%.

2. Which companies are prominent players in the Japan Property & Casualty Insurance Industry?

Key companies in the market include Tokio Marine & Nichido Fire Insurance Co Ltd, Sompo Holdings Inc, Rakuten General Insurance Co Ltd, MS&AD Insurance Group Holdings Inc, SAISON Automobile & Fire Insurance Co Ltd, SECOM General Insurance Co Ltd, Hitachi Capital Insurance Corporation, Nisshin Fire & Marine Insurance Co Ltd, Kyoei Fire & Marine Insurance Co Ltd, Mitsui Direct General Insurance Co Ltd **List Not Exhaustive.

3. What are the main segments of the Japan Property & Casualty Insurance Industry?

The market segments include Insurance Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Status of Automobile Insurance in Japan.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

July 2021 - Sompo International Holdings Ltd, a global, Bermuda-based specialty provider of property and casualty insurance and reinsurance, announced the launch of its Sompo Women in Insurance Management (SWIM) program, which aims to better prepare young women to assume future leadership roles at Sompo International. The initial program will begin in the United States in collaboration with High Point University located in High Point, North Carolina, to ultimately expand the program and approach to additional universities in the U.S. and internationally.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Property & Casualty Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Property & Casualty Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Property & Casualty Insurance Industry?

To stay informed about further developments, trends, and reports in the Japan Property & Casualty Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence