Key Insights

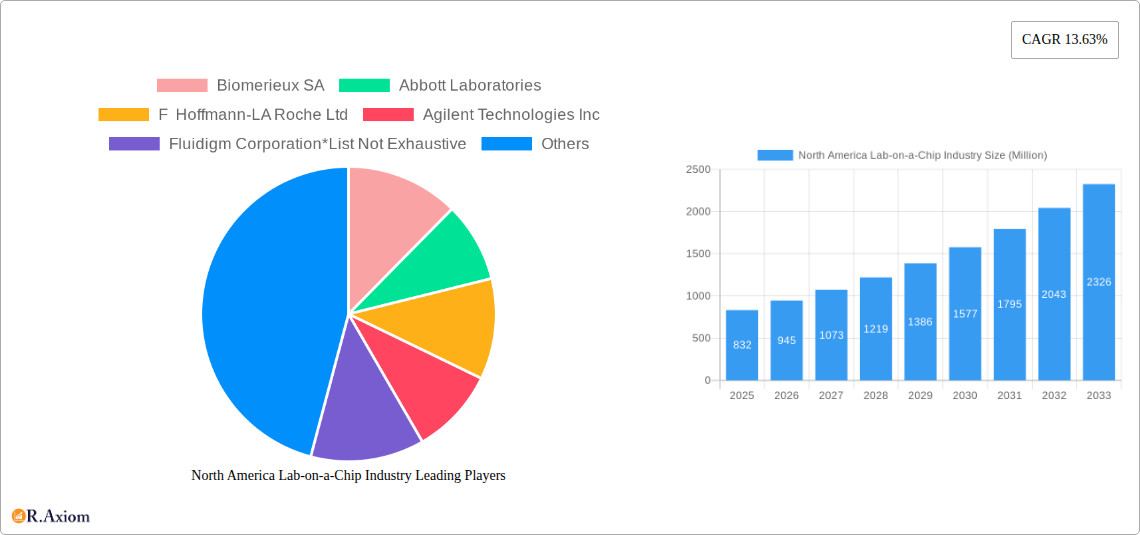

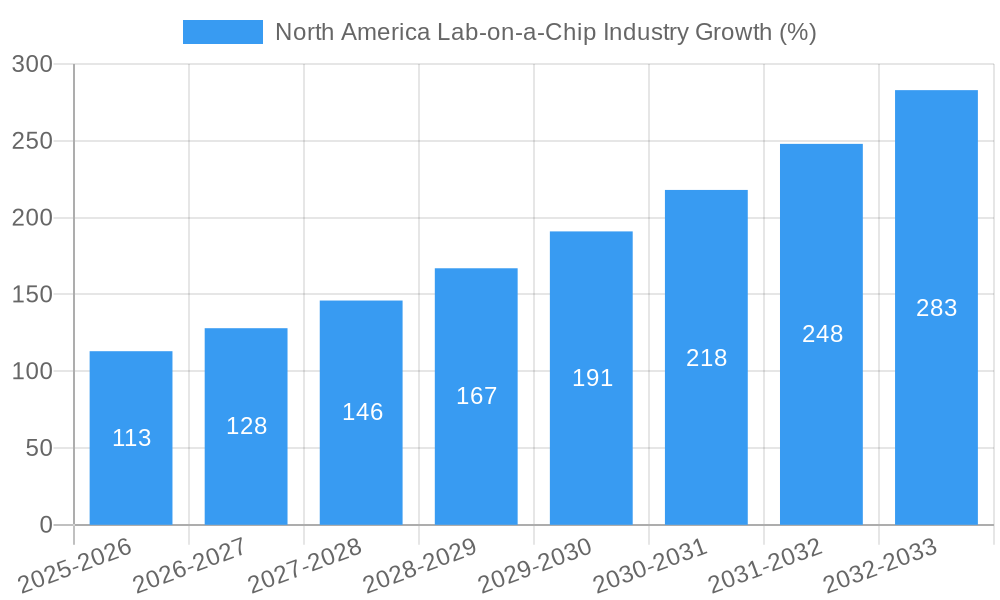

The North American lab-on-a-chip market, valued at approximately $X million in 2025, is poised for robust growth, projected to reach $Y million by 2033, exhibiting a compound annual growth rate (CAGR) of 13.63%. This expansion is driven by several key factors. Firstly, the increasing prevalence of chronic diseases necessitates faster and more efficient diagnostic tools, fueling demand for lab-on-a-chip technologies offering rapid, point-of-care testing. Secondly, the rising adoption of personalized medicine demands sophisticated analytical techniques, which lab-on-a-chip systems excel at providing through miniaturization and high throughput capabilities. Advancements in microfluidics, nanotechnology, and biosensors are further propelling market growth, enabling the development of more sensitive and specific diagnostic assays. The burgeoning biotechnology and pharmaceutical industries in North America, coupled with significant investments in research and development, contribute significantly to the market's expansion. Furthermore, government initiatives promoting point-of-care diagnostics and personalized medicine are creating a favorable regulatory environment for lab-on-a-chip technology adoption.

However, the market faces some challenges. High initial investment costs associated with developing and implementing lab-on-a-chip systems can be a barrier to entry for smaller companies and healthcare providers. Moreover, regulatory hurdles and the need for standardization across different lab-on-a-chip platforms can sometimes hinder broader market penetration. Despite these challenges, the significant advantages offered by lab-on-a-chip technology, such as reduced sample volume, faster turnaround times, and cost-effectiveness in the long run, are anticipated to outweigh these constraints, ensuring continued market growth throughout the forecast period. The strong presence of major players like Thermo Fisher Scientific, Illumina, and Abbott Laboratories in North America further solidifies the region's dominance in this rapidly evolving market. (Note: X and Y are estimations based on the provided 2025 market size and CAGR, requiring further data for precise calculation.)

This comprehensive report provides an in-depth analysis of the North America lab-on-a-chip industry, covering market size, growth drivers, challenges, and future opportunities. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. This report is crucial for industry stakeholders, investors, and researchers seeking actionable insights into this dynamic market.

North America Lab-on-a-Chip Industry Market Concentration & Innovation

The North American lab-on-a-chip market is characterized by a moderately concentrated landscape with several major players holding significant market share. Companies like Biomerieux SA, Abbott Laboratories, F Hoffmann-LA Roche Ltd, Agilent Technologies Inc, and Thermo Fisher Scientific dominate the market, collectively accounting for an estimated xx% of the total revenue in 2025. However, the presence of numerous smaller companies and startups fosters innovation and competition.

Market concentration is influenced by factors including R&D investments, technological advancements, regulatory approvals, and strategic acquisitions. The average M&A deal value in the sector during the historical period (2019-2024) was approximately $xx Million, reflecting substantial consolidation efforts.

- Innovation Drivers: Miniaturization, automation, point-of-care diagnostics, and integration with advanced technologies like AI and machine learning are driving innovation.

- Regulatory Framework: FDA regulations and other regional regulatory approvals significantly impact market dynamics. Stringent quality and safety standards necessitate substantial investment in compliance.

- Product Substitutes: Traditional laboratory methods pose a challenge, but the advantages of lab-on-a-chip technology, such as reduced cost and faster turnaround times, are driving market adoption.

- End-User Trends: Increasing demand for high-throughput screening, personalized medicine, and improved diagnostic accuracy are boosting market growth across various end-user segments.

North America Lab-on-a-Chip Industry Industry Trends & Insights

The North American lab-on-a-chip market is experiencing robust growth, driven by several key factors. The market is projected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), expanding from $xx Million in 2025 to $xx Million by 2033. Market penetration is particularly high in clinical diagnostics, driven by the increasing prevalence of chronic diseases and the demand for faster and more accurate diagnostic tests.

Technological disruptions, such as the development of advanced microfluidic devices and improved detection methods, are accelerating market growth. Consumer preferences are shifting toward personalized medicine and point-of-care diagnostics, creating opportunities for innovative lab-on-a-chip solutions. Competitive dynamics are characterized by both intense rivalry among established players and the emergence of innovative startups, leading to continuous product development and market expansion.

Dominant Markets & Segments in North America Lab-on-a-Chip Industry

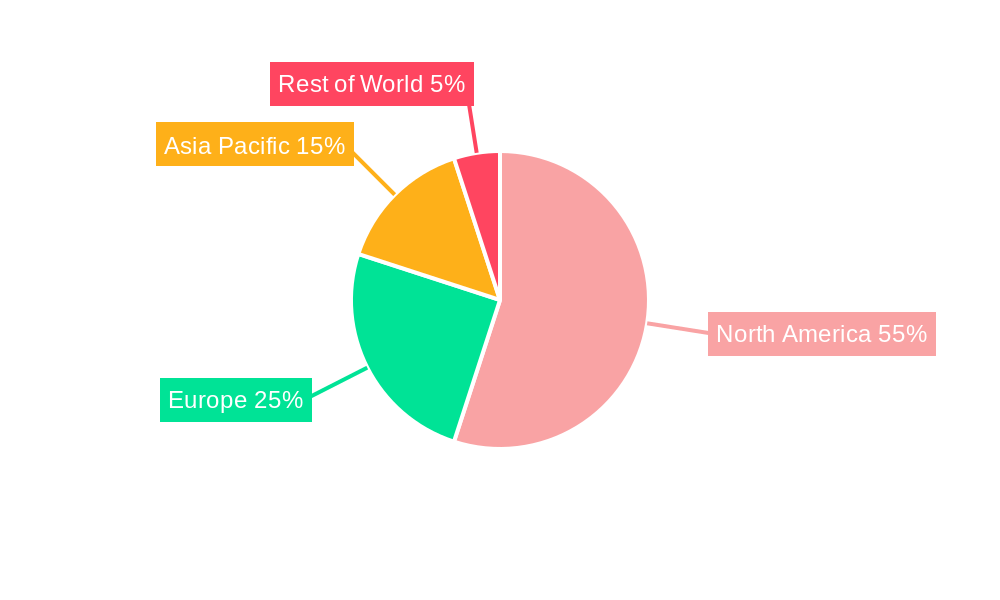

The United States dominates the North American lab-on-a-chip market, driven by robust healthcare infrastructure, high research and development spending, and a large pool of skilled professionals. Within the market segmentation:

By Product: Instruments hold the largest market share, followed by reagents and consumables, and then software and services. The high cost of instruments initially restricts market penetration, but the long-term cost-effectiveness of lab-on-a-chip technology offsets this.

By Application: Clinical diagnostics is the most significant segment due to the increasing demand for rapid and accurate diagnostic testing. Genomics and proteomics are also witnessing significant growth, fueled by advancements in personalized medicine.

By End-User: Biotechnology and pharmaceutical companies are leading adopters due to their extensive R&D activities. Hospitals and diagnostic centers represent another significant segment, given their reliance on efficient and accurate testing.

By Type: Lab-on-a-chip technology itself holds a larger market share than microarrays, owing to its greater versatility and potential for miniaturization.

Key drivers for market dominance include:

- Strong healthcare infrastructure: The US possesses a well-developed healthcare infrastructure, fostering rapid adoption of new technologies.

- High R&D spending: Significant investments in research and development fuel innovation in this field.

- Favorable regulatory environment: While stringent, the regulatory environment supports innovation.

North America Lab-on-a-Chip Industry Product Developments

Recent product developments focus on improving sensitivity, specificity, portability, and ease of use. Integration of advanced detection methods, such as fluorescence, electrochemical, and optical techniques, are enhancing the capabilities of lab-on-a-chip devices. The development of point-of-care diagnostic tools is a major focus, offering rapid diagnostics in settings beyond traditional laboratories. This trend caters to the growing demand for faster diagnostics and personalized healthcare solutions.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the North American lab-on-a-chip market across various segments:

By Product: Instruments, Reagents and Consumables, Software and Services. Each segment is analyzed in terms of market size, growth projections, and competitive dynamics.

By Application: Clinical Diagnostics, Drug Discovery, Genomics and Proteomics, Other Applications. This segmentation highlights the diverse applications of lab-on-a-chip technology across various industries.

By End-User: Biotechnology and Pharmaceutical Companies, Hospitals and Diagnostics Centers, Academic and Research Institutes. The analysis considers the unique needs and preferences of each user group.

By Type: Lab-on-a-chip, Microarray. This explores the distinct features and market potential of each technology.

Key Drivers of North America Lab-on-a-Chip Industry Growth

The growth of the North American lab-on-a-chip market is primarily driven by:

- Technological advancements: Continuous innovations in microfluidics, detection methods, and materials science are leading to improved device performance and functionality.

- Increasing demand for personalized medicine: The growing adoption of personalized healthcare approaches is driving demand for high-throughput screening and rapid diagnostic tests.

- Government funding and initiatives: Government support for research and development in life sciences is boosting innovation in this field.

Challenges in the North America Lab-on-a-Chip Industry Sector

Several factors pose challenges to the growth of the North American lab-on-a-chip market:

- High initial investment costs: The high cost of instrumentation can be a barrier to adoption, particularly for smaller laboratories and clinics.

- Regulatory hurdles: The stringent regulatory requirements for medical devices can delay product approvals and increase development costs.

- Supply chain disruptions: Global supply chain issues can impact the availability of critical components and materials.

Emerging Opportunities in North America Lab-on-a-Chip Industry

The North American lab-on-a-chip market offers several promising opportunities:

- Point-of-care diagnostics: The development of portable and user-friendly lab-on-a-chip devices for point-of-care testing is a significant growth opportunity.

- Integration with artificial intelligence: The integration of AI and machine learning algorithms can enhance the analytical capabilities of lab-on-a-chip systems.

- Expansion into new applications: The technology can find applications in various fields beyond diagnostics, including environmental monitoring and food safety testing.

Leading Players in the North America Lab-on-a-Chip Industry Market

- Biomerieux SA

- Abbott Laboratories

- F Hoffmann-LA Roche Ltd

- Agilent Technologies Inc

- Fluidigm Corporation

- Bio-Rad Laboratories

- PerkinElmer Inc

- Sysmex Corporation

- Illumina Inc

- Thermo Fisher Scientific

- Danaher Corporation (Beckman Coulter Inc)

Key Developments in North America Lab-on-a-Chip Industry Industry

May 2022: Invitae launched a new testing package for neuro-developmental disorders (NDDs) in children, leveraging chromosomal microarray analysis and next-generation sequencing. This expands the applications of lab-on-a-chip technologies in clinical diagnostics.

January 2022: Illumina, Inc. partnered with the National Cancer Center Japan to utilize high-throughput DNA sequencing for analyzing nasopharyngeal carcinoma, showcasing the technology's role in cancer research.

Strategic Outlook for North America Lab-on-a-Chip Industry Market

The North American lab-on-a-chip market is poised for substantial growth in the coming years, driven by ongoing technological advancements, increasing demand for personalized medicine, and supportive government policies. Continued investment in R&D, strategic partnerships, and expansion into new applications will be crucial for success in this dynamic market. The development of more affordable and user-friendly devices will also play a key role in broadening market access and driving wider adoption.

North America Lab-on-a-Chip Industry Segmentation

-

1. Type

- 1.1. Lab-on-a-chip

- 1.2. Microarray

-

2. Product

- 2.1. Instruments

- 2.2. Reagents and Consumables

- 2.3. Software and Services

-

3. Application

- 3.1. Clinical Diagnostics

- 3.2. Drug Discovery

- 3.3. Genomics and Proteomics

- 3.4. Other Applications

-

4. End User

- 4.1. Biotechnology and Pharmaceutical Companies

- 4.2. Hospitals and Diagnostics Centers

- 4.3. Academic and Research Institutes

-

5. Geography

- 5.1. United States

- 5.2. Canada

- 5.3. Mexico

North America Lab-on-a-Chip Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Lab-on-a-Chip Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 13.63% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Application of Proteomics And Genomics in Cancer Research; Technological Advances in the Materials in Microfluidics; Growth of Personalized Medicine

- 3.3. Market Restrains

- 3.3.1. Lack of Standardization; Availability of Alternative Technologies

- 3.4. Market Trends

- 3.4.1. Microarray are Anticipated to Hold Significant Share in the Studied Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Lab-on-a-Chip Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Lab-on-a-chip

- 5.1.2. Microarray

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Instruments

- 5.2.2. Reagents and Consumables

- 5.2.3. Software and Services

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Clinical Diagnostics

- 5.3.2. Drug Discovery

- 5.3.3. Genomics and Proteomics

- 5.3.4. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Biotechnology and Pharmaceutical Companies

- 5.4.2. Hospitals and Diagnostics Centers

- 5.4.3. Academic and Research Institutes

- 5.5. Market Analysis, Insights and Forecast - by Geography

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. United States

- 5.6.2. Canada

- 5.6.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States North America Lab-on-a-Chip Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Lab-on-a-chip

- 6.1.2. Microarray

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Instruments

- 6.2.2. Reagents and Consumables

- 6.2.3. Software and Services

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Clinical Diagnostics

- 6.3.2. Drug Discovery

- 6.3.3. Genomics and Proteomics

- 6.3.4. Other Applications

- 6.4. Market Analysis, Insights and Forecast - by End User

- 6.4.1. Biotechnology and Pharmaceutical Companies

- 6.4.2. Hospitals and Diagnostics Centers

- 6.4.3. Academic and Research Institutes

- 6.5. Market Analysis, Insights and Forecast - by Geography

- 6.5.1. United States

- 6.5.2. Canada

- 6.5.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Canada North America Lab-on-a-Chip Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Lab-on-a-chip

- 7.1.2. Microarray

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Instruments

- 7.2.2. Reagents and Consumables

- 7.2.3. Software and Services

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Clinical Diagnostics

- 7.3.2. Drug Discovery

- 7.3.3. Genomics and Proteomics

- 7.3.4. Other Applications

- 7.4. Market Analysis, Insights and Forecast - by End User

- 7.4.1. Biotechnology and Pharmaceutical Companies

- 7.4.2. Hospitals and Diagnostics Centers

- 7.4.3. Academic and Research Institutes

- 7.5. Market Analysis, Insights and Forecast - by Geography

- 7.5.1. United States

- 7.5.2. Canada

- 7.5.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Mexico North America Lab-on-a-Chip Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Lab-on-a-chip

- 8.1.2. Microarray

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Instruments

- 8.2.2. Reagents and Consumables

- 8.2.3. Software and Services

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Clinical Diagnostics

- 8.3.2. Drug Discovery

- 8.3.3. Genomics and Proteomics

- 8.3.4. Other Applications

- 8.4. Market Analysis, Insights and Forecast - by End User

- 8.4.1. Biotechnology and Pharmaceutical Companies

- 8.4.2. Hospitals and Diagnostics Centers

- 8.4.3. Academic and Research Institutes

- 8.5. Market Analysis, Insights and Forecast - by Geography

- 8.5.1. United States

- 8.5.2. Canada

- 8.5.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. United States North America Lab-on-a-Chip Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Lab-on-a-Chip Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Lab-on-a-Chip Industry Analysis, Insights and Forecast, 2019-2031

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 Biomerieux SA

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Abbott Laboratories

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 F Hoffmann-LA Roche Ltd

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Agilent Technologies Inc

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Fluidigm Corporation*List Not Exhaustive

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Bio-Rad Laboratories

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 PerkinElmer Inc

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Sysmex Corporation

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Illumina Inc

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Thermo Fisher Scientific

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.11 Danaher Corporation (Beckman Coulter Inc )

- 12.2.11.1. Overview

- 12.2.11.2. Products

- 12.2.11.3. SWOT Analysis

- 12.2.11.4. Recent Developments

- 12.2.11.5. Financials (Based on Availability)

- 12.2.1 Biomerieux SA

List of Figures

- Figure 1: North America Lab-on-a-Chip Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Lab-on-a-Chip Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 3: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 5: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 6: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Product 2019 & 2032

- Table 7: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 8: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Application 2019 & 2032

- Table 9: North America Lab-on-a-Chip Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 10: North America Lab-on-a-Chip Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 11: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 12: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Geography 2019 & 2032

- Table 13: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 14: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 15: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 17: United States North America Lab-on-a-Chip Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: United States North America Lab-on-a-Chip Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 19: Canada North America Lab-on-a-Chip Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Canada North America Lab-on-a-Chip Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 21: Mexico North America Lab-on-a-Chip Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Mexico North America Lab-on-a-Chip Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 23: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 24: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 25: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 26: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Product 2019 & 2032

- Table 27: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 28: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Application 2019 & 2032

- Table 29: North America Lab-on-a-Chip Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 30: North America Lab-on-a-Chip Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 31: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 32: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Geography 2019 & 2032

- Table 33: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 35: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 36: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 37: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 38: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Product 2019 & 2032

- Table 39: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 40: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Application 2019 & 2032

- Table 41: North America Lab-on-a-Chip Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 42: North America Lab-on-a-Chip Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 43: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 44: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Geography 2019 & 2032

- Table 45: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 46: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 47: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 48: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 49: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 50: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Product 2019 & 2032

- Table 51: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 52: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Application 2019 & 2032

- Table 53: North America Lab-on-a-Chip Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 54: North America Lab-on-a-Chip Industry Volume K Units Forecast, by End User 2019 & 2032

- Table 55: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 56: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Geography 2019 & 2032

- Table 57: North America Lab-on-a-Chip Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: North America Lab-on-a-Chip Industry Volume K Units Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Lab-on-a-Chip Industry?

The projected CAGR is approximately 13.63%.

2. Which companies are prominent players in the North America Lab-on-a-Chip Industry?

Key companies in the market include Biomerieux SA, Abbott Laboratories, F Hoffmann-LA Roche Ltd, Agilent Technologies Inc, Fluidigm Corporation*List Not Exhaustive, Bio-Rad Laboratories, PerkinElmer Inc, Sysmex Corporation, Illumina Inc, Thermo Fisher Scientific, Danaher Corporation (Beckman Coulter Inc ).

3. What are the main segments of the North America Lab-on-a-Chip Industry?

The market segments include Type, Product, Application, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.32 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Application of Proteomics And Genomics in Cancer Research; Technological Advances in the Materials in Microfluidics; Growth of Personalized Medicine.

6. What are the notable trends driving market growth?

Microarray are Anticipated to Hold Significant Share in the Studied Market.

7. Are there any restraints impacting market growth?

Lack of Standardization; Availability of Alternative Technologies.

8. Can you provide examples of recent developments in the market?

May 2022: Invitae, a California-based medical genetics company that plans to open a new laboratory and production facility in Morrisville, commercially launched a new testing package for neuro-developmental disorders (NDDs) in children. The package includes chromosomal microarray analysis, analysis for fragile X-related disorders, and a next-generation-sequencing panel of 200-plus genes in which variants are associated with NDDs.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Lab-on-a-Chip Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Lab-on-a-Chip Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Lab-on-a-Chip Industry?

To stay informed about further developments, trends, and reports in the North America Lab-on-a-Chip Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence