Key Insights

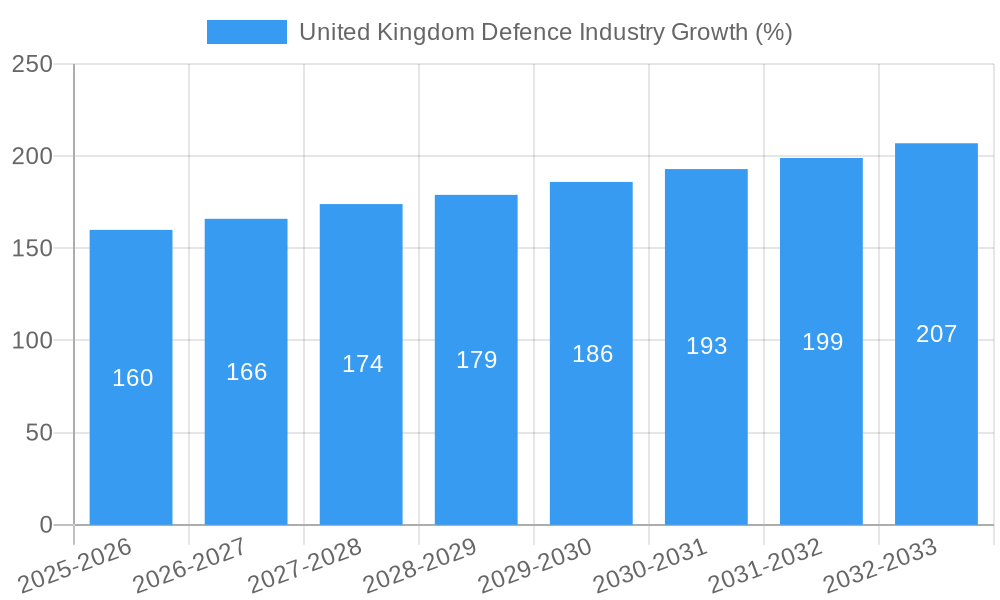

The United Kingdom defence industry, a significant player in global military spending, is projected to experience steady growth over the forecast period (2025-2033). With a global market size of $64.55 billion in 2025 and a Compound Annual Growth Rate (CAGR) of 3.12%, the UK's share, while not explicitly stated, can be reasonably estimated based on its historical contribution and ongoing geopolitical factors. Considering the UK's substantial military expenditure and its role in NATO, its defence industry likely represents a considerable portion of the global market, possibly exceeding $5 billion in 2025. Key drivers include modernization efforts across various military branches (Army, Navy, Air Force), investments in advanced technologies like C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) and unmanned systems, and rising geopolitical instability necessitating enhanced defence capabilities. Trends indicate a growing focus on cyber security, AI-driven solutions for defense applications, and collaborative partnerships between private companies and government entities to streamline development and procurement. However, potential restraints include budgetary constraints, regulatory hurdles related to technology acquisition and export controls, and competition from larger international defence contractors. Segmentation analysis reveals significant investments across fixed-wing aircraft, rotorcraft, naval vessels, and advanced weaponry, showcasing a diversified and robust UK defense industrial base.

The UK's defence sector benefits from a highly skilled workforce and a legacy of technological innovation. Major players like BAE Systems, Rolls-Royce, and QinetiQ are at the forefront of developing cutting-edge technologies. The government's continued commitment to defence spending and its strategic partnerships with allied nations will likely fuel future growth. Furthermore, the increasing focus on national security and counter-terrorism measures contributes to the sustained demand for advanced defence systems and services. Despite potential economic fluctuations and global uncertainties, the long-term outlook for the UK defence industry remains positive, fuelled by ongoing technological advancements and a persistent need for robust national security measures within a complex geopolitical landscape. A deeper analysis of specific segments (e.g., unmanned aerial vehicles or cyber security) would reveal finer-grained growth projections.

United Kingdom Defence Industry: 2019-2033 Market Analysis & Forecast Report

This comprehensive report provides a detailed analysis of the United Kingdom Defence Industry, covering market trends, competitive landscape, and future growth prospects from 2019 to 2033. The study period spans 2019-2024 (Historical Period), with 2025 as the base and estimated year, and a forecast period extending to 2033. The report offers actionable insights for industry stakeholders, investors, and government agencies. The market is valued at £xx Million in 2025 and is projected to reach £xx Million by 2033, exhibiting a CAGR of xx%.

United Kingdom Defence Industry Market Concentration & Innovation

This section analyzes the UK defence industry's market concentration, innovation drivers, regulatory landscape, and competitive dynamics. Key aspects include:

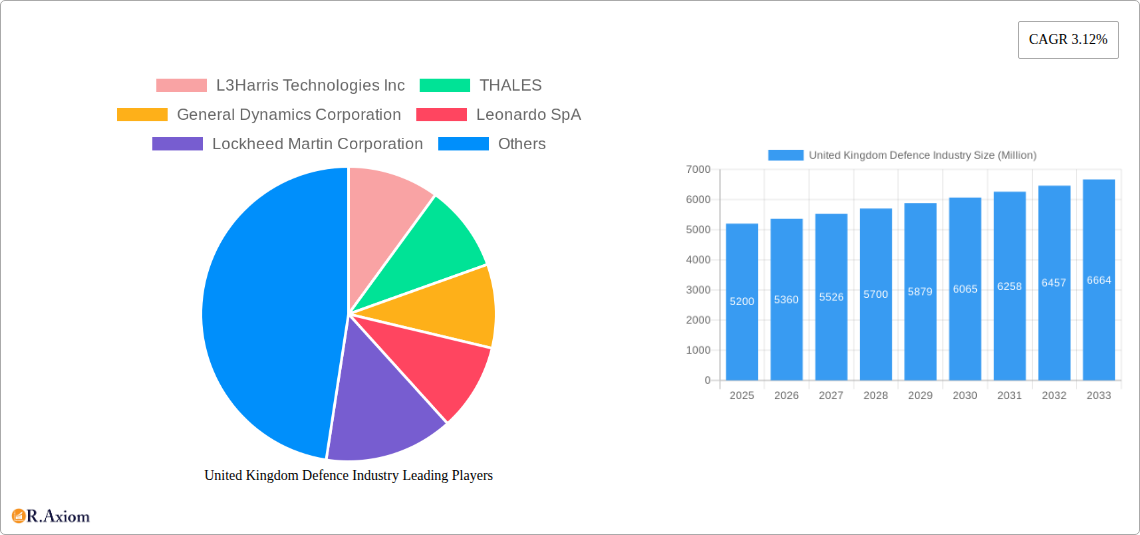

- Market Concentration: The UK defence market displays a moderately concentrated structure, with a few major players holding significant market share. BAE Systems PLC, for example, holds a substantial portion, while other multinational corporations like Lockheed Martin Corporation and Thales also have a considerable presence. The exact market share for each player varies by segment and is detailed within the full report.

- Innovation Drivers: Government funding for research and development (R&D), the need for technological advancements to maintain a competitive edge, and pressure to adopt cutting-edge technologies drive innovation. This includes focus on areas like AI, autonomous systems, and cyber security.

- Regulatory Framework: Strict regulations and oversight by the Ministry of Defence (MoD) shape the industry. This includes stringent quality control, security clearances, and export controls. Compliance is crucial for all operators.

- Product Substitutes & End-User Trends: The presence of substitutes is limited, as defence equipment often requires specialized technology and stringent security protocols. However, end-user trends include a shift towards increased automation, greater integration of systems, and lighter, more agile platforms.

- Mergers & Acquisitions (M&A): M&A activity has been significant in the sector, with deal values reaching £xx Million in recent years. These activities are driven by the need for companies to expand their product portfolios, enhance capabilities, and gain market share. Specific examples of M&A transactions, including deal values, are analyzed in the full report.

United Kingdom Defence Industry Industry Trends & Insights

The UK defence industry is experiencing significant transformation driven by various factors. Market growth is fuelled by increasing geopolitical instability, modernization efforts across the armed forces (Army, Navy, and Air Force), and a growing focus on national security. Technological advancements, particularly in areas like Artificial Intelligence (AI), unmanned systems, and cyber warfare, are disrupting traditional defence systems. Consumer preferences (i.e., the armed forces) are shifting towards more versatile, interoperable, and cost-effective solutions. Competitive dynamics are influenced by both domestic and international players, leading to increased innovation and pressure to deliver cutting-edge technologies. The report delves into these dynamics in detail, providing specific CAGR and market penetration data for key segments. We observe a strong emphasis on collaboration between private companies and government agencies to ensure effective modernization programs.

Dominant Markets & Segments in United Kingdom Defence Industry

The UK defence market displays significant strength across various segments, with several showing dominant positions.

- Dominant Armed Force: The UK's Army, Navy, and Air Force all represent significant markets, with specific spending priorities driving growth within each. Details of these priorities are provided within the full report.

- Dominant Equipment Types: Fixed-wing aircraft, naval vessels, and C4ISR systems represent some of the largest segments by value, driven by consistent demand for modernization and upgrades. Ground vehicles and weapons & ammunition also maintain significant market share.

- Key Drivers:

- Government Policy and Spending: Increased defence budgets and focused investment programs are primary drivers.

- Geopolitical Factors: Global instability and security concerns contribute significantly to demand.

- Technological Advancements: The adoption of new technologies necessitates upgrades and modernization.

A detailed analysis of each segment's market size, growth trajectory, and key drivers is provided in the full report.

United Kingdom Defence Industry Product Developments

Recent product innovations are centered on enhancing capabilities in areas like autonomous systems, cyber security, and AI-powered intelligence gathering. The emphasis is on developing highly integrated, interoperable systems that enhance situational awareness and improve operational effectiveness. These developments are crucial for the UK's defence forces to maintain technological superiority and address evolving threats.

Report Scope & Segmentation Analysis

This report comprehensively segments the UK defence market by:

- Armed Forces: Army, Navy, Air Force

- Equipment Type: Fixed-wing aircraft, rotorcraft, ground vehicles, naval vessels, C4ISR, weapons and ammunition, protection and training equipment, unmanned systems.

Each segment includes detailed analyses of market size, growth projections, and competitive dynamics, including key players' market share and strategies.

Key Drivers of United Kingdom Defence Industry Growth

Growth in the UK defence industry is primarily driven by:

- Increased Defence Spending: Government investments in modernising its armed forces drive significant growth.

- Technological Advancements: The integration of AI, unmanned systems, and cyber security technologies fuel demand for new systems.

- Geopolitical Instability: Global uncertainties and regional conflicts necessitate upgrades and expansion of military capabilities.

Challenges in the United Kingdom Defence Industry Sector

Challenges facing the UK defence industry include:

- Budgetary Constraints: Balancing defence spending with other national priorities can present challenges.

- Supply Chain Vulnerabilities: Reliance on international suppliers can introduce risks to the supply chain.

- Intense Competition: Competition from domestic and international players necessitates continuous innovation and cost control.

Emerging Opportunities in United Kingdom Defence Industry

Emerging opportunities lie in:

- Cybersecurity: The growing threat of cyberattacks creates demand for advanced cyber defence systems.

- AI and Autonomous Systems: The integration of AI and autonomous systems offers significant opportunities for innovation and capability enhancement.

- Space-Based Systems: Increased focus on space-based capabilities presents opportunities for investment and growth.

Leading Players in the United Kingdom Defence Industry Market

- BAE Systems PLC

- THALES

- General Dynamics Corporation

- Leonardo SpA

- Lockheed Martin Corporation

- Airbus SE

- Cobham Ultra SeniorCo S à r l

- MBDA

- RTX Corporation

- Babcock International Group PLC

- QinetiQ Group plc

- Northrop Grumman Corporation

- The Boeing Company

- HENSOLDT A

- L3Harris Technologies Inc

Key Developments in United Kingdom Defence Industry Industry

- 2023 (October): Announcement of a new £xx Million investment in the development of next-generation unmanned aerial vehicles.

- 2022 (June): Successful completion of sea trials for a new class of naval vessels, incorporating advanced sensor technologies.

- 2021 (March): Launch of a new strategic partnership between BAE Systems PLC and a leading technology firm to develop AI-powered defence systems. (Further details are included in the full report).

Strategic Outlook for United Kingdom Defence Industry Market

The UK defence industry is poised for continued growth, driven by sustained government investment, technological advancements, and the evolving global security landscape. Opportunities exist across multiple segments, particularly in areas like cybersecurity, AI, and unmanned systems. Companies that embrace innovation and adapt to changing technological trends will be best positioned to capitalize on the significant growth potential in the coming years.

United Kingdom Defence Industry Segmentation

-

1. Armed Forces

- 1.1. Army

- 1.2. Navy

- 1.3. Air Force

-

2. Type

- 2.1. Fixed-wing Aircraft

- 2.2. Rotorcraft

- 2.3. Ground Vehicles

- 2.4. Naval Vessels

- 2.5. C4ISR

- 2.6. Weapons and Ammunition

- 2.7. Protection and Training Equipment

- 2.8. Unmanned Systems

United Kingdom Defence Industry Segmentation By Geography

- 1. United Kingdom

United Kingdom Defence Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.12% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. The Navy is Expected to Witness the Highest Growth During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United Kingdom Defence Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Armed Forces

- 5.1.1. Army

- 5.1.2. Navy

- 5.1.3. Air Force

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Fixed-wing Aircraft

- 5.2.2. Rotorcraft

- 5.2.3. Ground Vehicles

- 5.2.4. Naval Vessels

- 5.2.5. C4ISR

- 5.2.6. Weapons and Ammunition

- 5.2.7. Protection and Training Equipment

- 5.2.8. Unmanned Systems

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Armed Forces

- 6. North America United Kingdom Defence Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1 United States

- 6.1.2 Canada

- 7. Europe United Kingdom Defence Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1 United Kingdom

- 7.1.2 France

- 7.1.3 Germany

- 7.1.4 Russia

- 7.1.5 Rest of Europe

- 8. Asia Pacific United Kingdom Defence Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1 China

- 8.1.2 India

- 8.1.3 Japan

- 8.1.4 South Korea

- 8.1.5 Rest of Asia Pacific

- 9. Latin America United Kingdom Defence Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 9.1.1 Brazil

- 9.1.2 Rest of Latin America

- 10. Middle East and Africa United Kingdom Defence Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 Saudi Arabia

- 10.1.2 United Arab Emirates

- 10.1.3 South Africa

- 10.1.4 Rest of Middle East and Africa

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 L3Harris Technologies Inc

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 THALES

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 General Dynamics Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Leonardo SpA

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Lockheed Martin Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Airbus SE

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Cobham Ultra SeniorCo S à r l

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 MBDA

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 RTX Corporation

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 BAE Systems PLC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Babcock International Group PLC

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 QinetiQ Group plc

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Northrop Grumman Corporation

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 The Boeing Company

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 HENSOLDT A

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 L3Harris Technologies Inc

List of Figures

- Figure 1: United Kingdom Defence Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: United Kingdom Defence Industry Share (%) by Company 2024

List of Tables

- Table 1: United Kingdom Defence Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: United Kingdom Defence Industry Revenue Million Forecast, by Armed Forces 2019 & 2032

- Table 3: United Kingdom Defence Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: United Kingdom Defence Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: United Kingdom Defence Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: United Kingdom Defence Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United Kingdom United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: France United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Germany United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Russia United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: United Kingdom Defence Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: China United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: India United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Japan United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: South Korea United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Rest of Asia Pacific United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: United Kingdom Defence Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: Brazil United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Latin America United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: United Kingdom Defence Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Saudi Arabia United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: United Arab Emirates United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: South Africa United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Rest of Middle East and Africa United Kingdom Defence Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: United Kingdom Defence Industry Revenue Million Forecast, by Armed Forces 2019 & 2032

- Table 29: United Kingdom Defence Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 30: United Kingdom Defence Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Defence Industry?

The projected CAGR is approximately 3.12%.

2. Which companies are prominent players in the United Kingdom Defence Industry?

Key companies in the market include L3Harris Technologies Inc, THALES, General Dynamics Corporation, Leonardo SpA, Lockheed Martin Corporation, Airbus SE, Cobham Ultra SeniorCo S à r l, MBDA, RTX Corporation, BAE Systems PLC, Babcock International Group PLC, QinetiQ Group plc, Northrop Grumman Corporation, The Boeing Company, HENSOLDT A.

3. What are the main segments of the United Kingdom Defence Industry?

The market segments include Armed Forces, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 64.55 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The Navy is Expected to Witness the Highest Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Defence Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Defence Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Defence Industry?

To stay informed about further developments, trends, and reports in the United Kingdom Defence Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence