Key Insights

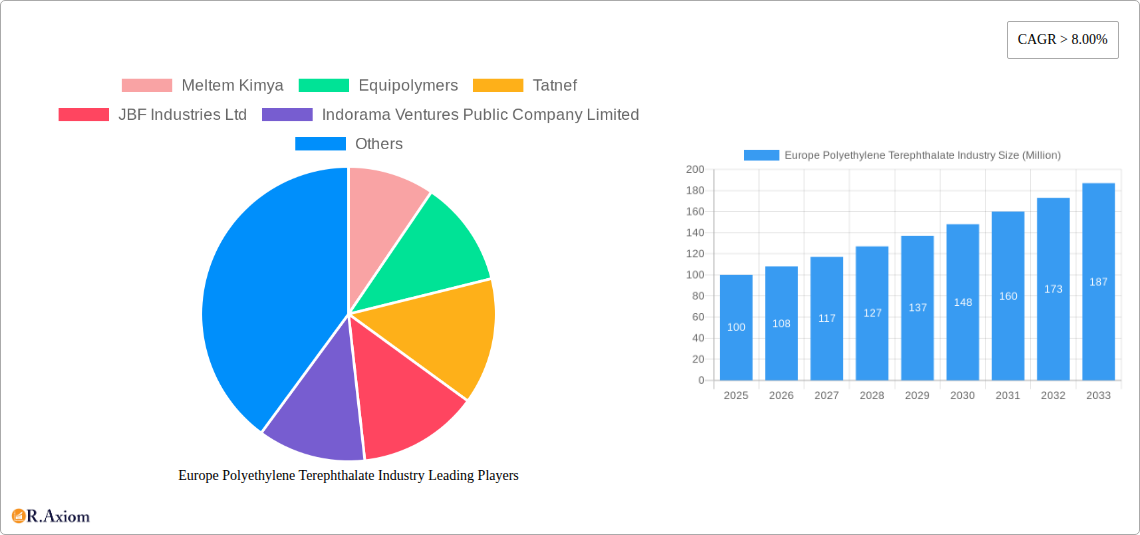

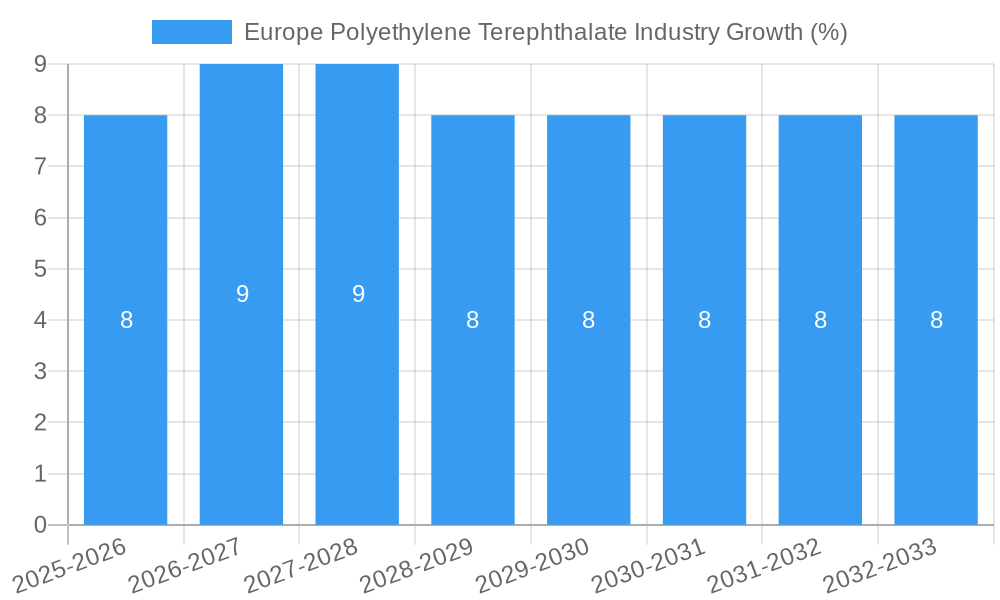

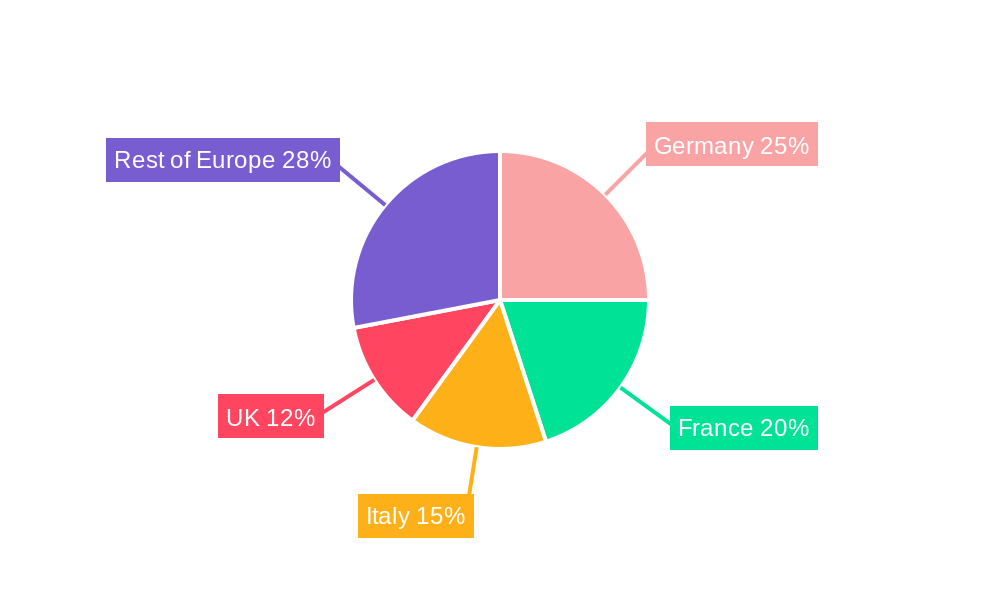

The European Polyethylene Terephthalate (PET) industry is experiencing robust growth, driven by increasing demand from the packaging, automotive, and building & construction sectors. The market, valued at approximately €[Estimate based on market size XX and value unit Million. For example, if XX represents 100 and the value unit is Million, the value would be €100 million in 2025], is projected to exhibit a Compound Annual Growth Rate (CAGR) exceeding 8% from 2025 to 2033. This growth is fueled by several key factors. Firstly, the rising consumption of bottled beverages and packaged food is significantly boosting demand for PET in packaging applications. Secondly, the automotive industry’s increasing use of PET in lightweight components contributes to market expansion. Furthermore, the building and construction sector is adopting PET for insulation and other applications, further driving market growth. Germany, France, Italy, and the United Kingdom represent the largest national markets within Europe, though other countries in the region also contribute significantly. While challenges such as fluctuating raw material prices and environmental concerns regarding PET's recyclability exist, the industry is actively addressing these through advancements in recycling technologies and the development of bio-based PET alternatives. This proactive approach is expected to mitigate potential restraints and maintain the overall positive growth trajectory.

The competitive landscape features a mix of both established global players and regional manufacturers. Companies like Indorama Ventures, Sibur Holding, and others are key players, competing on factors such as product quality, pricing, and technological innovation. The market is witnessing increased focus on sustainable PET production and improved recyclability, influencing both consumer preferences and regulatory landscape. The growth trajectory suggests that strategic investments in advanced recycling technologies and bio-based PET will be crucial for companies aiming to capitalize on future market opportunities. Furthermore, understanding regional regulations regarding plastic waste management will be critical for effective market penetration and sustained growth.

Europe Polyethylene Terephthalate (PET) Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Europe Polyethylene Terephthalate (PET) industry, covering market size, growth projections, key players, and emerging trends from 2019 to 2033. The report leverages extensive primary and secondary research to deliver actionable insights for industry stakeholders, including manufacturers, investors, and policymakers. With a focus on key segments and geographic regions, this report is an essential resource for understanding the current landscape and future trajectory of the European PET market.

Europe Polyethylene Terephthalate Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the European PET industry, examining market concentration, innovation drivers, regulatory frameworks, and recent M&A activities. The historical period (2019-2024) reveals a moderately concentrated market with several major players holding significant market share. The estimated market share for 2025 shows xx% for the top 5 players, while the remaining market share is distributed amongst smaller players. Innovation is driven by the increasing demand for sustainable and high-performance PET products, prompting investments in recycled PET (rPET) technologies and lightweighting solutions.

- Regulatory Framework: Stringent environmental regulations across Europe are driving the adoption of recycled content and sustainable manufacturing practices.

- Product Substitutes: Competition from alternative packaging materials, such as bioplastics and paper-based alternatives, is impacting market growth. However, the superior barrier properties and recyclability of PET continue to provide a competitive edge.

- End-User Trends: Growing demand from the packaging sector, particularly for food and beverage applications, is a major growth driver. The automotive and building & construction sectors also contribute significantly to PET demand.

- M&A Activities: Significant M&A activity has been observed, such as Alpek's acquisition of OCTAL in June 2022, resulting in increased production capacity and market consolidation. The total value of M&A deals in the period 2019-2024 is estimated at xx Million.

Europe Polyethylene Terephthalate Industry Industry Trends & Insights

The European PET industry is experiencing robust growth, driven by several key factors. The packaging segment remains the largest end-use application, exhibiting a CAGR of xx% during the forecast period (2025-2033). Increased consumer demand for convenience and ready-to-eat meals is fueling this growth. Technological advancements, such as the development of rPET materials and improved recycling technologies, are creating new opportunities. However, fluctuating raw material prices and supply chain disruptions pose challenges to market growth. The market penetration of rPET is steadily increasing, reaching xx% in 2025 and projected to reach xx% by 2033. This growth is significantly influenced by government policies promoting circular economy initiatives and consumer preference for sustainable products. Furthermore, competitive dynamics are characterized by increasing consolidation, leading to greater efficiency and technological advancements. The overall market shows a positive outlook, with continued growth driven by a combination of factors and supported by a steady CAGR throughout the forecast period.

Dominant Markets & Segments in Europe Polyethylene Terephthalate Industry

Germany, followed by France and the United Kingdom, are the leading markets for PET in Europe. These countries benefit from well-established manufacturing bases, robust infrastructure, and significant consumer demand. The Packaging segment accounts for the largest share of total consumption, driven by the food and beverage industry's preference for PET bottles and containers.

Key Drivers for Dominant Markets:

- Germany: Strong industrial base, advanced technology, and favorable government policies supporting sustainable packaging.

- France: Large consumer market, high demand for packaged goods, and focus on sustainable development initiatives.

- United Kingdom: Large population, well-developed retail sector, and increasing consumer awareness of sustainability.

- Packaging Segment: High demand for lightweight, recyclable packaging for food and beverages, coupled with the convenience it provides.

The Rest of Europe also shows considerable growth potential due to increasing industrialization and rising disposable incomes.

Europe Polyethylene Terephthalate Industry Product Developments

Recent innovations in the European PET industry focus on enhancing sustainability and performance. The development of ultra-thin-walled PET containers, as demonstrated by Novapet's launch of SPRIT B21, allows for reduced material usage and improved resource efficiency. Furthermore, the increasing use of rPET in PET products, driven by companies like SIBUR, significantly reduces environmental impact. These advancements highlight the industry's commitment to circular economy principles and address increasing consumer demand for eco-friendly products. This trend towards lighter, more recyclable, and sustainably sourced materials is expected to continue, shaping future product development and market competitiveness.

Report Scope & Segmentation Analysis

This report segments the European PET market based on end-user industry and geography.

End-User Industries: Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, Other End-user Industries. The Packaging segment dominates, showing xx Million in revenue in 2025, with projected growth to xx Million by 2033.

Geography: France, Germany, Italy, Russia, United Kingdom, Rest of Europe. Germany and France are leading consumers, demonstrating robust and steady growth.

Key Drivers of Europe Polyethylene Terephthalate Industry Growth

Several factors contribute to the growth of the European PET industry. Growing demand for convenient packaging, particularly in the food and beverage sector, is a major driver. Government initiatives promoting sustainability and circular economy principles are boosting the adoption of rPET. Technological advancements, including improved recycling technologies and the development of high-performance PET materials, are further enhancing market growth. Favorable economic conditions in several European countries also contribute to higher consumption.

Challenges in the Europe Polyethylene Terephthalate Industry Sector

The European PET industry faces several challenges, including fluctuating raw material prices, impacting profitability and requiring companies to adopt price optimization strategies. Supply chain disruptions can affect production and delivery schedules. Increasing competition from alternative packaging materials and stringent environmental regulations necessitate ongoing innovation and investment in sustainable technologies. The overall impact of these challenges varies depending on the specific company and its operational capabilities.

Emerging Opportunities in Europe Polyethylene Terephthalate Industry

The European PET market offers several emerging opportunities. The growing demand for sustainable packaging creates opportunities for companies focusing on rPET and bio-based PET. Innovations in PET packaging design, such as lightweighting and enhanced barrier properties, are also creating new avenues for growth. Expansion into new markets and product applications, such as in the healthcare and personal care sectors, represent further potential for growth.

Leading Players in the Europe Polyethylene Terephthalate Industry Market

- Meltem Kimya

- Equipolymers

- Tatnef

- JBF Industries Ltd

- Indorama Ventures Public Company Limited

- NEO GROUP

- Alfa S A B de C V

- Polyplex

- Novapet

- SIBUR Holding PJSC

Key Developments in Europe Polyethylene Terephthalate Industry Industry

- June 2022: Alpek acquired OCTAL, increasing its PET resin capacity by 576,000 tons.

- September 2022: SIBUR launched Vivilen rPET granules, containing up to 25–30% recycled polymers.

- November 2022: NOVAPET, S.A. launched ultra-thin-walled PET cups containing 30% recycled PET using Novapet SPRIT B21.

Strategic Outlook for Europe Polyethylene Terephthalate Industry Market

The European PET industry is poised for continued growth, driven by the increasing demand for sustainable and high-performance packaging solutions. The focus on rPET and circular economy initiatives will continue to shape industry dynamics. Technological innovations and strategic partnerships will play a crucial role in maintaining a competitive edge and expanding market share. The overall outlook is positive, with significant opportunities for companies that adapt to changing consumer preferences and regulatory landscapes.

Europe Polyethylene Terephthalate Industry Segmentation

-

1. End User Industry

- 1.1. Automotive

- 1.2. Building and Construction

- 1.3. Electrical and Electronics

- 1.4. Industrial and Machinery

- 1.5. Packaging

- 1.6. Other End-user Industries

Europe Polyethylene Terephthalate Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Polyethylene Terephthalate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 8.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Demand in Packaging Industry; Rising Demand in the Textile Industry

- 3.3. Market Restrains

- 3.3.1. Competition from Alternative Materials

- 3.4. Market Trends

- 3.4.1. Trend of using recycled PET (rPET) is gaining traction due to its environmental benefits

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Automotive

- 5.1.2. Building and Construction

- 5.1.3. Electrical and Electronics

- 5.1.4. Industrial and Machinery

- 5.1.5. Packaging

- 5.1.6. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Germany Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Polyethylene Terephthalate Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Meltem Kimya

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Equipolymers

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Tatnef

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 JBF Industries Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Indorama Ventures Public Company Limited

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 NEO GROUP

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Alfa S A B de C V

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Polyplex

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Novapet

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 SIBUR Holding PJSC

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Meltem Kimya

List of Figures

- Figure 1: Europe Polyethylene Terephthalate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Polyethylene Terephthalate Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Polyethylene Terephthalate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Polyethylene Terephthalate Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 3: Europe Polyethylene Terephthalate Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 4: Europe Polyethylene Terephthalate Industry Volume K Tons Forecast, by End User Industry 2019 & 2032

- Table 5: Europe Polyethylene Terephthalate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Polyethylene Terephthalate Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 7: Europe Polyethylene Terephthalate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Europe Polyethylene Terephthalate Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 9: Germany Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Germany Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 11: France Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 13: Italy Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Italy Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 15: United Kingdom Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: United Kingdom Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 17: Netherlands Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Netherlands Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 19: Sweden Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Sweden Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 21: Rest of Europe Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Europe Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 23: Europe Polyethylene Terephthalate Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 24: Europe Polyethylene Terephthalate Industry Volume K Tons Forecast, by End User Industry 2019 & 2032

- Table 25: Europe Polyethylene Terephthalate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Europe Polyethylene Terephthalate Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 27: United Kingdom Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: United Kingdom Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 29: Germany Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Germany Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 31: France Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: France Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 33: Italy Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Italy Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 35: Spain Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Spain Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 37: Netherlands Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Netherlands Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 39: Belgium Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Belgium Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 41: Sweden Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Sweden Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 43: Norway Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Norway Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 45: Poland Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Poland Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 47: Denmark Europe Polyethylene Terephthalate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Denmark Europe Polyethylene Terephthalate Industry Volume (K Tons) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Polyethylene Terephthalate Industry?

The projected CAGR is approximately > 8.00%.

2. Which companies are prominent players in the Europe Polyethylene Terephthalate Industry?

Key companies in the market include Meltem Kimya, Equipolymers, Tatnef, JBF Industries Ltd, Indorama Ventures Public Company Limited, NEO GROUP, Alfa S A B de C V, Polyplex, Novapet, SIBUR Holding PJSC.

3. What are the main segments of the Europe Polyethylene Terephthalate Industry?

The market segments include End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand in Packaging Industry; Rising Demand in the Textile Industry.

6. What are the notable trends driving market growth?

Trend of using recycled PET (rPET) is gaining traction due to its environmental benefits.

7. Are there any restraints impacting market growth?

Competition from Alternative Materials.

8. Can you provide examples of recent developments in the market?

November 2022: NOVAPET, S.A. launched ultra-thin-walled PET cups containing 30% recycled PET using Novapet SPRIT B21.September 2022: SIBUR launched the production of PET granules using recycled feedstock. The new product, Vivilen rPET granules, contains up to 25–30% recycled polymers and will now be manufactured at POLIEF.June 2022: Alpek acquired OCTAL, which increased Alpek's PET resin capacity by 576,000 tons, helping it meet customers' increased demand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Polyethylene Terephthalate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Polyethylene Terephthalate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Polyethylene Terephthalate Industry?

To stay informed about further developments, trends, and reports in the Europe Polyethylene Terephthalate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence