Key Insights

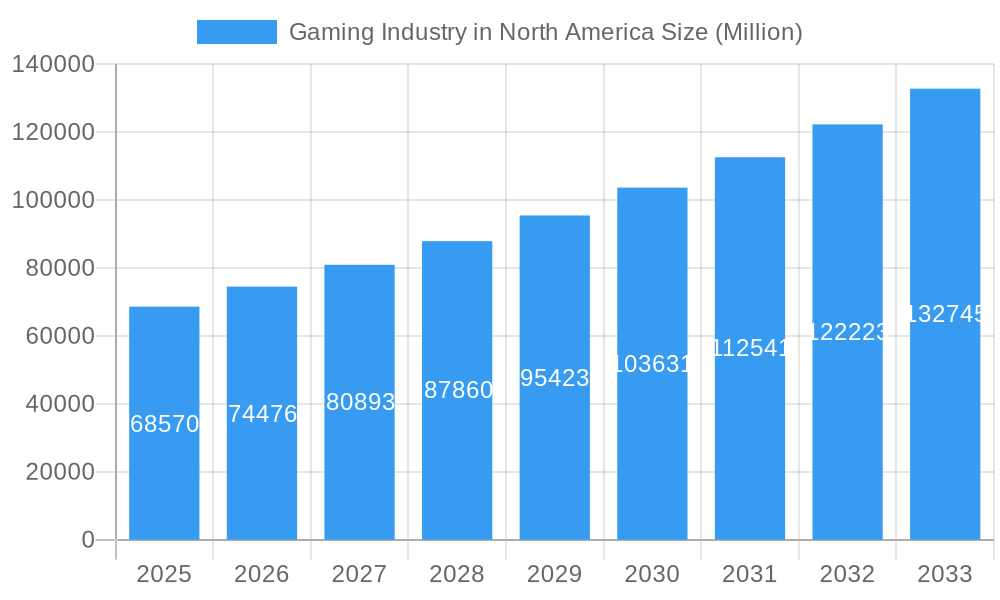

The North American gaming market, a significant segment of the global industry, is experiencing robust growth, projected to reach a substantial size. Driven by factors such as the increasing popularity of esports, the rise of mobile gaming, and the continued expansion of high-speed internet access, this market demonstrates significant potential. The consistent introduction of innovative game titles, coupled with technological advancements in game development and hardware, further fuels this expansion. While the exact market size in 2025 requires more specific data, using the provided CAGR of 8.65% and a base year of 2025, we can project significant growth over the forecast period (2025-2033). The dominance of the US within North America is expected to continue, given its large and engaged gaming community. However, the Canadian market also displays substantial growth potential, boosted by increasing smartphone penetration and the rising popularity of cloud gaming services. This growth is segmented across digital, physical, and online/microtransaction revenue streams, with digital likely maintaining a leading share due to the convenience and accessibility of digital distribution platforms. Competition within the sector remains fierce, with established players like Activision Blizzard, Electronic Arts, and Microsoft vying for market share alongside emerging independent developers and studios.

Gaming Industry in North America Market Size (In Billion)

Despite the overall positive outlook, the market faces potential challenges. These include the cyclical nature of game releases, the potential for market saturation in specific genres, and the ongoing need to innovate to capture and retain player interest. Furthermore, concerns regarding game addiction and the ethical considerations of microtransactions may also influence growth trajectory. The expansion of regulation and changes in consumer spending habits could also impact future market performance. However, ongoing technological advancements, the incorporation of new platforms and formats (such as virtual and augmented reality), and the sustained appeal of interactive entertainment are expected to offset these challenges and sustain the market's positive growth trajectory in the long term.

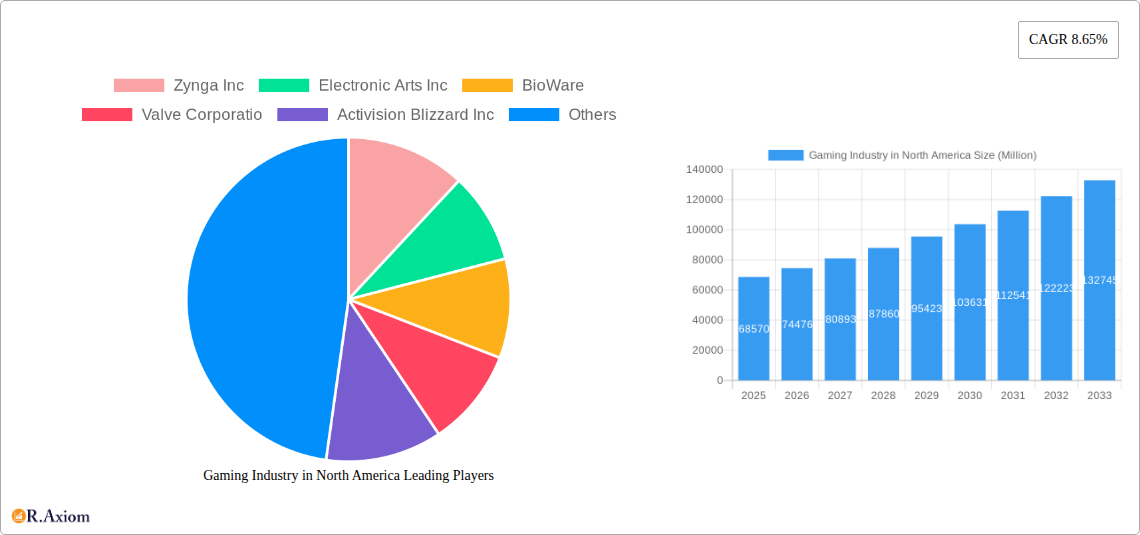

Gaming Industry in North America Company Market Share

This in-depth report provides a comprehensive analysis of the North American gaming industry, covering market size, segmentation, key players, growth drivers, challenges, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The forecast period is 2025-2033, and the historical period is 2019-2024. The report leverages extensive data analysis to provide actionable insights for industry stakeholders, investors, and businesses operating within this dynamic market. Expected market value in Millions unless otherwise stated.

Gaming Industry in North America Market Concentration & Innovation

This section analyzes the competitive landscape, innovation drivers, regulatory environment, and M&A activities within the North American gaming industry. The market exhibits a high degree of concentration, with a few dominant players holding significant market share. For example, Activision Blizzard Inc. and Electronic Arts Inc. command substantial portions of the market. However, smaller, specialized studios continue to innovate and disrupt specific niches.

Market Concentration Metrics (2024 Estimates):

- Top 3 Players Market Share: 60% (xx)

- Top 5 Players Market Share: 75% (xx)

- Average M&A Deal Value (2019-2024): $xx Million

Innovation Drivers:

- Advancements in game engines (Unreal Engine, Unity) driving enhanced graphics and gameplay.

- Expansion of cloud gaming services, improving accessibility and reducing hardware barriers.

- Growth of esports and competitive gaming, creating new revenue streams and engagement models.

- Emerging technologies such as VR/AR and blockchain creating novel gaming experiences.

Regulatory Frameworks:

- Varying regulations across states/provinces impacting game distribution and monetization strategies.

- Increasing scrutiny regarding loot boxes and in-app purchases, particularly concerning child protection.

- Data privacy regulations (e.g., CCPA, GDPR) shaping data collection and user consent practices.

Product Substitutes:

- Streaming services (Netflix, Disney+) and other forms of entertainment competing for consumer time and spending.

- Social media and mobile apps offering alternative engagement and social interaction.

End-User Trends:

- Shift towards mobile gaming and subscription models driving revenue diversification.

- Increased demand for cross-platform compatibility and seamless gaming experiences.

- Growing interest in casual and hyper-casual games, broadening the market's demographic reach.

M&A Activities:

The gaming industry has witnessed significant M&A activity in recent years, primarily driven by the consolidation of major players and the acquisition of smaller studios with specialized expertise. Deals have focused on acquiring intellectual property, technology, and talent to expand market presence and capabilities.

Gaming Industry in North America Industry Trends & Insights

The North American gaming market is experiencing robust growth, driven by a confluence of factors. Technological advancements, evolving consumer preferences, and the rise of esports are key contributors to this expansion. The market is witnessing a notable shift toward mobile and online gaming, along with the increasing popularity of subscription-based services. The competitive dynamics are intense, with established players vying for market share against emerging independent developers and innovative technologies.

Key Growth Drivers:

- Rising smartphone penetration and affordable mobile internet access.

- Increased adoption of cloud gaming and streaming platforms.

- The growing popularity of esports and competitive gaming.

- Expansion of the metaverse and immersive gaming experiences.

Technological Disruptions:

- Advancements in artificial intelligence (AI) and machine learning enhancing game design and player experience.

- Blockchain technology offering new possibilities for decentralized gaming and in-game economies.

- Virtual and Augmented Reality (VR/AR) technologies creating immersive and interactive gaming environments.

Consumer Preferences:

- Growing demand for free-to-play and subscription-based games.

- Increased preference for social and multiplayer gaming experiences.

- Rising demand for high-quality graphics and engaging storylines.

Competitive Dynamics:

The North American gaming market is fiercely competitive. Established players such as Electronic Arts Inc., Activision Blizzard Inc., and Microsoft Corporation compete with numerous independent developers and smaller studios. Competition is focused on securing exclusive content, technological innovation, and building strong gaming communities.

Market Growth Metrics (2019-2033):

- CAGR: xx%

- Market Penetration: xx% (by 2033)

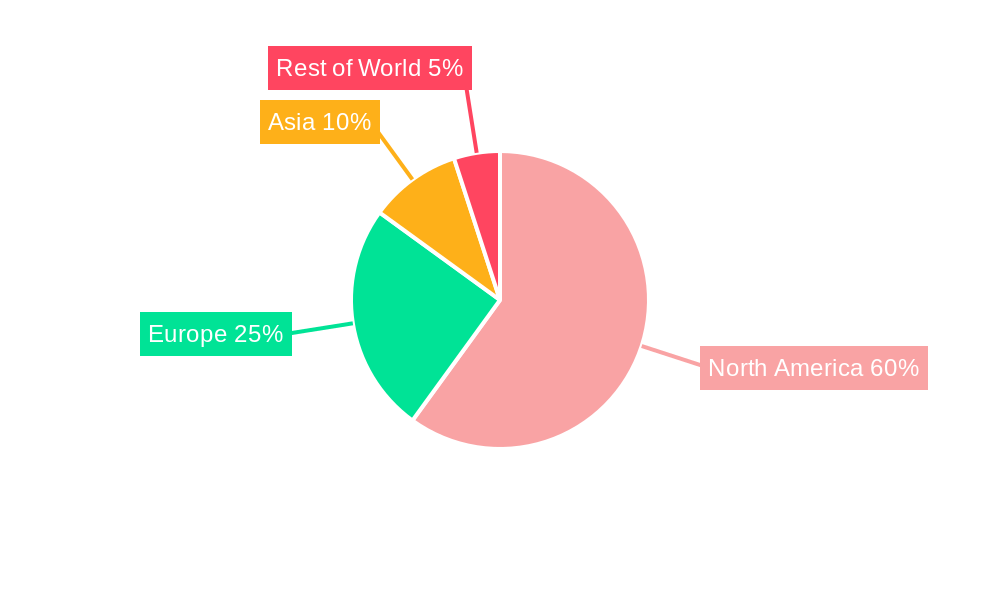

Dominant Markets & Segments in Gaming Industry in North America

The US represents the largest gaming market in North America, followed by Canada. The digital segment dominates overall gaming revenue, driven by the popularity of mobile and online games. Microtransactions continue to grow as a substantial revenue stream for many game publishers.

By Country:

- United States: Dominance is driven by a large and engaged player base, strong technological infrastructure, and high disposable income. The US also benefits from a well-established games development ecosystem.

- Canada: While smaller than the US market, Canada boasts a significant and active player base, with a growing presence in game development and esports.

By Gaming Type:

- Digital: This segment encompasses mobile, PC, and console digital downloads, representing the largest revenue share due to increased accessibility and convenience. The rise of digital distribution platforms has greatly accelerated this growth.

- Physical: While declining in relative terms, physical games (retail copies) still hold a segment of the market, mostly driven by collectors and those without convenient access to digital distribution.

- Online/Microtransactions: This rapidly expanding segment comprises in-app purchases, loot boxes, and subscriptions. It is a critical revenue source for many game publishers, especially those operating free-to-play models. The monetization model is constantly evolving due to regulatory pressures and consumer preferences.

Key Drivers of Regional Dominance:

- Economic Factors: High disposable incomes in the US drive higher spending on entertainment, including gaming.

- Technological Infrastructure: Robust internet access and digital infrastructure are crucial for supporting online and digital gaming experiences.

- Government Policies: Favorable regulatory environments can support the growth of the gaming industry.

Gaming Industry in North America Product Developments

The gaming industry is constantly innovating, producing enhanced graphics, improved gameplay, and new game mechanics. This extends beyond traditional genres to the integration of AR and VR technology, making gaming more immersive and interactive. Cloud-based gaming platforms are also reducing the barriers to entry, leading to a wider and more diverse player base. These innovations create competitive advantages based on unique game mechanics, compelling storylines, or superior technology.

Report Scope & Segmentation Analysis

This report segments the North American gaming market by gaming type (Digital, Physical, Online/Microtransactions) and by country (US, Canada). Each segment is analyzed based on its market size, growth projections, and competitive dynamics. The digital segment is projected to experience the highest growth over the forecast period. The US continues to be the dominant market, driven by high spending and consumer engagement. Future projections highlight a continuing trend toward digital distribution, driving the growth in online and microtransactions.

Key Drivers of Gaming Industry in North America Growth

Several factors fuel the growth of the North American gaming industry. Technological advancements, such as the evolution of game engines and the rise of cloud gaming, are major drivers. Increased smartphone penetration and internet access expand the market's reach. The popularity of esports and competitive gaming creates new revenue streams. Finally, the ever-evolving nature of games and game design, coupled with the expanding adoption of immersive technology like VR/AR, offers continuous opportunities for growth.

Challenges in the Gaming Industry in North America Sector

The North American gaming industry faces challenges including increased regulatory scrutiny of loot boxes and in-app purchases, affecting monetization strategies. Supply chain disruptions can impact the timely release of physical games. Intense competition and the rapid pace of technological change necessitate continuous investment in innovation and adaptation to remain competitive. The shifting consumer preferences also demand flexibility and responsiveness from developers.

Emerging Opportunities in Gaming Industry in North America

The metaverse presents a significant opportunity, offering immersive and interactive gaming experiences. Expansion into new markets through cloud gaming technologies and localization can tap into untapped player bases. The continued evolution of AR/VR technologies will create new avenues for gameplay and revenue generation.

Leading Players in the Gaming Industry in North America Market

Key Developments in Gaming Industry in North America Industry

- October 2022: Meta partnered with Microsoft Corporation to integrate Teams, Windows apps, and games onto Quest devices, expanding Meta's metaverse offerings.

- July 2022: Nuvei Corporation and GAN Limited partnered to provide payment solutions to gaming operators in the US and Canada, particularly relevant given the opening of Ontario's regulated gaming market.

Strategic Outlook for Gaming Industry in North America Market

The North American gaming market shows strong growth potential driven by technological innovation, increasing smartphone penetration, and the expanding popularity of esports and the metaverse. Companies must adapt to evolving consumer preferences, navigate regulatory changes, and continuously invest in research and development to maintain competitiveness. The industry's future is characterized by ongoing innovation, market consolidation, and the exploration of new technologies like VR/AR, blockchain, and AI to enhance gaming experiences and expand the player base.

Gaming Industry in North America Segmentation

-

1. Product Type

- 1.1. Digital Games

- 1.2. Physical Games

- 1.3. Online/Microtransactions

- 1.4. Virtual Reality (VR) and Augmented Reality (AR) Games

- 1.5. Mobile Games

-

2. Platform

- 2.1. Consoles

- 2.2. PCs

- 2.3. Mobile Devices

- 2.4. Virtual Reality Headsets

-

3. Region

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

Gaming Industry in North America Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

Gaming Industry in North America Regional Market Share

Geographic Coverage of Gaming Industry in North America

Gaming Industry in North America REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.65% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Digital Games

- 5.1.2. Physical Games

- 5.1.3. Online/Microtransactions

- 5.1.4. Virtual Reality (VR) and Augmented Reality (AR) Games

- 5.1.5. Mobile Games

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Consoles

- 5.2.2. PCs

- 5.2.3. Mobile Devices

- 5.2.4. Virtual Reality Headsets

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Gaming Industry in North America Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Digital Games

- 6.1.2. Physical Games

- 6.1.3. Online/Microtransactions

- 6.1.4. Virtual Reality (VR) and Augmented Reality (AR) Games

- 6.1.5. Mobile Games

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Consoles

- 6.2.2. PCs

- 6.2.3. Mobile Devices

- 6.2.4. Virtual Reality Headsets

- 6.3. Market Analysis, Insights and Forecast - by Region

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Zynga Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Electronic Arts Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BioWare

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Valve Corporatio

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Activision Blizzard Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Microsoft Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ubisoft Entertainment SA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Nintendo Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Take-Two Interactive Software Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sony Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Zynga Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Global Gaming Industry in North America Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Gaming Industry in North America Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Gaming Industry in North America Revenue (Million), by Product Type 2025 & 2033

- Figure 4: North America Gaming Industry in North America Volume (K Unit), by Product Type 2025 & 2033

- Figure 5: North America Gaming Industry in North America Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Gaming Industry in North America Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America Gaming Industry in North America Revenue (Million), by Platform 2025 & 2033

- Figure 8: North America Gaming Industry in North America Volume (K Unit), by Platform 2025 & 2033

- Figure 9: North America Gaming Industry in North America Revenue Share (%), by Platform 2025 & 2033

- Figure 10: North America Gaming Industry in North America Volume Share (%), by Platform 2025 & 2033

- Figure 11: North America Gaming Industry in North America Revenue (Million), by Region 2025 & 2033

- Figure 12: North America Gaming Industry in North America Volume (K Unit), by Region 2025 & 2033

- Figure 13: North America Gaming Industry in North America Revenue Share (%), by Region 2025 & 2033

- Figure 14: North America Gaming Industry in North America Volume Share (%), by Region 2025 & 2033

- Figure 15: North America Gaming Industry in North America Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Gaming Industry in North America Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Gaming Industry in North America Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Gaming Industry in North America Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gaming Industry in North America Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Gaming Industry in North America Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 3: Global Gaming Industry in North America Revenue Million Forecast, by Platform 2020 & 2033

- Table 4: Global Gaming Industry in North America Volume K Unit Forecast, by Platform 2020 & 2033

- Table 5: Global Gaming Industry in North America Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Gaming Industry in North America Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Gaming Industry in North America Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Gaming Industry in North America Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Gaming Industry in North America Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: Global Gaming Industry in North America Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 11: Global Gaming Industry in North America Revenue Million Forecast, by Platform 2020 & 2033

- Table 12: Global Gaming Industry in North America Volume K Unit Forecast, by Platform 2020 & 2033

- Table 13: Global Gaming Industry in North America Revenue Million Forecast, by Region 2020 & 2033

- Table 14: Global Gaming Industry in North America Volume K Unit Forecast, by Region 2020 & 2033

- Table 15: Global Gaming Industry in North America Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Gaming Industry in North America Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Gaming Industry in North America Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Gaming Industry in North America Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Gaming Industry in North America Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Gaming Industry in North America Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Gaming Industry in North America Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Gaming Industry in North America Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gaming Industry in North America?

The projected CAGR is approximately 8.65%.

2. Which companies are prominent players in the Gaming Industry in North America?

Key companies in the market include Zynga Inc, Electronic Arts Inc, BioWare, Valve Corporatio, Activision Blizzard Inc, Microsoft Corporation, Ubisoft Entertainment SA, Nintendo Co Ltd, Take-Two Interactive Software Inc, Sony Corporation.

3. What are the main segments of the Gaming Industry in North America?

The market segments include Product Type , Platform, Region.

4. Can you provide details about the market size?

The market size is estimated to be USD 68.57 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Smartphone and Internet Penetration; Adoption of Gaming Platforms. such as E-sports Betting and Fantasy Sites.

6. What are the notable trends driving market growth?

Rising Smartphone adoption and Internet Penetration Driving the Market Growth.

7. Are there any restraints impacting market growth?

Implementation and Integration Concerns Hindering the Market.

8. Can you provide examples of recent developments in the market?

October 2022 - Meta partnered with Microsoft Corporation to bring Teams, Windows apps, and games to Quest devices. The partnership is to bring new content, including Windows apps and Teams tie-ins, to Meta's metaverse hardware efforts.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gaming Industry in North America," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gaming Industry in North America report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gaming Industry in North America?

To stay informed about further developments, trends, and reports in the Gaming Industry in North America, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence