Key Insights

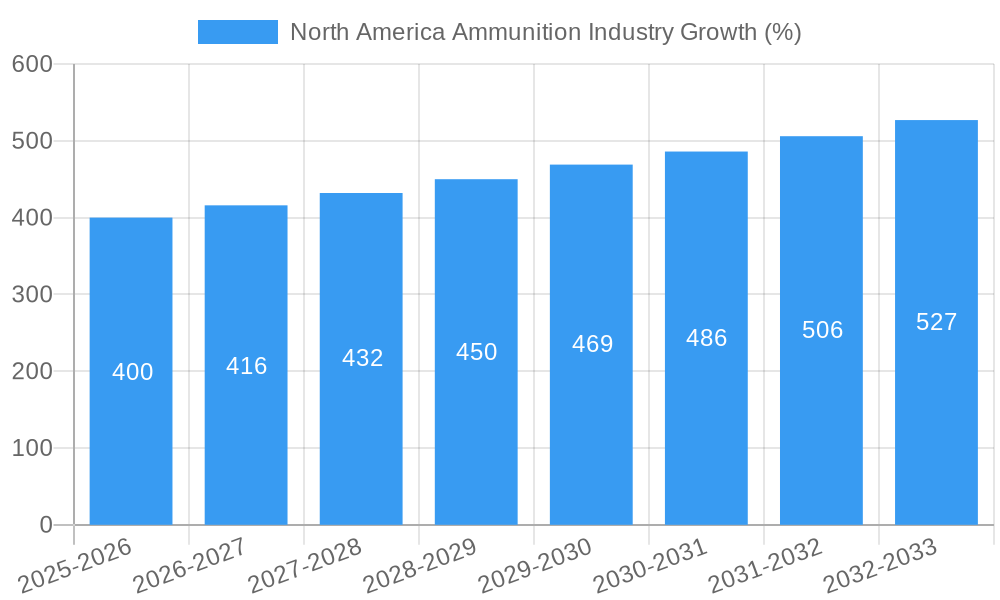

The North American ammunition market, valued at approximately $X billion in 2025, is projected to experience steady growth, exhibiting a compound annual growth rate (CAGR) of 4.00% from 2025 to 2033. This expansion is driven by several key factors. Firstly, sustained demand from both military and civilian sectors fuels market expansion. Military procurement continues to be a significant driver, particularly due to ongoing geopolitical instability and modernization efforts within armed forces. Simultaneously, the civilian market, encompassing hunting, sport shooting, and self-defense, contributes significantly to overall consumption. Growth within this segment is influenced by factors such as increasing firearm ownership, participation in shooting sports, and concerns about personal security. However, the market faces certain constraints, including stringent regulations on ammunition sales and manufacturing, potential fluctuations in raw material prices, and environmental concerns surrounding lead-based ammunition. Segmentation within the market reveals a diverse landscape, with small, medium, and large caliber ammunition catering to specific applications, further influencing market dynamics. The United States represents the largest segment within the North American market, owing to its substantial military spending and substantial civilian firearm ownership. Canada and Mexico contribute noticeably, yet at a smaller scale.

The competitive landscape is characterized by a mix of established industry giants like Nexter Group KNDS, General Dynamics, and Rheinmetall, alongside smaller specialized manufacturers. These companies constantly strive for technological advancements, aiming to enhance ammunition performance, reduce costs, and meet evolving market demands. The industry's future hinges on continued technological innovations, such as the development of advanced propellants and projectile designs, alongside strategic partnerships and mergers to maintain competitiveness. Furthermore, the growing emphasis on environmentally friendly ammunition, and the development of less-lethal alternatives, presents a significant avenue for future market growth and diversification. Sustained demand coupled with technological advancements and evolving regulations positions the North American ammunition market for moderate, yet consistent, growth throughout the forecast period.

North America Ammunition Industry: Market Analysis & Forecast (2019-2033)

This comprehensive report provides an in-depth analysis of the North America ammunition industry, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The study covers the period from 2019 to 2033, with a focus on the base year 2025 and forecast period 2025-2033. Key segments analyzed include small, medium, and large caliber ammunition, across civilian, military, and law enforcement end-user markets. The report leverages extensive primary and secondary research to deliver accurate market sizing, growth projections, and competitive landscaping.

North America Ammunition Industry Market Concentration & Innovation

The North American ammunition market exhibits a moderately concentrated structure, with key players holding significant market share. While precise market share figures are proprietary and vary by segment, leading companies like General Dynamics Corporation, Northrop Grumman Corporation, and BAE Systems PLC command substantial portions. The industry is characterized by continuous innovation driven by technological advancements in projectile design, propellant formulations, and smart ammunition technologies. Stringent regulatory frameworks, including those governing the manufacturing, storage, and sale of ammunition, influence market dynamics significantly. Substitutes, such as less lethal options and non-lethal weaponry, are impacting the market, particularly in civilian segments. Military end-user trends, such as increased demand for precision-guided munitions and advanced ammunition types, are shaping industry growth. The historical period (2019-2024) witnessed several M&A activities, with deal values estimated in the xx Million range, further consolidating market share among major players.

- Key Players: General Dynamics, Northrop Grumman, BAE Systems, Nexter Group KNDS, Rheinmetall AG, Global Ordnance LL, RUAG Group, CBC Global Ammunition, Winchester Ammunition (Olin Corporation), Nammo AS.

- Innovation Drivers: Advancements in materials science, smart munitions technology, and enhanced accuracy.

- Regulatory Frameworks: Strict regulations on manufacturing, distribution, and sales impacting market access and growth.

- M&A Activity: Significant consolidation through mergers and acquisitions in the historical period, with deal values totaling approximately xx Million.

North America Ammunition Industry Industry Trends & Insights

The North American ammunition market is projected to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by several factors including rising defense budgets, increasing demand for self-defense products in the civilian market, and the growing popularity of shooting sports. Technological disruptions, such as the development of advanced ammunition types with improved accuracy and lethality, are driving market innovation and enhancing product differentiation. Consumer preferences are shifting towards higher-quality, more reliable ammunition, leading to premiumization within certain segments. Competitive dynamics are characterized by intense rivalry among established players and the emergence of niche players specializing in specific ammunition types or end-user segments. Market penetration for advanced ammunition types, such as smart munitions, is expected to grow significantly during the forecast period, reaching xx% by 2033. The civilian segment is experiencing increased market penetration with estimates at xx% in 2025.

Dominant Markets & Segments in North America Ammunition Industry

The United States dominates the North American ammunition market, accounting for over xx% of the total market value. This dominance stems from several factors:

- High Military Spending: The US military's substantial defense budget drives significant demand for military-grade ammunition.

- Strong Civilian Market: A large and active civilian shooting sports and hunting community contributes to high civilian demand.

- Robust Manufacturing Base: The US possesses a mature and well-established ammunition manufacturing base.

Within the ammunition types, the small caliber segment holds the largest market share due to its widespread use in both civilian and military applications. The military segment remains the largest end-user, primarily driven by substantial governmental procurement and spending. The civilian market exhibits strong growth, particularly in the hunting and sport shooting segments.

North America Ammunition Industry Product Developments

Recent product developments focus on enhanced accuracy, reduced recoil, improved terminal ballistics, and smart ammunition technologies. These innovations are aimed at meeting the evolving needs of both military and civilian end-users, providing a competitive advantage by delivering superior performance and capabilities. The market is witnessing a trend towards increased use of advanced materials and manufacturing processes, leading to greater durability and reliability. These developments align with the growing demand for high-performance ammunition across various applications.

Report Scope & Segmentation Analysis

This report segments the North America ammunition market by type (small caliber, medium caliber, large caliber) and end-user (civilian, military).

By Type: The small caliber segment is the largest, characterized by high volume and diverse applications. Medium and large caliber segments cater to specialized military and industrial uses, exhibiting slower growth but higher price points.

By End-User: The military segment dominates due to large procurement contracts. The civilian segment shows steady growth driven by recreational shooting and hunting. The estimated market sizes for each segment and their projected growth rates over the forecast period are detailed within the full report.

Key Drivers of North America Ammunition Industry Growth

Several factors drive the growth of the North America ammunition industry:

- Increased Defense Spending: Government investment in military modernization and equipment upgrades fuels demand for ammunition.

- Growth in Civilian Markets: Rising popularity of shooting sports and hunting activities increases civilian demand.

- Technological Advancements: Innovations in ammunition technology enhance performance and create new market opportunities.

Challenges in the North America Ammunition Industry Sector

The industry faces several challenges:

- Stringent Regulations: Strict government regulations on ammunition manufacturing, distribution, and sales impact operational costs and market access.

- Supply Chain Disruptions: Global supply chain disruptions can affect raw material availability and production efficiency.

- Intense Competition: High competition among established players requires continuous innovation and efficiency improvements to maintain market share.

Emerging Opportunities in North America Ammunition Industry

Emerging opportunities include:

- Growth in Specialized Ammunition: Demand for specialized ammunition types, such as precision-guided munitions and less-lethal options, presents significant opportunities.

- Technological Advancements: Continued innovation in ammunition design and manufacturing offers opportunities for enhanced performance and capabilities.

- Expansion into New Markets: Exploring new geographic markets and end-user segments could yield significant growth potential.

Leading Players in the North America Ammunition Industry Market

- Nexter Group KNDS

- General Dynamics Corporation

- Rheinmetall AG

- Global Ordnance LL

- RUAG Group

- CBC Global Ammunition

- BAE Systems PLC

- Winchester Ammunition (Olin Corporation)

- Nammo AS

- Northrop Grumman Corporation

Key Developments in North America Ammunition Industry Industry

- 2022 Q4: General Dynamics announced a major contract for the supply of advanced ammunition to the US military.

- 2023 Q1: Northrop Grumman unveiled a new smart munition technology.

- 2023 Q2: A significant merger between two ammunition manufacturers reshaped the market landscape. (Further specific details are within the full report.)

Strategic Outlook for North America Ammunition Industry Market

The North America ammunition market is poised for continued growth, driven by sustained military demand, a vibrant civilian market, and ongoing technological innovation. Strategic opportunities lie in developing advanced ammunition technologies, expanding into new market segments, and enhancing supply chain resilience. The market is expected to witness increasing consolidation through mergers and acquisitions, leading to a more concentrated industry structure in the coming years.

North America Ammunition Industry Segmentation

-

1. Type

- 1.1. Small Caliber

- 1.2. Medium Caliber

- 1.3. Large Caliber

-

2. End User

- 2.1. Civilian

- 2.2. Military

-

3. Geography

-

3.1. North America

- 3.1.1. United States

- 3.1.2. Canada

-

3.1. North America

North America Ammunition Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

North America Ammunition Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Military Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Ammunition Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Small Caliber

- 5.1.2. Medium Caliber

- 5.1.3. Large Caliber

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Civilian

- 5.2.2. Military

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. North America

- 5.3.1.1. United States

- 5.3.1.2. Canada

- 5.3.1. North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States North America Ammunition Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Ammunition Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Ammunition Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Ammunition Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Nexter Group KNDS

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 General Dynamics Corporation

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Rheinmetall AG

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Global Ordnance LL

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 RUAG Group

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 CBC Global Ammunition

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 BAE Systems PLC

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Winchester Ammunition (Olin Corporation)

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Nammo AS

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Northrop Grumman Corporation

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Nexter Group KNDS

List of Figures

- Figure 1: North America Ammunition Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Ammunition Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Ammunition Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Ammunition Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: North America Ammunition Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 4: North America Ammunition Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: North America Ammunition Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Ammunition Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Ammunition Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Ammunition Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Ammunition Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Ammunition Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Ammunition Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 12: North America Ammunition Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 13: North America Ammunition Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 14: North America Ammunition Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States North America Ammunition Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Ammunition Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Ammunition Industry?

The projected CAGR is approximately 4.00%.

2. Which companies are prominent players in the North America Ammunition Industry?

Key companies in the market include Nexter Group KNDS, General Dynamics Corporation, Rheinmetall AG, Global Ordnance LL, RUAG Group, CBC Global Ammunition, BAE Systems PLC, Winchester Ammunition (Olin Corporation), Nammo AS, Northrop Grumman Corporation.

3. What are the main segments of the North America Ammunition Industry?

The market segments include Type, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Military Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Ammunition Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Ammunition Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Ammunition Industry?

To stay informed about further developments, trends, and reports in the North America Ammunition Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence