Key Insights

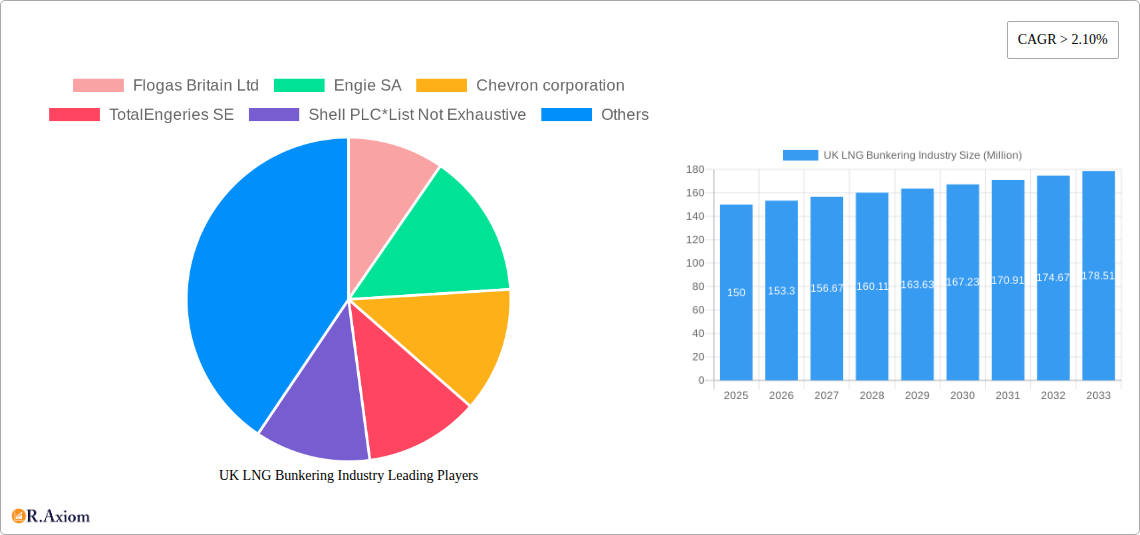

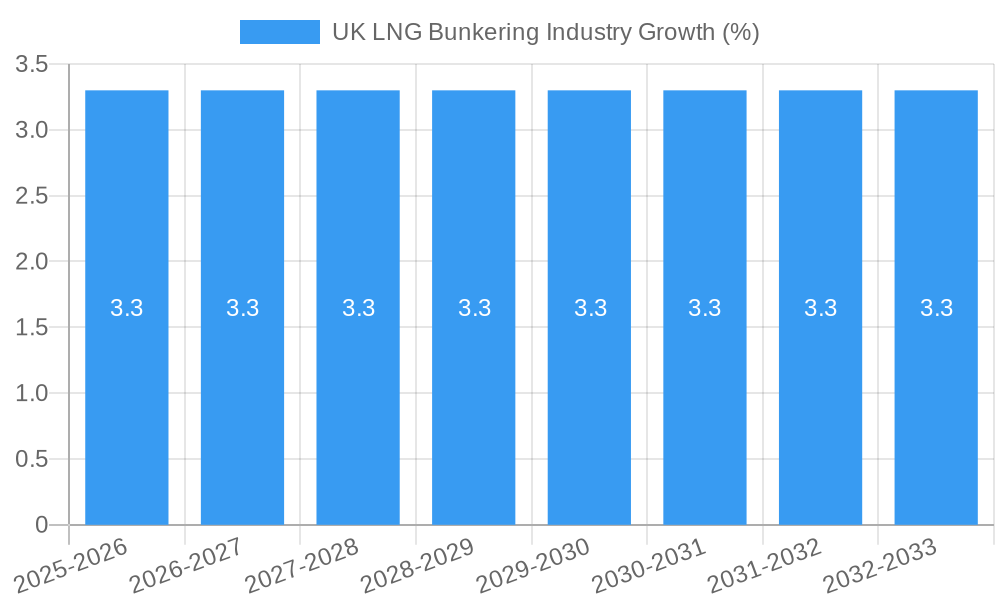

The UK LNG bunkering market, a crucial component of the broader European LNG market, is experiencing robust growth, driven by stringent emission regulations targeting the shipping industry and a growing emphasis on decarbonization. The market's expansion is fueled by increasing adoption of LNG as a cleaner alternative to traditional marine fuels, particularly within the port and transportation sectors. While precise UK-specific market sizing data is unavailable, extrapolating from the provided European context and a CAGR of 2.10%, we can estimate the 2025 UK LNG bunkering market value to be around £150 million (this is an estimation based on available data and is not fact). This figure is projected to increase significantly over the forecast period (2025-2033), mirroring the broader European trend. Key players like Flogas Britain Ltd, Engie SA, and major international energy corporations are actively investing in infrastructure and supply chains to meet this rising demand.

Growth is further supported by governmental incentives aimed at promoting cleaner shipping practices and the increasing availability of LNG bunkering infrastructure in key UK ports. However, challenges remain. High initial investment costs associated with LNG bunkering infrastructure and the fluctuating price of natural gas pose restraints to accelerated market growth. The market segmentation, encompassing both Bio-LNG and conventional LNG within shipping and port transportation applications, presents opportunities for specialized service providers and further fuels market diversification. The future success of the UK LNG bunkering market hinges on consistent policy support, technological advancements reducing costs, and the continued expansion of LNG-fueled vessels operating within UK waters.

UK LNG Bunkering Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the UK LNG bunkering industry, offering invaluable insights for stakeholders, investors, and industry professionals. The report covers the historical period (2019-2024), base year (2025), and forecasts the market's trajectory until 2033. The analysis incorporates key market segments (Natural gas, Bio-LNG) and applications (Shipping, Ports, Transportation), revealing growth drivers, challenges, and lucrative opportunities. Market size estimations in Millions are provided throughout.

UK LNG Bunkering Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the UK LNG bunkering market, examining market concentration, innovation drivers, regulatory frameworks, and M&A activities. The analysis reveals the market share of key players like Flogas Britain Ltd, Engie SA, Chevron Corporation, TotalEnergies SE, and Shell PLC (list not exhaustive), and assesses the impact of mergers and acquisitions on market dynamics. While precise market share figures are proprietary to the full report, preliminary analysis suggests a moderately concentrated market with the aforementioned companies holding a significant share collectively. The average M&A deal value in the period 2019-2024 is estimated at £xx Million, reflecting the sector's ongoing consolidation and strategic investments.

- Market Concentration: Moderately concentrated with a few major players dominating.

- Innovation Drivers: Stringent emission regulations, advancements in LNG technology, and growing demand for cleaner fuels.

- Regulatory Frameworks: The UK's commitment to decarbonization and maritime emission reduction targets significantly influences market growth.

- Product Substitutes: Competition from alternative marine fuels, such as methanol and ammonia, is emerging, but LNG remains a leading transitional fuel.

- End-User Trends: Increasing adoption of LNG bunkering by shipping companies due to environmental and economic considerations.

- M&A Activities: Strategic mergers and acquisitions are shaping the market landscape, driving consolidation and technological advancements.

UK LNG Bunkering Industry Industry Trends & Insights

This section delves into the key trends and insights shaping the UK LNG bunkering market. The analysis focuses on market growth drivers, technological disruptions, consumer preferences, and competitive dynamics, providing a comprehensive understanding of the market's evolution. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is projected at xx%, driven by increased demand for cleaner shipping fuels and government incentives. Market penetration of LNG as a marine fuel is expected to reach xx% by 2033. The report further explores the impact of technological advancements, such as the development of efficient LNG bunkering infrastructure and improved LNG storage and handling technologies. This analysis considers evolving consumer preferences towards environmentally friendly shipping solutions, the implications of global supply chain dynamics, and shifts in competitive dynamics, influenced by new entrants and strategic partnerships.

Dominant Markets & Segments in UK LNG Bunkering Industry

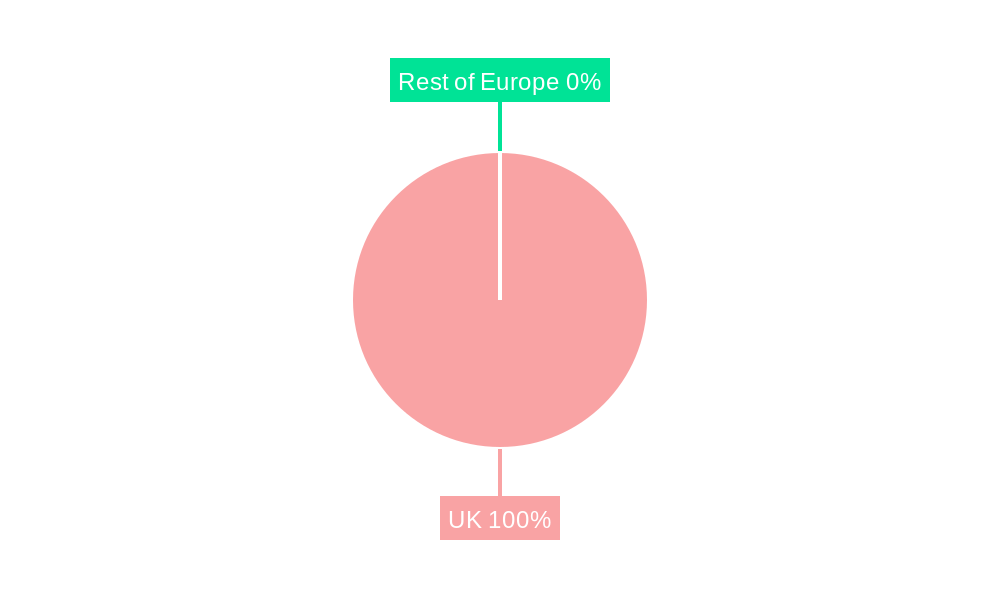

This section identifies the dominant market segments within the UK LNG bunkering industry, focusing on product (Natural gas, Bio-LNG) and application (Shipping, Ports, Transportation). The analysis reveals that the shipping segment is currently the dominant application, representing approximately xx% of the market in 2025, driven by stringent emission regulations and growing environmental concerns within the maritime sector. The UK is the leading region within the UK itself, due to its established port infrastructure and commitment to emission reduction targets.

Key Drivers for Shipping Dominance:

- Stringent emission regulations (e.g., IMO 2020)

- Growing environmental awareness amongst shipping companies

- Availability of LNG bunkering infrastructure in major ports

- Government incentives and subsidies for LNG adoption

Key Drivers for Natural Gas Dominance:

- Lower cost compared to Bio-LNG

- Established infrastructure and supply chains

- Wide availability

Detailed Dominance Analysis: The report provides a detailed analysis of the factors contributing to the dominance of the shipping segment and natural gas product, including economic policies, infrastructure development, and technological advancements.

UK LNG Bunkering Industry Product Developments

The UK LNG bunkering industry is witnessing significant product innovations, driven by the need for cleaner and more efficient fuels. The development of Bio-LNG, a sustainable alternative to conventional LNG, is gaining traction, offering a reduced carbon footprint compared to traditional fossil fuels. This progress is enhancing the industry's competitiveness by providing shipping companies with environmentally friendly options that comply with stricter emission regulations. Technological advancements in LNG storage and handling are also improving the efficiency and safety of bunkering operations.

Report Scope & Segmentation Analysis

This report segments the UK LNG bunkering market by product type (Natural Gas and Bio-LNG) and application (Shipping, Ports, and Transportation). The Natural Gas segment currently holds a larger market share, while Bio-LNG is experiencing rapid growth due to its sustainability advantages. Growth projections for both segments are included, with market sizes provided for each segment over the forecast period (2025-2033). Competitive dynamics within each segment are also analyzed.

- Natural Gas: This segment is expected to maintain a significant share of the market throughout the forecast period, driven by its established infrastructure and relatively lower cost.

- Bio-LNG: The Bio-LNG segment is poised for significant growth due to increasing environmental concerns and government policies promoting sustainable fuels. The segment is experiencing a faster growth rate than Natural Gas, with strong potential for market share increase.

- Shipping: This application segment dominates the overall market, driven by stringent emission regulations and the increasing adoption of LNG by shipping companies.

- Ports: The Ports segment represents an important area of growth, with infrastructure development in major ports facilitating LNG bunkering operations.

- Transportation: While less significant than shipping currently, the transportation segment (for example, heavy-duty trucking) is gaining traction, with ongoing developments in LNG infrastructure to support it.

Key Drivers of UK LNG Bunkering Industry Growth

The growth of the UK LNG bunkering industry is primarily driven by a confluence of factors. Stringent environmental regulations, such as IMO 2020, are compelling shipping companies to adopt cleaner fuels, significantly boosting demand for LNG. Government incentives and subsidies for LNG adoption are also playing a critical role. The development of advanced LNG bunkering infrastructure is further facilitating wider adoption. Finally, increasing awareness of environmental concerns amongst shipping companies and consumers promotes the transition towards sustainable fuels.

Challenges in the UK LNG Bunkering Industry Sector

Despite the growth potential, the UK LNG bunkering industry faces several challenges. High initial investment costs for LNG bunkering infrastructure can hinder wider adoption, particularly for smaller companies. The volatility of LNG prices can pose a significant risk to profitability. Furthermore, competition from alternative fuels, such as methanol and ammonia, needs to be considered. The limited availability of Bio-LNG presents a challenge to its wider adoption.

Emerging Opportunities in UK LNG Bunkering Industry

Emerging opportunities in the UK LNG bunkering industry include the growing market for Bio-LNG, driven by its environmental benefits. Technological advancements are continuing to enhance the efficiency and safety of LNG bunkering operations. Expansion of LNG bunkering infrastructure in smaller ports will also open up new growth avenues. The growing demand for LNG from sectors beyond shipping also presents opportunities for market diversification.

Leading Players in the UK LNG Bunkering Industry Market

- Flogas Britain Ltd

- Engie SA

- Chevron Corporation

- TotalEnergies SE

- Shell PLC

- List Not Exhaustive

Key Developments in UK LNG Bunkering Industry Industry

- May 2022: Avenir LNG announced the delivery of the Avenir Achievement, the second 20,000 cbm dual-purpose LNG supply and bunkering vessel from the Nantong CIMC Sinopacific Offshore & Engineering. This development significantly expands LNG bunkering capacity in the UK and enhances the industry's ability to meet growing demand.

Strategic Outlook for UK LNG Bunkering Industry Market

The UK LNG bunkering industry is poised for significant growth over the coming years, driven by a combination of factors including stricter environmental regulations, government support, and technological advancements. The increasing availability of Bio-LNG offers a sustainable pathway for the industry's future, and the expansion of LNG bunkering infrastructure will unlock further growth opportunities. The market's strategic outlook is positive, promising significant expansion and evolution in the coming decade.

UK LNG Bunkering Industry Segmentation

- 1. Tanker Fleet

- 2. Container Fleet

- 3. Bulk and General Cargo Fleet

- 4. Ferries and OSV

- 5. Others

UK LNG Bunkering Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

UK LNG Bunkering Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 2.10% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increase in the Demand for Electricity4.; Rising Adoption of Electric Vehicles

- 3.3. Market Restrains

- 3.3.1. 4.; New Sources of Distributed Electricity Generation

- 3.4. Market Trends

- 3.4.1. Ferries and OSV Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 5.2. Market Analysis, Insights and Forecast - by Container Fleet

- 5.3. Market Analysis, Insights and Forecast - by Bulk and General Cargo Fleet

- 5.4. Market Analysis, Insights and Forecast - by Ferries and OSV

- 5.5. Market Analysis, Insights and Forecast - by Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 6. North America UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 6.2. Market Analysis, Insights and Forecast - by Container Fleet

- 6.3. Market Analysis, Insights and Forecast - by Bulk and General Cargo Fleet

- 6.4. Market Analysis, Insights and Forecast - by Ferries and OSV

- 6.5. Market Analysis, Insights and Forecast - by Others

- 6.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 7. South America UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 7.2. Market Analysis, Insights and Forecast - by Container Fleet

- 7.3. Market Analysis, Insights and Forecast - by Bulk and General Cargo Fleet

- 7.4. Market Analysis, Insights and Forecast - by Ferries and OSV

- 7.5. Market Analysis, Insights and Forecast - by Others

- 7.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 8. Europe UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 8.2. Market Analysis, Insights and Forecast - by Container Fleet

- 8.3. Market Analysis, Insights and Forecast - by Bulk and General Cargo Fleet

- 8.4. Market Analysis, Insights and Forecast - by Ferries and OSV

- 8.5. Market Analysis, Insights and Forecast - by Others

- 8.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 9. Middle East & Africa UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 9.2. Market Analysis, Insights and Forecast - by Container Fleet

- 9.3. Market Analysis, Insights and Forecast - by Bulk and General Cargo Fleet

- 9.4. Market Analysis, Insights and Forecast - by Ferries and OSV

- 9.5. Market Analysis, Insights and Forecast - by Others

- 9.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 10. Asia Pacific UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 10.2. Market Analysis, Insights and Forecast - by Container Fleet

- 10.3. Market Analysis, Insights and Forecast - by Bulk and General Cargo Fleet

- 10.4. Market Analysis, Insights and Forecast - by Ferries and OSV

- 10.5. Market Analysis, Insights and Forecast - by Others

- 10.1. Market Analysis, Insights and Forecast - by Tanker Fleet

- 11. Germany UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 12. France UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 13. Italy UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 14. United Kingdom UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 15. Netherlands UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 16. Rest of Europe UK LNG Bunkering Industry Analysis, Insights and Forecast, 2019-2031

- 17. Competitive Analysis

- 17.1. Global Market Share Analysis 2024

- 17.2. Company Profiles

- 17.2.1 Flogas Britain Ltd

- 17.2.1.1. Overview

- 17.2.1.2. Products

- 17.2.1.3. SWOT Analysis

- 17.2.1.4. Recent Developments

- 17.2.1.5. Financials (Based on Availability)

- 17.2.2 Engie SA

- 17.2.2.1. Overview

- 17.2.2.2. Products

- 17.2.2.3. SWOT Analysis

- 17.2.2.4. Recent Developments

- 17.2.2.5. Financials (Based on Availability)

- 17.2.3 Chevron corporation

- 17.2.3.1. Overview

- 17.2.3.2. Products

- 17.2.3.3. SWOT Analysis

- 17.2.3.4. Recent Developments

- 17.2.3.5. Financials (Based on Availability)

- 17.2.4 TotalEngeries SE

- 17.2.4.1. Overview

- 17.2.4.2. Products

- 17.2.4.3. SWOT Analysis

- 17.2.4.4. Recent Developments

- 17.2.4.5. Financials (Based on Availability)

- 17.2.5 Shell PLC*List Not Exhaustive

- 17.2.5.1. Overview

- 17.2.5.2. Products

- 17.2.5.3. SWOT Analysis

- 17.2.5.4. Recent Developments

- 17.2.5.5. Financials (Based on Availability)

- 17.2.1 Flogas Britain Ltd

List of Figures

- Figure 1: Global UK LNG Bunkering Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Europe UK LNG Bunkering Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: Europe UK LNG Bunkering Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America UK LNG Bunkering Industry Revenue (Million), by Tanker Fleet 2024 & 2032

- Figure 5: North America UK LNG Bunkering Industry Revenue Share (%), by Tanker Fleet 2024 & 2032

- Figure 6: North America UK LNG Bunkering Industry Revenue (Million), by Container Fleet 2024 & 2032

- Figure 7: North America UK LNG Bunkering Industry Revenue Share (%), by Container Fleet 2024 & 2032

- Figure 8: North America UK LNG Bunkering Industry Revenue (Million), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 9: North America UK LNG Bunkering Industry Revenue Share (%), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 10: North America UK LNG Bunkering Industry Revenue (Million), by Ferries and OSV 2024 & 2032

- Figure 11: North America UK LNG Bunkering Industry Revenue Share (%), by Ferries and OSV 2024 & 2032

- Figure 12: North America UK LNG Bunkering Industry Revenue (Million), by Others 2024 & 2032

- Figure 13: North America UK LNG Bunkering Industry Revenue Share (%), by Others 2024 & 2032

- Figure 14: North America UK LNG Bunkering Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: North America UK LNG Bunkering Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: South America UK LNG Bunkering Industry Revenue (Million), by Tanker Fleet 2024 & 2032

- Figure 17: South America UK LNG Bunkering Industry Revenue Share (%), by Tanker Fleet 2024 & 2032

- Figure 18: South America UK LNG Bunkering Industry Revenue (Million), by Container Fleet 2024 & 2032

- Figure 19: South America UK LNG Bunkering Industry Revenue Share (%), by Container Fleet 2024 & 2032

- Figure 20: South America UK LNG Bunkering Industry Revenue (Million), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 21: South America UK LNG Bunkering Industry Revenue Share (%), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 22: South America UK LNG Bunkering Industry Revenue (Million), by Ferries and OSV 2024 & 2032

- Figure 23: South America UK LNG Bunkering Industry Revenue Share (%), by Ferries and OSV 2024 & 2032

- Figure 24: South America UK LNG Bunkering Industry Revenue (Million), by Others 2024 & 2032

- Figure 25: South America UK LNG Bunkering Industry Revenue Share (%), by Others 2024 & 2032

- Figure 26: South America UK LNG Bunkering Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: South America UK LNG Bunkering Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Europe UK LNG Bunkering Industry Revenue (Million), by Tanker Fleet 2024 & 2032

- Figure 29: Europe UK LNG Bunkering Industry Revenue Share (%), by Tanker Fleet 2024 & 2032

- Figure 30: Europe UK LNG Bunkering Industry Revenue (Million), by Container Fleet 2024 & 2032

- Figure 31: Europe UK LNG Bunkering Industry Revenue Share (%), by Container Fleet 2024 & 2032

- Figure 32: Europe UK LNG Bunkering Industry Revenue (Million), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 33: Europe UK LNG Bunkering Industry Revenue Share (%), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 34: Europe UK LNG Bunkering Industry Revenue (Million), by Ferries and OSV 2024 & 2032

- Figure 35: Europe UK LNG Bunkering Industry Revenue Share (%), by Ferries and OSV 2024 & 2032

- Figure 36: Europe UK LNG Bunkering Industry Revenue (Million), by Others 2024 & 2032

- Figure 37: Europe UK LNG Bunkering Industry Revenue Share (%), by Others 2024 & 2032

- Figure 38: Europe UK LNG Bunkering Industry Revenue (Million), by Country 2024 & 2032

- Figure 39: Europe UK LNG Bunkering Industry Revenue Share (%), by Country 2024 & 2032

- Figure 40: Middle East & Africa UK LNG Bunkering Industry Revenue (Million), by Tanker Fleet 2024 & 2032

- Figure 41: Middle East & Africa UK LNG Bunkering Industry Revenue Share (%), by Tanker Fleet 2024 & 2032

- Figure 42: Middle East & Africa UK LNG Bunkering Industry Revenue (Million), by Container Fleet 2024 & 2032

- Figure 43: Middle East & Africa UK LNG Bunkering Industry Revenue Share (%), by Container Fleet 2024 & 2032

- Figure 44: Middle East & Africa UK LNG Bunkering Industry Revenue (Million), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 45: Middle East & Africa UK LNG Bunkering Industry Revenue Share (%), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 46: Middle East & Africa UK LNG Bunkering Industry Revenue (Million), by Ferries and OSV 2024 & 2032

- Figure 47: Middle East & Africa UK LNG Bunkering Industry Revenue Share (%), by Ferries and OSV 2024 & 2032

- Figure 48: Middle East & Africa UK LNG Bunkering Industry Revenue (Million), by Others 2024 & 2032

- Figure 49: Middle East & Africa UK LNG Bunkering Industry Revenue Share (%), by Others 2024 & 2032

- Figure 50: Middle East & Africa UK LNG Bunkering Industry Revenue (Million), by Country 2024 & 2032

- Figure 51: Middle East & Africa UK LNG Bunkering Industry Revenue Share (%), by Country 2024 & 2032

- Figure 52: Asia Pacific UK LNG Bunkering Industry Revenue (Million), by Tanker Fleet 2024 & 2032

- Figure 53: Asia Pacific UK LNG Bunkering Industry Revenue Share (%), by Tanker Fleet 2024 & 2032

- Figure 54: Asia Pacific UK LNG Bunkering Industry Revenue (Million), by Container Fleet 2024 & 2032

- Figure 55: Asia Pacific UK LNG Bunkering Industry Revenue Share (%), by Container Fleet 2024 & 2032

- Figure 56: Asia Pacific UK LNG Bunkering Industry Revenue (Million), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 57: Asia Pacific UK LNG Bunkering Industry Revenue Share (%), by Bulk and General Cargo Fleet 2024 & 2032

- Figure 58: Asia Pacific UK LNG Bunkering Industry Revenue (Million), by Ferries and OSV 2024 & 2032

- Figure 59: Asia Pacific UK LNG Bunkering Industry Revenue Share (%), by Ferries and OSV 2024 & 2032

- Figure 60: Asia Pacific UK LNG Bunkering Industry Revenue (Million), by Others 2024 & 2032

- Figure 61: Asia Pacific UK LNG Bunkering Industry Revenue Share (%), by Others 2024 & 2032

- Figure 62: Asia Pacific UK LNG Bunkering Industry Revenue (Million), by Country 2024 & 2032

- Figure 63: Asia Pacific UK LNG Bunkering Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global UK LNG Bunkering Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global UK LNG Bunkering Industry Revenue Million Forecast, by Tanker Fleet 2019 & 2032

- Table 3: Global UK LNG Bunkering Industry Revenue Million Forecast, by Container Fleet 2019 & 2032

- Table 4: Global UK LNG Bunkering Industry Revenue Million Forecast, by Bulk and General Cargo Fleet 2019 & 2032

- Table 5: Global UK LNG Bunkering Industry Revenue Million Forecast, by Ferries and OSV 2019 & 2032

- Table 6: Global UK LNG Bunkering Industry Revenue Million Forecast, by Others 2019 & 2032

- Table 7: Global UK LNG Bunkering Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Global UK LNG Bunkering Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Germany UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: France UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Italy UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United Kingdom UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Netherlands UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Europe UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global UK LNG Bunkering Industry Revenue Million Forecast, by Tanker Fleet 2019 & 2032

- Table 16: Global UK LNG Bunkering Industry Revenue Million Forecast, by Container Fleet 2019 & 2032

- Table 17: Global UK LNG Bunkering Industry Revenue Million Forecast, by Bulk and General Cargo Fleet 2019 & 2032

- Table 18: Global UK LNG Bunkering Industry Revenue Million Forecast, by Ferries and OSV 2019 & 2032

- Table 19: Global UK LNG Bunkering Industry Revenue Million Forecast, by Others 2019 & 2032

- Table 20: Global UK LNG Bunkering Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: United States UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Canada UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Mexico UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Global UK LNG Bunkering Industry Revenue Million Forecast, by Tanker Fleet 2019 & 2032

- Table 25: Global UK LNG Bunkering Industry Revenue Million Forecast, by Container Fleet 2019 & 2032

- Table 26: Global UK LNG Bunkering Industry Revenue Million Forecast, by Bulk and General Cargo Fleet 2019 & 2032

- Table 27: Global UK LNG Bunkering Industry Revenue Million Forecast, by Ferries and OSV 2019 & 2032

- Table 28: Global UK LNG Bunkering Industry Revenue Million Forecast, by Others 2019 & 2032

- Table 29: Global UK LNG Bunkering Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Brazil UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Argentina UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: Global UK LNG Bunkering Industry Revenue Million Forecast, by Tanker Fleet 2019 & 2032

- Table 34: Global UK LNG Bunkering Industry Revenue Million Forecast, by Container Fleet 2019 & 2032

- Table 35: Global UK LNG Bunkering Industry Revenue Million Forecast, by Bulk and General Cargo Fleet 2019 & 2032

- Table 36: Global UK LNG Bunkering Industry Revenue Million Forecast, by Ferries and OSV 2019 & 2032

- Table 37: Global UK LNG Bunkering Industry Revenue Million Forecast, by Others 2019 & 2032

- Table 38: Global UK LNG Bunkering Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 39: United Kingdom UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Germany UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: France UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Italy UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Spain UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Russia UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Benelux UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Nordics UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Europe UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Global UK LNG Bunkering Industry Revenue Million Forecast, by Tanker Fleet 2019 & 2032

- Table 49: Global UK LNG Bunkering Industry Revenue Million Forecast, by Container Fleet 2019 & 2032

- Table 50: Global UK LNG Bunkering Industry Revenue Million Forecast, by Bulk and General Cargo Fleet 2019 & 2032

- Table 51: Global UK LNG Bunkering Industry Revenue Million Forecast, by Ferries and OSV 2019 & 2032

- Table 52: Global UK LNG Bunkering Industry Revenue Million Forecast, by Others 2019 & 2032

- Table 53: Global UK LNG Bunkering Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 54: Turkey UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Israel UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: GCC UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 57: North Africa UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: South Africa UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: Rest of Middle East & Africa UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Global UK LNG Bunkering Industry Revenue Million Forecast, by Tanker Fleet 2019 & 2032

- Table 61: Global UK LNG Bunkering Industry Revenue Million Forecast, by Container Fleet 2019 & 2032

- Table 62: Global UK LNG Bunkering Industry Revenue Million Forecast, by Bulk and General Cargo Fleet 2019 & 2032

- Table 63: Global UK LNG Bunkering Industry Revenue Million Forecast, by Ferries and OSV 2019 & 2032

- Table 64: Global UK LNG Bunkering Industry Revenue Million Forecast, by Others 2019 & 2032

- Table 65: Global UK LNG Bunkering Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 66: China UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 67: India UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 68: Japan UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 69: South Korea UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 70: ASEAN UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 71: Oceania UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 72: Rest of Asia Pacific UK LNG Bunkering Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK LNG Bunkering Industry?

The projected CAGR is approximately > 2.10%.

2. Which companies are prominent players in the UK LNG Bunkering Industry?

Key companies in the market include Flogas Britain Ltd, Engie SA, Chevron corporation, TotalEngeries SE, Shell PLC*List Not Exhaustive.

3. What are the main segments of the UK LNG Bunkering Industry?

The market segments include Tanker Fleet, Container Fleet, Bulk and General Cargo Fleet, Ferries and OSV, Others.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increase in the Demand for Electricity4.; Rising Adoption of Electric Vehicles.

6. What are the notable trends driving market growth?

Ferries and OSV Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; New Sources of Distributed Electricity Generation.

8. Can you provide examples of recent developments in the market?

May 2022: Avenir LNG announced the delivery of the Avenir Achievement, the second 20,000 cbm dual-purpose LNG supply and bunkering vessel from the Nantong CIMC Sinopacific Offshore & Engineering.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK LNG Bunkering Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK LNG Bunkering Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK LNG Bunkering Industry?

To stay informed about further developments, trends, and reports in the UK LNG Bunkering Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence