Key Insights

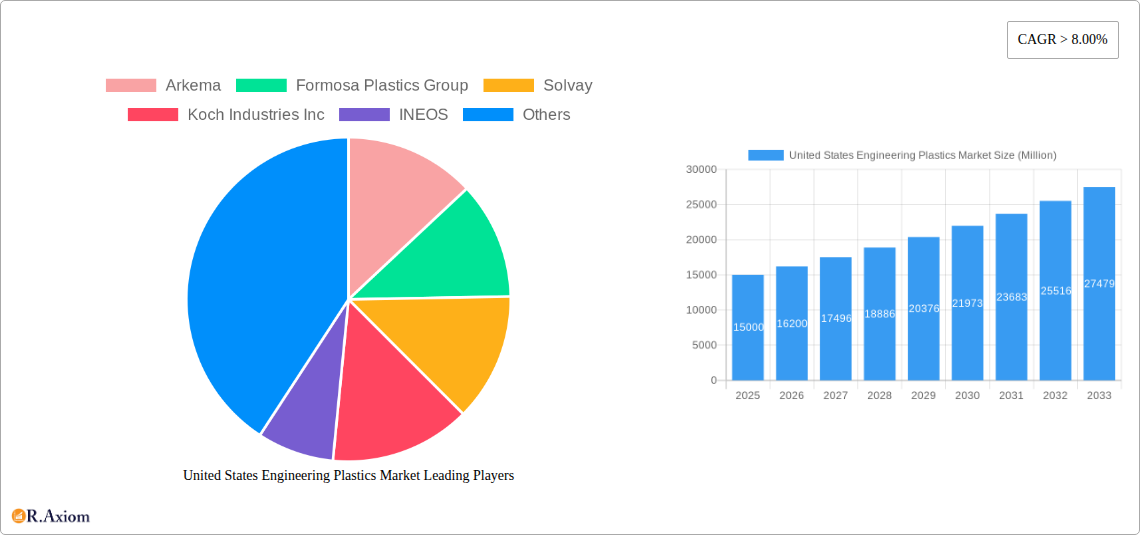

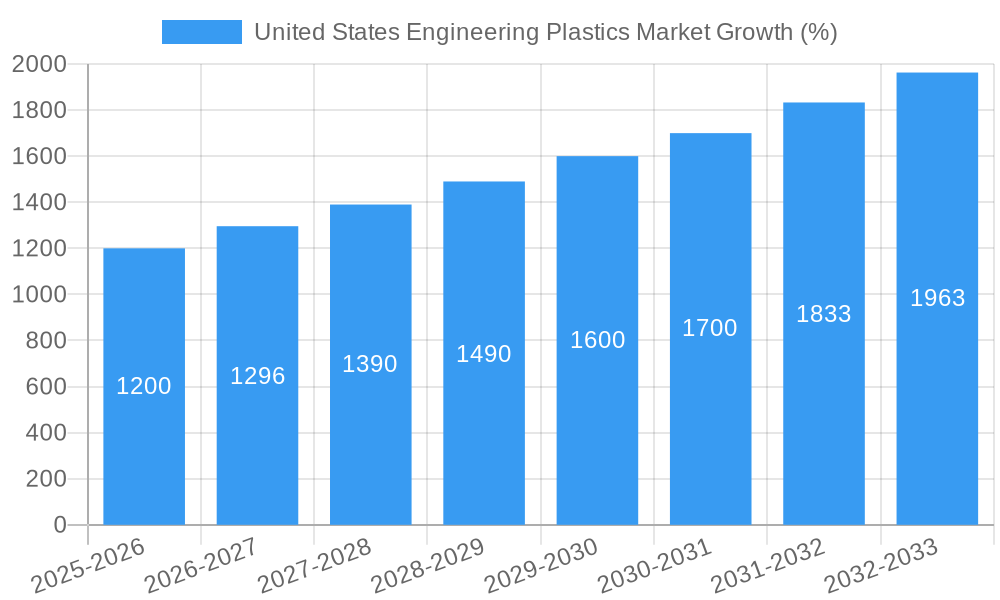

The United States engineering plastics market is experiencing robust growth, driven by increasing demand across diverse end-use sectors. The market, valued at approximately $15 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) exceeding 8% from 2025 to 2033. This expansion is fueled by several key factors. The automotive industry's shift towards lightweighting initiatives to improve fuel efficiency is a significant driver, increasing demand for high-performance engineering plastics like polyamides and polycarbonates. Similarly, the burgeoning electrical and electronics sector, particularly in renewable energy technologies and advanced electronics manufacturing, is contributing substantially to market growth. The building and construction industry's adoption of advanced materials for improved durability and energy efficiency is another key factor, with engineering plastics playing a crucial role in creating high-performance components. Furthermore, the aerospace industry's need for lightweight yet strong materials is driving demand for specialized engineering plastics such as PEEK and fluoropolymers. Growth is also being fueled by technological advancements leading to the development of new materials with enhanced properties such as improved thermal stability, chemical resistance, and mechanical strength.

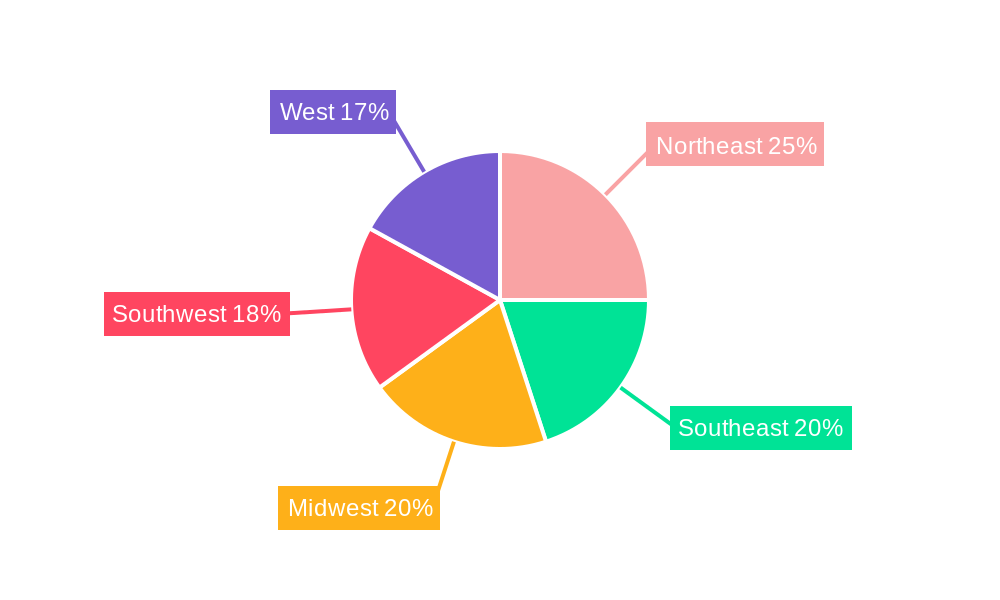

However, the market faces certain constraints. Fluctuations in raw material prices, particularly petroleum-based polymers, can impact production costs and profitability. Furthermore, the market's susceptibility to economic downturns, especially in sectors like automotive and construction, presents a potential risk. Nevertheless, the long-term outlook remains positive, with continued innovation and the growing preference for high-performance materials across diverse industries pointing towards sustained market expansion. The market segmentation reveals that fluoropolymers, polyamides, and polycarbonates are among the leading resin types driving growth, while the automotive, electrical and electronics, and building and construction sectors are significant end-use contributors. Regional analysis within the US indicates strong performance across all regions, reflecting widespread adoption across diverse industries.

United States Engineering Plastics Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the United States engineering plastics market, offering valuable insights for industry stakeholders, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with 2025 as the base year, this report meticulously examines market trends, growth drivers, challenges, and opportunities. The analysis encompasses various resin types, end-user industries, and leading market players, offering actionable intelligence for informed business strategies.

United States Engineering Plastics Market Market Concentration & Innovation

The United States engineering plastics market exhibits a moderately concentrated landscape, with several multinational corporations holding significant market share. Key players like Arkema, Formosa Plastics Group, Solvay, Koch Industries Inc, INEOS, Celanese Corporation, Indorama Ventures Public Company Limited, Ascend Performance Materials, BASF SE, SABIC, RTP Company, DuPont, Alfa S A B de C V, Covestro AG, and The Chemours Company contribute significantly to the overall market volume. The market share of these companies varies depending on the specific resin type and end-use industry. Recent M&A activities, such as Celanese Corporation's acquisition of DuPont's Mobility & Materials business, are reshaping the competitive landscape. Deal values for these transactions have reached hundreds of Millions of dollars, driving consolidation and influencing market dynamics. Innovation is driven by the increasing demand for high-performance materials with enhanced properties like lightweighting, durability, and sustainability. Regulatory frameworks, such as those focusing on environmental compliance and product safety, also play a crucial role in shaping market trends. Product substitution is a factor, with the emergence of bio-based and recycled engineering plastics challenging traditional materials. End-user trends toward lightweighting in automotive and aerospace applications and increased demand for electronics in consumer products are key drivers.

- Market Share: The top 5 players hold approximately xx% of the market share.

- M&A Activity: Recent deals have resulted in xx Million in value transferred in the last three years.

- Innovation Focus: Lightweighting, sustainability, enhanced performance.

- Regulatory Impact: Stringent environmental regulations are influencing material selection.

United States Engineering Plastics Market Industry Trends & Insights

The United States engineering plastics market is experiencing robust growth, driven by several key factors. The increasing demand from various end-use sectors, such as automotive, aerospace, and electronics, is a significant contributor. Technological advancements in materials science have led to the development of high-performance engineering plastics with improved properties, further fueling market expansion. Consumer preference for lightweight, durable, and sustainable products is also driving demand. The market is characterized by intense competition among established players and emerging companies, leading to continuous innovation and product differentiation. The market is expected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration in specific end-user segments like electric vehicles and renewable energy applications is experiencing rapid growth, further contributing to the overall market expansion. Technological disruptions, such as the development of additive manufacturing (3D printing) techniques for engineering plastics, are creating new opportunities and altering the production landscape. The competitive dynamics are primarily driven by pricing strategies, product innovation, and strategic partnerships.

Dominant Markets & Segments in United States Engineering Plastics Market

Within the United States engineering plastics market, the automotive and electrical & electronics sectors represent the most significant end-use industries. The dominance of these sectors is largely attributed to the high demand for lightweight, high-performance materials in vehicle manufacturing and the increasing complexity of electronic devices. Among resin types, Polybutylene Terephthalate (PBT), Polycarbonate (PC), and Polyamide are the leading segments, driven by their versatility, cost-effectiveness, and widespread applications.

- Key Drivers in Automotive Sector: Lightweighting regulations, electric vehicle adoption, increasing vehicle production.

- Key Drivers in Electrical & Electronics Sector: Miniaturization of devices, enhanced performance requirements, rising consumer electronics demand.

- Dominant Resin Types: PBT, PC, and Polyamide due to their versatile applications and cost-effectiveness.

The growth in these dominant segments is further fueled by several factors. The increasing demand for fuel-efficient vehicles in the automotive industry is leading to the adoption of lightweight engineering plastics. The rapid expansion of the electronics industry, with a focus on smaller, more efficient devices, drives demand for high-performance materials with superior electrical properties. Furthermore, the growing awareness of environmental concerns is leading to increased adoption of sustainable engineering plastics.

United States Engineering Plastics Market Product Developments

Recent product developments in the United States engineering plastics market highlight a strong focus on sustainability and enhanced performance. Companies are introducing bio-based alternatives, recycled materials, and plastics with improved thermal stability and chemical resistance. These innovations cater to the growing demand for environmentally friendly solutions and the need for materials capable of withstanding demanding operating conditions. The incorporation of nanomaterials and advanced fillers further enhances the properties of engineering plastics, improving their strength, stiffness, and other desirable characteristics. This leads to a better market fit across various applications.

Report Scope & Segmentation Analysis

This report segments the United States engineering plastics market based on resin type (Fluoropolymer, Polyphthalamide, PBT, PC, PEEK, PET, PI, PMMA, POM, ABS and SAN) and end-user industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, Other End-user Industries). Each segment is analyzed in terms of market size, growth projections, and competitive dynamics. The projected growth for each segment varies, reflecting the unique market drivers and challenges within each area. For instance, the aerospace segment is expected to exhibit a relatively higher growth rate driven by the increasing demand for lightweight and high-performance materials in aircraft manufacturing. In contrast, the building and construction segment might show moderate growth, influenced by the construction cycle and the adoption of advanced materials in this sector. The competitive dynamics differ across segments, with certain companies specializing in particular resin types or end-use applications.

Key Drivers of United States Engineering Plastics Market Growth

The growth of the United States engineering plastics market is fueled by several key drivers. The automotive industry's push for lightweight vehicles to improve fuel efficiency and reduce emissions is a significant driver. Technological advancements, such as the development of new polymer chemistries and improved processing techniques, are also contributing to market expansion. Government regulations promoting sustainability and the use of recycled materials are creating new opportunities for environmentally friendly engineering plastics. Finally, the ongoing expansion of the electronics and healthcare sectors, demanding high-performance materials, drives significant growth.

Challenges in the United States Engineering Plastics Market Sector

The United States engineering plastics market faces several challenges. Fluctuations in raw material prices and supply chain disruptions can impact production costs and market stability. Intense competition among manufacturers leads to price pressures and requires continuous innovation to maintain market share. Stringent environmental regulations and growing concerns about plastic waste pose challenges to producers, pushing them to develop sustainable alternatives. These factors, if not managed effectively, can constrain market growth. The impact of these factors can result in price increases of xx%, impacting affordability and potentially slowing market growth by xx%.

Emerging Opportunities in United States Engineering Plastics Market

Emerging opportunities in the United States engineering plastics market include the growing demand for sustainable and bio-based materials, the increasing use of engineering plastics in renewable energy applications, and the expanding use of additive manufacturing for customized plastic parts. These trends offer significant growth potential for companies able to adapt and innovate. The development of high-performance materials for specific applications, such as electric vehicle components and advanced medical devices, also presents substantial opportunities.

Leading Players in the United States Engineering Plastics Market Market

- Arkema

- Formosa Plastics Group

- Solvay

- Koch Industries Inc

- INEOS

- Celanese Corporation

- Indorama Ventures Public Company Limited

- Ascend Performance Materials

- BASF SE

- SABIC

- RTP Company

- DuPont

- Alfa S A B de C V

- Covestro AG

- The Chemours Company

Key Developments in United States Engineering Plastics Market Industry

- November 2022: Solvay and Orbia partnered to create the largest suspension-grade polyvinylidene fluoride (PVDF) production capacity in North America for battery materials. This significantly strengthens the supply chain for electric vehicle batteries.

- November 2022: Celanese Corporation acquired DuPont's Mobility & Materials business, expanding its engineered thermoplastics portfolio and market presence.

- February 2023: Covestro AG launched Makrolon 3638 polycarbonate for healthcare applications, showcasing innovation in specialized high-performance materials.

Strategic Outlook for United States Engineering Plastics Market Market

The future of the United States engineering plastics market appears promising, driven by continued growth in key end-use sectors, technological advancements, and a growing focus on sustainability. Opportunities exist in developing innovative solutions for electric vehicles, renewable energy, and healthcare applications. Companies that prioritize sustainability, invest in R&D, and adapt to evolving consumer preferences are well-positioned for success in this dynamic market. The market is poised for continued expansion, driven by a combination of factors such as technological innovation, growing end-use demand, and a shift towards sustainable practices.

United States Engineering Plastics Market Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Electrical and Electronics

- 1.5. Industrial and Machinery

- 1.6. Packaging

- 1.7. Other End-user Industries

-

2. Resin Type

-

2.1. Fluoropolymer

-

2.1.1. By Sub Resin Type

- 2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 2.1.1.3. Polytetrafluoroethylene (PTFE)

- 2.1.1.4. Polyvinylfluoride (PVF)

- 2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 2.1.1.6. Other Sub Resin Types

-

2.1.1. By Sub Resin Type

- 2.2. Liquid Crystal Polymer (LCP)

-

2.3. Polyamide (PA)

- 2.3.1. Aramid

- 2.3.2. Polyamide (PA) 6

- 2.3.3. Polyamide (PA) 66

- 2.3.4. Polyphthalamide

- 2.4. Polybutylene Terephthalate (PBT)

- 2.5. Polycarbonate (PC)

- 2.6. Polyether Ether Ketone (PEEK)

- 2.7. Polyethylene Terephthalate (PET)

- 2.8. Polyimide (PI)

- 2.9. Polymethyl Methacrylate (PMMA)

- 2.10. Polyoxymethylene (POM)

- 2.11. Styrene Copolymers (ABS and SAN)

-

2.1. Fluoropolymer

United States Engineering Plastics Market Segmentation By Geography

- 1. United States

United States Engineering Plastics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 8.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Low-pressure Membrane Technologies; Other Drivers

- 3.3. Market Restrains

- 3.3.1. Poor Fouling Resistance of Nano porous Membranes; Other Restraints

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United States Engineering Plastics Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Electrical and Electronics

- 5.1.5. Industrial and Machinery

- 5.1.6. Packaging

- 5.1.7. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Resin Type

- 5.2.1. Fluoropolymer

- 5.2.1.1. By Sub Resin Type

- 5.2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3. Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4. Polyvinylfluoride (PVF)

- 5.2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6. Other Sub Resin Types

- 5.2.1.1. By Sub Resin Type

- 5.2.2. Liquid Crystal Polymer (LCP)

- 5.2.3. Polyamide (PA)

- 5.2.3.1. Aramid

- 5.2.3.2. Polyamide (PA) 6

- 5.2.3.3. Polyamide (PA) 66

- 5.2.3.4. Polyphthalamide

- 5.2.4. Polybutylene Terephthalate (PBT)

- 5.2.5. Polycarbonate (PC)

- 5.2.6. Polyether Ether Ketone (PEEK)

- 5.2.7. Polyethylene Terephthalate (PET)

- 5.2.8. Polyimide (PI)

- 5.2.9. Polymethyl Methacrylate (PMMA)

- 5.2.10. Polyoxymethylene (POM)

- 5.2.11. Styrene Copolymers (ABS and SAN)

- 5.2.1. Fluoropolymer

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Northeast United States Engineering Plastics Market Analysis, Insights and Forecast, 2019-2031

- 7. Southeast United States Engineering Plastics Market Analysis, Insights and Forecast, 2019-2031

- 8. Midwest United States Engineering Plastics Market Analysis, Insights and Forecast, 2019-2031

- 9. Southwest United States Engineering Plastics Market Analysis, Insights and Forecast, 2019-2031

- 10. West United States Engineering Plastics Market Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Arkema

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Formosa Plastics Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Solvay

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Koch Industries Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 INEOS

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Celanese Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Indorama Ventures Public Company Limited

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Ascend Performance Materials

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 BASF SE

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 SABIC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 RTP Company

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 DuPont

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Alfa S A B de C V

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Covestro AG

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 The Chemours Compan

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Arkema

List of Figures

- Figure 1: United States Engineering Plastics Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: United States Engineering Plastics Market Share (%) by Company 2024

List of Tables

- Table 1: United States Engineering Plastics Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: United States Engineering Plastics Market Volume K Tons Forecast, by Region 2019 & 2032

- Table 3: United States Engineering Plastics Market Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 4: United States Engineering Plastics Market Volume K Tons Forecast, by End User Industry 2019 & 2032

- Table 5: United States Engineering Plastics Market Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 6: United States Engineering Plastics Market Volume K Tons Forecast, by Resin Type 2019 & 2032

- Table 7: United States Engineering Plastics Market Revenue Million Forecast, by Region 2019 & 2032

- Table 8: United States Engineering Plastics Market Volume K Tons Forecast, by Region 2019 & 2032

- Table 9: United States Engineering Plastics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: United States Engineering Plastics Market Volume K Tons Forecast, by Country 2019 & 2032

- Table 11: Northeast United States Engineering Plastics Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Northeast United States Engineering Plastics Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 13: Southeast United States Engineering Plastics Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Southeast United States Engineering Plastics Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 15: Midwest United States Engineering Plastics Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Midwest United States Engineering Plastics Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 17: Southwest United States Engineering Plastics Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Southwest United States Engineering Plastics Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 19: West United States Engineering Plastics Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: West United States Engineering Plastics Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 21: United States Engineering Plastics Market Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 22: United States Engineering Plastics Market Volume K Tons Forecast, by End User Industry 2019 & 2032

- Table 23: United States Engineering Plastics Market Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 24: United States Engineering Plastics Market Volume K Tons Forecast, by Resin Type 2019 & 2032

- Table 25: United States Engineering Plastics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: United States Engineering Plastics Market Volume K Tons Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Engineering Plastics Market?

The projected CAGR is approximately > 8.00%.

2. Which companies are prominent players in the United States Engineering Plastics Market?

Key companies in the market include Arkema, Formosa Plastics Group, Solvay, Koch Industries Inc, INEOS, Celanese Corporation, Indorama Ventures Public Company Limited, Ascend Performance Materials, BASF SE, SABIC, RTP Company, DuPont, Alfa S A B de C V, Covestro AG, The Chemours Compan.

3. What are the main segments of the United States Engineering Plastics Market?

The market segments include End User Industry, Resin Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Low-pressure Membrane Technologies; Other Drivers.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Poor Fouling Resistance of Nano porous Membranes; Other Restraints.

8. Can you provide examples of recent developments in the market?

February 2023: Covestro AG introduced Makrolon 3638 polycarbonate for healthcare and life sciences applications such as drug delivery devices, wellness and wearable devices, and single-use containers for biopharmaceutical manufacturing.November 2022: Solvay and Orbia announced a framework agreement to form a partnership for the production of suspension-grade polyvinylidene fluoride (PVDF) for battery materials, resulting in the largest capacity in North America.November 2022: Celanese Corporation completed the acquisition of the Mobility & Materials (“M&M”) business of DuPont. This acquisition enhanced the company's product portfolio of engineered thermoplastics through the addition of well-recognized brands and intellectual properties of DuPont.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Engineering Plastics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Engineering Plastics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Engineering Plastics Market?

To stay informed about further developments, trends, and reports in the United States Engineering Plastics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence