Key Insights

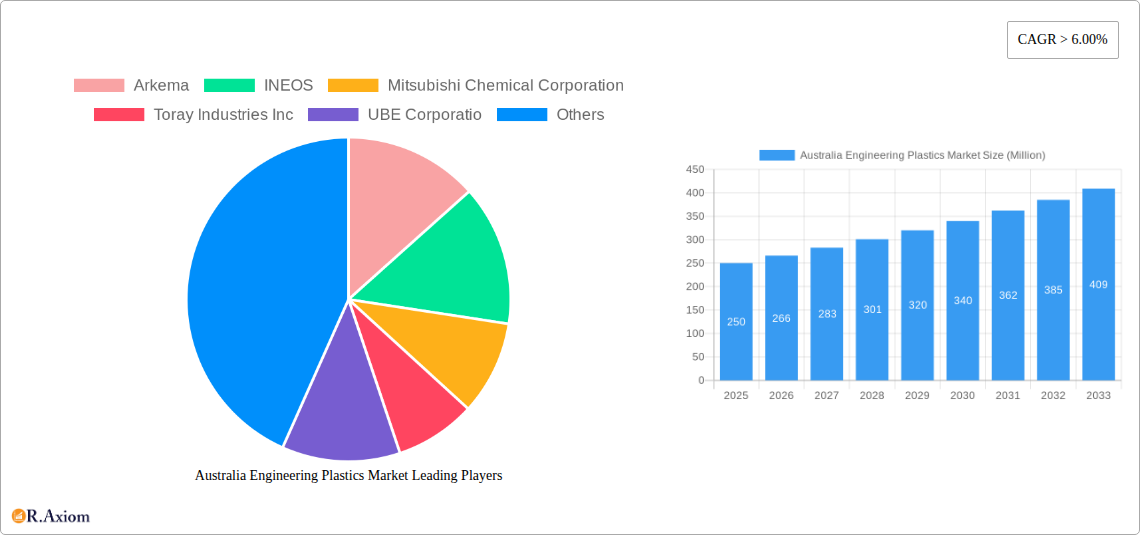

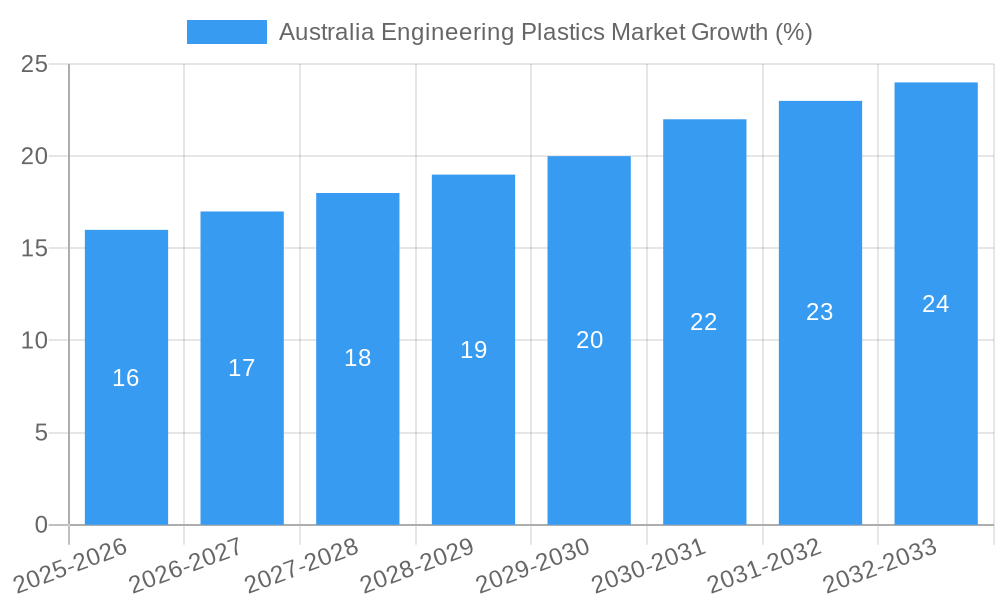

The Australian engineering plastics market, valued at approximately $XXX million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 6% from 2025 to 2033. This expansion is driven by several key factors. The burgeoning automotive industry, characterized by increased demand for lightweight and high-performance vehicles, is a significant contributor. Similarly, the building and construction sector's adoption of innovative materials for improved durability and energy efficiency fuels market growth. Furthermore, advancements in electrical and electronics manufacturing, particularly in areas like renewable energy and automation, are creating significant demand for specialized engineering plastics. The increasing preference for sustainable and recyclable materials is also shaping market trends, prompting manufacturers to develop and utilize environmentally friendly alternatives. Key resin types driving demand include polybutylene terephthalate (PBT), polycarbonate (PC), polyether ether ketone (PEEK), and polyimide (PI), reflecting the diverse application requirements across various end-user industries. Competition among established players such as Arkema, INEOS, Mitsubishi Chemical Corporation, and Toray Industries Inc., alongside regional players, is further intensifying innovation and driving down costs, benefiting end-users.

While the market presents significant opportunities, certain challenges exist. Fluctuations in raw material prices and potential supply chain disruptions pose ongoing risks. Furthermore, the regulatory landscape surrounding the use of certain plastics and the increasing emphasis on sustainability could necessitate adjustments in manufacturing processes and material choices. However, given the continuous advancements in material science and the growing demand for high-performance plastics across various sectors, the overall outlook for the Australian engineering plastics market remains positive throughout the forecast period, with particular emphasis on the aerospace, automotive, and electronics segments. The market is expected to see continuous innovation in material properties leading to better solutions for diverse applications, potentially driving even faster growth.

Australia Engineering Plastics Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Australia engineering plastics market, covering the period from 2019 to 2033. It offers valuable insights into market dynamics, growth drivers, challenges, and future opportunities, making it an essential resource for industry stakeholders, investors, and strategic decision-makers. The report leverages extensive market research and data analysis to deliver actionable intelligence for informed business strategies.

Australia Engineering Plastics Market Market Concentration & Innovation

The Australian engineering plastics market exhibits a moderately concentrated landscape, with a few major global players holding significant market share. Arkema, INEOS, Mitsubishi Chemical Corporation, Toray Industries Inc, UBE Corporation, LANXESS, BASF SE, SABIC, The Chemours Company, and Covestro AG are key participants, driving innovation and shaping market dynamics. Market share estimations for 2024 suggest BASF SE holds approximately xx% market share, followed by SABIC at xx%, and Covestro AG at xx%. The remaining market share is distributed among other players.

Innovation is a key driver, fueled by the demand for high-performance materials with enhanced properties. Stringent regulatory frameworks focusing on sustainability and environmental impact are also shaping the market. Product substitution, driven by advancements in bio-based and recycled plastics, is a notable trend. The market also witnesses continuous mergers and acquisitions (M&A) activity, with deal values exceeding xx Million AUD in the past five years. End-user trends, particularly in the automotive and aerospace sectors, demand lightweight, durable, and high-performance materials, influencing product development and market growth.

- Key Metrics: Market share (2024 estimates: BASF SE - xx%, SABIC - xx%, Covestro AG - xx%), M&A deal values (AUD xx Million over the past 5 years).

- Innovation Drivers: Demand for high-performance materials, sustainability regulations, product substitution with bio-based plastics.

- Competitive Dynamics: M&A activity, strategic partnerships, technological advancements.

Australia Engineering Plastics Market Industry Trends & Insights

The Australian engineering plastics market is experiencing robust growth, driven by increasing demand from various end-user industries. The automotive sector's shift towards lightweight vehicles and the expanding construction and infrastructure projects are major growth catalysts. Technological disruptions, including advancements in additive manufacturing (3D printing) and the development of sustainable materials, are reshaping the market landscape. Consumer preferences for eco-friendly and sustainable products are influencing product development and market trends. Competitive dynamics are characterized by innovation, strategic partnerships, and M&A activity. The market is projected to register a CAGR of xx% during the forecast period (2025-2033), with significant market penetration expected in the automotive and building & construction sectors. The overall market size is anticipated to reach xx Million AUD by 2033. This growth is further fueled by government initiatives promoting sustainable materials and infrastructure development.

Dominant Markets & Segments in Australia Engineering Plastics Market

Within the Australian engineering plastics market, the automotive and building & construction sectors are dominant end-user industries. The high demand for lightweight, durable, and high-performance materials in automobiles and the growing infrastructure development projects drive significant market growth in these sectors. Among resin types, Polybutylene Terephthalate (PBT) and Polycarbonate (PC) are currently leading segments.

- Key Drivers for Automotive: Lightweighting initiatives, increased vehicle production, stringent emission regulations.

- Key Drivers for Building & Construction: Infrastructure development, growing construction activity, demand for durable and high-performance materials.

- Key Drivers for PBT & PC: Superior properties, wide range of applications, cost-effectiveness.

The dominance of these sectors and resin types is attributed to various factors, including favorable economic policies, robust infrastructure development, and technological advancements. Specific government initiatives focusing on sustainable building practices and advancements in automotive technology are further strengthening the market position of these segments. However, other segments like aerospace, electrical & electronics, and packaging also show notable growth potential.

Australia Engineering Plastics Market Product Developments

Recent product innovations in the Australian engineering plastics market showcase a strong focus on sustainability and enhanced performance. Companies are increasingly introducing bio-based and recycled plastics, along with materials featuring improved thermal stability, impact resistance, and chemical resistance. These developments cater to growing demands for eco-friendly solutions and enhanced functionality in various applications. For example, the introduction of sustainable polyamide resin by LANXESS demonstrates a shift towards environmentally conscious materials. This trend of developing innovative sustainable products is expected to continue to shape market competition and drive demand.

Report Scope & Segmentation Analysis

This report segments the Australian engineering plastics market by both end-user industry and resin type, offering a granular view of market dynamics across various sub-segments. The end-user segments include Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-user Industries. Resin types covered are Fluoropolymer, Polyphthalamide, Polybutylene Terephthalate (PBT), Polycarbonate (PC), Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), Polyimide (PI), Polymethyl Methacrylate (PMMA), Polyoxymethylene (POM), and Styrene Copolymers (ABS and SAN). Each segment's analysis includes market size estimations, growth projections, and competitive dynamics, providing a comprehensive market overview.

Key Drivers of Australia Engineering Plastics Market Growth

The growth of the Australian engineering plastics market is primarily driven by several factors. Firstly, the booming automotive industry with its focus on lightweighting and improved fuel efficiency is a significant driver. Secondly, substantial government investment in infrastructure projects, coupled with rising construction activities, fuels demand for high-performance building materials. Finally, technological advancements in materials science, leading to the development of high-performance plastics with enhanced properties, contribute significantly to market expansion.

Challenges in the Australia Engineering Plastics Market Sector

The Australian engineering plastics market faces several challenges. Fluctuations in raw material prices, particularly oil-based feedstocks, impact production costs and profitability. Furthermore, increasing environmental regulations related to plastic waste management require companies to adopt sustainable practices, potentially increasing costs. Intense competition from both domestic and international players also adds pressure on margins. These factors can potentially hinder market growth if not addressed proactively.

Emerging Opportunities in Australia Engineering Plastics Market

Emerging opportunities lie in the growing demand for sustainable and bio-based engineering plastics. The increasing focus on reducing carbon footprints across various industries presents a significant market for eco-friendly materials. Advancements in 3D printing technology also open new avenues for customized plastic parts and innovative designs. Furthermore, exploring new applications for high-performance engineering plastics in emerging sectors such as renewable energy and medical devices holds considerable potential.

Leading Players in the Australia Engineering Plastics Market Market

- Arkema

- INEOS

- Mitsubishi Chemical Corporation

- Toray Industries Inc

- UBE Corporation

- LANXESS

- BASF SE

- SABIC

- The Chemours Company

- Covestro AG

Key Developments in Australia Engineering Plastics Market Industry

- September 2022: LANXESS introduced Durethan ECO, a sustainable polyamide resin using recycled glass fibers.

- October 2022: BASF SE launched Ultraform LowPCF and Ultraform BMB, sustainable POM products with reduced carbon footprints.

- February 2023: Covestro AG introduced Makrolon 3638 polycarbonate for healthcare and life science applications.

Strategic Outlook for Australia Engineering Plastics Market Market

The Australian engineering plastics market is poised for continued growth, driven by increasing demand from key end-user sectors and a strong focus on innovation and sustainability. The development of advanced materials with enhanced properties, coupled with the growing adoption of sustainable manufacturing practices, will shape the market's future trajectory. Opportunities exist in exploring new applications, expanding into emerging sectors, and leveraging technological advancements for sustained growth and market leadership.

Australia Engineering Plastics Market Segmentation

-

1. End User Industry

- 1.1. Aerospace

- 1.2. Automotive

- 1.3. Building and Construction

- 1.4. Electrical and Electronics

- 1.5. Industrial and Machinery

- 1.6. Packaging

- 1.7. Other End-user Industries

-

2. Resin Type

-

2.1. Fluoropolymer

-

2.1.1. By Sub Resin Type

- 2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 2.1.1.3. Polytetrafluoroethylene (PTFE)

- 2.1.1.4. Polyvinylfluoride (PVF)

- 2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 2.1.1.6. Other Sub Resin Types

-

2.1.1. By Sub Resin Type

- 2.2. Liquid Crystal Polymer (LCP)

-

2.3. Polyamide (PA)

- 2.3.1. Aramid

- 2.3.2. Polyamide (PA) 6

- 2.3.3. Polyamide (PA) 66

- 2.3.4. Polyphthalamide

- 2.4. Polybutylene Terephthalate (PBT)

- 2.5. Polycarbonate (PC)

- 2.6. Polyether Ether Ketone (PEEK)

- 2.7. Polyethylene Terephthalate (PET)

- 2.8. Polyimide (PI)

- 2.9. Polymethyl Methacrylate (PMMA)

- 2.10. Polyoxymethylene (POM)

- 2.11. Styrene Copolymers (ABS and SAN)

-

2.1. Fluoropolymer

Australia Engineering Plastics Market Segmentation By Geography

- 1. Australia

Australia Engineering Plastics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 6.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Usage in Sealing Applications; Surging Applications in the Automotive Industry

- 3.3. Market Restrains

- 3.3.1. Increasingly Stringent Environmental Regulations and Hazardous Working Conditions; Other Restraints

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Engineering Plastics Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Aerospace

- 5.1.2. Automotive

- 5.1.3. Building and Construction

- 5.1.4. Electrical and Electronics

- 5.1.5. Industrial and Machinery

- 5.1.6. Packaging

- 5.1.7. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Resin Type

- 5.2.1. Fluoropolymer

- 5.2.1.1. By Sub Resin Type

- 5.2.1.1.1. Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2. Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3. Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4. Polyvinylfluoride (PVF)

- 5.2.1.1.5. Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6. Other Sub Resin Types

- 5.2.1.1. By Sub Resin Type

- 5.2.2. Liquid Crystal Polymer (LCP)

- 5.2.3. Polyamide (PA)

- 5.2.3.1. Aramid

- 5.2.3.2. Polyamide (PA) 6

- 5.2.3.3. Polyamide (PA) 66

- 5.2.3.4. Polyphthalamide

- 5.2.4. Polybutylene Terephthalate (PBT)

- 5.2.5. Polycarbonate (PC)

- 5.2.6. Polyether Ether Ketone (PEEK)

- 5.2.7. Polyethylene Terephthalate (PET)

- 5.2.8. Polyimide (PI)

- 5.2.9. Polymethyl Methacrylate (PMMA)

- 5.2.10. Polyoxymethylene (POM)

- 5.2.11. Styrene Copolymers (ABS and SAN)

- 5.2.1. Fluoropolymer

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Arkema

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 INEOS

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Mitsubishi Chemical Corporation

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Toray Industries Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 UBE Corporatio

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 LANXESS

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 BASF SE

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 SABIC

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 The Chemours Company

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Covestro AG

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Arkema

List of Figures

- Figure 1: Australia Engineering Plastics Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Australia Engineering Plastics Market Share (%) by Company 2024

List of Tables

- Table 1: Australia Engineering Plastics Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Australia Engineering Plastics Market Volume kilotons Forecast, by Region 2019 & 2032

- Table 3: Australia Engineering Plastics Market Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 4: Australia Engineering Plastics Market Volume kilotons Forecast, by End User Industry 2019 & 2032

- Table 5: Australia Engineering Plastics Market Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 6: Australia Engineering Plastics Market Volume kilotons Forecast, by Resin Type 2019 & 2032

- Table 7: Australia Engineering Plastics Market Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Australia Engineering Plastics Market Volume kilotons Forecast, by Region 2019 & 2032

- Table 9: Australia Engineering Plastics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Australia Engineering Plastics Market Volume kilotons Forecast, by Country 2019 & 2032

- Table 11: Australia Engineering Plastics Market Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 12: Australia Engineering Plastics Market Volume kilotons Forecast, by End User Industry 2019 & 2032

- Table 13: Australia Engineering Plastics Market Revenue Million Forecast, by Resin Type 2019 & 2032

- Table 14: Australia Engineering Plastics Market Volume kilotons Forecast, by Resin Type 2019 & 2032

- Table 15: Australia Engineering Plastics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Australia Engineering Plastics Market Volume kilotons Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Engineering Plastics Market?

The projected CAGR is approximately > 6.00%.

2. Which companies are prominent players in the Australia Engineering Plastics Market?

Key companies in the market include Arkema, INEOS, Mitsubishi Chemical Corporation, Toray Industries Inc, UBE Corporatio, LANXESS, BASF SE, SABIC, The Chemours Company, Covestro AG.

3. What are the main segments of the Australia Engineering Plastics Market?

The market segments include End User Industry, Resin Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Usage in Sealing Applications; Surging Applications in the Automotive Industry.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Increasingly Stringent Environmental Regulations and Hazardous Working Conditions; Other Restraints.

8. Can you provide examples of recent developments in the market?

February 2023: Covestro AG introduced Makrolon 3638 polycarbonate for healthcare and life sciences applications such as drug delivery devices, wellness and wearable devices, and single-use containers for biopharmaceutical manufacturing.October 2022: BASF SE introduced two new sustainable POM products, Ultraform LowPCF (Low Product Carbon Footprint) and Ultraform BMB (Biomass Balance), to reduce the carbon footprint, save fossil resources, and support the reduction of greenhouse gas (GHG) emissions.September 2022: LANXESS introduced a sustainable polyamide resin, Durethan ECO, which consists of recycled fibers made from waste glass to reduce its carbon footprint.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in kilotons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Engineering Plastics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Engineering Plastics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Engineering Plastics Market?

To stay informed about further developments, trends, and reports in the Australia Engineering Plastics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence