Key Insights

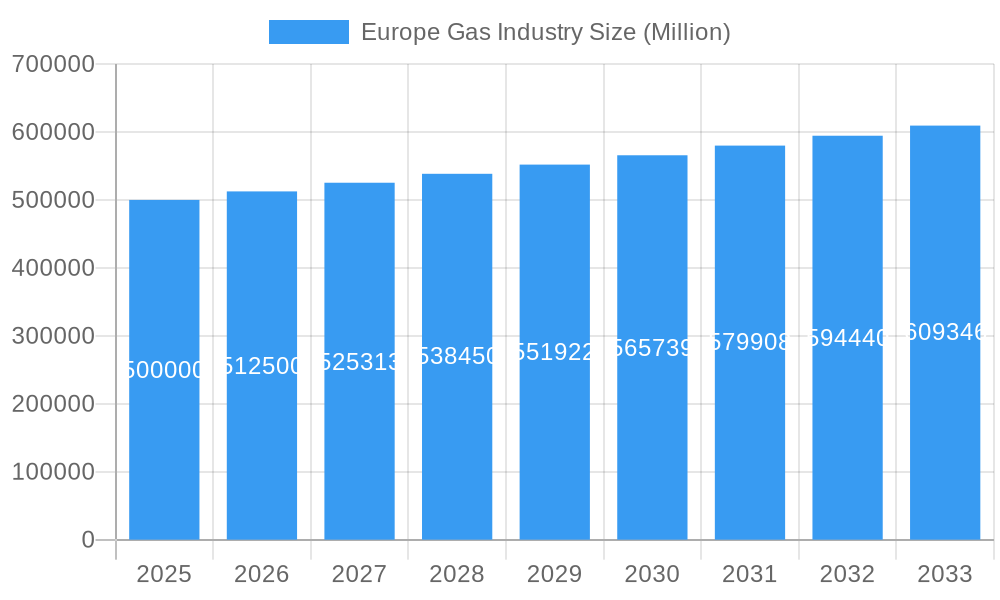

The European Gas Industry is poised for significant expansion, driven by a Compound Annual Growth Rate (CAGR) of 4.5%. The market size is projected to reach €1223.8 million by 2024. Key growth catalysts include escalating industrial activity, increased energy consumption from a growing population, and the strategic shift towards a lower-carbon energy framework. This transition, while essential for environmental goals, introduces complexities such as the need for stable gas supply to complement the intermittent nature of renewable energy sources, highlighting the critical balance between energy security and sustainability. Geopolitical factors and evolving energy infrastructure regulations also pose significant market restraints. The industry segments into upstream (exploration and production), midstream (transportation and storage), and downstream (distribution and retail). Leading global entities such as Chevron, BP, TotalEnergies, ExxonMobil, and Equinor, alongside numerous national and regional operators, shape the competitive environment. The forecast period, from 2024 to 2033, anticipates continued, albeit potentially tempered, growth as the industry harmonizes energy security imperatives with ambitious sustainability objectives.

Europe Gas Industry Market Size (In Billion)

The competitive arena is marked by strategic consolidation and diversification. While major international corporations retain substantial market influence, specialized firms focusing on renewable gas production and advanced distribution technologies are gaining traction. Significant regional disparities exist across Europe, with varying levels of gas production, import reliance, and commitment to renewable energy alternatives. Future market trajectory will be heavily influenced by effective policy frameworks supporting both gas infrastructure modernization and the advancement of cleaner energy solutions. Prioritizing energy security, expediting regulatory processes, and bolstering gas storage capabilities will be paramount for optimizing market performance in the upcoming years.

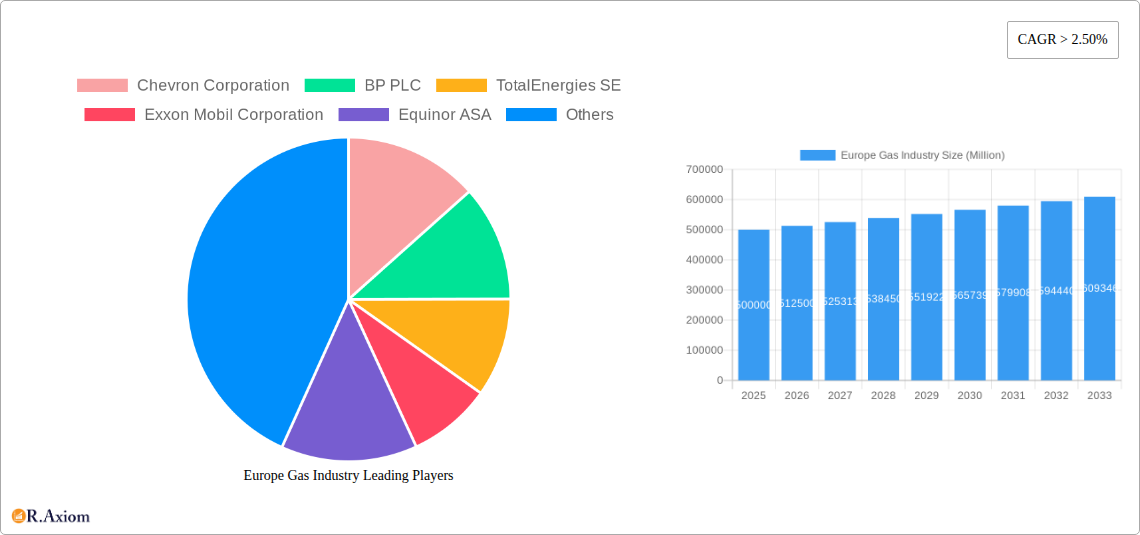

Europe Gas Industry Company Market Share

Europe Gas Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the Europe gas industry, covering market trends, competitive dynamics, and future growth prospects from 2019 to 2033. The study period encompasses historical data (2019-2024), the base year (2025), and a detailed forecast (2025-2033). Key market players, including Chevron Corporation, BP PLC, TotalEnergies SE, Exxon Mobil Corporation, Equinor ASA, NK Lukoil PAO, Gazprom PJSC ADR, and Rosneft Oil Co PJSC (list not exhaustive), are analyzed in detail. This report is crucial for industry stakeholders, investors, and strategic decision-makers seeking actionable insights into this dynamic market.

Europe Gas Industry Market Concentration & Innovation

This section analyzes the market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and M&A activities within the European gas industry. We examine market share distribution amongst major players and delve into the value and impact of significant mergers and acquisitions.

Market Concentration: The European gas market exhibits a moderately concentrated structure, with a few dominant players holding significant market share. XX% of the market is controlled by the top 5 players in 2025, a figure projected to slightly decrease to XX% by 2033 due to increased competition and regulatory changes.

Innovation Drivers: Innovation is driven by the need for enhanced energy efficiency, reduced carbon emissions, and the exploration of alternative gas sources, including biomethane and hydrogen blending. Investment in smart metering and grid modernization is also a significant driver.

Regulatory Frameworks: Stringent environmental regulations and policies aimed at reducing greenhouse gas emissions are shaping the industry landscape. The EU's climate targets are heavily influencing investment decisions and technological advancements within the sector.

Product Substitutes: Growing competition from renewable energy sources, such as wind and solar power, poses a significant challenge. The increasing adoption of electric vehicles is also impacting natural gas demand in the transportation sector.

End-User Trends: Industrial users account for the largest share of natural gas consumption, followed by residential and power generation sectors. Shifts in industrial processes and government incentives for energy efficiency are altering consumption patterns.

M&A Activities: The past five years have seen significant M&A activity within the European gas industry, with deal values exceeding xx Million in 2024. These transactions reflect efforts by major players to consolidate market share, access new technologies, and expand their geographical reach.

Europe Gas Industry Industry Trends & Insights

This section explores key industry trends impacting the European gas market, including growth drivers, technological disruptions, evolving consumer preferences, and competitive dynamics. We analyze market growth using compound annual growth rate (CAGR) and delve into market penetration rates for specific technologies and services.

The European gas market experienced a CAGR of XX% during the historical period (2019-2024) and is projected to maintain a CAGR of XX% during the forecast period (2025-2033). This growth is fueled by increasing energy demand, particularly in the industrial sector, despite the growth of renewable energy sources. However, the transition towards renewable energy is expected to influence consumption patterns, leading to a slowing of overall gas market growth and increasing pressure on profitability. Technological advancements, such as improved extraction techniques and pipeline infrastructure upgrades, are driving efficiency gains. Consumer preferences are shifting towards cleaner energy options, creating both opportunities and challenges for gas companies. The competitive landscape is intensifying with the entrance of new players and the expansion of existing ones, leading to price competition and increased focus on innovation and sustainability. The market penetration of smart metering technologies is increasing steadily, reaching XX% by 2025. This facilitates better energy management and grid optimization.

Dominant Markets & Segments in Europe Gas Industry

This section pinpoints the leading region, country, or segment within the European gas industry, providing detailed dominance analysis using bullet points for key drivers and paragraphs for in-depth insights.

Germany holds the largest market share, driven primarily by its robust industrial base and extensive gas infrastructure.

- Key Drivers for Germany's Dominance:

- Large industrial sector with high energy demand.

- Well-established pipeline network connecting to various gas sources.

- Government policies supporting gas infrastructure development (though shifting towards renewables).

- Strategic location as a major transit hub for gas imports.

The UK and France also represent substantial markets within Europe, demonstrating a strong reliance on natural gas across diverse segments, particularly in power generation and industrial manufacturing. However, both countries are increasingly focusing on diversifying their energy portfolios, leading to a decrease in gas reliance compared to Germany.

Europe Gas Industry Product Developments

Recent product innovations focus on improving efficiency and reducing environmental impact. Advancements in gas processing technologies lead to cleaner gas and the development of hydrogen blending capabilities, promoting a transition towards a lower-carbon energy system. The increased adoption of smart gas meters enhances energy management and facilitates real-time monitoring of consumption, while investment in digital infrastructure is improving grid performance. This innovation is crucial for maintaining the competitiveness of gas in the face of increasing pressure from renewables.

Report Scope & Segmentation Analysis

This report segments the European gas market based on multiple factors. The segments considered are: By Gas Type (Natural Gas, Biomethane, Liquefied Petroleum Gas (LPG)), By Application (Residential, Commercial, Industrial, Power Generation, Transportation), and By Country (Germany, UK, France, Italy, Spain, Poland, and other European Countries). Each segment's growth projection, market size, and competitive dynamics are specifically analyzed. Growth projections vary depending on the segment. For example, the biomethane segment is anticipated to experience the highest growth due to increasing regulatory mandates and incentives for renewable energy sources. The industrial segment remains the largest consumer, yet its growth rate is slowing due to efficiency improvements and renewable energy integration within industrial processes. The competitive intensity varies across the segments, with a few dominant players in the larger segments and higher competition in the niche segments such as biomethane.

Key Drivers of Europe Gas Industry Growth

Key growth drivers in the European gas industry include increasing energy demand from industrial and residential sectors, the development of robust pipeline infrastructure, and government incentives to support the sector. Technological advancements in gas extraction, processing, and distribution also contribute to efficiency gains and market expansion. The transition towards a lower-carbon energy system is encouraging the utilization of alternative gas sources like biomethane, creating opportunities for new technologies and market participants.

Challenges in the Europe Gas Industry Sector

The European gas industry faces significant challenges, including fluctuating gas prices driven by global supply chain issues and geopolitical instability. Stricter environmental regulations are increasing compliance costs and are driving the need for innovative solutions. Competition from renewable energy sources and the increasing push for energy independence are significantly impacting the long-term growth outlook for the industry. These factors are significantly affecting profitability and investment decisions.

Emerging Opportunities in Europe Gas Industry

The European gas industry presents opportunities in areas such as the growth of biomethane and other renewable gas sources. Technological innovations in gas storage and transportation enhance energy security. Investment in green gas infrastructure, such as carbon capture, utilization, and storage (CCUS) technologies, offers significant growth potential. Expanding into new markets and developing innovative business models contribute to the industry's sustained growth and adaptation to the changing energy landscape.

Leading Players in the Europe Gas Industry Market

- Chevron Corporation

- BP PLC

- TotalEnergies SE

- Exxon Mobil Corporation

- Equinor ASA

- NK Lukoil PAO

- Gazprom PJSC ADR

- Rosneft Oil Co PJSC

Key Developments in Europe Gas Industry Industry

September 2022: Russia's Gazprom announced shipping 42.4 Million cubic meters (mcm) of natural gas to Europe via Ukraine. This action demonstrated Russia's strategy to reduce its reliance on the US dollar and exert geopolitical influence on the European gas market. This had a short-term impact on gas prices and heightened concerns about energy security for several European nations.

September 2022: The inauguration of the Baltic Pipe at Goleniów, Poland, marked the completion of a significant infrastructure project. This pipeline significantly increases Norway's gas export capacity to Poland and Central Europe. This development improved energy diversification for the region and reduced reliance on Russian gas, demonstrating the shift towards more resilient energy supply chains.

Strategic Outlook for Europe Gas Industry Market

The future of the European gas industry hinges on adapting to the energy transition. While natural gas will continue to play a significant role in the energy mix in the near term, its long-term dominance is challenged by renewable energy sources. Companies that successfully invest in technologies like carbon capture and hydrogen blending will be better positioned for long-term success. The focus on improving energy efficiency, fostering innovation in renewable gas sources, and ensuring energy security will shape the industry's strategic direction. Investing in new infrastructure to handle renewable gas imports, such as hydrogen, will also prove to be increasingly crucial.

Europe Gas Industry Segmentation

-

1. Application

- 1.1. Utilities

- 1.2. Industrial

- 1.3. Commercial

Europe Gas Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

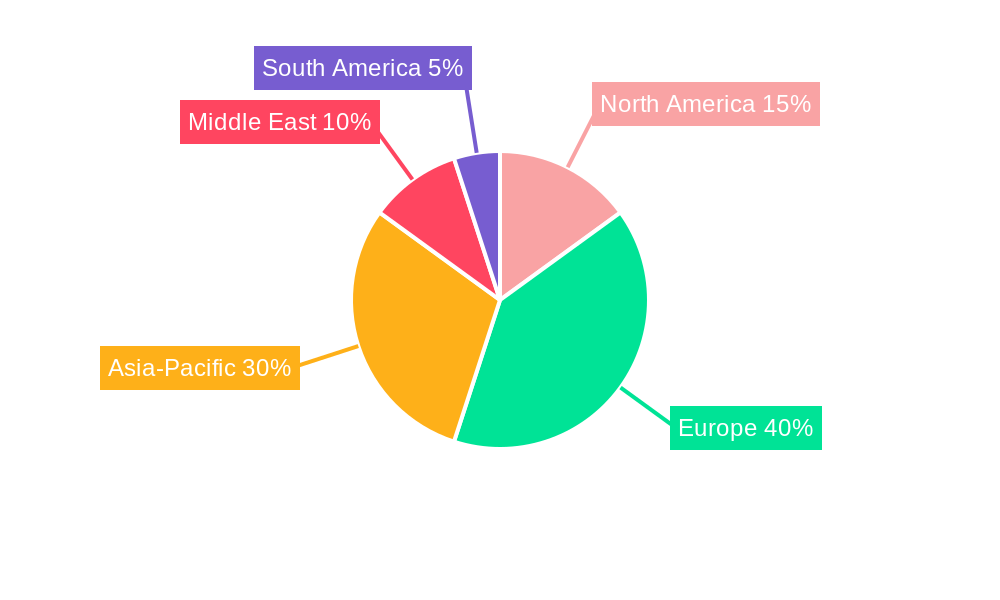

Europe Gas Industry Regional Market Share

Geographic Coverage of Europe Gas Industry

Europe Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Utilities

- 5.1.2. Industrial

- 5.1.3. Commercial

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Germany

- 5.2.2. United Kingdom

- 5.2.3. France

- 5.2.4. Italy

- 5.2.5. Spain

- 5.2.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Europe Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Utilities

- 6.1.2. Industrial

- 6.1.3. Commercial

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Germany Europe Gas Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Utilities

- 7.1.2. Industrial

- 7.1.3. Commercial

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. United Kingdom Europe Gas Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Utilities

- 8.1.2. Industrial

- 8.1.3. Commercial

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. France Europe Gas Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Utilities

- 9.1.2. Industrial

- 9.1.3. Commercial

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Italy Europe Gas Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Utilities

- 10.1.2. Industrial

- 10.1.3. Commercial

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Spain Europe Gas Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Utilities

- 11.1.2. Industrial

- 11.1.3. Commercial

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Rest of Europe Europe Gas Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Application

- 12.1.1. Utilities

- 12.1.2. Industrial

- 12.1.3. Commercial

- 12.1. Market Analysis, Insights and Forecast - by Application

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Chevron Corporation

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 BP PLC

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 TotalEnergies SE

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Exxon Mobil Corporation

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Equinor ASA

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 NK Lukoil PAO

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Gazprom PJSC ADR

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Rosneft Oil Co PJSC*List Not Exhaustive

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.1 Chevron Corporation

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Europe Gas Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Germany Europe Gas Industry Revenue (million), by Application 2025 & 2033

- Figure 3: Germany Europe Gas Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: Germany Europe Gas Industry Revenue (million), by Country 2025 & 2033

- Figure 5: Germany Europe Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: United Kingdom Europe Gas Industry Revenue (million), by Application 2025 & 2033

- Figure 7: United Kingdom Europe Gas Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: United Kingdom Europe Gas Industry Revenue (million), by Country 2025 & 2033

- Figure 9: United Kingdom Europe Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: France Europe Gas Industry Revenue (million), by Application 2025 & 2033

- Figure 11: France Europe Gas Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: France Europe Gas Industry Revenue (million), by Country 2025 & 2033

- Figure 13: France Europe Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Italy Europe Gas Industry Revenue (million), by Application 2025 & 2033

- Figure 15: Italy Europe Gas Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Italy Europe Gas Industry Revenue (million), by Country 2025 & 2033

- Figure 17: Italy Europe Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Spain Europe Gas Industry Revenue (million), by Application 2025 & 2033

- Figure 19: Spain Europe Gas Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Spain Europe Gas Industry Revenue (million), by Country 2025 & 2033

- Figure 21: Spain Europe Gas Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Rest of Europe Europe Gas Industry Revenue (million), by Application 2025 & 2033

- Figure 23: Rest of Europe Europe Gas Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Rest of Europe Europe Gas Industry Revenue (million), by Country 2025 & 2033

- Figure 25: Rest of Europe Europe Gas Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Europe Gas Industry Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Europe Gas Industry Revenue million Forecast, by Region 2020 & 2033

- Table 3: Global Europe Gas Industry Revenue million Forecast, by Application 2020 & 2033

- Table 4: Global Europe Gas Industry Revenue million Forecast, by Country 2020 & 2033

- Table 5: Global Europe Gas Industry Revenue million Forecast, by Application 2020 & 2033

- Table 6: Global Europe Gas Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: Global Europe Gas Industry Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Europe Gas Industry Revenue million Forecast, by Country 2020 & 2033

- Table 9: Global Europe Gas Industry Revenue million Forecast, by Application 2020 & 2033

- Table 10: Global Europe Gas Industry Revenue million Forecast, by Country 2020 & 2033

- Table 11: Global Europe Gas Industry Revenue million Forecast, by Application 2020 & 2033

- Table 12: Global Europe Gas Industry Revenue million Forecast, by Country 2020 & 2033

- Table 13: Global Europe Gas Industry Revenue million Forecast, by Application 2020 & 2033

- Table 14: Global Europe Gas Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Gas Industry?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Europe Gas Industry?

Key companies in the market include Chevron Corporation, BP PLC, TotalEnergies SE, Exxon Mobil Corporation, Equinor ASA, NK Lukoil PAO, Gazprom PJSC ADR, Rosneft Oil Co PJSC*List Not Exhaustive.

3. What are the main segments of the Europe Gas Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 1223.8 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Utility Sector (i.e.. Power Generation) Sector Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

September 2022: Russia's Gazprom announced shipping 42.4 million cubic meters (mcm) of natural gas to Europe via Ukraine. The shift was part of a push by Russia to reduce its reliance on the US dollar.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Gas Industry?

To stay informed about further developments, trends, and reports in the Europe Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence