Key Insights

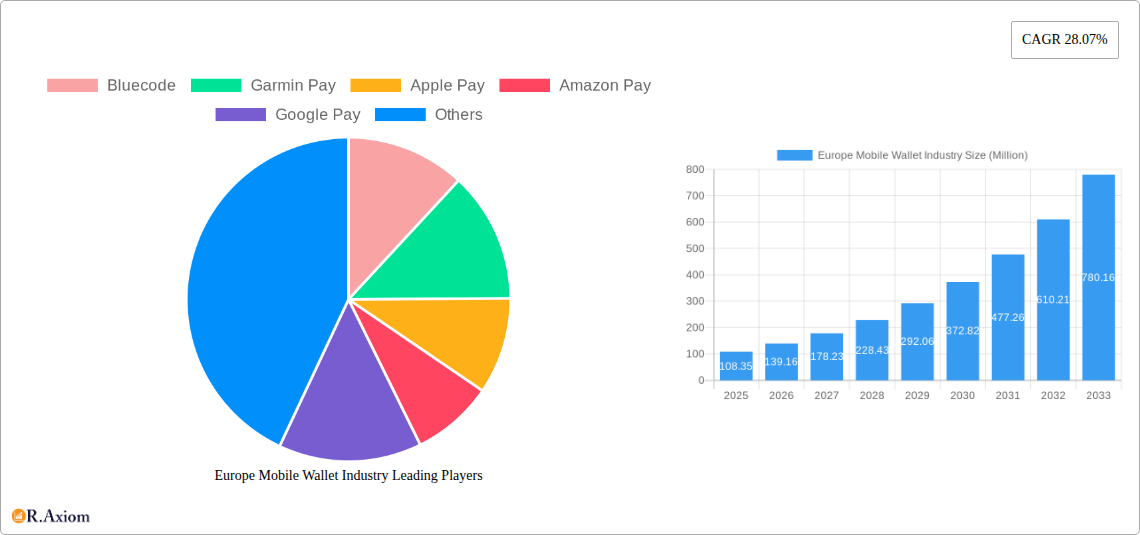

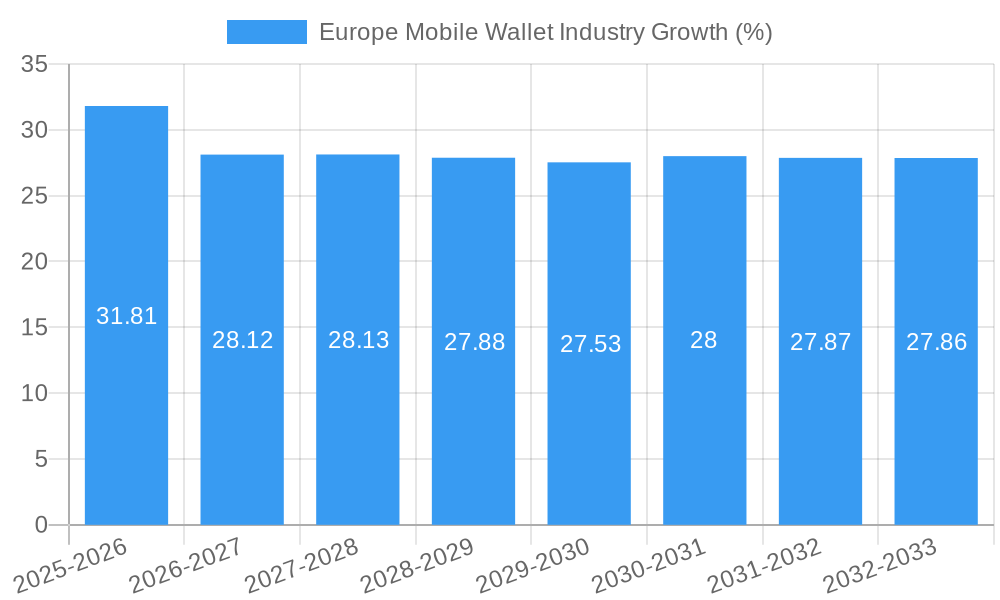

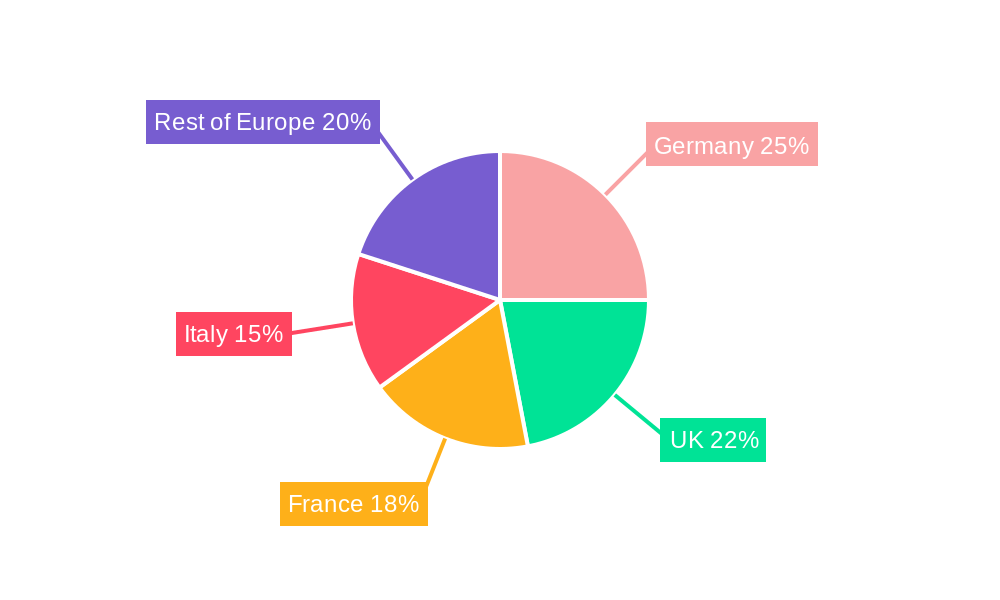

The European mobile wallet market is experiencing robust growth, projected to reach €108.35 million in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 28.07% from 2025 to 2033. This expansion is fueled by several key drivers. Increasing smartphone penetration across Europe, coupled with rising consumer adoption of digital payment methods, is a significant factor. Enhanced security features and user-friendly interfaces offered by mobile wallets are also attracting a wider user base. Furthermore, the growing prevalence of contactless payments and the increasing integration of mobile wallets with loyalty programs and rewards systems are contributing to this upward trajectory. The market's segmentation reveals a strong preference for proximity payments, likely driven by convenience and speed. Germany, the UK, France, and Italy represent the largest national markets within Europe, reflecting their advanced digital infrastructure and higher consumer spending power. However, the "Rest of Europe" segment also shows substantial potential for growth as digitalization expands in less developed markets. Competitive rivalry among established players like Apple Pay, Google Pay, Samsung Pay, and PayPal, alongside emerging fintech companies such as Klarna and Bluecode, ensures innovation and further fuels market expansion.

The continued growth of the European mobile wallet market depends on several factors. Addressing consumer concerns around data security and privacy will be crucial to maintaining confidence in the technology. Expansion into rural and less digitally connected areas requires further infrastructure development and targeted marketing initiatives. The ongoing integration of mobile wallets with other financial services and applications, such as banking and loyalty programs, will further enhance their utility and drive adoption. Furthermore, regulatory frameworks supporting the adoption of mobile payments and promoting interoperability across different platforms are vital for sustainable growth. The emergence of new technologies, such as biometric authentication and advanced fraud detection systems, will further enhance the security and appeal of mobile wallets, underpinning the market’s continued positive trajectory.

This in-depth report provides a comprehensive analysis of the Europe mobile wallet industry, covering market size, growth drivers, competitive landscape, and future outlook. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The report offers actionable insights for industry stakeholders, including mobile wallet providers, financial institutions, and technology companies. This report is crucial for understanding the dynamic European mobile payments landscape and formulating effective strategies for growth and market penetration.

Europe Mobile Wallet Industry Market Concentration & Innovation

The European mobile wallet market exhibits a moderately concentrated landscape, dominated by established players like Apple Pay, Google Pay, PayPal, and Samsung Pay, alongside regional players such as Bluecode and Klarna. However, increasing innovation and the entry of new fintech companies are gradually shaping a more competitive environment. The market's innovative nature is driven by advancements in near-field communication (NFC) technology, the rise of biometric authentication, and the integration of mobile wallets with various services, enhancing user experience. Stringent regulatory frameworks, including PSD2 and GDPR, influence the market, impacting data security and interoperability. Product substitutes, such as traditional credit and debit cards, continue to compete, but the increasing convenience and security of mobile wallets are gradually shifting consumer preferences. Significant M&A activities are expected, with deal values potentially reaching XX Million in the coming years, primarily driven by the need for expansion and technological integration. Market share data for key players in 2025 is estimated as follows:

- Apple Pay: 25%

- Google Pay: 20%

- PayPal: 15%

- Samsung Pay: 10%

- Others: 30%

Europe Mobile Wallet Industry Industry Trends & Insights

The European mobile wallet market is experiencing robust growth, with a Compound Annual Growth Rate (CAGR) projected at xx% during the forecast period (2025-2033). This growth is fueled by several key factors: the increasing adoption of smartphones, rising e-commerce penetration, the expanding digital economy, and the growing preference for contactless payments. Technological disruptions, including advancements in blockchain technology and the integration of artificial intelligence (AI) for fraud detection and personalized offers, are further accelerating market expansion. Consumer preferences are increasingly shifting towards seamless, secure, and versatile payment solutions, driving the demand for feature-rich mobile wallets. Competitive dynamics are intensifying, with companies focusing on strategic partnerships, product differentiation, and aggressive marketing to gain market share. Market penetration is expected to reach xx% by 2033, indicating significant growth potential in the coming years. The COVID-19 pandemic accelerated the adoption of contactless payments, pushing the market's growth trajectory upwards.

Dominant Markets & Segments in Europe Mobile Wallet Industry

The UK, Germany, and France represent the dominant markets within Europe for mobile wallets, driven by high smartphone penetration, robust digital infrastructure, and a favorable regulatory environment. Italy and the rest of Europe are also exhibiting significant growth, albeit at a slightly slower pace.

By Country:

- UK: High smartphone penetration, strong digital infrastructure, early adoption of contactless payments.

- Germany: Growing digital literacy, increasing acceptance of mobile payments among businesses.

- France: Increasing government initiatives to promote digital payments.

- Italy: Growing adoption among younger demographics, increasing e-commerce activity.

- Rest of Europe: Significant growth potential, driven by increasing smartphone and internet penetration.

By Payment Mode:

- Proximity Payment: Dominates the market due to ease of use and widespread NFC adoption. Growth driven by increased contactless POS terminals.

- Remote Payment: Experiencing rapid growth driven by e-commerce boom and increasing online transactions.

Europe Mobile Wallet Industry Product Developments

Recent product innovations include enhanced security features, such as biometric authentication and tokenization, alongside the integration of various loyalty programs and reward systems within mobile wallets. The emergence of super apps, offering integrated payment and other financial services, is transforming the competitive landscape. The key advantage of these products is their seamless integration with existing digital ecosystems and user-friendly interfaces. Technological trends, such as the integration of blockchain technology for enhanced security and AI-driven fraud detection, are shaping the future of mobile wallet products.

Report Scope & Segmentation Analysis

This report segments the European mobile wallet market by payment mode (Proximity Payment, Remote Payment) and by country (UK, Germany, France, Italy, Rest of Europe). Each segment's growth projections, market sizes (in Millions), and competitive dynamics are analyzed separately. For instance, the proximity payment segment is experiencing faster growth due to increased contactless POS infrastructure, while the remote payment segment is propelled by the growth in e-commerce.

Key Drivers of Europe Mobile Wallet Industry Growth

Key drivers of growth include increasing smartphone penetration, rising e-commerce adoption, government support for digitalization, and the growing preference for contactless and cashless transactions. The increasing adoption of NFC technology is further enhancing the convenience of mobile payments. Regulatory changes promoting open banking and fostering innovation also contribute significantly to the market's growth. These factors combined lead to significant market expansion in the coming years.

Challenges in the Europe Mobile Wallet Industry Sector

The industry faces challenges like security concerns, data privacy regulations (like GDPR), and the need for robust fraud prevention mechanisms. Interoperability between different mobile wallet systems remains a challenge. The high initial investment cost for infrastructure and technology can also deter smaller players from entering the market. Consumer awareness and adoption rates vary across countries, leading to uneven market penetration. These challenges pose significant obstacles to achieving wider adoption across Europe.

Emerging Opportunities in Europe Mobile Wallet Industry

Emerging opportunities include the integration of mobile wallets with Internet of Things (IoT) devices, expansion into underserved markets within Europe, and the development of specialized solutions for specific industry segments (e.g., healthcare, transportation). The growing adoption of biometrics and AI for enhanced security and personalized experiences presents further opportunities for innovation and expansion. The increasing demand for digital identity solutions could further drive growth.

Leading Players in the Europe Mobile Wallet Industry Market

- Bluecode

- Garmin Pay

- Apple Pay

- Amazon Pay

- Google Pay

- Klarna

- Bit Pay

- Fitbit Pay

- PayPal

- Samsung Pay

Key Developments in Europe Mobile Wallet Industry Industry

- May 2022: Google announced Google Wallet for Android devices, enhancing contactless payment capabilities and storing digital IDs.

- June 2022: Bluecode and TWINT achieved interoperability, enhancing cross-platform usage.

- October 2022: Deutsche Bank and Fiserv launched Vert, providing payment acceptance and banking services to SMEs.

- October 2022: NPCI International Payments (NIPL) and Worldline partnered to facilitate UPI payments for Indians in Europe.

- February 2023: Enfuce and Starcart partnered to offer embedded virtual card payments, enhancing competition among online vendors.

Strategic Outlook for Europe Mobile Wallet Industry Market

The future of the European mobile wallet market is promising, with continued growth driven by technological advancements, increasing digitalization, and favorable regulatory frameworks. The focus on enhanced security, user experience, and the integration of value-added services will be key to success. Expansion into new markets and the development of innovative solutions tailored to specific customer needs will present significant opportunities for growth and market leadership in the years to come. The market's continued evolution will reshape the landscape of digital payments in Europe.

Europe Mobile Wallet Industry Segmentation

-

1. Payment Mode

- 1.1. Proximity Payment

- 1.2. Remote Payment

Europe Mobile Wallet Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Mobile Wallet Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 28.07% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Adoption of the Digitalization in Europe; Pay-backs and Reward Strategies to Boost Market Growth; Instant payments are becoming increasingly widespread

- 3.3. Market Restrains

- 3.3.1 High Dependence on External Sources to Balance the Skill Deficit; Vendor Lock In; Compliance Issues

- 3.3.2 Migration Complexity

- 3.3.3 And Security Risks

- 3.4. Market Trends

- 3.4.1. E-commerce to Drive the Mobile Payments Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Payment Mode

- 5.1.1. Proximity Payment

- 5.1.2. Remote Payment

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Payment Mode

- 6. Germany Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Mobile Wallet Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Bluecode

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Garmin Pay

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Apple Pay

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Amazon Pay

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Google Pay

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Klarna

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Bit Pay

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Fitbit Pay

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Paypal

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Samsung Pay

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Bluecode

List of Figures

- Figure 1: Europe Mobile Wallet Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Mobile Wallet Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Mobile Wallet Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Mobile Wallet Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Europe Mobile Wallet Industry Revenue Million Forecast, by Payment Mode 2019 & 2032

- Table 4: Europe Mobile Wallet Industry Volume K Unit Forecast, by Payment Mode 2019 & 2032

- Table 5: Europe Mobile Wallet Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Mobile Wallet Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 7: Europe Mobile Wallet Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Europe Mobile Wallet Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 9: Germany Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Germany Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 11: France Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 13: Italy Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Italy Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: United Kingdom Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: United Kingdom Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: Netherlands Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Netherlands Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: Sweden Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Sweden Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Rest of Europe Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Europe Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Europe Mobile Wallet Industry Revenue Million Forecast, by Payment Mode 2019 & 2032

- Table 24: Europe Mobile Wallet Industry Volume K Unit Forecast, by Payment Mode 2019 & 2032

- Table 25: Europe Mobile Wallet Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Europe Mobile Wallet Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 27: United Kingdom Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: United Kingdom Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 29: Germany Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Germany Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 31: France Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: France Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 33: Italy Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Italy Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 35: Spain Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Spain Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 37: Netherlands Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Netherlands Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 39: Belgium Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Belgium Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 41: Sweden Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Sweden Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 43: Norway Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Norway Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 45: Poland Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Poland Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 47: Denmark Europe Mobile Wallet Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Denmark Europe Mobile Wallet Industry Volume (K Unit) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Mobile Wallet Industry?

The projected CAGR is approximately 28.07%.

2. Which companies are prominent players in the Europe Mobile Wallet Industry?

Key companies in the market include Bluecode, Garmin Pay, Apple Pay, Amazon Pay, Google Pay, Klarna, Bit Pay, Fitbit Pay, Paypal, Samsung Pay.

3. What are the main segments of the Europe Mobile Wallet Industry?

The market segments include Payment Mode.

4. Can you provide details about the market size?

The market size is estimated to be USD 108.35 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of the Digitalization in Europe; Pay-backs and Reward Strategies to Boost Market Growth; Instant payments are becoming increasingly widespread.

6. What are the notable trends driving market growth?

E-commerce to Drive the Mobile Payments Market.

7. Are there any restraints impacting market growth?

High Dependence on External Sources to Balance the Skill Deficit; Vendor Lock In; Compliance Issues. Migration Complexity. And Security Risks.

8. Can you provide examples of recent developments in the market?

February 2023 - Card issuing and processing powerhouse Enfuce and Starcart e-commerce aggregator partnered to provide embedded virtual card payments to its merchants and customers with security and speed. Using Enfuce's turnkey Card as a Service (CaaS), online vendors can compete fairly with their rivals and attract clients they wouldn't ordinarily be able to.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Mobile Wallet Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Mobile Wallet Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Mobile Wallet Industry?

To stay informed about further developments, trends, and reports in the Europe Mobile Wallet Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence