Key Insights

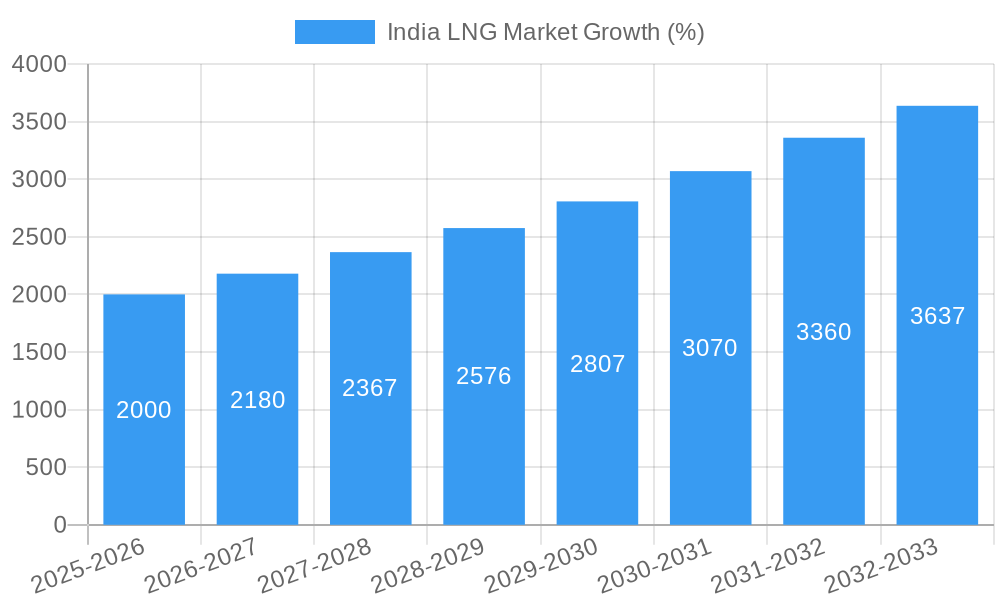

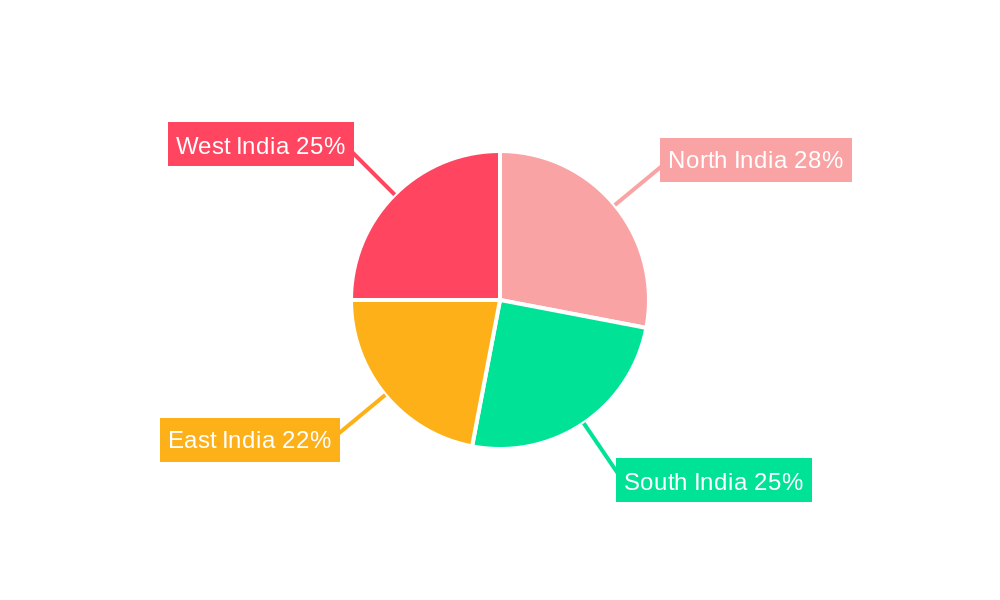

The India LNG market is experiencing robust growth, projected to expand significantly over the forecast period (2025-2033). Driven by increasing energy demand, particularly in the burgeoning city gas distribution (CGD) sector and petrochemical industries, the market is poised for a compound annual growth rate (CAGR) exceeding 8%. This growth is fueled by government initiatives promoting cleaner energy sources and the expansion of LNG infrastructure, including liquefaction plants, regasification terminals, and LNG shipping capabilities. Key players like Adani Total Gas, Shell PLC, and Petronet LNG Ltd are actively investing in this sector, enhancing the market's competitive landscape. However, challenges such as infrastructure limitations in certain regions and potential price volatility in the global LNG market could act as restraints. The segmentation reveals the significant contributions of LNG infrastructure and various applications, with city gas distribution and petrochemicals being major drivers of growth. Regional disparities exist within India, with North, South, East, and West India presenting diverse market opportunities based on varying levels of infrastructure development and energy consumption patterns. The market's future trajectory is heavily reliant on continued infrastructure investments and the sustained adoption of LNG as a cleaner and efficient fuel source.

The substantial growth in the Indian LNG market is expected to continue throughout the forecast period, driven by consistent demand from power generation, industrial processes, and transportation. The government's strong focus on reducing reliance on fossil fuels and promoting environmentally friendly alternatives provides a significant tailwind. While challenges remain, including the need for continuous improvements in distribution networks and managing potential supply chain disruptions, the overall outlook remains optimistic. Strategic partnerships between domestic and international players are fostering innovation and technological advancements in LNG handling and processing. The sustained focus on enhancing safety standards and environmental protection will be vital to ensuring the responsible and sustainable growth of the Indian LNG market in the coming years. This robust growth presents lucrative opportunities for both domestic and international investors looking to capitalize on India's energy transition.

This detailed report provides a comprehensive analysis of the India LNG market, encompassing market size, growth drivers, competitive landscape, and future outlook. The study period covers 2019-2033, with 2025 as the base year and forecast period spanning 2025-2033. This report is essential for industry stakeholders, investors, and businesses seeking to understand and capitalize on the burgeoning opportunities within the Indian LNG sector.

India LNG Market Market Concentration & Innovation

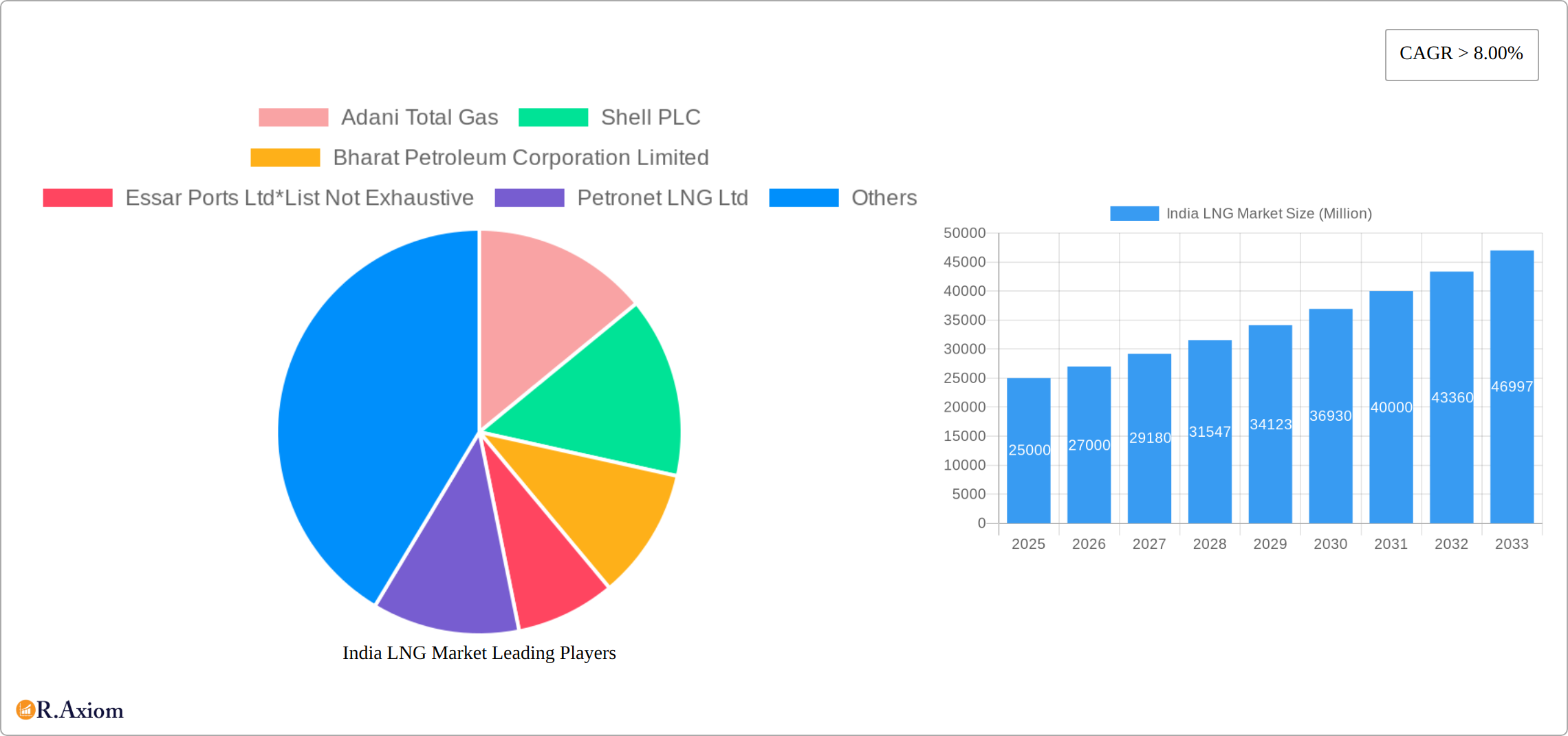

The Indian LNG market exhibits a moderately concentrated structure, with key players like Adani Total Gas, Shell PLC, Bharat Petroleum Corporation Limited, Petronet LNG Ltd, GSPC LNG Limited, and GAIL Limited holding significant market share. However, the emergence of new entrants and ongoing investments signal a dynamic competitive landscape. Market share estimations for 2025 indicate Adani Total Gas holds approximately 25% of the market, followed by Shell PLC at 18%, and Bharat Petroleum Corporation Limited at 15%. The remaining share is distributed among other players, including Essar Ports Ltd, GSPC LNG Limited and GAIL Limited.

Innovation in the sector is driven by the need for efficient LNG infrastructure, including advanced liquefaction and regasification technologies. Regulatory frameworks, such as the government's emphasis on cleaner energy sources, are also key drivers. Product substitutes, primarily other fossil fuels like coal and oil, still pose a challenge, but the increasing focus on environmental sustainability favours LNG's growth. End-user trends, such as the expansion of City Gas Distribution (CGD) networks, are significantly boosting demand. Mergers and acquisitions (M&A) activity, exemplified by Petronet LNG's investments detailed below, indicates strategic consolidation and expansion within the market. Total M&A deal values in the sector for 2024 reached approximately USD xx Million.

India LNG Market Industry Trends & Insights

The Indian LNG market is experiencing robust growth, driven by increasing energy demand, government initiatives promoting natural gas usage, and investments in LNG infrastructure. The CAGR for the forecast period (2025-2033) is estimated at xx%, with market penetration expected to reach xx% by 2033. Technological disruptions are influencing the sector, with a shift towards floating storage regasification units (FSRUs) and advancements in LNG transportation and storage technologies. Consumer preferences are increasingly favouring cleaner energy sources, fueling demand for LNG as a transition fuel. Competitive dynamics are characterized by both intense competition among established players and the entry of new players, especially in the LNG import terminal space. The increasing number of LNG import terminals will add to the overall market capacity and increase competition.

Dominant Markets & Segments in India LNG Market

The dominant segment within the Indian LNG market is City Gas Distribution (CGD), driven by the government's push to expand natural gas networks across the country. Key drivers include favorable government policies, supportive infrastructure development, and increasing urbanization. Within LNG infrastructure, LNG regasification facilities show significant growth potential due to the rising demand for imported LNG.

Key Drivers for CGD:

- Expanding CGD networks

- Government subsidies and incentives

- Growing urbanization and industrialization

- Replacement of traditional fuels

Key Drivers for LNG Regasification:

- Increasing LNG imports

- Development of new regasification terminals

- Government support for infrastructure development

- Proximity to major consumption centers

The western region of India dominates the LNG market due to its established industrial and urban centers, coupled with robust infrastructure.

India LNG Market Product Developments

Recent product developments in the Indian LNG market are significantly enhancing efficiency, safety, and cost-effectiveness across the entire LNG value chain, from liquefaction to transportation and regasification. This includes advancements in liquefaction and regasification technologies, the utilization of innovative materials for improved storage and transportation, and the optimization of supply chain logistics. These improvements are not only driving down costs but also contributing to a more environmentally sustainable LNG sector. The increasing adoption of Floating Storage Regasification Units (FSRUs) provides a flexible and economically viable solution for smaller-scale LNG import requirements, thereby opening up new market opportunities, particularly in regions with limited pipeline infrastructure.

Further innovations include the development of advanced cryogenic technologies for enhanced efficiency in LNG handling, as well as the integration of digital technologies for improved monitoring, control, and predictive maintenance of LNG infrastructure. This focus on technological advancement positions the Indian LNG market for robust future growth while minimizing environmental impact.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation of the Indian LNG market, categorized by infrastructure (LNG liquefaction plants, LNG regasification terminals, LNG shipping) and application (City Gas Distribution (CGD), petrochemicals, power generation, and other industrial applications). Each segment is meticulously analyzed, encompassing market size estimations, future growth projections, and a detailed examination of the competitive landscape.

LNG Liquefaction Plants: While currently dominated by a few major players, the liquefaction segment's near-term growth potential is somewhat limited due to existing capacity. However, long-term expansion is anticipated to meet increasing domestic demand.

LNG Regasification Facilities: This segment is experiencing robust growth, fueled by a surge in LNG imports and the development of new import terminals across the country. The expansion of regasification capacity is crucial for ensuring adequate supply to meet rising demand.

LNG Shipping: The increasing volume of LNG trade is driving significant growth in the LNG shipping segment. This segment is characterized by intense competition amongst shipping companies vying for market share.

City Gas Distribution (CGD): This segment represents the largest and fastest-growing application of LNG in India, driven by substantial government support and the ongoing expansion of CGD networks across urban and rural areas.

Petrochemicals: The petrochemical industry constitutes a significant, albeit relatively stable, segment, utilizing LNG as a vital feedstock for various petrochemical processes.

Power Generation & Other Industrial Applications: This segment encompasses diverse applications, including power generation, industrial processes, and other niche uses of LNG, contributing to the overall market growth.

Key Drivers of India LNG Market Growth

Several factors drive the growth of the Indian LNG market, including the government's push for cleaner fuels, rising energy demand, expanding CGD networks, and investments in LNG infrastructure. The government's initiatives to reduce reliance on imported coal and increase the share of natural gas in the energy mix are major catalysts. Furthermore, technological advancements in LNG liquefaction and regasification are improving efficiency and reducing costs.

Challenges in the India LNG Market Sector

Despite significant growth potential, the Indian LNG market faces challenges including infrastructure bottlenecks, regulatory hurdles, and competition from other fuels. The development of new infrastructure, including pipelines and storage facilities, remains a critical challenge. Furthermore, fluctuating global LNG prices and potential supply chain disruptions represent significant risks. The high initial investment required for LNG infrastructure projects can deter some market players.

Emerging Opportunities in India LNG Market

Emerging opportunities lie in the expansion of CGD networks, the development of LNG bunkering facilities, and the growing demand for LNG in the industrial and power sectors. The increasing adoption of FSRUs opens new avenues for smaller-scale LNG import terminals and offers flexibility to underserved regions. The potential for the use of LNG as a transportation fuel presents a significant, emerging opportunity.

Leading Players in the India LNG Market Market

- Adani Total Gas

- Shell PLC

- Bharat Petroleum Corporation Limited

- Essar Ports Ltd

- Petronet LNG Ltd

- GSPC LNG Limited

- GAIL Limited

- H-Energy Private Limited

- JSW Infrastructure

Key Developments in India LNG Market Industry

- April 2022: Petronet LNG announced plans for a floating LNG terminal in Odisha by 2025 (INR 1600 crore investment), along with a further INR 600 crore investment to expand the Dahej LNG terminal capacity to 22.5 MTPA. These investments demonstrate a commitment to enhancing LNG import and regasification capabilities.

- January 2022: LNG Alliance announced a USD 290 Million investment in an LNG import terminal in Karnataka, incorporating India's first dedicated LNG bunkering facility (4 MTPA capacity). This initiative significantly enhances LNG supply infrastructure and supports the growth of the LNG bunkering sector.

- [Add other key developments with dates and brief descriptions. Include details on new projects, expansions, and regulatory changes.]

Strategic Outlook for India LNG Market Market

The Indian LNG market is poised for substantial growth in the coming years, driven by strong government support, rising energy demand, and technological advancements. The expansion of CGD networks, the development of new LNG import terminals, and the increasing adoption of LNG in various sectors present significant opportunities for both existing and new market participants. The strategic focus should be on infrastructure development, technological innovation, and optimizing the supply chain to meet the growing demand.

India LNG Market Segmentation

-

1. LNG Infrastructure

- 1.1. LNG Liquefaction Plants

- 1.2. LNG Regasification Facilities

- 1.3. LNG Shipping

- 2. LNG Trade

-

3. Application

- 3.1. City Gas Distribution

- 3.2. Petrochemicals

- 3.3. Other Applications

India LNG Market Segmentation By Geography

- 1. India

India LNG Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 8.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities

- 3.3. Market Restrains

- 3.3.1. 4.; Increasing Adoption of Clean Power Sources

- 3.4. Market Trends

- 3.4.1. City Gas Distribution segments to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India LNG Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by LNG Infrastructure

- 5.1.1. LNG Liquefaction Plants

- 5.1.2. LNG Regasification Facilities

- 5.1.3. LNG Shipping

- 5.2. Market Analysis, Insights and Forecast - by LNG Trade

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. City Gas Distribution

- 5.3.2. Petrochemicals

- 5.3.3. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by LNG Infrastructure

- 6. North India India LNG Market Analysis, Insights and Forecast, 2019-2031

- 7. South India India LNG Market Analysis, Insights and Forecast, 2019-2031

- 8. East India India LNG Market Analysis, Insights and Forecast, 2019-2031

- 9. West India India LNG Market Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Adani Total Gas

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Shell PLC

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Bharat Petroleum Corporation Limited

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Essar Ports Ltd*List Not Exhaustive

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Petronet LNG Ltd

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 GSPC LNG Limited

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 GAIL Limited

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 H-Energy Private Limited

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 JSW Infrastructure

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.1 Adani Total Gas

List of Figures

- Figure 1: India LNG Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India LNG Market Share (%) by Company 2024

List of Tables

- Table 1: India LNG Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India LNG Market Volume metric tonnes Forecast, by Region 2019 & 2032

- Table 3: India LNG Market Revenue Million Forecast, by LNG Infrastructure 2019 & 2032

- Table 4: India LNG Market Volume metric tonnes Forecast, by LNG Infrastructure 2019 & 2032

- Table 5: India LNG Market Revenue Million Forecast, by LNG Trade 2019 & 2032

- Table 6: India LNG Market Volume metric tonnes Forecast, by LNG Trade 2019 & 2032

- Table 7: India LNG Market Revenue Million Forecast, by Application 2019 & 2032

- Table 8: India LNG Market Volume metric tonnes Forecast, by Application 2019 & 2032

- Table 9: India LNG Market Revenue Million Forecast, by Region 2019 & 2032

- Table 10: India LNG Market Volume metric tonnes Forecast, by Region 2019 & 2032

- Table 11: India LNG Market Revenue Million Forecast, by Country 2019 & 2032

- Table 12: India LNG Market Volume metric tonnes Forecast, by Country 2019 & 2032

- Table 13: North India India LNG Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: North India India LNG Market Volume (metric tonnes) Forecast, by Application 2019 & 2032

- Table 15: South India India LNG Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: South India India LNG Market Volume (metric tonnes) Forecast, by Application 2019 & 2032

- Table 17: East India India LNG Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: East India India LNG Market Volume (metric tonnes) Forecast, by Application 2019 & 2032

- Table 19: West India India LNG Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: West India India LNG Market Volume (metric tonnes) Forecast, by Application 2019 & 2032

- Table 21: India LNG Market Revenue Million Forecast, by LNG Infrastructure 2019 & 2032

- Table 22: India LNG Market Volume metric tonnes Forecast, by LNG Infrastructure 2019 & 2032

- Table 23: India LNG Market Revenue Million Forecast, by LNG Trade 2019 & 2032

- Table 24: India LNG Market Volume metric tonnes Forecast, by LNG Trade 2019 & 2032

- Table 25: India LNG Market Revenue Million Forecast, by Application 2019 & 2032

- Table 26: India LNG Market Volume metric tonnes Forecast, by Application 2019 & 2032

- Table 27: India LNG Market Revenue Million Forecast, by Country 2019 & 2032

- Table 28: India LNG Market Volume metric tonnes Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India LNG Market?

The projected CAGR is approximately > 8.00%.

2. Which companies are prominent players in the India LNG Market?

Key companies in the market include Adani Total Gas, Shell PLC, Bharat Petroleum Corporation Limited, Essar Ports Ltd*List Not Exhaustive, Petronet LNG Ltd, GSPC LNG Limited, GAIL Limited, H-Energy Private Limited, JSW Infrastructure.

3. What are the main segments of the India LNG Market?

The market segments include LNG Infrastructure, LNG Trade, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities.

6. What are the notable trends driving market growth?

City Gas Distribution segments to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Clean Power Sources.

8. Can you provide examples of recent developments in the market?

In April 2022, Petronet LNG announced the development of a floating LNG terminal in Odisha by 2025 at the cost of INR 1600 crore. Furthermore, Petronet is likely to invest INR 600 crore in raising the capacity of the Dahej LNG import terminal to 22.5 million tonnes per annum from the current 17.5 million tonnes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in metric tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India LNG Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India LNG Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India LNG Market?

To stay informed about further developments, trends, and reports in the India LNG Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence