Key Insights

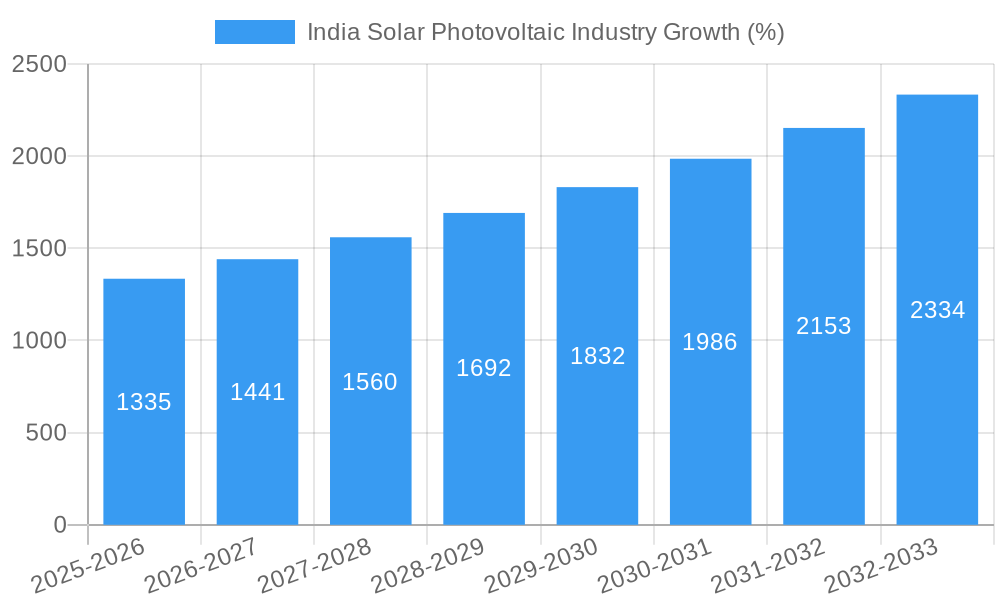

The Indian solar photovoltaic (PV) industry is experiencing robust growth, driven by the government's ambitious renewable energy targets, decreasing PV module costs, and increasing energy demand. With a Compound Annual Growth Rate (CAGR) exceeding 8.90%, the market, valued at (estimated) ₹X million in 2025, is projected to reach a significant size by 2033. Several factors contribute to this expansion. Government policies promoting solar energy adoption, including subsidies and tax benefits, are incentivizing both residential and commercial installations. The declining cost of solar PV modules makes solar energy increasingly competitive with traditional power sources. Furthermore, the diversification of end-user segments – residential, commercial and industrial (C&I), and utility – ensures a broad market base. The market is segmented by PV type (thin film, crystalline silicon), deployment (ground-mounted, rooftop), fueling competition and innovation. Leading players like Adani Group, Tata Power Solar, Mahindra Susten, and international companies such as First Solar and ABB, are actively shaping the market landscape. Regional variations in growth are expected, with potentially higher adoption rates in states with favorable solar irradiance and supportive government initiatives. However, challenges remain, including land acquisition complexities, grid integration issues, and dependence on imported components.

Despite these challenges, the long-term outlook for the Indian solar PV market remains positive. Continued technological advancements, improved energy storage solutions, and further government support are likely to further propel growth. The market is witnessing a shift towards larger-scale projects, driven by the increasing demand for renewable energy from utilities. The growing focus on sustainable development and environmental concerns is also boosting the adoption of solar PV technology. The competitive landscape is dynamic, with both domestic and foreign players vying for market share, leading to innovative product offerings and cost reductions, benefiting consumers and furthering market expansion.

India Solar Photovoltaic Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the Indian solar photovoltaic (PV) industry, offering actionable insights for stakeholders across the value chain. The report covers the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. It examines market size, growth drivers, challenges, opportunities, and competitive dynamics, incorporating recent industry developments and projecting future trends. The report leverages extensive data analysis and expert insights to provide a clear and concise understanding of this rapidly evolving market. The market is segmented by type (thin film, crystalline silicon), end-user (residential, commercial & industrial (C&I), utility), and deployment (ground-mounted, rooftop).

India Solar Photovoltaic Industry Market Concentration & Innovation

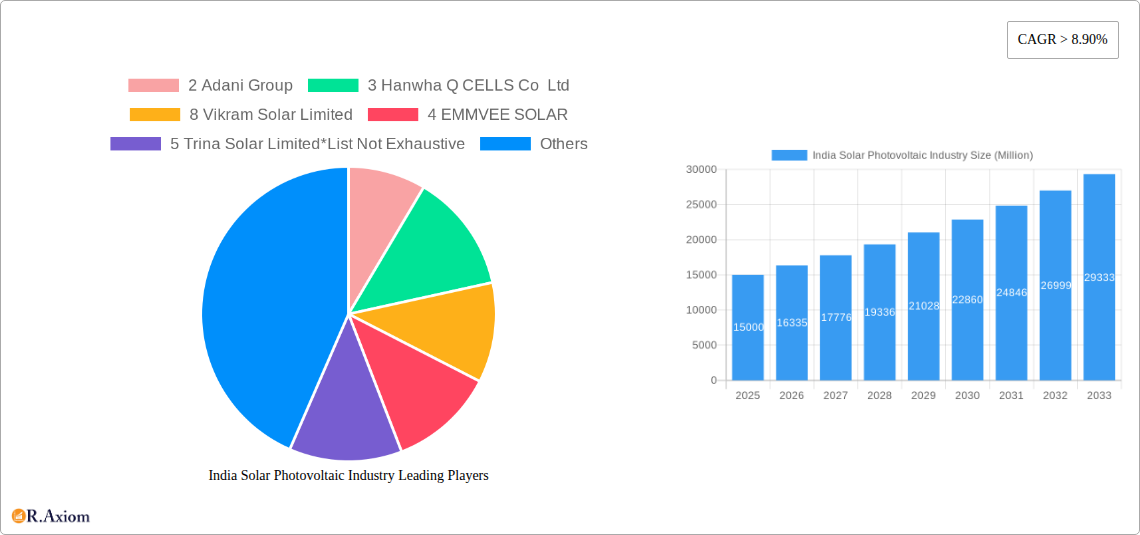

The Indian solar PV market exhibits a dynamic interplay between established players and emerging entrants. Market concentration is moderate, with a few large players holding significant shares but numerous smaller companies contributing to the overall growth. While Adani Group, Hanwha Q CELLS Co Ltd, Vikram Solar Limited, EMMVEE SOLAR, and Trina Solar Limited are among the leading players, the landscape is far from monolithic. Domestic players like Sterling And Wilson Pvt Ltd, Tata Power Solar Systems Ltd, and Mahindra Susten Pvt Ltd actively compete with foreign players such as First Solar Inc, ABB, ACME Solar, Azure Power Global Limited, and SMA Solar Technology AG.

Innovation is driven by government policies promoting renewable energy adoption, the declining cost of solar PV technology, and increasing demand for cleaner energy. Regulatory frameworks such as the Jawaharlal Nehru National Solar Mission (JNNSM) play a crucial role in shaping the industry’s growth. Product substitutes, primarily other renewable energy sources, exert limited pressure given the cost-effectiveness and scalability of solar PV. End-user trends show a strong shift towards large-scale utility projects, alongside increasing uptake in C&I and residential segments. M&A activity is moderate, with deal values fluctuating depending on market conditions. Key deals have focused on strengthening supply chains, expanding project portfolios, and gaining market share. Estimates suggest xx Million in M&A deal value in the past 5 years, although accurate data is difficult to obtain. The average market share of the top 5 players is approximately xx%.

India Solar Photovoltaic Industry Industry Trends & Insights

The Indian solar PV industry is experiencing rapid growth, propelled by several factors. The government's commitment to renewable energy targets, coupled with decreasing solar PV costs and improving grid infrastructure, is driving substantial market expansion. The Compound Annual Growth Rate (CAGR) for the industry during the historical period (2019-2024) was estimated at xx%, and is projected to reach xx% during the forecast period (2025-2033). Technological advancements, including higher-efficiency solar cells and improved energy storage solutions, are enhancing the competitiveness of solar PV. Consumer preferences are increasingly shifting towards cost-effective, reliable, and sustainable energy solutions, further boosting demand. Competitive dynamics are marked by intense rivalry among domestic and international players, leading to continuous innovation and price reductions. Market penetration is gradually increasing across all segments, particularly in the utility sector, indicating strong growth potential for the foreseeable future. Challenges exist in grid integration and land acquisition, but the overall trend points toward sustained growth.

Dominant Markets & Segments in India Solar Photovoltaic Industry

By Type: Crystalline silicon technology currently dominates the Indian solar PV market, holding over xx% of the market share. This is primarily due to its established technology, lower manufacturing costs, and higher efficiency compared to thin-film solar cells. Thin-film technology, while less dominant, has niche applications and is expected to witness moderate growth.

By End-User: The utility sector is the largest segment of the Indian solar PV market. This is primarily because of the large-scale projects undertaken by government agencies and private developers for generating electricity. The C&I sector is showing consistent growth due to the increasing awareness of environmental sustainability and energy cost savings. Residential solar PV adoption is increasing although at a slower rate due to higher initial investment costs and challenges with rooftop installations in densely populated areas.

By Deployment: Ground-mounted solar PV projects account for the largest share of the market due to their suitability for large-scale installations and higher energy yields. Rooftop solar PV is gaining traction in the residential and C&I segments, driven by policies encouraging distributed generation. The growth in ground mounted solar projects is primarily driven by government initiatives, supporting large-scale solar parks and infrastructure projects.

Key drivers for this dominance include supportive government policies, such as financial incentives and streamlined permitting processes, alongside a robust infrastructure development program supporting transmission lines and grid integration. The vast potential for solar energy generation in India also plays a pivotal role.

India Solar Photovoltaic Industry Product Developments

Recent product innovations focus on enhancing efficiency, durability, and cost-effectiveness of solar PV modules. Technological advancements, including the use of PERC (Passivated Emitter and Rear Cell) technology and bifacial solar cells, are improving energy generation capabilities. These advancements, coupled with improved energy storage solutions and smart grid technologies, are improving the overall competitiveness of solar PV systems. The market is seeing a shift towards larger-capacity modules, leading to reduced balance-of-system costs and facilitating faster project deployment. This trend is driven by both technological improvements and economies of scale.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Indian solar PV market, segmented by type, end-user, and deployment.

By Type: The report assesses the market size and growth prospects for both crystalline silicon and thin-film solar PV technologies, highlighting the competitive landscape and technology trends. The crystalline silicon segment is projected to dominate, while thin-film is expected to witness niche growth.

By End-User: The report analyzes the market for residential, C&I, and utility solar PV systems. The utility segment is anticipated to continue leading, while the C&I segment is expected to grow robustly. The residential segment shows potential but faces adoption hurdles.

By Deployment: The analysis covers ground-mounted and rooftop solar PV installations. Ground-mounted projects hold a significant share, while rooftop installations are seeing rising adoption.

Growth projections for each segment are presented, taking into account various factors like technology advancements, government policies, and market competition.

Key Drivers of India Solar Photovoltaic Industry Growth

The growth of the Indian solar PV industry is driven by several factors. The government's ambitious renewable energy targets, aiming for significant solar capacity additions, provide a strong impetus. Decreasing solar PV costs make solar energy increasingly competitive with traditional sources. Furthermore, supportive policies and financial incentives accelerate adoption. Technological advancements contribute to enhanced efficiency and reduced costs, leading to wider market penetration. Finally, rising energy demand and concerns about environmental sustainability reinforce the industry's growth trajectory.

Challenges in the India Solar Photovoltaic Industry Sector

The Indian solar PV sector faces several challenges. Land acquisition for large-scale projects often poses significant hurdles, leading to delays and increased costs. Grid integration can be problematic in certain regions, hindering the seamless flow of solar energy into the national grid. Intermittency of solar power necessitates robust energy storage solutions, but the deployment of battery storage systems presents cost and technological challenges. Furthermore, supply chain disruptions and import dependencies can affect the industry's overall growth. Estimates suggest that these factors have contributed to a xx% reduction in project completion rates in some areas.

Emerging Opportunities in India Solar Photovoltaic Industry

The Indian solar PV industry presents numerous opportunities. The growing demand for clean energy, driven by environmental concerns and increasing energy needs, opens vast possibilities. The development of smart grids and integrated energy management systems offer avenues for value creation. The integration of solar PV with energy storage solutions enhances grid stability and promotes energy access in remote areas. Furthermore, the development of innovative financing mechanisms can attract greater private sector investment. The burgeoning C&I sector presents a significant growth opportunity.

Leading Players in the India Solar Photovoltaic Industry Market

- Adani Group

- Hanwha Q CELLS Co Ltd

- Vikram Solar Limited

- EMMVEE SOLAR

- Trina Solar Limited

- Sterling And Wilson Pvt Ltd

- Tata Power Solar Systems Ltd

- Mahindra Susten Pvt Ltd

- First Solar Inc

- ABB

- ACME Solar

- Azure Power Global Limited

- SMA Solar Technology AG

Key Developments in India Solar Photovoltaic Industry Industry

January 2022: SJVN secured a 125MW solar project in Uttar Pradesh, comprising 75MW in Jalaun and 50MW in Kanpur Dehat. This highlights the ongoing growth in utility-scale solar projects.

December 2021: Tata Power secured India's largest solar plus battery project (100MW solar, 120MWh battery storage) from SECI, signifying the increasing importance of energy storage solutions.

Strategic Outlook for India Solar Photovoltaic Industry Market

The Indian solar PV market is poised for significant growth in the coming years. Continued government support, decreasing technology costs, and rising energy demand are key catalysts. The integration of solar PV with energy storage and smart grid technologies will further enhance the sector's attractiveness. Focus on efficiency improvements, cost reduction, and supply chain diversification will be crucial for continued success. The increasing adoption of rooftop solar in the residential and C&I segments offers substantial market expansion opportunities. The long-term outlook is extremely positive, driven by India's ambitious renewable energy goals and the urgent need for clean energy solutions.

India Solar Photovoltaic Industry Segmentation

-

1. Type

- 1.1. Thin film

- 1.2. Crystalline Silicon

-

2. End-User

- 2.1. Residential

- 2.2. Commercial and Indudstrial (C&I)

- 2.3. Utility

-

3. Deployment

- 3.1. Ground-mounted

- 3.2. Rooftop-Solar

India Solar Photovoltaic Industry Segmentation By Geography

- 1. India

India Solar Photovoltaic Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 8.90% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Supportive Government Policies for Developing Solar Energy4.; Declining Cost of Solar Power Technology

- 3.3. Market Restrains

- 3.3.1. 4.; Unpredictability in the Continuity of Power Supply

- 3.4. Market Trends

- 3.4.1. Rooftop Solar PV Segment Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Thin film

- 5.1.2. Crystalline Silicon

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Residential

- 5.2.2. Commercial and Indudstrial (C&I)

- 5.2.3. Utility

- 5.3. Market Analysis, Insights and Forecast - by Deployment

- 5.3.1. Ground-mounted

- 5.3.2. Rooftop-Solar

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

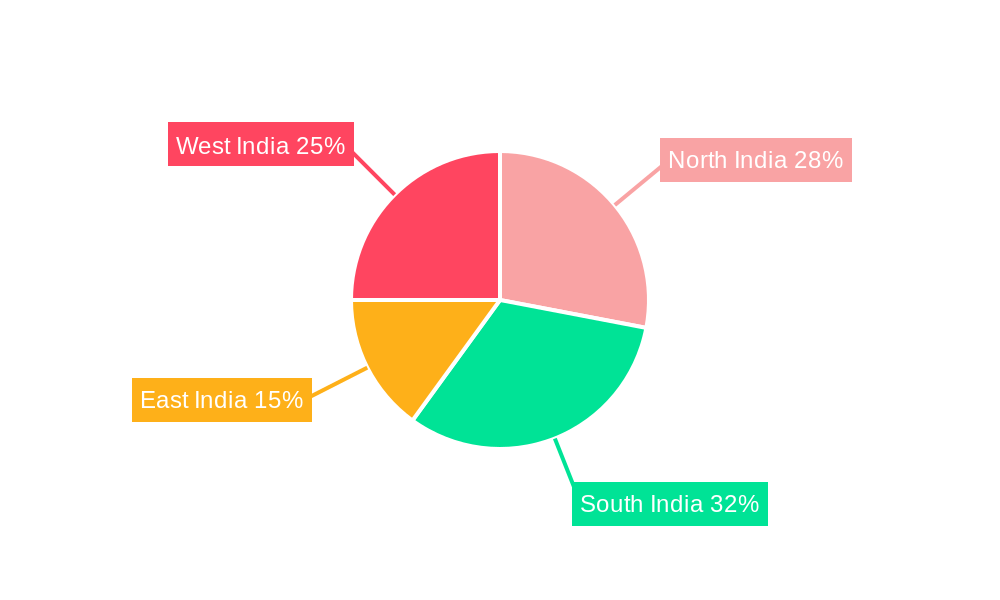

- 6. North India India Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India India Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India India Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India India Solar Photovoltaic Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 2 Adani Group

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 3 Hanwha Q CELLS Co Ltd

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 8 Vikram Solar Limited

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 4 EMMVEE SOLAR

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 5 Trina Solar Limited*List Not Exhaustive

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Domestic Players

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 6 Sterling And Wilson Pvt Ltd

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 7 Tata Power Solar Systems Ltd

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 5 Mahindra Susten Pvt Ltd

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Foreign Players

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 2 First Solar Inc

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 1 ABB

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 1 ACME Solar

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 3 Azure Power Global Limited

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.15 4 SMA Solar Technology AG

- 10.2.15.1. Overview

- 10.2.15.2. Products

- 10.2.15.3. SWOT Analysis

- 10.2.15.4. Recent Developments

- 10.2.15.5. Financials (Based on Availability)

- 10.2.1 2 Adani Group

List of Figures

- Figure 1: India Solar Photovoltaic Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Solar Photovoltaic Industry Share (%) by Company 2024

List of Tables

- Table 1: India Solar Photovoltaic Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Solar Photovoltaic Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: India Solar Photovoltaic Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 4: India Solar Photovoltaic Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 5: India Solar Photovoltaic Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: India Solar Photovoltaic Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: North India India Solar Photovoltaic Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: South India India Solar Photovoltaic Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: East India India Solar Photovoltaic Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: West India India Solar Photovoltaic Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: India Solar Photovoltaic Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 12: India Solar Photovoltaic Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 13: India Solar Photovoltaic Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 14: India Solar Photovoltaic Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Solar Photovoltaic Industry?

The projected CAGR is approximately > 8.90%.

2. Which companies are prominent players in the India Solar Photovoltaic Industry?

Key companies in the market include 2 Adani Group, 3 Hanwha Q CELLS Co Ltd, 8 Vikram Solar Limited, 4 EMMVEE SOLAR, 5 Trina Solar Limited*List Not Exhaustive, Domestic Players, 6 Sterling And Wilson Pvt Ltd, 7 Tata Power Solar Systems Ltd, 5 Mahindra Susten Pvt Ltd, Foreign Players, 2 First Solar Inc, 1 ABB, 1 ACME Solar, 3 Azure Power Global Limited, 4 SMA Solar Technology AG.

3. What are the main segments of the India Solar Photovoltaic Industry?

The market segments include Type, End-User, Deployment.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Policies for Developing Solar Energy4.; Declining Cost of Solar Power Technology.

6. What are the notable trends driving market growth?

Rooftop Solar PV Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Unpredictability in the Continuity of Power Supply.

8. Can you provide examples of recent developments in the market?

In January 2022, SJVN (Satluj Jal Vidyut Nigam Ltd.) bagged a solar project of 125MW in Uttar Pradesh, through a bidding process held by Uttar Pradesh New and Renewable Energy Development Agency (UPNEDA). It includes a 75MW grid-connected solar PV project in Jalaun and a 50MW solar project in Kanpur Dehat districts.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Solar Photovoltaic Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Solar Photovoltaic Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Solar Photovoltaic Industry?

To stay informed about further developments, trends, and reports in the India Solar Photovoltaic Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence