Key Insights

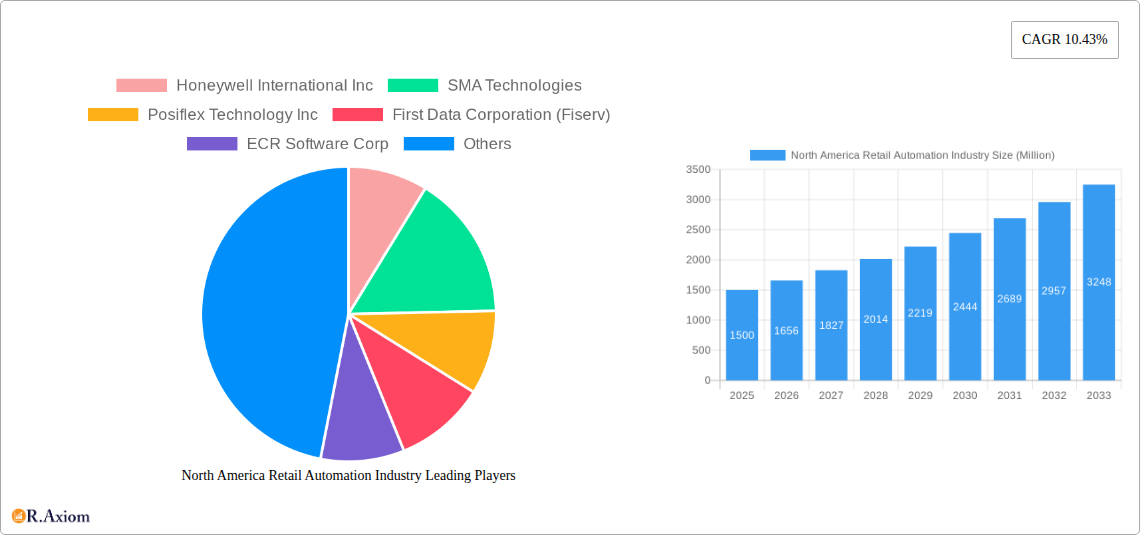

The North American retail automation market, valued at approximately $XX million in 2025, is projected to experience robust growth, driven by a compound annual growth rate (CAGR) of 10.43% from 2025 to 2033. This expansion is fueled by several key factors. The increasing adoption of self-checkout kiosks, automated inventory management systems, and advanced analytics platforms across various retail segments—grocery, general merchandise, and hospitality—is significantly boosting market demand. E-commerce growth and the need for efficient order fulfillment are further driving automation investments. Furthermore, labor shortages and the escalating costs associated with manual processes are compelling retailers to embrace automation solutions for improved operational efficiency and cost reduction. The United States, being the largest economy in North America, represents a significant portion of the market share, followed by Canada. Technological advancements, such as the integration of artificial intelligence (AI) and machine learning (ML) in retail automation systems, are enhancing functionalities and driving market growth further.

However, high initial investment costs associated with automation technologies and the potential need for significant workforce retraining pose challenges to market expansion. Concerns regarding data security and system integration complexities also act as potential restraints. Nevertheless, the long-term benefits of improved efficiency, reduced operational costs, and enhanced customer experiences are expected to outweigh these initial hurdles, ensuring continued market growth throughout the forecast period. The market segmentation by component (hardware and software) and end-user (grocery, general merchandise, hospitality) provides valuable insights for strategic planning and investment decisions. Specific sub-segments within grocery, such as supermarkets and convenience stores, are expected to show particularly strong growth given their high transaction volumes and the potential for automation to streamline operations significantly.

This in-depth report provides a comprehensive analysis of the North America retail automation industry, covering market size, segmentation, growth drivers, challenges, and key players. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The forecast period is 2025-2033, and the historical period encompasses 2019-2024. This report is essential for industry stakeholders, investors, and businesses seeking to understand the dynamics and future potential of this rapidly evolving market.

North America Retail Automation Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the North American retail automation market, examining market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and mergers & acquisitions (M&A) activities. The market is moderately concentrated, with a few major players holding significant market share. However, the presence of numerous smaller, specialized companies indicates a dynamic and competitive environment.

Market Concentration: The top 5 players account for approximately xx% of the market share in 2025, indicating a moderately concentrated market. This concentration is expected to remain relatively stable over the forecast period, though smaller companies may gain share through innovation and niche specialization.

Innovation Drivers: Key drivers of innovation include the increasing demand for enhanced efficiency, improved customer experience, and reduced operational costs. Advancements in artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT) are fueling the development of sophisticated automation solutions.

Regulatory Framework: The regulatory environment varies across North America, with differing regulations concerning data privacy, security, and labor laws impacting the adoption of automation technologies.

Product Substitutes: While automation offers significant advantages, there are alternative solutions, such as manual processes or legacy systems. However, the cost-effectiveness and efficiency gains of automation are driving rapid adoption.

End-User Trends: Retailers are increasingly focusing on omnichannel strategies, demanding integrated solutions that seamlessly connect online and offline operations. This trend fuels demand for advanced automation technologies.

M&A Activities: The retail automation industry has witnessed several significant M&A activities in recent years, with deal values reaching xx Million in 2024. These activities are driven by the need to expand market reach, access new technologies, and consolidate market share. Examples include [mention specific examples if available, with deal values].

North America Retail Automation Industry Industry Trends & Insights

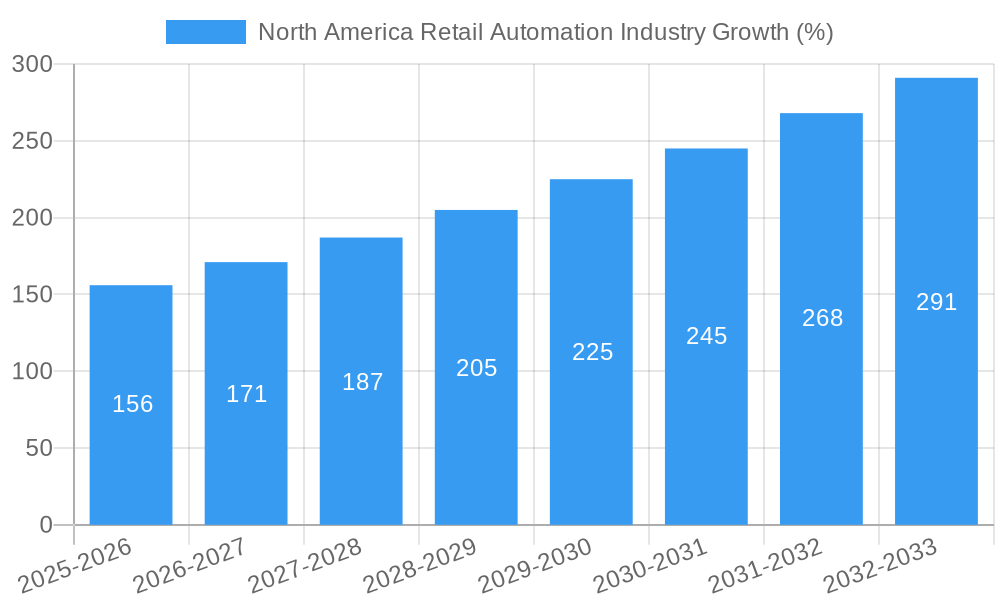

The North American retail automation market is experiencing robust growth, driven by several key factors. The market is projected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration of retail automation solutions is expected to reach xx% by 2033, up from xx% in 2025.

The increasing adoption of e-commerce and omnichannel retailing is a major growth driver, necessitating efficient order fulfillment and inventory management systems. Technological advancements, such as AI and IoT-enabled solutions, are enhancing the capabilities of retail automation systems, leading to greater efficiency and productivity. Consumers are demanding faster delivery times and personalized shopping experiences, putting pressure on retailers to adopt automation technologies to meet these expectations. The competitive landscape is highly dynamic, with both established players and emerging companies vying for market share through innovation and strategic partnerships. These factors collectively contribute to the impressive growth trajectory of the North American retail automation market.

Dominant Markets & Segments in North America Retail Automation Industry

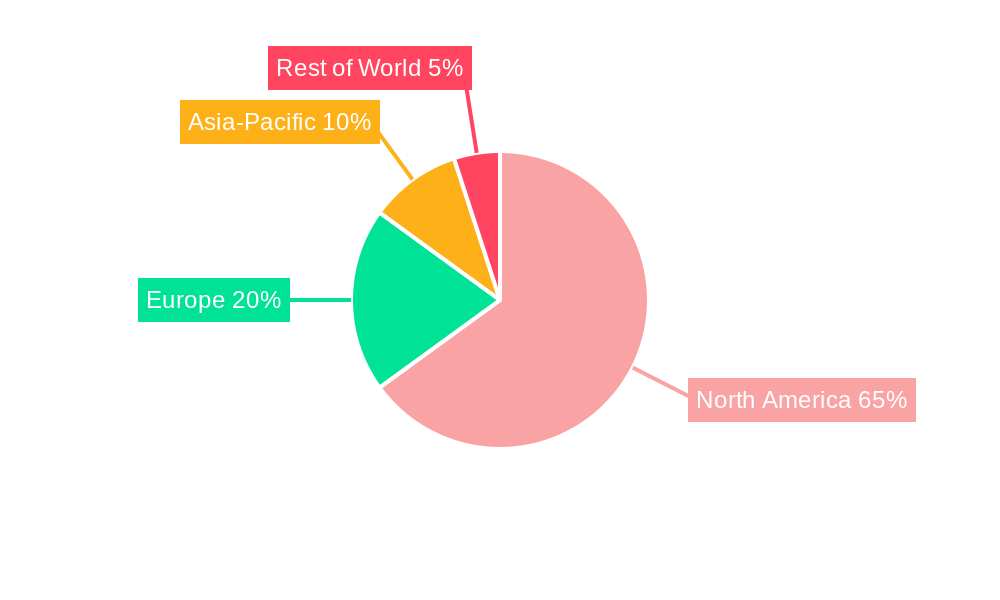

The United States dominates the North American retail automation market, owing to its large retail sector and higher adoption rate of automation technologies. Canada also shows significant growth potential, driven by increasing investments in retail infrastructure and technological advancements.

By Component:

Hardware: This segment is expected to maintain its dominance, driven by the need for robust and reliable physical infrastructure for automated systems.

Software: The software segment is experiencing rapid growth, fueled by the increasing demand for sophisticated analytics and data management capabilities.

By End-User:

Grocery: This segment represents a significant portion of the market, with supermarkets and hypermarkets driving the demand for automation solutions to streamline operations and enhance customer experience.

General Merchandise: The general merchandise segment is witnessing increasing adoption of automation technologies across hardgoods, softgoods, and mixed general merchandise stores.

Hospitality: The hospitality industry is increasingly leveraging automation solutions to improve efficiency and customer service in hotels and restaurants.

Key Drivers:

- Favorable economic conditions in the US and Canada.

- Government initiatives promoting technological advancements.

- Strong retail infrastructure.

North America Retail Automation Industry Product Developments

Recent product innovations focus on integrated solutions combining hardware and software to optimize various retail functions, such as inventory management, point-of-sale (POS) systems, and customer relationship management (CRM). These systems utilize AI and ML for predictive analytics, improving efficiency and enhancing the customer experience. The competitive advantage lies in the integration of multiple functionalities into a unified platform, enabling seamless data flow and real-time insights. This trend reflects the broader shift towards comprehensive solutions rather than standalone products.

Report Scope & Segmentation Analysis

This report segments the North American retail automation market by component (hardware and software) and end-user (grocery, general merchandise, and hospitality). It further breaks down the market by country (United States and Canada). Growth projections are provided for each segment, alongside detailed market size estimations and competitive landscape analysis. The grocery segment shows the highest growth potential, driven by the increasing demand for efficient supply chain management and enhanced customer experience in supermarkets and hypermarkets. The software segment is projected to grow at a faster rate than the hardware segment, reflecting the increasing importance of data analytics and sophisticated software solutions.

Key Drivers of North America Retail Automation Industry Growth

Technological advancements, particularly in AI, ML, and IoT, are significantly driving market growth. Economic factors, such as increased consumer spending and retailer investments in improving operational efficiency, further contribute to the expansion. Favorable government regulations and policies promoting technological adoption are also supportive factors. For instance, tax incentives for businesses investing in automation technologies are influencing market growth.

Challenges in the North America Retail Automation Industry Sector

Implementation costs can be substantial, representing a significant barrier for smaller retailers. Supply chain disruptions and shortages of critical components can impact the availability and cost of automation solutions. Intense competition and the need for continuous innovation pose challenges to established players. These challenges, if not effectively addressed, could impact market growth. For example, a xx% increase in component costs in 2022 led to a xx% slowdown in deployment in the smaller retail segment.

Emerging Opportunities in North America Retail Automation Industry

The rise of e-commerce and omnichannel retailing presents significant opportunities for the development and adoption of innovative automation solutions. Advancements in robotics and automation are creating opportunities for task automation in areas like warehouse operations and inventory management. Increased focus on data security and personalized customer experiences creates demand for sophisticated automation systems. These trends represent substantial growth potential for companies operating in this sector.

Leading Players in the North America Retail Automation Industry Market

- Honeywell International Inc

- SMA Technologies

- Posiflex Technology Inc

- First Data Corporation (Fiserv)

- ECR Software Corp

- NCR Corporation

- Fujitsu Limited

- Diebold Nixdorf Incorporated

- Zebra Technologies Corporation

- Datalogic SpA

Key Developments in North America Retail Automation Industry Industry

April 2023: Walmart Inc. announces plans to automate two-thirds of its stores by the end of 2026, focusing on improved inventory management and enhanced customer experience. This initiative significantly impacts the market, increasing demand for automation solutions.

February 2023: United Natural Foods Inc. (UNFI) partners with ECRS to integrate its Professional Services suite with ECRS’ CATAPULT POS system. This collaboration enhances the functionalities of retail automation systems, impacting market dynamics.

Strategic Outlook for North America Retail Automation Industry Market

The North American retail automation market is poised for continued growth, driven by technological advancements, evolving consumer preferences, and the increasing need for operational efficiency among retailers. The market will witness further integration of AI, ML, and IoT technologies into automation systems, leading to more sophisticated and intelligent solutions. Opportunities exist for companies offering comprehensive, integrated solutions that cater to the specific needs of different retail segments. The focus will shift toward solutions that enhance customer experience, improve supply chain efficiency, and improve data security.

North America Retail Automation Industry Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

-

2. End-User

- 2.1. Grocery

- 2.2. General

- 2.3. Hospital

North America Retail Automation Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Retail Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.43% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Faster Services; Growth Among Retail Industry and E-commerce; Increasing Retail Automation in Grocery Stores

- 3.3. Market Restrains

- 3.3.1. Slow Adoption of Automated Machine Learning Tools

- 3.4. Market Trends

- 3.4.1. Grocery Segment is expected grow at a higher pace.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Grocery

- 5.2.2. General

- 5.2.3. Hospital

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. United States North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Retail Automation Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Honeywell International Inc

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 SMA Technologies

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Posiflex Technology Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 First Data Corporation (Fiserv)

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 ECR Software Corp

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 NCR Corporation

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Fujitsu Limited

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Diebold Nixdorf Incorporated

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Zebra Technologies Corporation

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Datalogic SpA

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Honeywell International Inc

List of Figures

- Figure 1: North America Retail Automation Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Retail Automation Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Retail Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Retail Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 3: North America Retail Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 4: North America Retail Automation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: North America Retail Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: North America Retail Automation Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 11: North America Retail Automation Industry Revenue Million Forecast, by End-User 2019 & 2032

- Table 12: North America Retail Automation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 13: United States North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Retail Automation Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Retail Automation Industry?

The projected CAGR is approximately 10.43%.

2. Which companies are prominent players in the North America Retail Automation Industry?

Key companies in the market include Honeywell International Inc, SMA Technologies, Posiflex Technology Inc, First Data Corporation (Fiserv), ECR Software Corp, NCR Corporation, Fujitsu Limited, Diebold Nixdorf Incorporated, Zebra Technologies Corporation, Datalogic SpA.

3. What are the main segments of the North America Retail Automation Industry?

The market segments include Component, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Faster Services; Growth Among Retail Industry and E-commerce; Increasing Retail Automation in Grocery Stores.

6. What are the notable trends driving market growth?

Grocery Segment is expected grow at a higher pace..

7. Are there any restraints impacting market growth?

Slow Adoption of Automated Machine Learning Tools.

8. Can you provide examples of recent developments in the market?

In April 2023, Walmart Inc. plans to automate two-thirds of its stores by the end of 2026 to improve inventory accuracy and flow, reduce costs, and enhance the overall shopping experience. The move is part of the organization’s strategy to reengineer its supply chain and make a more intelligent and connected omnichannel network to meet customers’ needs better. This involves a more significant use of data, intelligent software, and automation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Retail Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Retail Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Retail Automation Industry?

To stay informed about further developments, trends, and reports in the North America Retail Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence