Key Insights

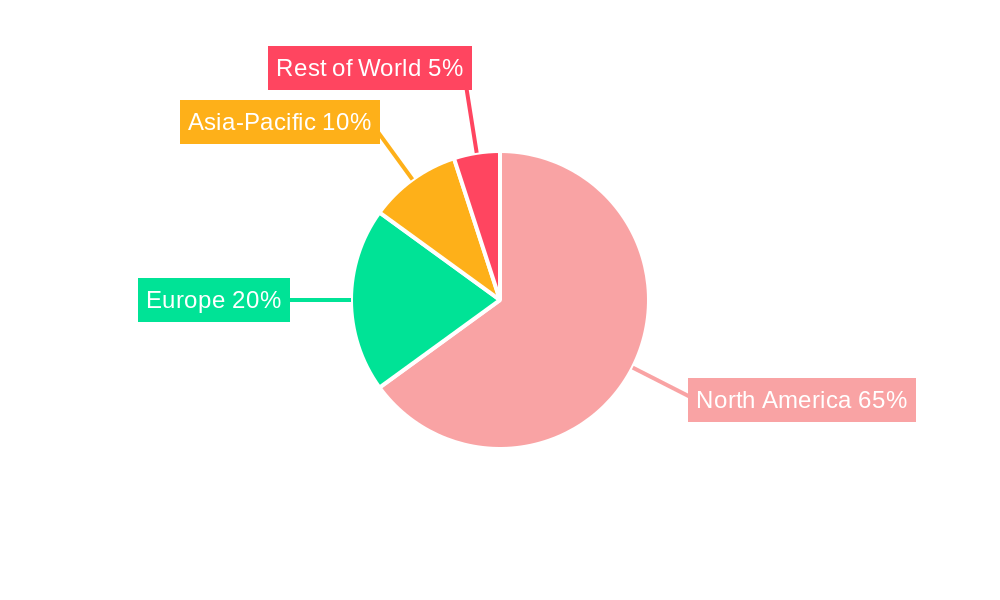

The North American smart grid technology market is experiencing robust growth, driven by increasing energy demands, the need for improved grid reliability and efficiency, and the integration of renewable energy sources. The market's Compound Annual Growth Rate (CAGR) exceeding 6.00% from 2019 to 2024 suggests a significant upward trajectory, projected to continue through 2033. Key growth drivers include the expanding adoption of advanced metering infrastructure (AMI) for enhanced energy monitoring and management, the implementation of demand-response programs to optimize energy consumption, and the upgrading of transmission systems to accommodate increased renewable energy integration. The market is segmented by technology application area (transmission, demand response, AMI, and others), company type (manufacturer, supplier, distributor), and application (residential, commercial, and industrial). Major players like Itron Inc, Honeywell International Inc, ABB Ltd, and Siemens AG are actively shaping the market through technological innovations and strategic partnerships. The United States, as the largest economy in North America, holds the dominant market share, followed by Canada and Mexico. However, growth opportunities are also emerging in the rest of North America, driven by increasing government initiatives promoting smart grid adoption and energy efficiency.

The substantial investment in smart grid technologies across North America is further propelled by the increasing concerns regarding climate change and the necessity for a sustainable energy future. The shift towards decarbonization and the integration of distributed energy resources (DERs) are crucial factors driving the demand for smart grid solutions. The residential sector is witnessing considerable growth owing to rising consumer awareness and the availability of smart home technologies. Commercial and industrial sectors are adopting smart grid technologies to optimize energy costs, improve operational efficiency, and reduce their environmental footprint. While some restraints exist, such as high initial investment costs and the complexity of integrating diverse technologies, these are being mitigated by government incentives, technological advancements, and innovative financing models. The forecast period (2025-2033) is expected to witness further market expansion, driven by the continued deployment of smart grid technologies across various sectors and regions.

North America Smart Grid Technology Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North America Smart Grid Technology market, covering the period 2019-2033. It offers actionable insights for stakeholders, including manufacturers, suppliers, distributors, and investors, by examining market trends, key players, and future growth opportunities. The report uses 2025 as the base year and provides forecasts until 2033. The market is segmented by technology application area (Transmission, Demand Response, Advanced Metering Infrastructure (AMI), Other), company type (Manufacturer, Supplier, Distributor), and application (Residential, Commercial, Industrial).

North America Smart Grid Technology Market Concentration & Innovation

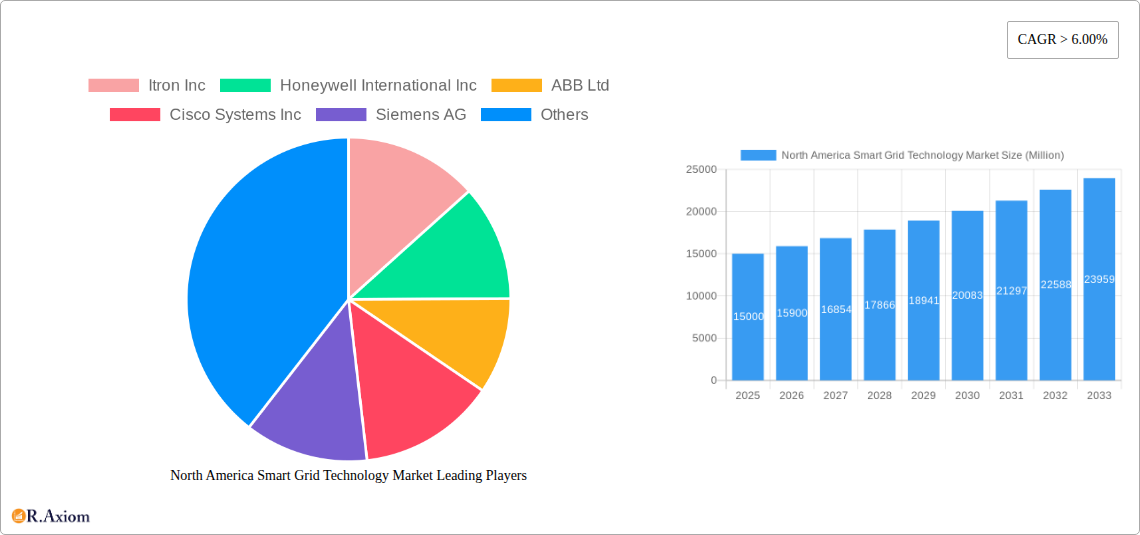

The North American smart grid technology market exhibits a moderately concentrated landscape, with several major players holding significant market share. Itron Inc, Honeywell International Inc, ABB Ltd, Cisco Systems Inc, Siemens AG, Schneider Electric SE, Hitachi Ltd, Eaton Corporation PLC, and General Electric Company are key players, though the market also encompasses numerous smaller, specialized firms. Market share data for 2025 estimates Itron Inc at xx%, Honeywell International Inc at xx%, ABB Ltd at xx%, and the remaining players sharing the rest. Mergers and acquisitions (M&A) activity has been a notable factor, with deal values ranging from USD xx Million to USD xx Million in recent years, primarily focused on expanding technological capabilities and geographical reach. Innovation is driven by the need for enhanced grid reliability, efficiency, and integration of renewable energy sources. Stringent regulatory frameworks, particularly in the US and Canada, mandate upgrades and smart grid deployments, further fueling innovation. Product substitutes, such as improved traditional grid infrastructure, pose limited competition given the superior capabilities of smart grid technologies. End-user trends indicate a growing preference for real-time monitoring, data analytics, and improved customer service provided by smart grids.

North America Smart Grid Technology Market Industry Trends & Insights

The North American smart grid technology market is experiencing robust growth, driven by several key factors. Government initiatives promoting energy efficiency and renewable energy integration, alongside increasing energy demand and aging infrastructure, are major catalysts. Technological advancements, such as the development of advanced sensors, communication protocols, and data analytics tools, are significantly enhancing smart grid capabilities. Consumer preferences are shifting toward greater transparency and control over energy consumption, leading to higher adoption of smart meters and demand-response programs. The market is also witnessing a surge in cybersecurity investments to protect against potential threats. The overall market is projected to exhibit a CAGR of xx% during the forecast period (2025-2033), with market penetration steadily increasing across various segments. Competitive dynamics are characterized by intense rivalry among established players and the emergence of innovative startups.

Dominant Markets & Segments in North America Smart Grid Technology Market

Leading Region: The US dominates the North American smart grid market due to its large energy consumption, extensive grid infrastructure, and substantial government investments. Canada holds a significant, albeit smaller, share.

Dominant Technology Application Area: Advanced Metering Infrastructure (AMI) currently holds the largest market share, driven by widespread adoption of smart meters for improved energy monitoring and billing. Demand response programs are also growing rapidly.

Leading Company Type: Manufacturers currently hold the largest share, however, suppliers and distributors are also expanding their roles and market presence in the support services and smart grid technology integrations.

Dominant Application: The commercial and industrial sectors are exhibiting strong growth, driven by energy cost optimization initiatives and the increasing integration of distributed energy resources. Residential adoption is also gaining traction but at a slower pace.

Key drivers for the dominant segments include supportive economic policies favoring renewable energy integration, robust investment in grid modernization, and government regulations promoting grid efficiency and resilience.

North America Smart Grid Technology Market Product Developments

Recent product innovations focus on enhancing grid automation, improving data analytics capabilities, and strengthening cybersecurity features. New technologies like AI and machine learning are being integrated into smart grid solutions for predictive maintenance and improved grid management. These innovations offer competitive advantages by providing greater efficiency, reliability, and security. Market fit is strong, especially with rising consumer demand for sustainable and efficient energy solutions.

Report Scope & Segmentation Analysis

This report segments the North American smart grid technology market in the following ways:

Technology Application Area: Transmission, Demand Response, AMI, Other. Each segment exhibits different growth projections reflecting specific market dynamics and technological maturity. AMI is currently the largest segment, while transmission is expected to experience significant growth in the coming years.

Company Type: Manufacturer, Supplier, Distributor. Market sizes and competitive dynamics vary significantly across these categories. Manufacturers dominate, however, the roles of suppliers and distributors are becoming more crucial in the rapidly expanding market.

Application: Residential, Commercial, Industrial. Growth rates differ based on adoption rates, technological needs, and economic factors in each sector. The commercial and industrial sectors currently represent the largest markets.

Key Drivers of North America Smart Grid Technology Market Growth

The market's growth is fueled by factors such as:

- Government initiatives: The USD 10.5 billion Grid Resilience and Innovation Partnership program in the US (September 2022) exemplifies strong government support for smart grid development.

- Technological advancements: Improvements in data analytics, AI, and communication technologies constantly enhance smart grid capabilities.

- Rising energy demand and aging infrastructure: The need to modernize and upgrade aging grid infrastructure is driving adoption.

Challenges in the North America Smart Grid Technology Market Sector

Challenges include:

- High initial investment costs: The significant upfront investment required for smart grid implementation can be a deterrent for some stakeholders.

- Cybersecurity concerns: The increasing complexity of smart grids raises concerns about potential cyberattacks.

- Interoperability issues: Ensuring seamless communication and data exchange between different smart grid components remains a challenge.

These factors can potentially impact market growth by slowing adoption rates.

Emerging Opportunities in North America Smart Grid Technology Market

Opportunities exist in:

- Microgrids and distributed energy resources (DERs): The integration of DERs necessitates advanced smart grid management solutions.

- Advanced data analytics and AI: Leveraging these technologies to optimize grid operations offers significant potential.

- Expanding into rural areas: Addressing energy access and reliability issues in underserved areas presents significant opportunities.

Leading Players in the North America Smart Grid Technology Market Market

- Itron Inc

- Honeywell International Inc

- ABB Ltd

- Cisco Systems Inc

- Siemens AG

- Schneider Electric SE

- Hitachi Ltd

- Eaton Corporation PLC

- General Electric Company

Key Developments in North America Smart Grid Technology Market Industry

- February 2023: Trilliant's strategic agreement with Grupo Saesa expands AMI and smart grid adoption in South America, demonstrating the global reach of these technologies and the potential for future partnerships.

- September 2022: The US Department of Energy's USD 10.5 billion investment in grid resilience and innovation significantly boosts market growth and accelerates smart grid deployment.

Strategic Outlook for North America Smart Grid Technology Market Market

The North American smart grid technology market is poised for significant growth in the coming years. Continued government support, technological advancements, and increasing consumer demand for sustainable energy will drive market expansion. Opportunities exist in various segments, particularly AMI and demand response, creating attractive prospects for both established players and new entrants. The market's future hinges on addressing challenges like cybersecurity risks and interoperability issues, ensuring sustainable and widespread adoption.

North America Smart Grid Technology Market Segmentation

-

1. Technology Application Area

- 1.1. Transmission

- 1.2. Demand Response

- 1.3. Advanced Metering Infrastructure (AMI)

- 1.4. Other Technology Application Areas

-

2. Geography

- 2.1. United States

- 2.2. Canada

- 2.3. Rest of North America

North America Smart Grid Technology Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Smart Grid Technology Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

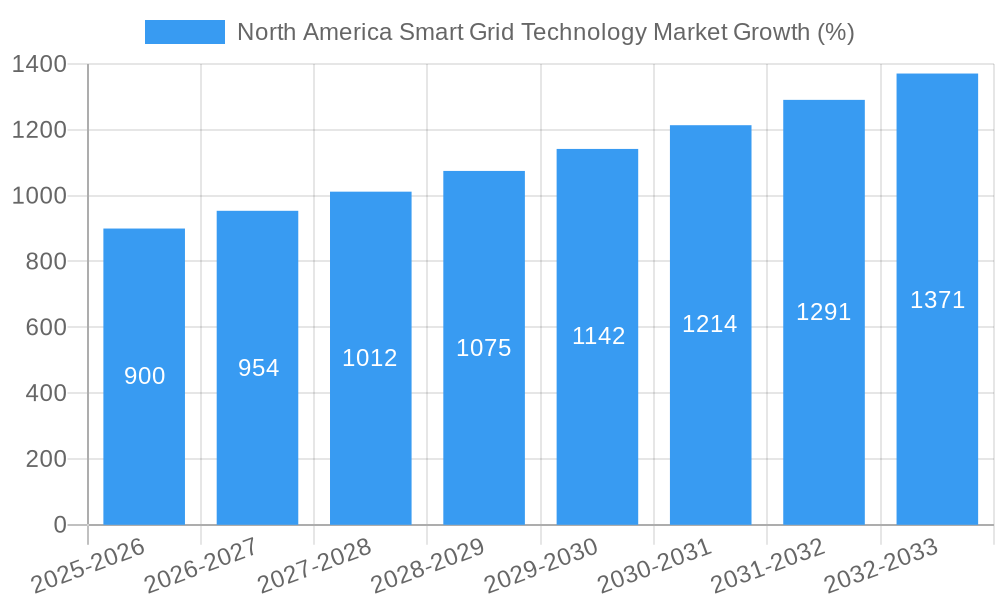

| Growth Rate | CAGR of > 6.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Growing Oil and Gas Industry4.; Rapid Growth in the Industrial Sector

- 3.3. Market Restrains

- 3.3.1. 4.; Fluctuation in Oil and Gas Prices

- 3.4. Market Trends

- 3.4.1. Advanced Metering Infrastructure to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 5.1.1. Transmission

- 5.1.2. Demand Response

- 5.1.3. Advanced Metering Infrastructure (AMI)

- 5.1.4. Other Technology Application Areas

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United States

- 5.2.2. Canada

- 5.2.3. Rest of North America

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 6. United States North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 6.1.1. Transmission

- 6.1.2. Demand Response

- 6.1.3. Advanced Metering Infrastructure (AMI)

- 6.1.4. Other Technology Application Areas

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United States

- 6.2.2. Canada

- 6.2.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 7. Canada North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 7.1.1. Transmission

- 7.1.2. Demand Response

- 7.1.3. Advanced Metering Infrastructure (AMI)

- 7.1.4. Other Technology Application Areas

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United States

- 7.2.2. Canada

- 7.2.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 8. Rest of North America North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 8.1.1. Transmission

- 8.1.2. Demand Response

- 8.1.3. Advanced Metering Infrastructure (AMI)

- 8.1.4. Other Technology Application Areas

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United States

- 8.2.2. Canada

- 8.2.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 9. United States North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Smart Grid Technology Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Itron Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Honeywell International Inc

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 ABB Ltd

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Cisco Systems Inc

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Siemens AG

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Schneider Electric SE

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Hitachi Ltd *List Not Exhaustive

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Eaton Corporation PLC

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 General Electric Company

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.1 Itron Inc

List of Figures

- Figure 1: North America Smart Grid Technology Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Smart Grid Technology Market Share (%) by Company 2024

List of Tables

- Table 1: North America Smart Grid Technology Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Smart Grid Technology Market Revenue Million Forecast, by Technology Application Area 2019 & 2032

- Table 3: North America Smart Grid Technology Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 4: North America Smart Grid Technology Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: North America Smart Grid Technology Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States North America Smart Grid Technology Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada North America Smart Grid Technology Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico North America Smart Grid Technology Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America North America Smart Grid Technology Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: North America Smart Grid Technology Market Revenue Million Forecast, by Technology Application Area 2019 & 2032

- Table 11: North America Smart Grid Technology Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 12: North America Smart Grid Technology Market Revenue Million Forecast, by Country 2019 & 2032

- Table 13: North America Smart Grid Technology Market Revenue Million Forecast, by Technology Application Area 2019 & 2032

- Table 14: North America Smart Grid Technology Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 15: North America Smart Grid Technology Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: North America Smart Grid Technology Market Revenue Million Forecast, by Technology Application Area 2019 & 2032

- Table 17: North America Smart Grid Technology Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: North America Smart Grid Technology Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Smart Grid Technology Market?

The projected CAGR is approximately > 6.00%.

2. Which companies are prominent players in the North America Smart Grid Technology Market?

Key companies in the market include Itron Inc, Honeywell International Inc, ABB Ltd, Cisco Systems Inc, Siemens AG, Schneider Electric SE, Hitachi Ltd *List Not Exhaustive, Eaton Corporation PLC, General Electric Company.

3. What are the main segments of the North America Smart Grid Technology Market?

The market segments include Technology Application Area, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Oil and Gas Industry4.; Rapid Growth in the Industrial Sector.

6. What are the notable trends driving market growth?

Advanced Metering Infrastructure to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Fluctuation in Oil and Gas Prices.

8. Can you provide examples of recent developments in the market?

February 2023: Trilliant, a major international provider of advanced metering infrastructure (AMI), smart grid, smart cities, and IoT solutions, established a long-term strategic agreement with Grupo Saesa. Grupo Saesa would use Trilliant's software and RF communication platforms for AMI, smart grid, and IIoT applications, which is expected help the company improve its customer experience while also delivering secure and dependable electricity.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Smart Grid Technology Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Smart Grid Technology Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Smart Grid Technology Market?

To stay informed about further developments, trends, and reports in the North America Smart Grid Technology Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence