Key Insights

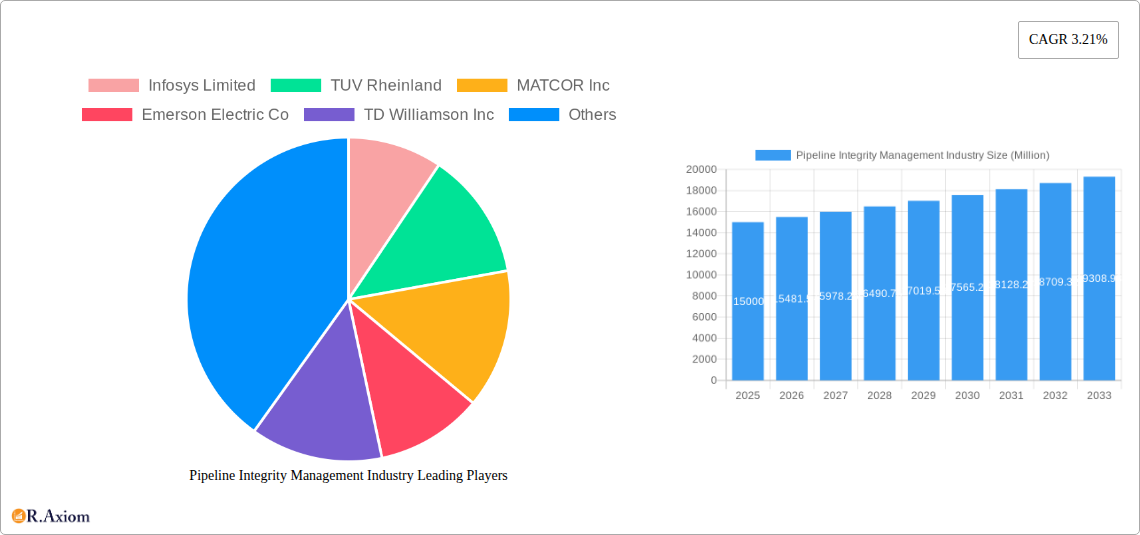

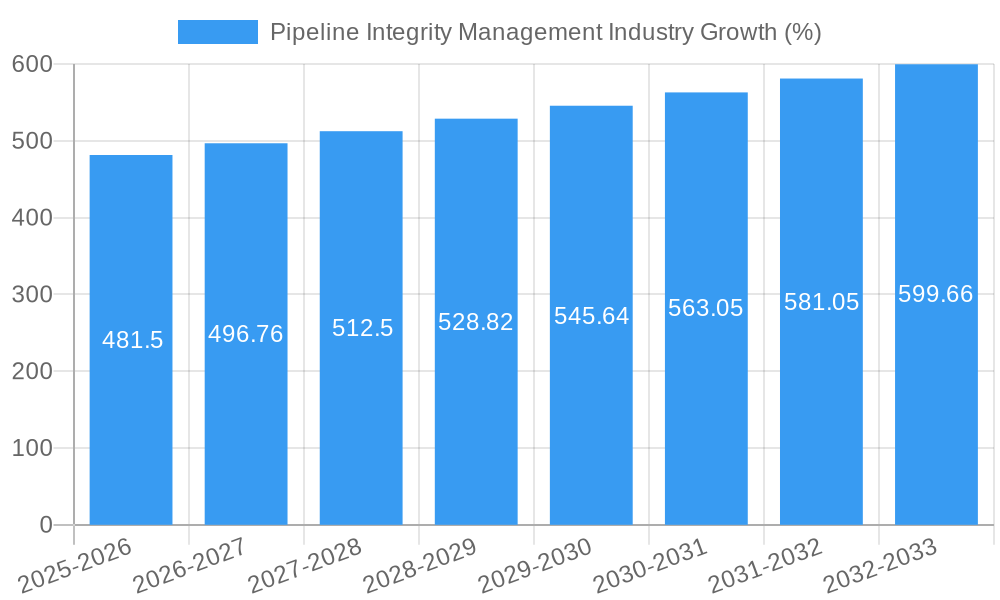

The global pipeline integrity management (PIM) market, valued at approximately $XX million in 2025, is projected to experience steady growth, driven by increasing demand for safer and more efficient pipeline operations. A compound annual growth rate (CAGR) of 3.21% from 2025 to 2033 indicates a significant expansion, reaching an estimated market size of $YY million by 2033 (Note: YY is a calculated value based on the provided CAGR and 2025 market size. Exact figure requires the missing 2025 market size "XX"). Several factors contribute to this growth, including stringent government regulations aimed at preventing pipeline failures and environmental disasters, the growing adoption of advanced technologies such as smart pigs and data analytics for improved pipeline monitoring, and the increasing need for efficient pipeline maintenance and repair in aging infrastructure across North America, Europe, and the Asia-Pacific region. The onshore segment currently dominates the market, owing to the extensive network of onshore pipelines compared to offshore pipelines. However, the offshore segment is projected to witness faster growth due to substantial investments in offshore oil and gas exploration and production. Within service types, inspection services hold the largest market share currently, but repair and refurbishment services are expected to exhibit faster growth due to the increasing age of many existing pipeline systems. Key players like Infosys, TÜV Rheinland, and Baker Hughes are leveraging technological advancements and strategic partnerships to maintain their market positions and cater to the growing demand for comprehensive PIM solutions.

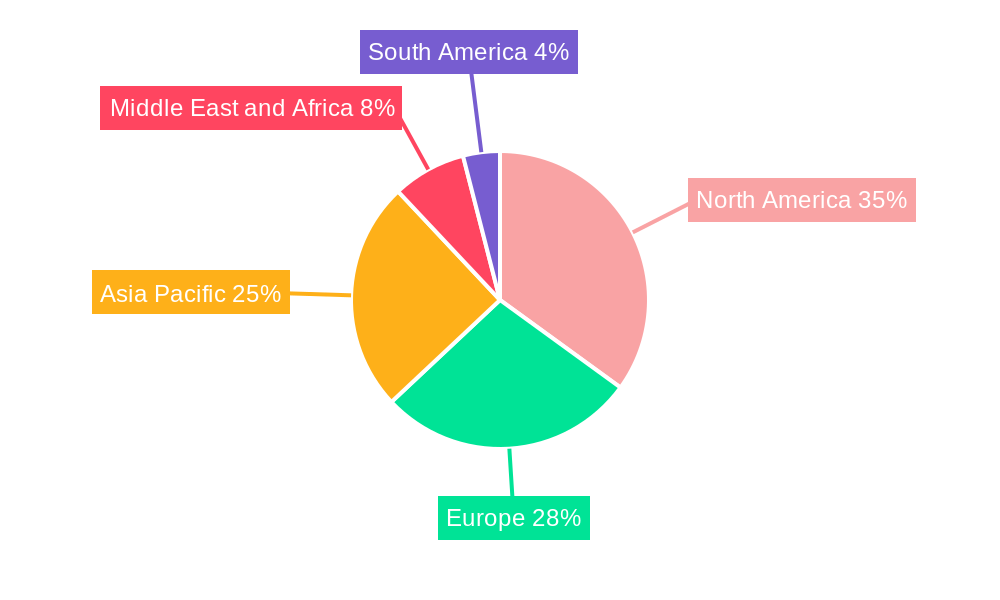

The market segmentation reveals significant regional variations. North America and Europe currently hold substantial market share due to mature pipeline infrastructure and stringent regulatory frameworks. However, the Asia-Pacific region, particularly China and India, is anticipated to experience rapid growth during the forecast period driven by the increasing energy demand and substantial investments in pipeline infrastructure development. The Middle East and Africa, fueled by the ongoing expansion of oil and gas production, also presents significant growth opportunities. While challenges such as high initial investment costs for advanced PIM technologies and skilled labor shortages exist, the long-term prospects for the pipeline integrity management market remain positive, driven by the critical need for safe and reliable pipeline operations and environmental protection.

Pipeline Integrity Management Industry: A Comprehensive Market Report (2019-2033)

This detailed report provides a comprehensive analysis of the Pipeline Integrity Management industry, covering market size, growth drivers, challenges, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The forecast period is 2025-2033, and the historical period encompasses 2019-2024. The report utilizes data-driven insights to offer actionable strategies for industry stakeholders. The market is valued at $XX Million in 2025 and is projected to reach $XX Million by 2033, exhibiting a CAGR of XX%.

Pipeline Integrity Management Industry Market Concentration & Innovation

This section analyzes the competitive landscape of the Pipeline Integrity Management industry, focusing on market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and M&A activities. The industry is moderately concentrated, with key players holding significant market share. However, the emergence of innovative technologies is fostering competition and driving market expansion. Market share data for 2025 shows that Baker Hughes Company holds approximately XX% market share, followed by Emerson Electric Co with XX%, and TUV Rheinland with XX%. The remaining market share is distributed among other players such as Infosys Limited, MATCOR Inc, TD Williamson Inc, SGS SA, TWI Ltd, EnerMech Limited, and Bureau Veritas SA.

Innovation Drivers:

- Advancements in non-destructive testing (NDT) technologies.

- Development of smart pipelines and advanced monitoring systems.

- Increased adoption of data analytics and machine learning for predictive maintenance.

Regulatory Frameworks: Stringent regulations regarding pipeline safety and environmental protection are driving the adoption of advanced integrity management practices. These regulations are increasing the demand for inspection, maintenance, and repair services.

Mergers & Acquisitions (M&A): The Pipeline Integrity Management industry has witnessed several M&A activities in recent years, primarily focused on expanding service offerings and geographical reach. The total value of M&A deals in the industry from 2019 to 2024 is estimated at $XX Million. For example, a significant M&A deal in XX involved the acquisition of a smaller pipeline inspection company by a larger player. This strengthened their position in a specific market segment.

Pipeline Integrity Management Industry Industry Trends & Insights

The Pipeline Integrity Management market is experiencing robust growth, driven by several factors. The increasing demand for oil and gas, coupled with stringent safety regulations, necessitates proactive pipeline integrity management strategies. Technological advancements in inspection technologies, such as advanced sensors and data analytics, are further accelerating market growth. A shift towards predictive maintenance, enabled by data-driven insights, is improving operational efficiency and reducing downtime. Consumer preference for enhanced safety and environmental protection is also a significant driver. Competitive dynamics are marked by both collaboration and competition. Strategic partnerships are common for sharing expertise and technology. Simultaneously, companies are investing heavily in R&D to develop innovative solutions and gain a competitive edge. The market penetration of advanced inspection techniques, such as inline inspection tools (ILI) and remotely operated vehicles (ROVs), is increasing significantly.

Dominant Markets & Segments in Pipeline Integrity Management Industry

The onshore segment dominates the Pipeline Integrity Management market, accounting for approximately XX% of the total market share in 2025. This dominance is primarily attributed to the extensive network of onshore pipelines globally and the higher probability of pipeline degradation due to environmental factors. However, the offshore segment is expected to witness significant growth in the coming years, driven by the increasing exploration and production of oil and gas in offshore regions. Inspection services constitute the largest share within service type segment, followed by repair and refurbishment services. The crude oil sector is currently the dominant sector within the industry; however, natural gas is expected to show significant growth.

Key Drivers for Onshore Dominance:

- Extensive existing onshore pipeline infrastructure.

- Higher susceptibility to corrosion and other forms of degradation.

- Greater accessibility for inspection and repair.

Key Drivers for Crude Oil Sector Dominance:

- High demand for crude oil globally.

- Longer pipeline distances for crude oil transportation.

- Increased focus on safety and environmental compliance for crude oil pipelines.

Pipeline Integrity Management Industry Product Developments

Recent product innovations include advanced inline inspection tools with enhanced capabilities for detecting and characterizing pipeline defects, remotely operated vehicles (ROVs) with improved maneuverability and inspection capabilities, and sophisticated data analytics platforms for predictive maintenance. These advancements offer several competitive advantages, including improved accuracy in defect detection, reduced downtime, and optimized maintenance schedules. This technology's market fit is excellent, particularly in addressing the growing need for efficient and reliable pipeline integrity management in the face of ever stricter safety regulations.

Report Scope & Segmentation Analysis

This report segments the Pipeline Integrity Management market based on location of deployment (onshore and offshore), service type (inspection, cleaning, repair, and refurbishment), and sector (crude oil and natural gas). Each segment is analyzed in detail, including growth projections, market size, and competitive dynamics. The onshore segment is projected to experience a CAGR of XX% during the forecast period, while the offshore segment is expected to grow at a CAGR of XX%. Within service type, inspection services are projected to maintain their dominant position, with a CAGR of XX%. The Crude oil sector shows higher growth potential compared to Natural Gas due to higher infrastructure development in this segment.

Key Drivers of Pipeline Integrity Management Industry Growth

The growth of the Pipeline Integrity Management industry is propelled by several factors. Stringent government regulations aimed at enhancing pipeline safety are a major driver, mandating regular inspections and maintenance. The increasing demand for oil and gas, particularly in emerging economies, fuels the need for efficient and reliable pipeline networks. Technological advancements, such as the adoption of advanced NDT techniques and data analytics, are streamlining inspection processes and improving pipeline integrity.

Challenges in the Pipeline Integrity Management Industry Sector

The industry faces challenges including high initial investment costs associated with implementing advanced integrity management systems, the complexity of pipeline networks, and the need for highly skilled personnel to operate and maintain these systems. Supply chain disruptions can also significantly impact the availability of necessary equipment and services. Increased competition from new entrants with innovative technologies adds to the pressure. The cumulative impact of these challenges resulted in an estimated XX% decrease in project completion rates in XX.

Emerging Opportunities in Pipeline Integrity Management Industry

Emerging opportunities include the development and deployment of next-generation technologies, such as AI-powered predictive maintenance systems and advanced sensor technologies. The increasing adoption of digital twin technology offers further opportunities. Expanding into new and developing markets with significant pipeline infrastructure needs also offers promising potential. The integration of renewable energy sources into pipeline operations presents another area for growth.

Leading Players in the Pipeline Integrity Management Industry Market

- Infosys Limited

- TUV Rheinland

- MATCOR Inc

- Emerson Electric Co

- TD Williamson Inc

- SGS SA

- TWI Ltd

- Baker Hughes Company

- EnerMech Limited

- Bureau Veritas SA

Key Developments in Pipeline Integrity Management Industry Industry

- November 2021: Schneider Electric and Prisma Photonics partnered to enhance oil and gas pipeline monitoring using fiber sensing technology. This development significantly improves real-time pipeline security and integrity assessment.

- August 2021: The Dakota Access Pipeline (DAPL) expansion increased capacity by 180,000 BPD, emphasizing the ongoing investment in and growth of pipeline infrastructure. This expansion indirectly increased the demand for pipeline integrity management services.

Strategic Outlook for Pipeline Integrity Management Industry Market

The Pipeline Integrity Management market is poised for significant growth over the next decade, driven by increasing demand for oil and gas, stringent safety regulations, and technological advancements. The integration of digital technologies, like AI and machine learning, will further enhance operational efficiency and reduce risks. Companies that invest in research and development, build strategic partnerships, and adopt a proactive approach to pipeline integrity management are likely to achieve significant market success. The future market potential is immense, with significant opportunities for both established players and new entrants.

Pipeline Integrity Management Industry Segmentation

-

1. Sector

- 1.1. Crude Oil

- 1.2. Natural Gas

-

2. Location of Deployment

- 2.1. Onshore

- 2.2. Offshore

-

3. Service Type

- 3.1. Inspection Services

- 3.2. Cleaning Services

- 3.3. Repair and Refurbishment Services

Pipeline Integrity Management Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Asia Pacific

- 2.1. China

- 2.2. India

- 2.3. Malaysia

- 2.4. Australia

- 2.5. Rest of Asia Pacific

-

3. Europe

- 3.1. United Kingdom

- 3.2. Norway

- 3.3. Russia

- 3.4. Rest of Europe

-

4. Middle East and Africa

- 4.1. Saudi Arabia

- 4.2. United Arab Emirates

- 4.3. Nigeria

- 4.4. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Pipeline Integrity Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.21% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Growing Vehicle Ownership4.; Government Initiatives

- 3.3. Market Restrains

- 3.3.1. 4.; Volatile Crude Oil Prices

- 3.4. Market Trends

- 3.4.1. Increasing Demand for Natural Gas Pipeline Infrastructure

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Crude Oil

- 5.1.2. Natural Gas

- 5.2. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.2.1. Onshore

- 5.2.2. Offshore

- 5.3. Market Analysis, Insights and Forecast - by Service Type

- 5.3.1. Inspection Services

- 5.3.2. Cleaning Services

- 5.3.3. Repair and Refurbishment Services

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Asia Pacific

- 5.4.3. Europe

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. North America Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Crude Oil

- 6.1.2. Natural Gas

- 6.2. Market Analysis, Insights and Forecast - by Location of Deployment

- 6.2.1. Onshore

- 6.2.2. Offshore

- 6.3. Market Analysis, Insights and Forecast - by Service Type

- 6.3.1. Inspection Services

- 6.3.2. Cleaning Services

- 6.3.3. Repair and Refurbishment Services

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Asia Pacific Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 7.1.1. Crude Oil

- 7.1.2. Natural Gas

- 7.2. Market Analysis, Insights and Forecast - by Location of Deployment

- 7.2.1. Onshore

- 7.2.2. Offshore

- 7.3. Market Analysis, Insights and Forecast - by Service Type

- 7.3.1. Inspection Services

- 7.3.2. Cleaning Services

- 7.3.3. Repair and Refurbishment Services

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 8. Europe Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 8.1.1. Crude Oil

- 8.1.2. Natural Gas

- 8.2. Market Analysis, Insights and Forecast - by Location of Deployment

- 8.2.1. Onshore

- 8.2.2. Offshore

- 8.3. Market Analysis, Insights and Forecast - by Service Type

- 8.3.1. Inspection Services

- 8.3.2. Cleaning Services

- 8.3.3. Repair and Refurbishment Services

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 9. Middle East and Africa Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 9.1.1. Crude Oil

- 9.1.2. Natural Gas

- 9.2. Market Analysis, Insights and Forecast - by Location of Deployment

- 9.2.1. Onshore

- 9.2.2. Offshore

- 9.3. Market Analysis, Insights and Forecast - by Service Type

- 9.3.1. Inspection Services

- 9.3.2. Cleaning Services

- 9.3.3. Repair and Refurbishment Services

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 10. South America Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 10.1.1. Crude Oil

- 10.1.2. Natural Gas

- 10.2. Market Analysis, Insights and Forecast - by Location of Deployment

- 10.2.1. Onshore

- 10.2.2. Offshore

- 10.3. Market Analysis, Insights and Forecast - by Service Type

- 10.3.1. Inspection Services

- 10.3.2. Cleaning Services

- 10.3.3. Repair and Refurbishment Services

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 11. North America Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Rest of North America

- 12. Asia Pacific Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 China

- 12.1.2 India

- 12.1.3 Malaysia

- 12.1.4 Australia

- 12.1.5 Rest of Asia Pacific

- 13. Europe Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 United Kingdom

- 13.1.2 Norway

- 13.1.3 Russia

- 13.1.4 Rest of Europe

- 14. Middle East and Africa Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 Saudi Arabia

- 14.1.2 United Arab Emirates

- 14.1.3 Nigeria

- 14.1.4 Rest of Middle East and Africa

- 15. South America Pipeline Integrity Management Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Infosys Limited

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 TUV Rheinland

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 MATCOR Inc

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Emerson Electric Co

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 TD Williamson Inc

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 SGS SA

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 TWI Ltd

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Baker Hughes Company

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 EnerMech Limited

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Bureau Veritas SA

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Infosys Limited

List of Figures

- Figure 1: Global Pipeline Integrity Management Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Asia Pacific Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Asia Pacific Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Europe Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Europe Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Pipeline Integrity Management Industry Revenue (Million), by Sector 2024 & 2032

- Figure 13: North America Pipeline Integrity Management Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 14: North America Pipeline Integrity Management Industry Revenue (Million), by Location of Deployment 2024 & 2032

- Figure 15: North America Pipeline Integrity Management Industry Revenue Share (%), by Location of Deployment 2024 & 2032

- Figure 16: North America Pipeline Integrity Management Industry Revenue (Million), by Service Type 2024 & 2032

- Figure 17: North America Pipeline Integrity Management Industry Revenue Share (%), by Service Type 2024 & 2032

- Figure 18: North America Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: North America Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific Pipeline Integrity Management Industry Revenue (Million), by Sector 2024 & 2032

- Figure 21: Asia Pacific Pipeline Integrity Management Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 22: Asia Pacific Pipeline Integrity Management Industry Revenue (Million), by Location of Deployment 2024 & 2032

- Figure 23: Asia Pacific Pipeline Integrity Management Industry Revenue Share (%), by Location of Deployment 2024 & 2032

- Figure 24: Asia Pacific Pipeline Integrity Management Industry Revenue (Million), by Service Type 2024 & 2032

- Figure 25: Asia Pacific Pipeline Integrity Management Industry Revenue Share (%), by Service Type 2024 & 2032

- Figure 26: Asia Pacific Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Asia Pacific Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Europe Pipeline Integrity Management Industry Revenue (Million), by Sector 2024 & 2032

- Figure 29: Europe Pipeline Integrity Management Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 30: Europe Pipeline Integrity Management Industry Revenue (Million), by Location of Deployment 2024 & 2032

- Figure 31: Europe Pipeline Integrity Management Industry Revenue Share (%), by Location of Deployment 2024 & 2032

- Figure 32: Europe Pipeline Integrity Management Industry Revenue (Million), by Service Type 2024 & 2032

- Figure 33: Europe Pipeline Integrity Management Industry Revenue Share (%), by Service Type 2024 & 2032

- Figure 34: Europe Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Europe Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East and Africa Pipeline Integrity Management Industry Revenue (Million), by Sector 2024 & 2032

- Figure 37: Middle East and Africa Pipeline Integrity Management Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 38: Middle East and Africa Pipeline Integrity Management Industry Revenue (Million), by Location of Deployment 2024 & 2032

- Figure 39: Middle East and Africa Pipeline Integrity Management Industry Revenue Share (%), by Location of Deployment 2024 & 2032

- Figure 40: Middle East and Africa Pipeline Integrity Management Industry Revenue (Million), by Service Type 2024 & 2032

- Figure 41: Middle East and Africa Pipeline Integrity Management Industry Revenue Share (%), by Service Type 2024 & 2032

- Figure 42: Middle East and Africa Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 43: Middle East and Africa Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

- Figure 44: South America Pipeline Integrity Management Industry Revenue (Million), by Sector 2024 & 2032

- Figure 45: South America Pipeline Integrity Management Industry Revenue Share (%), by Sector 2024 & 2032

- Figure 46: South America Pipeline Integrity Management Industry Revenue (Million), by Location of Deployment 2024 & 2032

- Figure 47: South America Pipeline Integrity Management Industry Revenue Share (%), by Location of Deployment 2024 & 2032

- Figure 48: South America Pipeline Integrity Management Industry Revenue (Million), by Service Type 2024 & 2032

- Figure 49: South America Pipeline Integrity Management Industry Revenue Share (%), by Service Type 2024 & 2032

- Figure 50: South America Pipeline Integrity Management Industry Revenue (Million), by Country 2024 & 2032

- Figure 51: South America Pipeline Integrity Management Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 3: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 4: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Service Type 2019 & 2032

- Table 5: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: China Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: India Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Malaysia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Australia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Asia Pacific Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: United Kingdom Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Norway Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Russia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Europe Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Saudi Arabia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: United Arab Emirates Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Nigeria Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Rest of Middle East and Africa Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Brazil Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Argentina Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Rest of South America Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 31: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 32: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Service Type 2019 & 2032

- Table 33: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: United States Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Canada Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Rest of North America Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 38: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 39: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Service Type 2019 & 2032

- Table 40: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 41: China Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: India Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Malaysia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Australia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Rest of Asia Pacific Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 47: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 48: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Service Type 2019 & 2032

- Table 49: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 50: United Kingdom Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: Norway Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Russia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: Rest of Europe Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 55: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 56: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Service Type 2019 & 2032

- Table 57: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: Saudi Arabia Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: United Arab Emirates Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Nigeria Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Rest of Middle East and Africa Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 62: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 63: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 64: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Service Type 2019 & 2032

- Table 65: Global Pipeline Integrity Management Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 66: Brazil Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 67: Argentina Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 68: Rest of South America Pipeline Integrity Management Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pipeline Integrity Management Industry?

The projected CAGR is approximately 3.21%.

2. Which companies are prominent players in the Pipeline Integrity Management Industry?

Key companies in the market include Infosys Limited, TUV Rheinland, MATCOR Inc, Emerson Electric Co, TD Williamson Inc, SGS SA, TWI Ltd, Baker Hughes Company, EnerMech Limited, Bureau Veritas SA.

3. What are the main segments of the Pipeline Integrity Management Industry?

The market segments include Sector, Location of Deployment, Service Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Vehicle Ownership4.; Government Initiatives.

6. What are the notable trends driving market growth?

Increasing Demand for Natural Gas Pipeline Infrastructure.

7. Are there any restraints impacting market growth?

4.; Volatile Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

In November 2021, Schneider Electric, and Prisma Photonics, a provider of next-generation fiber sensing for smart infrastructure, announced a partnership to help oil and gas pipeline owners and operators prevent accidental and malicious activity by providing real-time intelligence and precise monitoring of oil and gas infrastructure.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pipeline Integrity Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pipeline Integrity Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pipeline Integrity Management Industry?

To stay informed about further developments, trends, and reports in the Pipeline Integrity Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence