Key Insights

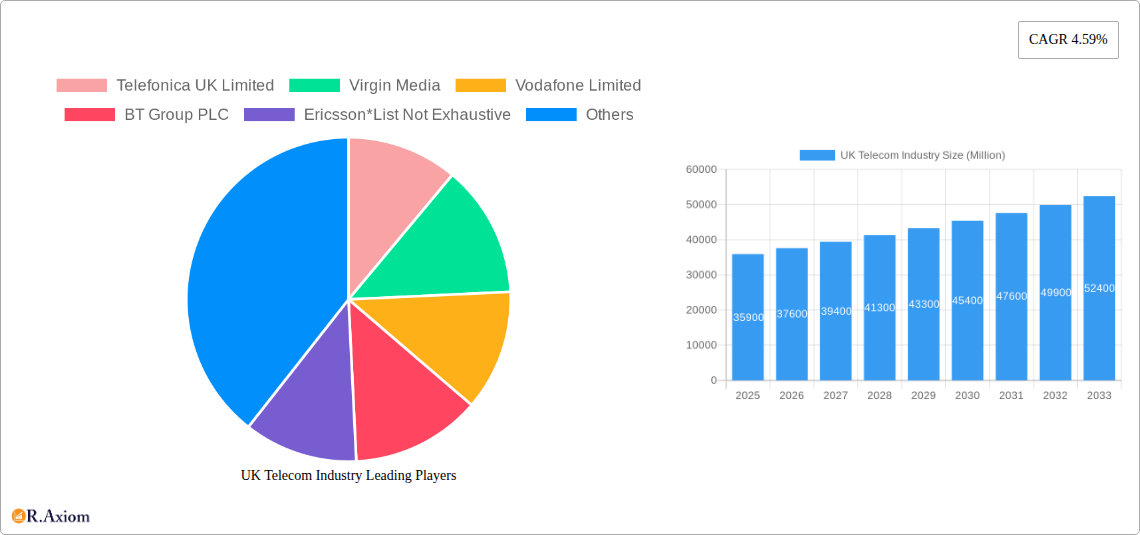

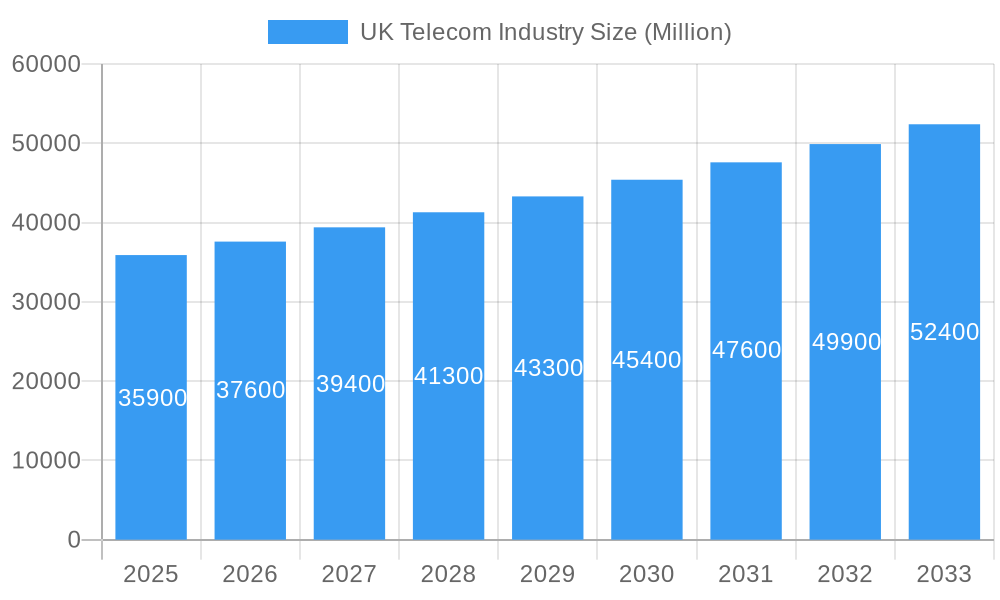

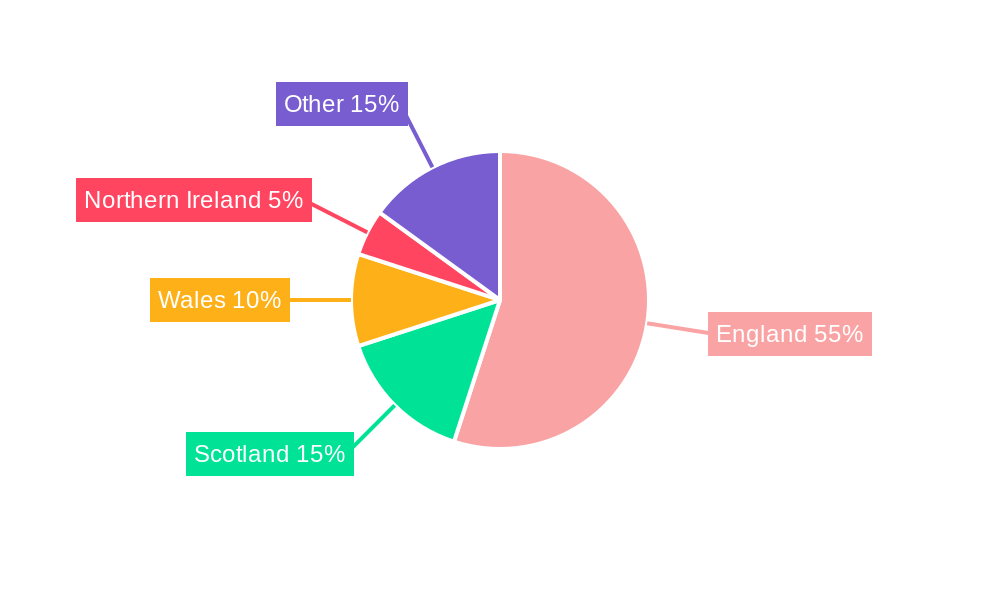

The UK telecom industry, valued at £35.90 billion in 2025, is projected to experience steady growth, with a Compound Annual Growth Rate (CAGR) of 4.59% from 2025 to 2033. This expansion is driven by several factors. Increased mobile data consumption fueled by the proliferation of smartphones and high-speed internet access is a primary driver. The rising adoption of over-the-top (OTT) services like Netflix and Spotify, alongside growing demand for pay-TV packages, contributes significantly to market growth. Furthermore, advancements in 5G technology are paving the way for innovative services and applications, further stimulating market expansion. However, intense competition among established players like BT Group, Vodafone, and Virgin Media, alongside the emergence of disruptive players, presents a key restraint. Regulatory changes and the need for continuous investment in network infrastructure also pose challenges. Segmentation analysis reveals that wireless data and messaging services, including internet and handset data packages, are a dominant revenue generator, followed by voice services and OTT/PayTV services. The average revenue per user (ARPU) across services will likely see moderate growth, driven by higher-value data packages and bundled services. The market's regional distribution is largely concentrated across England, Scotland, Wales, and Northern Ireland, with variations in penetration and ARPU across these regions likely influenced by factors such as population density and economic development.

UK Telecom Industry Market Size (In Billion)

Looking ahead to 2033, the UK telecom market is expected to be significantly larger, driven by sustained increases in mobile data consumption and the continued adoption of advanced technologies like 5G and the Internet of Things (IoT). However, maintaining this growth trajectory will depend on managing competitive pressures, navigating evolving regulatory landscapes, and making strategic investments in network infrastructure to support increasing demand. The industry will likely see further consolidation as smaller players struggle to compete with larger, more established firms. The successful players will be those that effectively adapt to changing consumer preferences, leverage technological advancements, and provide innovative and value-added services. Focus on improving customer service and building strong brand loyalty will be crucial factors in securing market share.

UK Telecom Industry Company Market Share

UK Telecom Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the UK Telecom industry, covering market size, segmentation, competitive landscape, key trends, and future growth prospects. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. The report leverages extensive primary and secondary research to offer actionable insights for industry stakeholders, investors, and businesses operating within the UK Telecom sector. All financial values are expressed in millions.

UK Telecom Industry Market Concentration & Innovation

The UK telecom market exhibits a high degree of concentration, with a few dominant players commanding significant market share. BT Group PLC, Vodafone Limited, and Virgin Media consistently rank among the top players, exhibiting robust market presence across various segments. Market share fluctuations are observed annually due to competitive pressures and strategic initiatives, like M&A activity. For example, the proposed merger between Vodafone and Three, if successful, would significantly alter the market landscape. The total M&A deal value for the sector in 2022 was approximately £xx Million, showcasing the level of investment and consolidation within the industry.

Innovation in the UK telecom sector is driven by several factors, including:

- Technological advancements: 5G rollout, advancements in fibre broadband infrastructure, and the rise of IoT technologies are reshaping the competitive landscape.

- Regulatory frameworks: Ofcom’s regulatory policies significantly influence market dynamics, fostering competition and driving innovation in network infrastructure and service offerings.

- Product substitutes: The emergence of OTT services (Over-The-Top) presents a notable challenge to traditional telecom providers, forcing innovation in service bundles and pricing strategies.

- End-user trends: Growing demand for higher bandwidth, data-centric services, and improved network coverage necessitates continuous innovation.

The market is characterized by ongoing M&A activity, further consolidating market power among key players. These activities often lead to improved network infrastructure, enhanced service offerings, and greater economies of scale.

UK Telecom Industry Industry Trends & Insights

The UK telecom market demonstrates steady growth driven by increasing smartphone penetration, rising data consumption, and the adoption of advanced technologies like 5G. The industry is witnessing a shift from voice-centric services towards data-centric offerings, reflected in the substantial growth of mobile data and broadband subscriptions. The CAGR for the overall telecom services market from 2020 to 2027 is estimated at xx%, with mobile data and broadband experiencing the most rapid growth. Market penetration for 5G services is steadily rising, reaching an estimated xx% by 2027.

Technological disruptions, such as the widespread adoption of cloud computing and AI, are transforming operational efficiency and service delivery. Consumer preference for bundled services, attractive pricing packages, and seamless customer experience influences the industry’s competitive dynamics. This has pushed providers to innovate with tiered packages, discount strategies, and improved customer service. These trends are influencing the competitive landscape, with companies constantly adapting to maintain market share and attract new customers.

Dominant Markets & Segments in UK Telecom Industry

The UK telecom market is largely dominated by the Wireless: Data and Messaging Services segment, contributing significantly to overall industry revenue. The growth in this segment is driven by:

- Increased smartphone penetration: Nearly every UK household now owns at least one smartphone, driving demand for mobile data.

- Growing data consumption: Streaming services, online gaming, and social media are increasing the demand for high-speed mobile internet.

- Bundled packages: Combined data and messaging deals make it more affordable for consumers to utilize high-bandwidth mobile services.

The Average Revenue Per User (ARPU) for the overall services segment in 2024 was estimated at £xx, demonstrating a gradual rise over the past few years.

- Voice Services: While declining in revenue, voice services continue to hold a significant share, primarily due to existing customer base and fixed-line services.

- Wireless: Data and Messaging Services: This segment shows exceptional growth, driven by increasing data consumption and adoption of data-centric packages. Market size estimates for 2020-2027 show exponential growth.

- OTT and PayTV Services: This segment exhibits moderate growth, driven by the increasing popularity of streaming services.

UK Telecom Industry Product Developments

Recent product innovations have focused on enhancing network infrastructure, improving data speeds, and providing customers with more value for their money. The introduction of 5G network capabilities, advanced Wi-Fi technologies (as seen with Vodafone’s Pro II plan), and innovative data bundles are key examples. These advancements aim to improve customer experience and compete more effectively in a rapidly evolving market.

Report Scope & Segmentation Analysis

This report segments the UK telecom market primarily by services:

- Voice Services: This includes both fixed-line and mobile voice services, analyzing growth projections, market size, and competitive dynamics within this segment.

- Wireless: Data and Messaging Services: This covers mobile data, messaging services, and related packages, analyzing growth, market size, and competitive strategies related to data packages and discounts.

- OTT and PayTV Services: This segment encompasses over-the-top streaming services and pay television offerings, including growth projections, market size, and the competitive strategies of providers.

Key Drivers of UK Telecom Industry Growth

Growth in the UK telecom industry is fueled by several factors, including:

- Technological advancements: 5G rollout, fibre optic broadband expansion, and the Internet of Things (IoT) are driving demand for higher bandwidth and enhanced connectivity.

- Economic factors: Increasing disposable incomes are leading to greater consumer spending on telecom services.

- Regulatory environment: Favorable regulatory policies encourage investment in network infrastructure and promote competition.

Challenges in the UK Telecom Industry Sector

The UK telecom industry faces several challenges:

- Intense competition: The market is highly competitive, with numerous established players and new entrants vying for market share, putting downward pressure on prices.

- High infrastructure costs: Investing in and maintaining advanced network infrastructure, particularly for 5G deployment, requires substantial capital expenditure.

- Regulatory hurdles: Navigating complex regulations and obtaining necessary licenses can be challenging and time-consuming.

Emerging Opportunities in UK Telecom Industry

The UK telecom market presents numerous emerging opportunities:

- 5G expansion: Further expansion of 5G network coverage will create new opportunities for service providers to offer innovative data-centric services.

- IoT growth: The increasing number of connected devices creates opportunities to develop and offer tailored IoT solutions to enterprises and consumers.

- Cloud computing: Adoption of cloud-based services will enhance network efficiency and allow for greater flexibility in service offerings.

Leading Players in the UK Telecom Industry Market

- Telefonica UK Limited

- Virgin Media

- Vodafone Limited

- BT Group PLC

- Ericsson

- TalkTalk Telecom Group

- Lycamobile

- Sky UK Limited

- Sitel Group

- Teleperformance

Key Developments in UK Telecom Industry Industry

- October 2022: Vodafone launched its Pro II plan, featuring cutting-edge Wi-Fi 6E technology for enhanced home broadband speeds.

- October 2022: BT Group PLC launched the AI Accelerator, an internal ML-Ops platform for optimizing AI model deployments.

- October 2022: Vodafone and Three announced merger talks, aiming to create a stronger competitor in the UK market.

Strategic Outlook for UK Telecom Industry Market

The UK telecom market is poised for continued growth, driven by technological advancements, increasing data consumption, and the expansion of 5G networks. Opportunities abound in areas like IoT, cloud services, and advanced network capabilities. The strategic focus for providers should be on adapting to evolving consumer demands, investing in cutting-edge technology, and building robust, reliable, and secure networks to maintain a competitive edge in this dynamic market.

UK Telecom Industry Segmentation

-

1. Servi

-

1.1. Voice Services

- 1.1.1. Wired

- 1.1.2. Wireless

- 1.2. Data and

- 1.3. OTT and PayTV Services

-

1.1. Voice Services

UK Telecom Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

UK Telecom Industry Regional Market Share

Geographic Coverage of UK Telecom Industry

UK Telecom Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.59% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising demand for 5G; Growth of IoT usage in Telecom

- 3.3. Market Restrains

- 3.3.1. ; Deployment Issues & Competition From Rival LPWAN Technologies

- 3.4. Market Trends

- 3.4.1. 5G Roll-Out in the United Kingdom to Drive the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global UK Telecom Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Servi

- 5.1.1. Voice Services

- 5.1.1.1. Wired

- 5.1.1.2. Wireless

- 5.1.2. Data and

- 5.1.3. OTT and PayTV Services

- 5.1.1. Voice Services

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Servi

- 6. North America UK Telecom Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Servi

- 6.1.1. Voice Services

- 6.1.1.1. Wired

- 6.1.1.2. Wireless

- 6.1.2. Data and

- 6.1.3. OTT and PayTV Services

- 6.1.1. Voice Services

- 6.1. Market Analysis, Insights and Forecast - by Servi

- 7. South America UK Telecom Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Servi

- 7.1.1. Voice Services

- 7.1.1.1. Wired

- 7.1.1.2. Wireless

- 7.1.2. Data and

- 7.1.3. OTT and PayTV Services

- 7.1.1. Voice Services

- 7.1. Market Analysis, Insights and Forecast - by Servi

- 8. Europe UK Telecom Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Servi

- 8.1.1. Voice Services

- 8.1.1.1. Wired

- 8.1.1.2. Wireless

- 8.1.2. Data and

- 8.1.3. OTT and PayTV Services

- 8.1.1. Voice Services

- 8.1. Market Analysis, Insights and Forecast - by Servi

- 9. Middle East & Africa UK Telecom Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Servi

- 9.1.1. Voice Services

- 9.1.1.1. Wired

- 9.1.1.2. Wireless

- 9.1.2. Data and

- 9.1.3. OTT and PayTV Services

- 9.1.1. Voice Services

- 9.1. Market Analysis, Insights and Forecast - by Servi

- 10. Asia Pacific UK Telecom Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Servi

- 10.1.1. Voice Services

- 10.1.1.1. Wired

- 10.1.1.2. Wireless

- 10.1.2. Data and

- 10.1.3. OTT and PayTV Services

- 10.1.1. Voice Services

- 10.1. Market Analysis, Insights and Forecast - by Servi

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Telefonica UK Limited

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Virgin Media

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Vodafone Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BT Group PLC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Ericsson*List Not Exhaustive

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 TalkTalk Telecom Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Lycamobile

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sky UK Limited

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Sitel Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Teleperformance

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Telefonica UK Limited

List of Figures

- Figure 1: Global UK Telecom Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 3: North America UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 4: North America UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 7: South America UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 8: South America UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: South America UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 11: Europe UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 12: Europe UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 15: Middle East & Africa UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 16: Middle East & Africa UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Middle East & Africa UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 19: Asia Pacific UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 20: Asia Pacific UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Asia Pacific UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 2: Global UK Telecom Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 4: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Mexico UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 9: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Brazil UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Argentina UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 14: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Russia UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Benelux UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Nordics UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 25: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Turkey UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Israel UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: GCC UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: North Africa UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Africa UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 33: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: China UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: India UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Japan UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Korea UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: ASEAN UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Oceania UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Telecom Industry?

The projected CAGR is approximately 4.59%.

2. Which companies are prominent players in the UK Telecom Industry?

Key companies in the market include Telefonica UK Limited, Virgin Media, Vodafone Limited, BT Group PLC, Ericsson*List Not Exhaustive, TalkTalk Telecom Group, Lycamobile, Sky UK Limited, Sitel Group, Teleperformance.

3. What are the main segments of the UK Telecom Industry?

The market segments include Servi.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.90 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising demand for 5G; Growth of IoT usage in Telecom.

6. What are the notable trends driving market growth?

5G Roll-Out in the United Kingdom to Drive the Market.

7. Are there any restraints impacting market growth?

; Deployment Issues & Competition From Rival LPWAN Technologies.

8. Can you provide examples of recent developments in the market?

October 2022 - Vodafone unveiled its Pro II plan, the speediest Wi-Fi technology across all homes in the United Kingdom. The new Ultra Hub and Super Wi-Fi booster employ the most recent Wi-Fi 6E technology, which may offer Wi-Fi to more than 150 devices. This is a first for any significant broadband provider in the United Kingdom.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Telecom Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Telecom Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Telecom Industry?

To stay informed about further developments, trends, and reports in the UK Telecom Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence