Key Insights

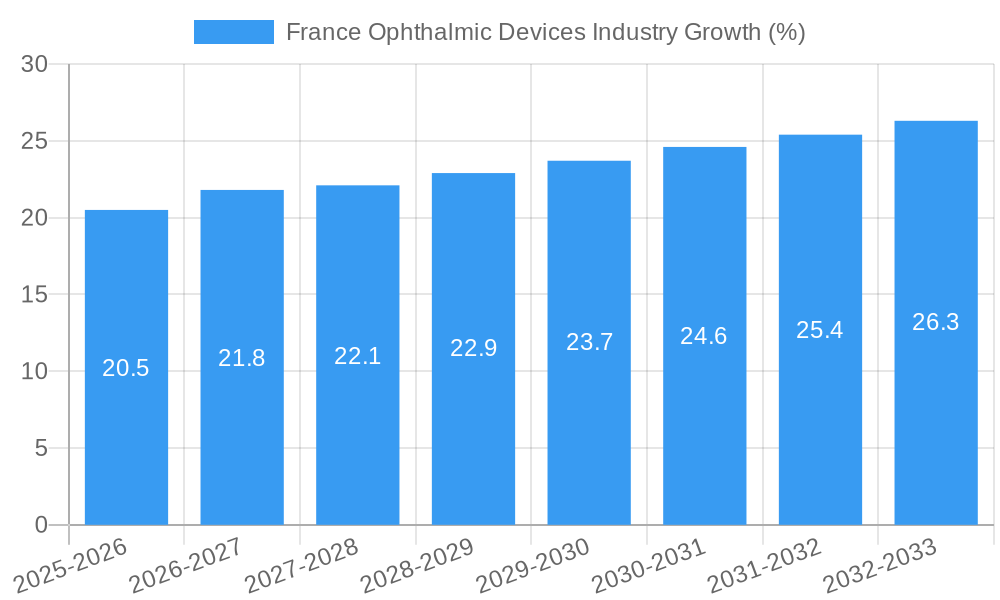

The French ophthalmic devices market, valued at approximately €[Estimate based on market size XX and currency conversion, e.g., €500 million] in 2025, is projected to experience steady growth with a Compound Annual Growth Rate (CAGR) of 4.10% from 2025 to 2033. This growth is driven by several key factors. The aging population in France is a significant contributor, leading to an increased prevalence of age-related eye diseases like cataracts, glaucoma, and macular degeneration, thereby boosting demand for diagnostic and treatment devices. Furthermore, advancements in surgical techniques, particularly minimally invasive procedures, coupled with the introduction of innovative devices offering improved precision and efficacy, are fueling market expansion. Technological advancements in areas like laser refractive surgery and intraocular lenses are also significantly impacting market growth. Increased healthcare spending and government initiatives promoting eye health awareness further contribute to the positive outlook.

However, the market faces certain restraints. High costs associated with advanced ophthalmic devices can limit accessibility for some patients, particularly those without comprehensive health insurance. Stringent regulatory approvals and reimbursement processes for new technologies can also impede market penetration. Competition among established players like Johnson & Johnson, Alcon, and Zeiss, alongside emerging companies introducing disruptive innovations, will continue shaping the market landscape. The segmentation analysis reveals strong growth potential across all device categories, with surgical devices, including those for cataract surgery and refractive procedures, expected to dominate the market, followed by diagnostic and monitoring devices and vision correction devices. The sustained focus on improving patient outcomes and technological innovation is expected to drive the market towards premium device adoption in the years to come.

France Ophthalmic Devices Industry: 2019-2033 Market Report

This comprehensive report provides a detailed analysis of the France ophthalmic devices market from 2019 to 2033, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The report covers market size, segmentation, growth drivers, challenges, competitive landscape, and future outlook. It leverages extensive data analysis and expert insights to provide actionable intelligence for informed strategic planning.

France Ophthalmic Devices Industry Market Concentration & Innovation

The French ophthalmic devices market exhibits a moderately concentrated structure, with a few multinational corporations holding significant market share. Key players like Johnson & Johnson, Alcon Inc, and EssilorLuxottica SA command substantial portions of the market, while regional and specialized players compete in niche segments. Market share dynamics are influenced by technological advancements, regulatory approvals, and pricing strategies. Innovation in areas such as minimally invasive surgical techniques, advanced imaging technologies, and personalized vision correction solutions are driving market growth. Regulatory frameworks, primarily set by the French Ministry of Health, influence product approvals and market access. The presence of strong intellectual property protections stimulates continuous innovation. Product substitutes, such as alternative therapies and lifestyle changes, pose a moderate competitive threat. End-user trends, including an aging population and rising prevalence of eye diseases, significantly influence market demand. Mergers and acquisitions (M&A) activities, exemplified by HOYA VISION CARE's acquisition of Medic'Oeil (June 2022), demonstrate industry consolidation and expansion strategies. These deals often involve substantial capital investment; for example, the €23 Million investment in Horus Pharma demonstrates the interest in ophthalmology’s growth. The average M&A deal value in this sector over the historical period (2019-2024) is estimated at xx Million.

France Ophthalmic Devices Industry Industry Trends & Insights

The French ophthalmic devices market has witnessed consistent growth over the historical period (2019-2024). Driven by factors such as an aging population, increasing prevalence of ophthalmic diseases (e.g., cataracts, glaucoma, age-related macular degeneration), rising healthcare expenditure, and technological advancements in diagnostic and treatment modalities, the market is projected to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration of advanced technologies, particularly in surgical devices and diagnostic imaging, is increasing, leading to improved treatment outcomes and patient satisfaction. Consumer preferences are shifting towards minimally invasive procedures, personalized treatment options, and greater access to eye care services. The competitive landscape is characterized by intense rivalry among established players and emerging companies, leading to innovative product development and strategic partnerships. Technological disruptions, such as the integration of artificial intelligence (AI) and machine learning (ML) in diagnostic tools and surgical robots, are reshaping the market. Market penetration for AI-powered diagnostic devices is predicted at xx% by 2033, while the market penetration of minimally invasive surgical devices is expected to reach xx% by 2033.

Dominant Markets & Segments in France Ophthalmic Devices Industry

The French ophthalmic devices market is largely driven by the urban areas, reflecting higher healthcare infrastructure and accessibility to advanced technologies. Within the segmentation, Surgical Devices holds the largest market share, driven by the high incidence of cataract surgery and other ophthalmic procedures. Other Surgical Devices and Diagnostic and Monitoring Devices segments are also experiencing significant growth, fueled by increasing demand for advanced diagnostic tools and minimally invasive surgical devices. Vision Correction Devices exhibit considerable potential owing to the growing prevalence of refractive errors.

Key Drivers for Dominant Segments:

- Surgical Devices: High prevalence of cataracts and other conditions requiring surgery, advancements in minimally invasive techniques, and increasing availability of advanced surgical equipment.

- Diagnostic and Monitoring Devices: Rising demand for early diagnosis and precise monitoring of eye diseases, technological advancements in imaging and diagnostic technologies, and government initiatives to promote early detection programs.

- Vision Correction Devices: Increasing prevalence of refractive errors (myopia, hyperopia, astigmatism), rising disposable incomes, and technological advancements in vision correction techniques (e.g., LASIK, SMILE).

The dominance of Surgical Devices is attributed to the high volume of cataract surgeries performed annually in France, coupled with the availability of sophisticated surgical equipment and experienced ophthalmologists.

France Ophthalmic Devices Industry Product Developments

Recent product innovations include advanced intraocular lenses (IOLs), sophisticated diagnostic imaging systems (e.g., OCT, optical coherence tomography), and minimally invasive surgical devices. These innovations enhance surgical precision, improve patient outcomes, and expand treatment options. New product launches are driven by the demand for less invasive procedures and greater efficiency. The integration of digital technologies and artificial intelligence is further transforming the field, creating new possibilities for personalized treatments and improved diagnostic accuracy. The key to market success lies in delivering clinically effective, cost-efficient, and user-friendly products that meet the evolving needs of healthcare providers and patients.

Report Scope & Segmentation Analysis

This report segments the France ophthalmic devices market based on device type: Surgical Devices (including Cataract Surgery Devices, Glaucoma Surgery Devices, and Retinal Surgery Devices), Other Surgical Devices (including Laser Devices, Phacoemulsification Machines and Microscopes) and Diagnostic and Monitoring Devices (including Optical Coherence Tomography (OCT), Fundus Cameras, Visual Field Analyzers). Each segment is analyzed based on market size, growth projections, and competitive dynamics. The Surgical Devices segment projects the fastest growth due to the high prevalence of age-related eye diseases, while the Diagnostic and Monitoring Devices segment is projected to witness significant growth driven by technological advancements. The market size for Surgical Devices in 2025 is estimated at xx Million, and it is projected to reach xx Million by 2033. The Diagnostic and Monitoring Devices market is projected to grow from xx Million in 2025 to xx Million by 2033. The competitive landscape varies across segments; some are dominated by a few major players, while others have a more fragmented structure.

Key Drivers of France Ophthalmic Devices Industry Growth

Several factors contribute to the growth of the French ophthalmic devices market. The aging population, leading to an increased prevalence of age-related eye diseases, is a primary driver. Rising healthcare expenditure and government initiatives to improve healthcare access enhance market expansion. Technological advancements in device technology, producing minimally invasive procedures and improved accuracy, are key factors. Strong regulatory support for medical device innovation also contributes. The increasing adoption of advanced diagnostic tools for early detection and management of eye diseases further fuels market growth.

Challenges in the France Ophthalmic Devices Industry Sector

The French ophthalmic devices market faces challenges including stringent regulatory pathways for device approval, impacting time-to-market. The high cost of advanced devices can limit accessibility for some patients, especially in underserved areas. Intense competition among numerous players, both domestic and international, also creates hurdles. Supply chain disruptions may affect the availability of devices and components, creating uncertainty. Reimbursement policies and pricing negotiations with healthcare payers present ongoing challenges.

Emerging Opportunities in France Ophthalmic Devices Industry

The integration of artificial intelligence and machine learning in diagnostic and treatment tools offers significant opportunities for innovation and improved patient outcomes. The growing demand for personalized medicine and customized treatment approaches creates niches for specialized devices and services. The expansion of teleophthalmology and remote patient monitoring solutions presents considerable potential. Investment in research and development of new technologies, including gene therapy and regenerative medicine, holds promise for future advancements. The increasing adoption of minimally invasive surgical techniques provides a promising market segment.

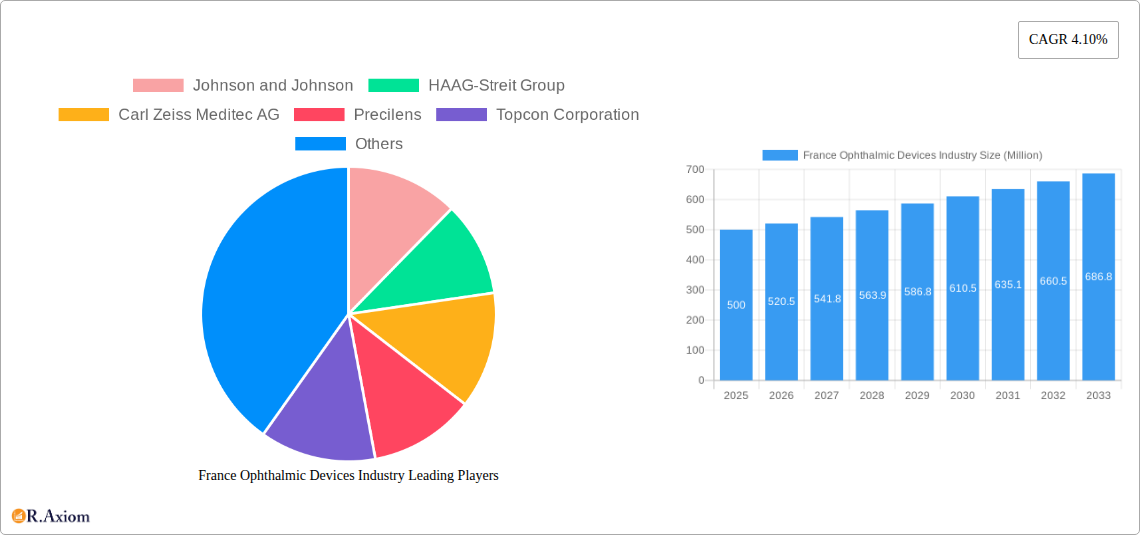

Leading Players in the France Ophthalmic Devices Industry Market

- Johnson & Johnson

- HAAG-Streit Group

- Carl Zeiss Meditec AG

- Precilens

- Topcon Corporation

- Alcon Inc

- Bausch Health Companies Inc

- Ziemer Ophthalmic Systems AG

- Nidek Co Ltd

- EssilorLuxottica SA

- Hoya Corporation

Key Developments in France Ophthalmic Devices Industry Industry

- June 2022: HOYA VISION CARE acquired Medic'Oeil, expanding its reach in the French ophthalmology market and strengthening its distribution network.

- March 2022: The Nov Sante Actions Non Cotees fund invested €23 Million in Horus Pharma, boosting the French pharmaceutical company's development and indicating strong investor confidence in the French ophthalmology sector.

Strategic Outlook for France Ophthalmic Devices Industry Market

The France ophthalmic devices market is poised for continued growth, fueled by technological advancements, an aging population, and rising healthcare expenditure. Strategic investments in innovation, particularly in AI-powered diagnostics and minimally invasive surgical technologies, will be crucial for market success. Companies that effectively address the challenges of regulatory hurdles, cost constraints, and competition while adapting to evolving consumer preferences are likely to experience significant growth in the coming years. The integration of digital technologies and the expansion of teleophthalmology hold particularly promising prospects for market expansion and improvement in patient care.

France Ophthalmic Devices Industry Segmentation

-

1. Devices

-

1.1. Surgical Devices

- 1.1.1. Glaucoma Drainage Devices

- 1.1.2. Glaucoma Stents and Implants

- 1.1.3. Intraocular Lenses

- 1.1.4. Lasers

- 1.1.5. Other Surgical Devices

-

1.2. Diagnostic and Monitoring Devices

- 1.2.1. Autorefractors and Keratometers

- 1.2.2. Corneal Topography Systems

- 1.2.3. Ophthalmic Ultrasound Imaging Systems

- 1.2.4. Ophthalmoscopes

- 1.2.5. Optical Coherence Tomography Scanners

- 1.2.6. Other Diagnostic and Monitoring Devices

-

1.3. Vision Correction Devices

- 1.3.1. Spectacles

- 1.3.2. Contact Lenses

-

1.1. Surgical Devices

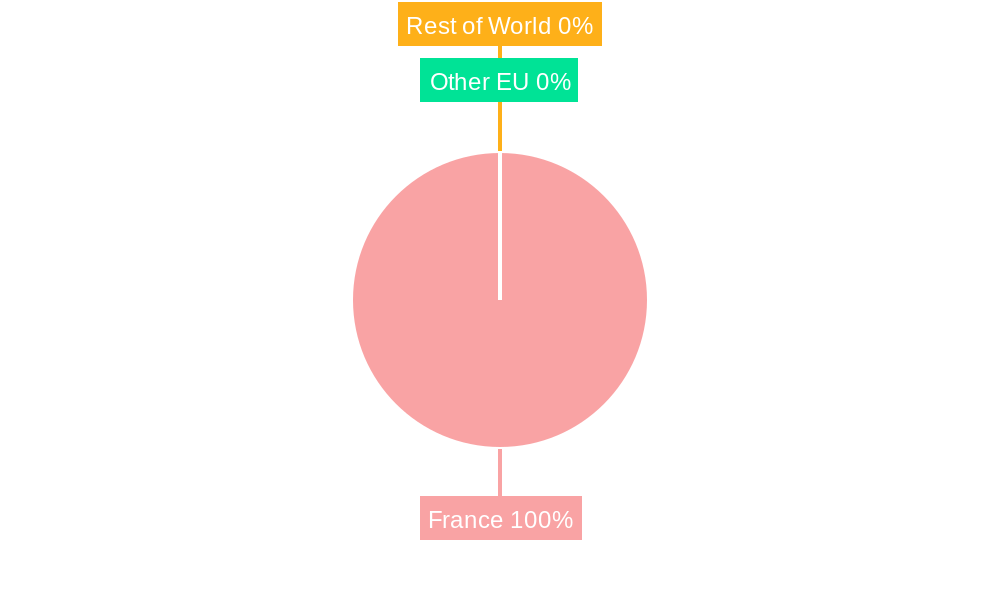

France Ophthalmic Devices Industry Segmentation By Geography

- 1. France

France Ophthalmic Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.10% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Demographic Shift and Increasing Prevalence of Eye Diseases; Rising Geriatric Population

- 3.3. Market Restrains

- 3.3.1. Risk Associated with Ophthalmic Procedures

- 3.4. Market Trends

- 3.4.1. Contact Lenses Segment is Expected to Hold Significant Market Share Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. France Ophthalmic Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Devices

- 5.1.1. Surgical Devices

- 5.1.1.1. Glaucoma Drainage Devices

- 5.1.1.2. Glaucoma Stents and Implants

- 5.1.1.3. Intraocular Lenses

- 5.1.1.4. Lasers

- 5.1.1.5. Other Surgical Devices

- 5.1.2. Diagnostic and Monitoring Devices

- 5.1.2.1. Autorefractors and Keratometers

- 5.1.2.2. Corneal Topography Systems

- 5.1.2.3. Ophthalmic Ultrasound Imaging Systems

- 5.1.2.4. Ophthalmoscopes

- 5.1.2.5. Optical Coherence Tomography Scanners

- 5.1.2.6. Other Diagnostic and Monitoring Devices

- 5.1.3. Vision Correction Devices

- 5.1.3.1. Spectacles

- 5.1.3.2. Contact Lenses

- 5.1.1. Surgical Devices

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. France

- 5.1. Market Analysis, Insights and Forecast - by Devices

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Johnson and Johnson

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 HAAG-Streit Group

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Carl Zeiss Meditec AG

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Precilens

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Topcon Corporation

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Alcon Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Bausch Health Companies Inc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Ziemer Ophthalmic Systems AG

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Nidek Co Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 EssilorLuxottica SA

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Hoya Corporation

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 Johnson and Johnson

List of Figures

- Figure 1: France Ophthalmic Devices Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: France Ophthalmic Devices Industry Share (%) by Company 2024

List of Tables

- Table 1: France Ophthalmic Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: France Ophthalmic Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: France Ophthalmic Devices Industry Revenue Million Forecast, by Devices 2019 & 2032

- Table 4: France Ophthalmic Devices Industry Volume K Unit Forecast, by Devices 2019 & 2032

- Table 5: France Ophthalmic Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: France Ophthalmic Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 7: France Ophthalmic Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: France Ophthalmic Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 9: France Ophthalmic Devices Industry Revenue Million Forecast, by Devices 2019 & 2032

- Table 10: France Ophthalmic Devices Industry Volume K Unit Forecast, by Devices 2019 & 2032

- Table 11: France Ophthalmic Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: France Ophthalmic Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the France Ophthalmic Devices Industry?

The projected CAGR is approximately 4.10%.

2. Which companies are prominent players in the France Ophthalmic Devices Industry?

Key companies in the market include Johnson and Johnson, HAAG-Streit Group, Carl Zeiss Meditec AG, Precilens, Topcon Corporation, Alcon Inc, Bausch Health Companies Inc, Ziemer Ophthalmic Systems AG, Nidek Co Ltd, EssilorLuxottica SA, Hoya Corporation.

3. What are the main segments of the France Ophthalmic Devices Industry?

The market segments include Devices.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Demographic Shift and Increasing Prevalence of Eye Diseases; Rising Geriatric Population.

6. What are the notable trends driving market growth?

Contact Lenses Segment is Expected to Hold Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Risk Associated with Ophthalmic Procedures.

8. Can you provide examples of recent developments in the market?

In June 2022, HOYA VISION CARE acquired Medic'Oeil, a network of ophthalmology practices in France. Medic'Oeil operates a total of seven centers in different regions where vision care equipment and administrative resources are shared between a number of ophthalmologists.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "France Ophthalmic Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the France Ophthalmic Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the France Ophthalmic Devices Industry?

To stay informed about further developments, trends, and reports in the France Ophthalmic Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence