Key Insights

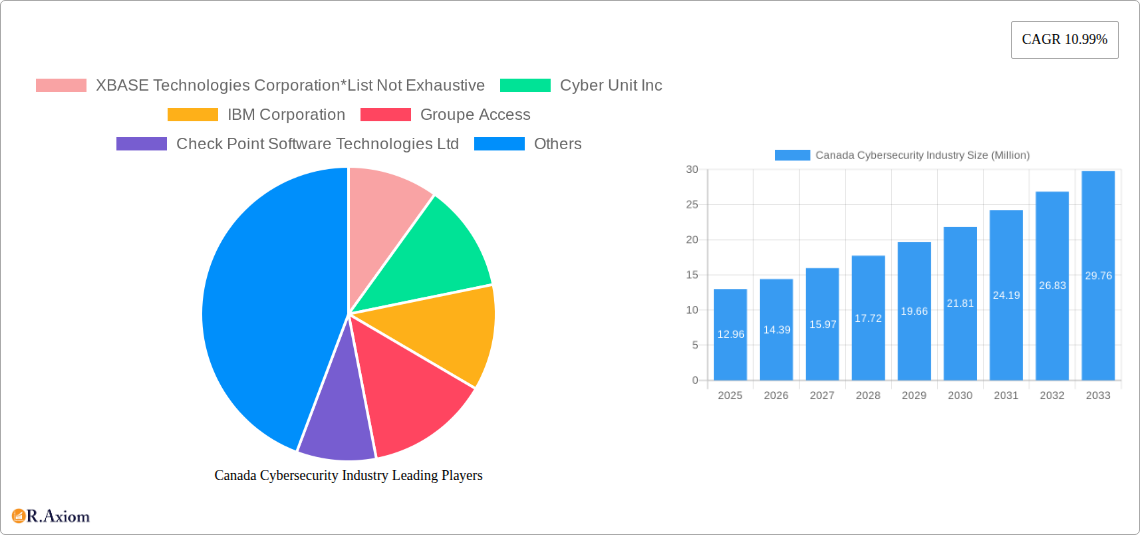

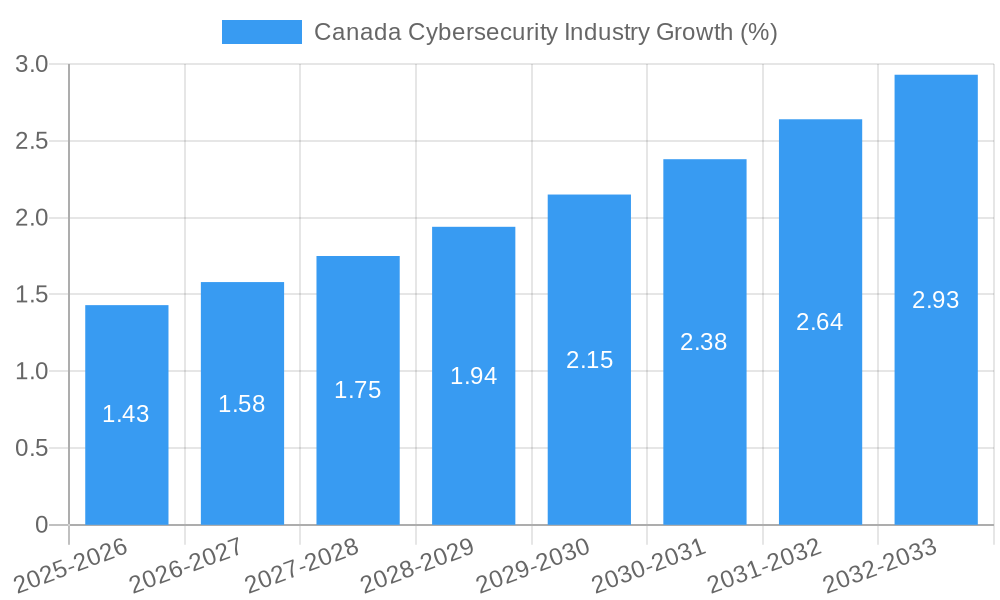

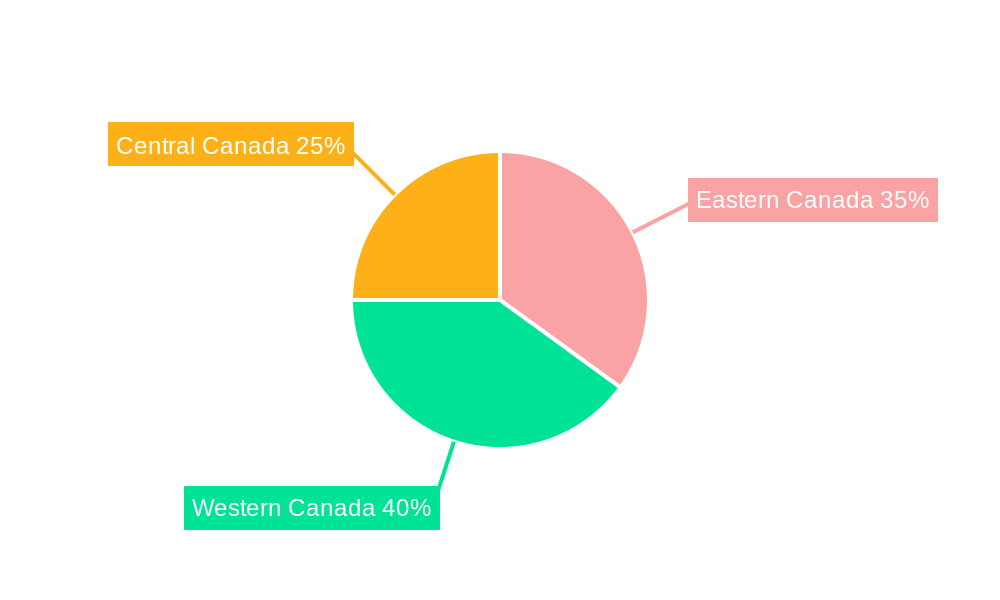

The Canadian cybersecurity market, valued at $12.96 million in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 10.99% from 2025 to 2033. This expansion is driven by several key factors. Increasing digitalization across all sectors—BFSI, healthcare, manufacturing, government & defense, and IT and telecommunications—fuels heightened vulnerability to cyber threats, necessitating robust security solutions. The rising adoption of cloud-based services, while offering scalability and flexibility, also presents new attack vectors, thereby stimulating demand for cloud security solutions. Furthermore, evolving cyberattack sophistication and the increasing frequency of data breaches are compelling organizations to invest heavily in preventative and reactive cybersecurity measures. This includes a shift towards comprehensive security strategies encompassing various security types, encompassing both on-premise and cloud deployments. The Canadian government's proactive stance on cybersecurity regulation and initiatives further underscores the market's growth trajectory. Regional variations exist, with potentially higher growth anticipated in regions like Western Canada due to its robust technological infrastructure and the concentration of key industries.

The market segmentation reveals a dynamic landscape. While precise figures for each segment (by deployment, end-user, and offering type) are unavailable, the significant growth in cloud adoption suggests a strong preference for cloud-based security solutions within the Canadian market. The BFSI and government & defense sectors are likely to be the largest end-users due to their critical infrastructure and stringent regulatory requirements. The competitive landscape is characterized by a mix of global players like IBM, Microsoft, and Check Point, alongside smaller, specialized firms. This competition fosters innovation and drives pricing pressures, ultimately benefiting Canadian businesses seeking comprehensive and cost-effective cybersecurity solutions. Continued investment in research and development within the cybersecurity sector, coupled with skilled workforce development, are vital to sustaining this growth trajectory.

Canada Cybersecurity Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Canadian cybersecurity industry, covering market size, segmentation, key players, growth drivers, challenges, and future opportunities. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The forecast period is 2025-2033, and the historical period covers 2019-2024. This report is invaluable for industry stakeholders, investors, and businesses seeking to understand and capitalize on the evolving landscape of cybersecurity in Canada.

Canada Cybersecurity Industry Market Concentration & Innovation

The Canadian cybersecurity market exhibits a moderately concentrated landscape, with a few large multinational corporations holding significant market share alongside numerous smaller, specialized firms. While precise market share figures for individual companies are proprietary and vary by segment, estimates suggest that the top 5 players account for approximately xx% of the total market revenue in 2025. Innovation is driven by several factors: increasing sophistication of cyber threats, evolving government regulations (e.g., PIPEDA), and the growing adoption of cloud computing and IoT devices. Mergers and acquisitions (M&A) activity is robust, with deal values reaching an estimated xx Million in 2024, indicating consolidation and expansion within the industry. For example, the acquisition of smaller niche players by larger firms enhances their service offerings and expands their reach. Product substitution is a significant factor, with continuous advancements in technologies like AI and machine learning leading to the replacement of older, less effective solutions. End-user trends favour integrated security solutions that offer comprehensive protection across multiple platforms and devices.

Canada Cybersecurity Industry Industry Trends & Insights

The Canadian cybersecurity market is experiencing robust growth, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fuelled by several key factors, including the rising prevalence of cyberattacks targeting businesses and governments, increased awareness of data privacy regulations, and the expanding adoption of digital technologies across various sectors. Technological disruptions, particularly the rise of AI-powered security solutions, cloud-based security services, and extended detection and response (XDR) capabilities, are reshaping the competitive landscape. Consumer preferences are shifting towards integrated, user-friendly security solutions that require minimal technical expertise. The market is becoming increasingly competitive, with established players facing challenges from both smaller agile startups and international competitors. Market penetration of advanced threat protection solutions remains relatively low, presenting significant growth opportunities.

Dominant Markets & Segments in Canada Cybersecurity Industry

The Canadian cybersecurity market is diversified, but certain segments show clear dominance.

- By End User: The Government & Defense sector leads due to its critical infrastructure and sensitive data, followed closely by BFSI (Banking, Financial Services, and Insurance) due to stringent regulatory compliance requirements and high-value assets. These segments are characterized by significant investments in advanced security technologies and specialized expertise. The Healthcare sector is also experiencing rapid growth, driven by the increasing adoption of electronic health records and connected medical devices.

- By Deployment: Cloud-based deployments are experiencing the fastest growth, driven by scalability, cost-efficiency, and enhanced accessibility. This trend is accelerated by increasing government mandates promoting cloud adoption. On-premise solutions, however, remain prevalent for organizations with strict data sovereignty requirements.

- By Offering: Services are the dominant segment, reflecting the need for specialized expertise in threat detection, incident response, and security consulting. This sector encompasses a wide array of services, from vulnerability assessments to security audits and managed security services.

The dominance of these segments is primarily driven by factors like increasing cyber threats specific to each industry, stringent regulatory frameworks in sectors like finance and healthcare, and the overall adoption of digital technologies. Government initiatives to encourage cybersecurity investment and infrastructure upgrades in these critical sectors further boost the segment's growth.

Canada Cybersecurity Industry Product Developments

Recent product innovations focus on enhancing the effectiveness of security solutions through AI-powered threat detection, automation, and integration with cloud platforms. This includes the development of advanced threat detection and response systems (e.g., XDR), enhanced data loss prevention (DLP) tools, and improved security information and event management (SIEM) solutions. These advanced capabilities offer improved threat visibility, enhanced response times, and reduced overall security risk. The focus is on integrating security seamlessly within existing IT infrastructure and adapting to the dynamic threatscape of the cloud and IoT environments. The market favors solutions that provide a holistic approach to security, rather than individual point products.

Report Scope & Segmentation Analysis

This report segments the Canadian cybersecurity market by various criteria:

By Offering: Security Type (e.g., network security, endpoint security, cloud security, data security, etc.) Each type experiences varying growth rates based on specific market needs and technological advancements. Market size is highly dependent on the adoption rate in each sector and the level of government spending on each security segment. Competition is intense due to a large number of players, forcing constant innovation and price competitiveness.

By Deployment: Cloud and On-premise solutions, reflecting differing user needs and IT infrastructures. Market size projections suggest a faster CAGR for cloud deployments, while on-premise retains a significant market share due to legacy systems and regulatory compliance. Competition in cloud security is increasing due to new players and the ease of market entry.

By End-User: BFSI, Healthcare, Manufacturing, Government & Defense, IT and Telecommunication, and Other End Users. Market size for each segment varies widely, based on industry-specific threats, regulatory requirements, and digitalization levels. Competition in each sector is influenced by specialized solutions providers tailoring their services to specific industry needs.

Other Types: Services encompasses a significant portion of the market, driven by demand for professional security expertise.

Key Drivers of Canada Cybersecurity Industry Growth

Several factors drive the growth of Canada's cybersecurity industry:

- Increased Cyberattacks: The rising frequency and sophistication of cyber threats, targeting both businesses and government entities, are forcing organizations to invest heavily in cybersecurity solutions.

- Stringent Government Regulations: Canada's robust data privacy regulations (PIPEDA) and increasing cybersecurity standards push organizations to improve their security postures.

- Technological Advancements: Innovation in areas such as AI, machine learning, and cloud computing fuels the development of more effective security solutions.

- Growing Adoption of Cloud Computing and IoT: Increased reliance on cloud services and interconnected devices expands the attack surface, driving demand for robust cybersecurity measures.

Challenges in the Canada Cybersecurity Industry Sector

The Canadian cybersecurity industry faces several challenges:

- Skills Shortage: A significant lack of qualified cybersecurity professionals hinders the industry's growth. This skill shortage is causing challenges in providing adequate security services across the board.

- High Cost of Security Solutions: Implementing and maintaining robust cybersecurity infrastructure can be extremely expensive for organizations, particularly smaller businesses.

- Evolving Threat Landscape: Cybercriminals constantly adapt their tactics, making it challenging to stay ahead of emerging threats. This necessitates continuous investment in updating security measures.

- Regulatory Complexity: Navigating the complex web of cybersecurity regulations can prove difficult for organizations, requiring significant effort for compliance.

Emerging Opportunities in Canada Cybersecurity Industry

Significant opportunities exist within the Canadian cybersecurity market:

- Growth of Cloud Security: The increasing adoption of cloud services creates a large market for cloud-based security solutions.

- Demand for AI-powered Security: The use of AI and machine learning to automate threat detection and response offers significant efficiency gains.

- Focus on IoT Security: The proliferation of IoT devices presents both challenges and opportunities for securing these interconnected systems.

- Expansion into Specialized Sectors: Growth potential exists in providing tailored cybersecurity solutions to specific industry segments, such as healthcare and finance.

Leading Players in the Canada Cybersecurity Industry Market

- XBASE Technologies Corporation

- Cyber Unit Inc

- IBM Corporation

- Groupe Access

- Check Point Software Technologies Ltd

- Cisco Systems Inc

- F12 Net

- Microsoft Corporation

- ELEKS Holding OU

- Sophos Ltd

- ProofPoint Inc

Key Developments in Canada Cybersecurity Industry Industry

January 2022: Proofpoint Inc acquired Dathena, enhancing its cloud-based security solutions with AI-driven data classification. This acquisition significantly strengthens Proofpoint's position in the market by addressing the growing need for robust data protection in hybrid work environments.

May 2022: Microsoft Corporation expanded its cybersecurity capabilities with the launch of Microsoft Security Experts, combining expert-trained technologies with human-led services, offering comprehensive managed security solutions to address complex cyber threats. This expansion underscores Microsoft's commitment to providing advanced security solutions for organizations of all sizes.

Strategic Outlook for Canada Cybersecurity Industry Market

The Canadian cybersecurity market is poised for continued growth, driven by increasing cyber threats, stringent regulations, and the expanding adoption of digital technologies. Opportunities abound in the areas of cloud security, AI-powered solutions, and specialized industry-specific offerings. Companies that can effectively address the skills shortage and offer innovative, cost-effective solutions will be well-positioned to capitalize on this expanding market. The continued focus on proactive threat detection, incident response, and data privacy will be critical for future success. The industry's growth will be closely linked to government initiatives, technological advancements, and the evolving threat landscape.

Canada Cybersecurity Industry Segmentation

-

1. Offering

-

1.1. Security Type

- 1.1.1. Cloud Security

- 1.1.2. Data Security

- 1.1.3. Identity Access Management

- 1.1.4. Network Security

- 1.1.5. Consumer Security

- 1.1.6. Infrastructure Protection

- 1.1.7. Other Types

- 1.2. Services

-

1.1. Security Type

-

2. Deployment

- 2.1. Cloud

- 2.2. On-premise

-

3. End User

- 3.1. BFSI

- 3.2. Healthcare

- 3.3. Manufacturing

- 3.4. Government & Defense

- 3.5. IT and Telecommunication

- 3.6. Other End Users

Canada Cybersecurity Industry Segmentation By Geography

- 1. Canada

Canada Cybersecurity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.99% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Rising Digitalization

- 3.2.2 e-Commerce

- 3.2.3 and IT Infrastructure for Businesses; Economic Growth Supporting New Businesses; Government Policies for Cybersecurity Driving the Market

- 3.3. Market Restrains

- 3.3.1. Lack of Cybersecurity Workforce

- 3.4. Market Trends

- 3.4.1. Government Policies to Dominate the Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Security Type

- 5.1.1.1. Cloud Security

- 5.1.1.2. Data Security

- 5.1.1.3. Identity Access Management

- 5.1.1.4. Network Security

- 5.1.1.5. Consumer Security

- 5.1.1.6. Infrastructure Protection

- 5.1.1.7. Other Types

- 5.1.2. Services

- 5.1.1. Security Type

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. BFSI

- 5.3.2. Healthcare

- 5.3.3. Manufacturing

- 5.3.4. Government & Defense

- 5.3.5. IT and Telecommunication

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Eastern Canada Canada Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 7. Western Canada Canada Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 8. Central Canada Canada Cybersecurity Industry Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 XBASE Technologies Corporation*List Not Exhaustive

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 Cyber Unit Inc

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 IBM Corporation

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 Groupe Access

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 Check Point Software Technologies Ltd

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Cisco Systems Inc

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 F12 Net

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Microsoft Corporation

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 ELEKS Holding OU

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 Sophos Ltd

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.11 ProofPoint Inc

- 9.2.11.1. Overview

- 9.2.11.2. Products

- 9.2.11.3. SWOT Analysis

- 9.2.11.4. Recent Developments

- 9.2.11.5. Financials (Based on Availability)

- 9.2.1 XBASE Technologies Corporation*List Not Exhaustive

List of Figures

- Figure 1: Canada Cybersecurity Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Canada Cybersecurity Industry Share (%) by Company 2024

List of Tables

- Table 1: Canada Cybersecurity Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Canada Cybersecurity Industry Revenue Million Forecast, by Offering 2019 & 2032

- Table 3: Canada Cybersecurity Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 4: Canada Cybersecurity Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Canada Cybersecurity Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Canada Cybersecurity Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Eastern Canada Canada Cybersecurity Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Western Canada Canada Cybersecurity Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Central Canada Canada Cybersecurity Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Canada Cybersecurity Industry Revenue Million Forecast, by Offering 2019 & 2032

- Table 11: Canada Cybersecurity Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 12: Canada Cybersecurity Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 13: Canada Cybersecurity Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Cybersecurity Industry?

The projected CAGR is approximately 10.99%.

2. Which companies are prominent players in the Canada Cybersecurity Industry?

Key companies in the market include XBASE Technologies Corporation*List Not Exhaustive, Cyber Unit Inc, IBM Corporation, Groupe Access, Check Point Software Technologies Ltd, Cisco Systems Inc, F12 Net, Microsoft Corporation, ELEKS Holding OU, Sophos Ltd, ProofPoint Inc.

3. What are the main segments of the Canada Cybersecurity Industry?

The market segments include Offering, Deployment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.96 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Digitalization. e-Commerce. and IT Infrastructure for Businesses; Economic Growth Supporting New Businesses; Government Policies for Cybersecurity Driving the Market.

6. What are the notable trends driving market growth?

Government Policies to Dominate the Market Growth.

7. Are there any restraints impacting market growth?

Lack of Cybersecurity Workforce.

8. Can you provide examples of recent developments in the market?

May 2022 - Microsoft Corporation announced the expansion of its cybersecurity capabilities under the Microsoft Security Experts service category, combining expert-trained technologies with human-led services. The new managed services include Microsoft Defender Experts for Hunting and Microsoft Defender Experts for XDR.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Cybersecurity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Cybersecurity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Cybersecurity Industry?

To stay informed about further developments, trends, and reports in the Canada Cybersecurity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence