Key Insights

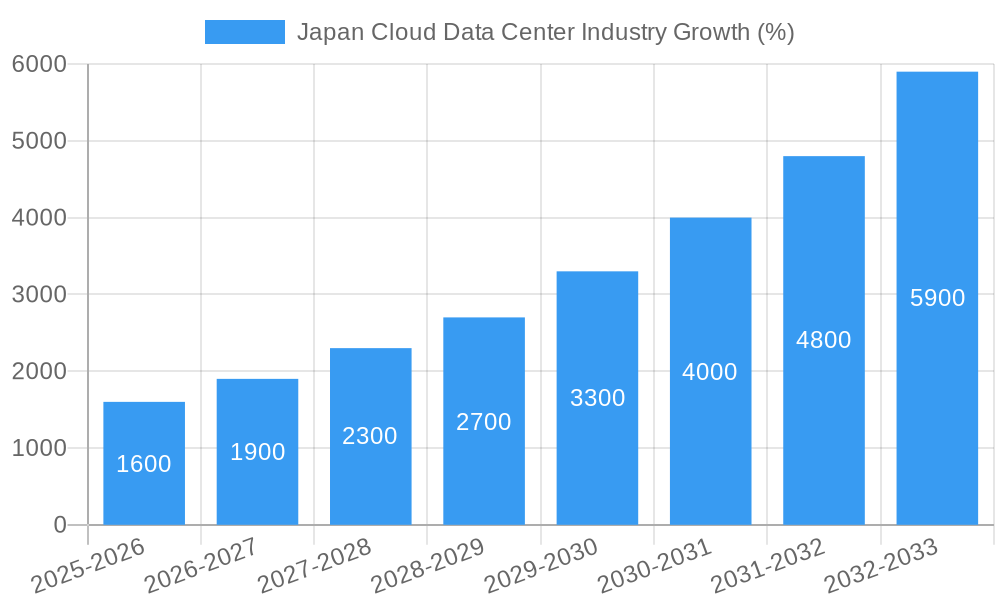

The Japan cloud data center market is experiencing robust growth, driven by the increasing adoption of cloud computing services across various sectors, including finance, manufacturing, and telecommunications. The market's 21.06% CAGR (2019-2024) indicates significant expansion, fueled by factors such as the rising demand for digital transformation initiatives, the proliferation of big data applications requiring substantial storage and processing power, and the government's push for digitalization. Key growth hotspots include Osaka and Tokyo, reflecting the concentration of businesses and technological infrastructure in these metropolitan areas. The market is segmented by data center size (small, medium, mega, massive), tier type (Tier 1, Tier 2, Tier 3, etc.), and utilization (utilized, non-utilized), providing a granular view of the industry's structure. While precise market size figures are not available, based on the CAGR and considering the global cloud data center market trends, a reasonable estimate for the 2025 market size could fall in the range of $5-10 billion USD, given the advanced digital economy in Japan. Large enterprises and hyperscale providers are major drivers of demand, impacting the development of larger, Tier-1 facilities. However, the market faces challenges such as high land costs in major cities, stringent regulations, and the need for robust disaster recovery strategies in a seismically active region. Future growth will be shaped by advancements in technologies like edge computing, 5G rollout, and the increasing adoption of AI and machine learning, which will further increase demand for sophisticated data center infrastructure.

The competitive landscape includes both international giants like Equinix and Digital Realty Trust, and domestic players like NTT Ltd and KDDI Corporation (Telehouse). This mix reflects both the global nature of the cloud computing market and the strong presence of established Japanese telecommunications and technology companies. The continued expansion of cloud services, particularly those focused on hybrid and multi-cloud deployments, will likely intensify competition and drive further innovation within the sector. The forecast period of 2025-2033 presents significant opportunities for growth, particularly for providers who can offer solutions that address the specific needs of Japanese businesses and comply with the country’s stringent regulatory framework. Strategic partnerships and investments in advanced technologies will be crucial for sustained success in this dynamic market.

Japan Cloud Data Center Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Japan cloud data center industry, encompassing market size, segmentation, competitive landscape, and future growth projections. The report covers the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033. Key segments analyzed include geographic location (Tokyo, Osaka, Rest of Japan), data center size (Small, Medium, Mega, Massive, Large), tier type (Tier 1, Tier 2, Tier 3), and absorption (Utilized, Non-Utilized). The report also examines major industry players, including Equinix Inc, Zenlayer Inc, and NTT Ltd., and analyzes their strategic initiatives and market share. This report is essential for industry stakeholders, investors, and businesses seeking to understand and capitalize on the growth opportunities within the dynamic Japanese cloud data center market. The report includes detailed financial projections and valuable insights to inform strategic decision-making. Expected market value in 2025 is estimated at xx Million.

Japan Cloud Data Center Industry Market Concentration & Innovation

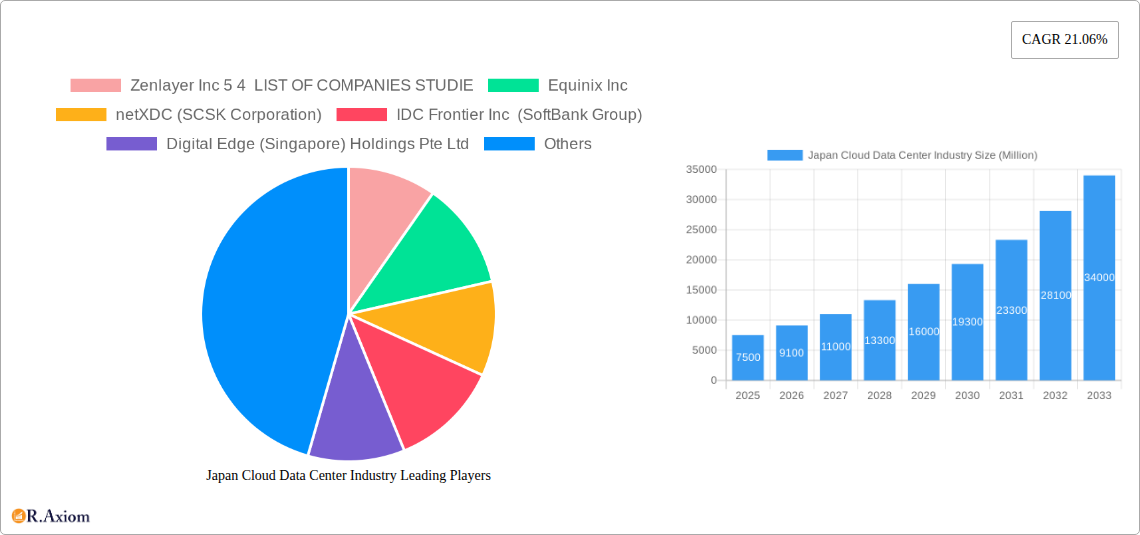

The Japanese cloud data center market exhibits a moderately concentrated landscape, with a handful of major players holding significant market share. Equinix, NTT Ltd., and SoftBank (through IDC Frontier) are among the dominant players. However, smaller, specialized providers and new entrants continue to emerge, fostering competition and innovation. Market share data for 2024 reveals Equinix holding approximately xx% of the market, NTT Ltd. holding xx%, and SoftBank holding xx%, with the remaining share distributed among other players. Innovation is driven by increasing demand for high-capacity, low-latency data centers, fueled by the growth of cloud computing, 5G networks, and the burgeoning digital economy. Regulatory frameworks, while generally supportive of technological advancement, also place emphasis on data security and privacy, influencing investment decisions and operational practices. M&A activity in the sector has been relatively moderate in recent years, with deal values averaging around xx Million per transaction. Key M&A activities include several smaller acquisitions focused on enhancing network connectivity and regional expansion. End-user trends show a growing preference for hyperscale data centers and robust disaster recovery capabilities, driving investment in advanced technologies like AI-powered infrastructure management and sustainable energy solutions.

Japan Cloud Data Center Industry Industry Trends & Insights

The Japan cloud data center market is experiencing robust growth, driven by several key factors. The increasing adoption of cloud services across various industries, coupled with the government's digital transformation initiatives, is significantly boosting demand for data center capacity. The compound annual growth rate (CAGR) is projected to be xx% during the forecast period (2025-2033). This growth is further fueled by technological disruptions, including the widespread adoption of edge computing, which is creating demand for strategically located data centers closer to end-users. Consumer preferences are shifting towards higher levels of reliability, security, and sustainability, prompting data center operators to invest in advanced technologies and environmentally friendly solutions. Competitive dynamics are characterized by intense competition among established players and the emergence of new players, resulting in price pressures and increased innovation. Market penetration of cloud services is estimated to reach xx% by 2033, showcasing the transformative impact of cloud computing on the Japanese business landscape.

Dominant Markets & Segments in Japan Cloud Data Center Industry

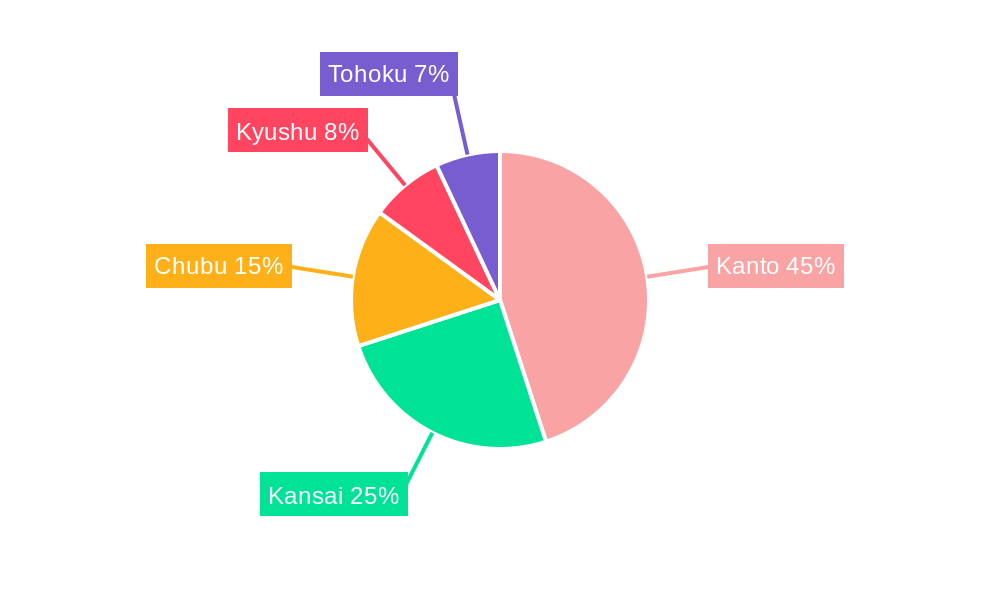

Leading Regions: Tokyo and Osaka are the dominant markets, accounting for the majority of data center capacity and investment. This dominance is primarily due to their established IT infrastructure, strong connectivity, and concentration of businesses and consumers. The "Rest of Japan" segment demonstrates steady growth, driven by increasing regional digitalization efforts.

Data Center Size: Large and Mega data centers currently dominate the market, catering to the needs of hyperscale cloud providers and large enterprises. However, the demand for smaller and medium-sized facilities is also increasing, reflecting the growth of smaller businesses and specialized applications.

Tier Type: Tier III data centers currently hold a significant share, reflecting the demand for high availability and redundancy. Tier IV facilities are also gaining traction, especially among organizations with stringent reliability requirements.

Absorption: Utilized capacity is currently high, reflecting strong demand, but non-utilized capacity also exists, reflecting the cyclical nature of the industry and the time needed to commission new facilities. This creates opportunities for expansion and further investment.

Other End-Users: The financial services sector, government agencies, and telecommunications companies are major consumers of data center services, driving significant demand.

The dominance of Tokyo and Osaka is mainly due to superior infrastructure, concentration of businesses, and government incentives. The government's digitalization drive is fueling investments across all segments.

Japan Cloud Data Center Industry Product Developments

Recent product innovations in the Japanese cloud data center market focus on enhancing efficiency, security, and sustainability. This includes the adoption of advanced cooling technologies, AI-powered management systems, and renewable energy sources. Data centers are increasingly incorporating features like edge computing capabilities, enabling low-latency applications and enhanced performance for various services. These developments are strategically aligned with market demands for greater efficiency, reduced environmental impact, and enhanced performance, creating a competitive advantage for providers who adopt these innovative solutions.

Report Scope & Segmentation Analysis

This report segments the Japan cloud data center market by geographic location (Tokyo, Osaka, Rest of Japan), data center size (Small, Medium, Mega, Massive, Large), tier type (Tier 1, Tier 2, Tier 3), and absorption (Utilized, Non-Utilized). Each segment is analyzed based on its current market size, growth projections, and competitive dynamics. Growth projections vary across segments, with Tokyo and Osaka expected to continue their dominance due to strong demand and infrastructure development. The mega and large data center segments are poised for significant growth driven by hyperscale cloud adoption. The utilized capacity segment is expected to grow steadily, although some non-utilized capacity will remain due to cyclical demand and construction timelines.

Key Drivers of Japan Cloud Data Center Industry Growth

Several key factors are driving the growth of the Japan cloud data center industry: the increasing adoption of cloud computing across various sectors, supportive government policies promoting digital transformation, substantial investments in advanced infrastructure, and the demand for high-capacity, low-latency services to support emerging technologies like 5G and IoT. Furthermore, the ongoing digitalization efforts of Japanese businesses and the rise of data-intensive applications are significantly increasing the demand for secure and reliable data center services. These factors collectively create a favorable environment for sustained growth in the coming years.

Challenges in the Japan Cloud Data Center Industry Sector

The Japan cloud data center sector faces challenges including high land costs and limited availability in prime locations, particularly in Tokyo and Osaka. Competition from established international players and the need for significant upfront investment represent further obstacles. Ensuring compliance with stringent data privacy regulations and navigating potential supply chain disruptions also present operational complexities. The impact of these challenges can be quantified in terms of project delays, increased operating costs, and reduced profit margins for certain players.

Emerging Opportunities in Japan Cloud Data Center Industry

Significant opportunities exist in the expansion of edge data centers to support 5G and IoT applications. Growth is also anticipated in the development of sustainable and energy-efficient data center solutions. The increasing demand for specialized cloud services for industries like finance and healthcare creates further opportunities. Moreover, the government's continued support for digital transformation will continue to fuel investments in the sector. These opportunities create a dynamic landscape ripe for innovation and strategic growth.

Leading Players in the Japan Cloud Data Center Industry Market

- Zenlayer Inc

- Equinix Inc

- netXDC (SCSK Corporation)

- IDC Frontier Inc (SoftBank Group)

- Digital Edge (Singapore) Holdings Pte Ltd

- NEC Corporation

- Colt Technology Services

- Digital Realty Trust Inc

- AirTrunk Operating Pty Ltd

- Telehouse (KDDI Corporation)

- Arteria Networks Corporation

- NTT Ltd

Key Developments in Japan Cloud Data Center Industry Industry

November 2022: Equinix announced its 15th international business exchange (IBX) data center in Tokyo, Japan, representing a USD 115 Million investment and adding 3,700 cabinets once fully operational. This significantly increased capacity in a key market.

October 2022: Zenlayer's joint venture with Megaport expands its global reach and enhances service offerings, potentially increasing its market share and competitive edge.

September 2022: NTT Corporation's investment in the "Keihanna Data Center" expands capacity in Kyoto prefecture, highlighting investment in regional infrastructure.

These developments demonstrate significant investment in expanding capacity and enhancing service offerings, reflecting the continued growth and dynamism of the Japanese cloud data center market.

Strategic Outlook for Japan Cloud Data Center Industry Market

The Japanese cloud data center market is poised for continued strong growth, driven by ongoing digital transformation initiatives, increasing cloud adoption, and the emergence of new technologies. Opportunities for growth exist in expanding capacity, enhancing sustainability, and developing specialized services to meet the diverse needs of various sectors. Future market potential is substantial, with continued investment expected across all segments. Strategic positioning for future success requires a focus on innovation, scalability, and operational efficiency in a highly competitive and rapidly evolving landscape.

Japan Cloud Data Center Industry Segmentation

-

1. Hotspot

- 1.1. Osaka

- 1.2. Tokyo

- 1.3. Rest of Japan

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1 and 2

- 3.2. Tier 3

- 3.3. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

5. Colocation Type

- 5.1. Hyperscale

- 5.2. Retail

- 5.3. Wholesale

-

6. End User

- 6.1. BFSI

- 6.2. Cloud

- 6.3. E-Commerce

- 6.4. Government

- 6.5. Manufacturing

- 6.6. Media & Entertainment

- 6.7. Telecom

- 6.8. Other End User

Japan Cloud Data Center Industry Segmentation By Geography

- 1. Japan

Japan Cloud Data Center Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 21.06% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rise of E-Commerce; Flourishing Startup Culture

- 3.3. Market Restrains

- 3.3.1. Slow Penetration Rate in Developing Countries

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. Osaka

- 5.1.2. Tokyo

- 5.1.3. Rest of Japan

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1 and 2

- 5.3.2. Tier 3

- 5.3.3. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.5. Market Analysis, Insights and Forecast - by Colocation Type

- 5.5.1. Hyperscale

- 5.5.2. Retail

- 5.5.3. Wholesale

- 5.6. Market Analysis, Insights and Forecast - by End User

- 5.6.1. BFSI

- 5.6.2. Cloud

- 5.6.3. E-Commerce

- 5.6.4. Government

- 5.6.5. Manufacturing

- 5.6.6. Media & Entertainment

- 5.6.7. Telecom

- 5.6.8. Other End User

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. Kanto Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 7. Kansai Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 8. Chubu Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 9. Kyushu Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 10. Tohoku Japan Cloud Data Center Industry Analysis, Insights and Forecast, 2019-2031

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Zenlayer Inc 5 4 LIST OF COMPANIES STUDIE

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Equinix Inc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 netXDC (SCSK Corporation)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 IDC Frontier Inc (SoftBank Group)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Digital Edge (Singapore) Holdings Pte Ltd

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 NEC Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Colt Technology Services

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Digital Realty Trust Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 AirTrunk Operating Pty Ltd

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Telehouse (KDDI Corporation)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Arteria Networks Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 NTT Ltd

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Zenlayer Inc 5 4 LIST OF COMPANIES STUDIE

List of Figures

- Figure 1: Japan Cloud Data Center Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Japan Cloud Data Center Industry Share (%) by Company 2024

List of Tables

- Table 1: Japan Cloud Data Center Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Japan Cloud Data Center Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Japan Cloud Data Center Industry Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 4: Japan Cloud Data Center Industry Volume K Unit Forecast, by Hotspot 2019 & 2032

- Table 5: Japan Cloud Data Center Industry Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 6: Japan Cloud Data Center Industry Volume K Unit Forecast, by Data Center Size 2019 & 2032

- Table 7: Japan Cloud Data Center Industry Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 8: Japan Cloud Data Center Industry Volume K Unit Forecast, by Tier Type 2019 & 2032

- Table 9: Japan Cloud Data Center Industry Revenue Million Forecast, by Absorption 2019 & 2032

- Table 10: Japan Cloud Data Center Industry Volume K Unit Forecast, by Absorption 2019 & 2032

- Table 11: Japan Cloud Data Center Industry Revenue Million Forecast, by Colocation Type 2019 & 2032

- Table 12: Japan Cloud Data Center Industry Volume K Unit Forecast, by Colocation Type 2019 & 2032

- Table 13: Japan Cloud Data Center Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 14: Japan Cloud Data Center Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 15: Japan Cloud Data Center Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 16: Japan Cloud Data Center Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 17: Japan Cloud Data Center Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Japan Cloud Data Center Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 19: Kanto Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Kanto Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Kansai Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Kansai Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Chubu Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Chubu Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 25: Kyushu Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Kyushu Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 27: Tohoku Japan Cloud Data Center Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Tohoku Japan Cloud Data Center Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 29: Japan Cloud Data Center Industry Revenue Million Forecast, by Hotspot 2019 & 2032

- Table 30: Japan Cloud Data Center Industry Volume K Unit Forecast, by Hotspot 2019 & 2032

- Table 31: Japan Cloud Data Center Industry Revenue Million Forecast, by Data Center Size 2019 & 2032

- Table 32: Japan Cloud Data Center Industry Volume K Unit Forecast, by Data Center Size 2019 & 2032

- Table 33: Japan Cloud Data Center Industry Revenue Million Forecast, by Tier Type 2019 & 2032

- Table 34: Japan Cloud Data Center Industry Volume K Unit Forecast, by Tier Type 2019 & 2032

- Table 35: Japan Cloud Data Center Industry Revenue Million Forecast, by Absorption 2019 & 2032

- Table 36: Japan Cloud Data Center Industry Volume K Unit Forecast, by Absorption 2019 & 2032

- Table 37: Japan Cloud Data Center Industry Revenue Million Forecast, by Colocation Type 2019 & 2032

- Table 38: Japan Cloud Data Center Industry Volume K Unit Forecast, by Colocation Type 2019 & 2032

- Table 39: Japan Cloud Data Center Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 40: Japan Cloud Data Center Industry Volume K Unit Forecast, by End User 2019 & 2032

- Table 41: Japan Cloud Data Center Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: Japan Cloud Data Center Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Cloud Data Center Industry?

The projected CAGR is approximately 21.06%.

2. Which companies are prominent players in the Japan Cloud Data Center Industry?

Key companies in the market include Zenlayer Inc 5 4 LIST OF COMPANIES STUDIE, Equinix Inc, netXDC (SCSK Corporation), IDC Frontier Inc (SoftBank Group), Digital Edge (Singapore) Holdings Pte Ltd, NEC Corporation, Colt Technology Services, Digital Realty Trust Inc, AirTrunk Operating Pty Ltd, Telehouse (KDDI Corporation), Arteria Networks Corporation, NTT Ltd.

3. What are the main segments of the Japan Cloud Data Center Industry?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption, Colocation Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rise of E-Commerce; Flourishing Startup Culture.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Slow Penetration Rate in Developing Countries.

8. Can you provide examples of recent developments in the market?

November 2022: Equinix announced its 15th international business exchange (IBX) data centre in Tokyo, Japan. The company said that it has made an initial investment of USD 115 million on the new data centre, touted TY15. The first phase of TY15 will provide an initial capacity of approximately 1,200 cabinets, and 3,700 cabinets when fully built out.October 2022: Zenlayer entered into a joint venture with Megaport to strengthen and expand its presence globally. The partnership is aimed at providing enhanced services such as improved network connectivity, real time provisioning, and on demand private connectivity for its clients around the globe.September 2022: NTT Corporation announced to invest approximately YEN 40 billion through NTT Global Data Centers Corporation to build new "Keihanna Data Center" in Kyoto Prefecture. The building is a four-story, seismic-isolated structure that will stably supply a total of 30 MW for IT load (starting at 6 MW and gradually expanding) to a server room space of 10,900 sqm (equivalent to 4,800 racks).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Cloud Data Center Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Cloud Data Center Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Cloud Data Center Industry?

To stay informed about further developments, trends, and reports in the Japan Cloud Data Center Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence