Key Insights

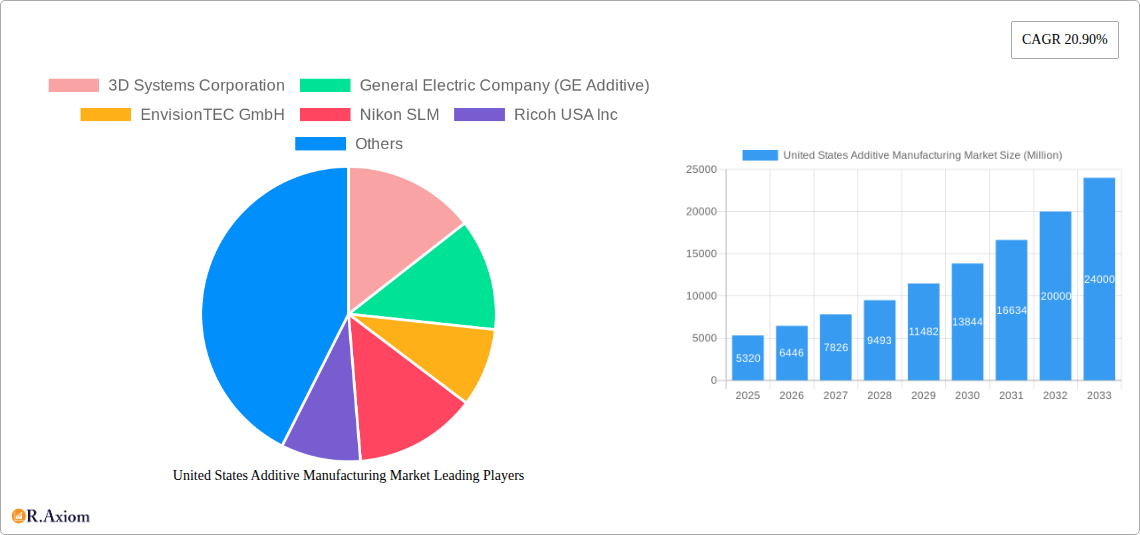

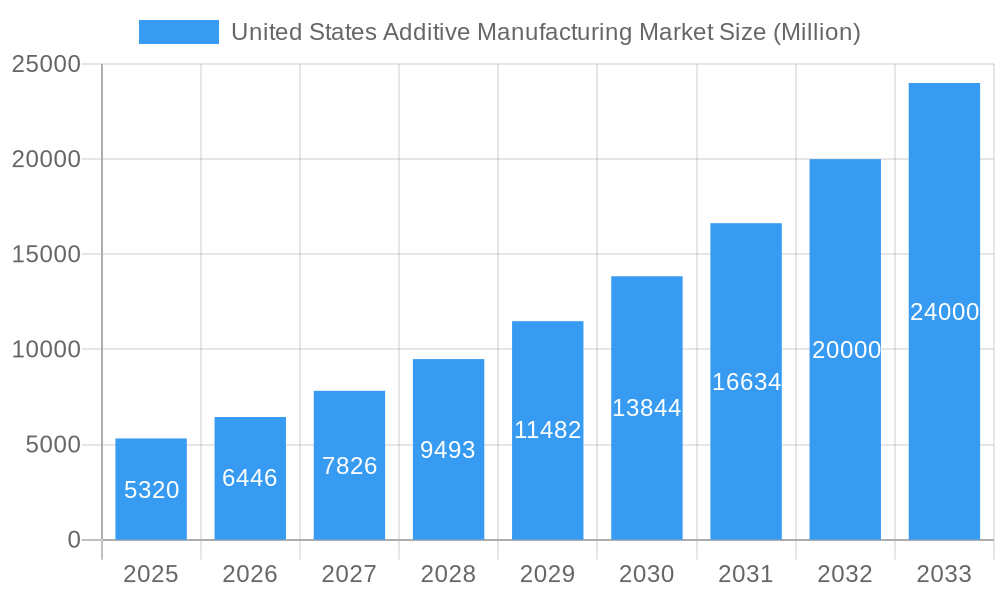

The United States additive manufacturing (AM) market, valued at $5.32 billion in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 20.90% from 2025 to 2033. This significant expansion is driven by several key factors. Increasing adoption of AM technologies across diverse industries, such as aerospace, automotive, healthcare, and consumer goods, is a major catalyst. The ability of AM to produce complex geometries, lightweight components, and customized products at lower costs compared to traditional manufacturing methods is fueling market demand. Furthermore, advancements in materials science, leading to the development of high-performance polymers, metals, and composites suitable for AM processes, are expanding the application scope of this technology. Government initiatives promoting domestic manufacturing and technological innovation are also contributing to market growth. Competition among established players like 3D Systems, GE Additive, and Stratasys, along with emerging innovative companies, is fostering technological advancements and driving down prices, making AM more accessible to a wider range of businesses.

United States Additive Manufacturing Market Market Size (In Billion)

However, challenges remain. The relatively high initial investment costs associated with AM equipment and materials can act as a barrier to entry for smaller companies. Concerns regarding scalability and the need for skilled workforce to operate and maintain AM systems pose additional hurdles. Despite these limitations, the long-term prospects for the US AM market remain exceptionally positive. The continued development of faster, more reliable, and cost-effective AM technologies, coupled with growing awareness of its benefits across various sectors, is expected to drive substantial market expansion throughout the forecast period. The market's focus is shifting towards wider adoption, improved material properties, and increased efficiency, ensuring sustained growth and innovation in the coming years.

United States Additive Manufacturing Market Company Market Share

United States Additive Manufacturing Market: A Comprehensive Report (2019-2033)

This comprehensive report provides a detailed analysis of the United States Additive Manufacturing (AM) market, covering the period from 2019 to 2033. It delves into market dynamics, technological advancements, key players, and future growth prospects, offering invaluable insights for industry stakeholders. The report leverages a robust data set to forecast market size, identify key trends, and reveal untapped opportunities within this rapidly evolving sector.

United States Additive Manufacturing Market Market Concentration & Innovation

The United States additive manufacturing market is characterized by a dynamic and evolving landscape, blending the influence of established industry leaders with the disruptive force of emerging innovators. While a discernible concentration exists among key players, driven by substantial research and development investments, extensive intellectual property portfolios, and robust brand recognition, the ecosystem thrives on the significant contributions of a vast number of smaller companies and ambitious startups. These agile entities are instrumental in pushing the boundaries of innovation and fostering a competitive environment. For 2024, preliminary market share estimates indicate that the top five dominant companies collectively command approximately 60-65% of the market, with industry stalwarts such as 3D Systems Corporation, General Electric Company (through its GE Additive division), and Stratasys Ltd. consistently recognized as frontrunners.

Innovation within the additive manufacturing (AM) sector is a multi-faceted pursuit, propelled by continuous breakthroughs in materials science, the refinement of diverse printing technologies (including but not limited to Stereolithography (SLA), Selective Laser Sintering (SLS), Directed Energy Deposition (DED), and Multi Jet Fusion (MJF)), and the development of sophisticated software solutions. Navigating this innovative terrain requires a keen understanding of stringent regulatory frameworks, particularly those pertaining to material safety, product certification, and design integrity, which exert a significant influence on both the pace of innovation and market access. The emergence of novel materials, boasting enhanced properties such as superior strength-to-weight ratios, increased thermal resistance, and advanced biocompatibility for metals and polymers alike, is a critical catalyst for expanding the application scope of AM. While traditional manufacturing processes continue to represent a competitive alternative, the inherent advantages of AM—namely, its unparalleled capabilities in rapid prototyping, highly customized production runs, and efficient on-demand manufacturing—are progressively widening its market penetration. Shifting end-user preferences, which increasingly favor mass customization and the acceleration of product lifecycles, are a powerful driving force behind the widespread adoption of AM technologies across a broad spectrum of industries.

Mergers and acquisitions (M&A) have emerged as a pivotal strategic tool in shaping the trajectory and competitive dynamics of the United States additive manufacturing market. Although precise financial figures for all transactions are not always publicly disclosed, the cumulative impact of significant M&A activities over the past five years, with reported average deal values in the range of $50-$100 million, underscores a clear trend towards market consolidation, the acquisition of specialized expertise, and the synergistic integration of complementary technologies. These strategic moves are not only indicative of the immense strategic importance attributed to AM but also highlight an ongoing and vigorous race among companies to secure and fortify their positions as market leaders.

United States Additive Manufacturing Market Industry Trends & Insights

The United States additive manufacturing market is experiencing robust growth, driven by increased demand across diverse sectors. The market is expected to register a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, reaching a market value of xx Million by 2033. This growth is attributed to several converging factors: growing adoption of additive manufacturing in prototyping and low-volume production; increasing demand for customized products in industries such as aerospace, automotive, and healthcare; advancements in 3D printing technologies, resulting in faster printing speeds, higher accuracy, and improved material properties; and government initiatives and funding programs designed to promote the development and adoption of advanced manufacturing technologies, including additive manufacturing.

Technological advancements, such as the development of multi-material printing capabilities and the integration of AI in process optimization, are further accelerating market growth. However, the market faces challenges, including relatively high equipment costs, material limitations, and the need for skilled labor. Despite these challenges, market penetration is expanding rapidly, particularly within industries where customization, speed-to-market, and reduced material waste are critical success factors. Competitive dynamics are characterized by both intense competition among established players and the emergence of new entrants leveraging innovative technologies.

Dominant Markets & Segments in United States Additive Manufacturing Market

The aerospace and defense sectors represent the most dominant segments within the United States additive manufacturing market, accounting for a significant share of the total market value. The strong growth in these sectors is attributed to several key drivers:

- High Demand for Lightweight and High-Strength Parts: Additive manufacturing enables the creation of complex, lightweight parts with high strength-to-weight ratios, which are essential for aerospace and defense applications.

- Reduced Lead Times and Costs: AM technologies help to significantly reduce lead times and costs associated with the production of complex parts, which is critical in these time-sensitive industries.

- Increased Design Flexibility: AM enables the creation of parts with intricate geometries that are impossible to manufacture using traditional methods, leading to improved product performance and efficiency.

- Government Funding and Initiatives: Government initiatives and funding programs focused on advanced manufacturing technologies are further fueling growth within these sectors.

The dominance of these sectors is expected to continue, although growth in other sectors like healthcare and automotive is also accelerating, reflecting the widespread application of AM technologies across various industries.

United States Additive Manufacturing Market Product Developments

Recent product developments showcase a clear trend toward larger build volumes, faster printing speeds, and enhanced material capabilities. The introduction of robotic integration, as seen with the Alchemist 1, indicates a shift towards automated, high-throughput AM solutions. These advancements are addressing key limitations of traditional AM systems, expanding applications into high-volume production and larger-scale components. The market is witnessing increasing focus on materials suitable for specific industries such as biocompatible polymers for medical implants or high-temperature alloys for aerospace components.

Report Scope & Segmentation Analysis

This comprehensive report meticulously segments the United States additive manufacturing market to provide an in-depth understanding of its diverse components. The segmentation is structured around key parameters including:

- Technology: Categorizing the market by prevalent AM processes such as Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Melting (SLM), Direct Metal Laser Sintering (DMLS), and others.

- Material: Analyzing the market based on the types of materials utilized, including a broad range of polymers, advanced metals, and specialized ceramics.

- Application: Delineating market segments by their primary use cases, such as rapid prototyping, the creation of functional tooling, and the production of end-use parts.

- End-Use Industry: Examining the market's penetration and growth within key sectors including aerospace, automotive, healthcare, consumer goods, and industrial manufacturing.

Growth projections are carefully tailored to each segment, with notable emphasis placed on metal-based AM, which is experiencing exceptionally robust expansion fueled by escalating demand for high-performance, lightweight components in critical sectors like aerospace and automotive. Competitive dynamics are also analyzed at a granular level, revealing distinct levels of competition across various technologies and material categories. Market sizes are rigorously estimated for each technology, material, and application type, offering a precise and detailed view of the market's intricate segmentation.

Key Drivers of United States Additive Manufacturing Market Growth

The sustained and accelerated growth of the United States additive manufacturing market is underpinned by a confluence of powerful driving forces. Paramount among these are continuous technological advancements, encompassing not only faster printing speeds and the development of materials with superior mechanical and functional properties but also the engineering of larger build volumes, collectively enabling broader application possibilities. Concurrently, a burgeoning demand for customized products across a multitude of industries, coupled with the inherent cost and time efficiencies offered by AM technologies for both small-batch production and intricate designs, are significantly bolstering market expansion. Furthermore, strategic government initiatives aimed at fostering domestic advanced manufacturing capabilities and the increasing availability of a skilled workforce, adept in operating and innovating with AM systems, are acting as crucial enablers and catalysts for the sector's growth.

Challenges in the United States Additive Manufacturing Market Sector

Notwithstanding its impressive growth trajectory, the United States additive manufacturing market is not without its inherent challenges, which can temper its full potential. A significant hurdle remains the high capital expenditure associated with advanced AM equipment, presenting a substantial barrier to entry for many businesses, particularly smaller enterprises and startups. Additionally, the vulnerability of supply chains for specialized materials and critical equipment components can lead to disruptions and impact production timelines. The persistent shortage of skilled personnel, specifically those with the expertise to operate, maintain, and optimize complex AM systems, poses another considerable challenge, as the talent pool for these specialized roles is still developing. Finally, the intense competition among established players and the rapid emergence of new entrants further contribute to a dynamic and demanding market landscape, requiring continuous adaptation and strategic foresight from all stakeholders.

Emerging Opportunities in United States Additive Manufacturing Market

The additive manufacturing market presents several significant emerging opportunities. The increasing adoption of AM for mass customization and on-demand production is opening up new markets and applications. The development of new materials and printing processes for specific industries, particularly those requiring high-strength, lightweight components, offers considerable opportunities for growth. Increased integration of AM with other technologies, such as AI and robotics, is creating new possibilities for streamlining production processes. The expansion into new applications such as personalized medicine and sustainable manufacturing provides further growth potential.

Leading Players in the United States Additive Manufacturing Market Market

- 3D Systems Corporation

- General Electric Company (GE Additive)

- EnvisionTEC GmbH

- Nikon SLM

- Ricoh USA Inc

- EOS GmbH

- Exone Company

- MCOR Technology Ltd

- Materialise NV

- Optomec Inc

- Stratasys Ltd

- SLM Solutions Group AG

Key Developments in United States Additive Manufacturing Market Industry

- June 2024: Nikon SLM Solutions AG significantly bolstered its North American presence by commencing production of its high-performance NXG XII 600 metal additive manufacturing machine within the U.S. This strategic move aims to better serve the escalating demand from diverse industries across the continent and enhance local manufacturing capabilities.

- June 2024: Ricoh USA Inc. introduced RICOH All-In 3D Print, a comprehensive, fully managed on-site 3D printing solution designed to simplify and optimize the production workflow for 3D-printed prototypes, thereby streamlining the product development cycle for businesses.

- April 2024: Meltio, in collaboration with Accufacture, unveiled the Alchemist 1, an innovative large-scale robotic Directed Energy Deposition (DED) 3D printing work cell. This advanced system is specifically engineered for the efficient and precise production of large, dense metal parts, opening new possibilities for industrial applications.

Strategic Outlook for United States Additive Manufacturing Market Market

The United States additive manufacturing market is poised for significant growth over the next decade. Continued technological advancements, increasing demand for customized products, and supportive government policies will drive market expansion. The integration of AM into existing manufacturing processes and the exploration of new applications, such as personalized medicine and sustainable manufacturing, will create further growth opportunities. Companies that invest in R&D, expand their material and process capabilities, and develop robust supply chains will be best positioned to capitalize on the market's future potential.

United States Additive Manufacturing Market Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. Desktop 3D Printer

- 1.1.2. Industrial 3D Printer

-

1.2. Software

- 1.2.1. Design Software

- 1.2.2. Inspection Software

- 1.2.3. Scanning Software

- 1.3. Services

-

1.1. Hardware

-

2. Material

- 2.1. Polymer

- 2.2. Metal

- 2.3. Ceramic

-

3. Technology

- 3.1. Stereo Lithography

- 3.2. Selective Laser Sintering

- 3.3. Fused Deposition Modelling

- 3.4. Binder Jetting Printing

- 3.5. Other Technologies

-

4. End-user Vertical

- 4.1. Automotive

- 4.2. Aerospace and Defense

- 4.3. Healthcare

- 4.4. Consumer Electronics

- 4.5. Power and Energy

- 4.6. Fashion and Jewelry

- 4.7. Dentistry

- 4.8. Other End-user Verticals

United States Additive Manufacturing Market Segmentation By Geography

- 1. United States

United States Additive Manufacturing Market Regional Market Share

Geographic Coverage of United States Additive Manufacturing Market

United States Additive Manufacturing Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. Desktop 3D Printer

- 5.1.1.2. Industrial 3D Printer

- 5.1.2. Software

- 5.1.2.1. Design Software

- 5.1.2.2. Inspection Software

- 5.1.2.3. Scanning Software

- 5.1.3. Services

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Polymer

- 5.2.2. Metal

- 5.2.3. Ceramic

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. Stereo Lithography

- 5.3.2. Selective Laser Sintering

- 5.3.3. Fused Deposition Modelling

- 5.3.4. Binder Jetting Printing

- 5.3.5. Other Technologies

- 5.4. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.4.1. Automotive

- 5.4.2. Aerospace and Defense

- 5.4.3. Healthcare

- 5.4.4. Consumer Electronics

- 5.4.5. Power and Energy

- 5.4.6. Fashion and Jewelry

- 5.4.7. Dentistry

- 5.4.8. Other End-user Verticals

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. United States Additive Manufacturing Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. Desktop 3D Printer

- 6.1.1.2. Industrial 3D Printer

- 6.1.2. Software

- 6.1.2.1. Design Software

- 6.1.2.2. Inspection Software

- 6.1.2.3. Scanning Software

- 6.1.3. Services

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Polymer

- 6.2.2. Metal

- 6.2.3. Ceramic

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. Stereo Lithography

- 6.3.2. Selective Laser Sintering

- 6.3.3. Fused Deposition Modelling

- 6.3.4. Binder Jetting Printing

- 6.3.5. Other Technologies

- 6.4. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.4.1. Automotive

- 6.4.2. Aerospace and Defense

- 6.4.3. Healthcare

- 6.4.4. Consumer Electronics

- 6.4.5. Power and Energy

- 6.4.6. Fashion and Jewelry

- 6.4.7. Dentistry

- 6.4.8. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 3D Systems Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 General Electric Company (GE Additive)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 EnvisionTEC GmbH

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Nikon SLM

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ricoh USA Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 EOS GmbH

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Exone Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 MCOR Technology Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Materialise NV

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Optomec Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Stratasys Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 SLM Solutions Group AG*List Not Exhaustive

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 3D Systems Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Additive Manufacturing Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United States Additive Manufacturing Market Share (%) by Company 2025

List of Tables

- Table 1: United States Additive Manufacturing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 2: United States Additive Manufacturing Market Volume Billion Forecast, by Component 2020 & 2033

- Table 3: United States Additive Manufacturing Market Revenue Million Forecast, by Material 2020 & 2033

- Table 4: United States Additive Manufacturing Market Volume Billion Forecast, by Material 2020 & 2033

- Table 5: United States Additive Manufacturing Market Revenue Million Forecast, by Technology 2020 & 2033

- Table 6: United States Additive Manufacturing Market Volume Billion Forecast, by Technology 2020 & 2033

- Table 7: United States Additive Manufacturing Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 8: United States Additive Manufacturing Market Volume Billion Forecast, by End-user Vertical 2020 & 2033

- Table 9: United States Additive Manufacturing Market Revenue Million Forecast, by Region 2020 & 2033

- Table 10: United States Additive Manufacturing Market Volume Billion Forecast, by Region 2020 & 2033

- Table 11: United States Additive Manufacturing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 12: United States Additive Manufacturing Market Volume Billion Forecast, by Component 2020 & 2033

- Table 13: United States Additive Manufacturing Market Revenue Million Forecast, by Material 2020 & 2033

- Table 14: United States Additive Manufacturing Market Volume Billion Forecast, by Material 2020 & 2033

- Table 15: United States Additive Manufacturing Market Revenue Million Forecast, by Technology 2020 & 2033

- Table 16: United States Additive Manufacturing Market Volume Billion Forecast, by Technology 2020 & 2033

- Table 17: United States Additive Manufacturing Market Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 18: United States Additive Manufacturing Market Volume Billion Forecast, by End-user Vertical 2020 & 2033

- Table 19: United States Additive Manufacturing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 20: United States Additive Manufacturing Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Additive Manufacturing Market?

The projected CAGR is approximately 20.90%.

2. Which companies are prominent players in the United States Additive Manufacturing Market?

Key companies in the market include 3D Systems Corporation, General Electric Company (GE Additive), EnvisionTEC GmbH, Nikon SLM, Ricoh USA Inc, EOS GmbH, Exone Company, MCOR Technology Ltd, Materialise NV, Optomec Inc, Stratasys Ltd, SLM Solutions Group AG*List Not Exhaustive.

3. What are the main segments of the United States Additive Manufacturing Market?

The market segments include Component, Material, Technology, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.32 Million as of 2022.

5. What are some drivers contributing to market growth?

Customization. Personalization. Complex Geometries. and Design Freedom; Rapid Prototyping and Time to Market; Increasing Adoption of Industry 4.0 and Digital Transformation.

6. What are the notable trends driving market growth?

The Selective Laser Sintering Segment is Expected to Hold a Significant Share of the Market.

7. Are there any restraints impacting market growth?

Customization. Personalization. Complex Geometries. and Design Freedom; Rapid Prototyping and Time to Market; Increasing Adoption of Industry 4.0 and Digital Transformation.

8. Can you provide examples of recent developments in the market?

June 2024: Nikon SLM Solutions AG commenced the production of its NXG XII 600 metal Additive Manufacturing machine in the United States. The expansion of its manufacturing capabilities provides North American customers with a fully ‘American Made’ metal AM machine. The manufacturing unit has the ability to meet the increasing demand for its metal additive manufacturing solutions across key industries, including aerospace, defense, automotive, and energy.June 2024: Ricoh USA Inc. announced the launch of its fully managed on-site 3D printing solution, RICOH All-In 3D Print. Designed to streamline the production of 3D-printed product prototypes and other additive manufacturing uses, this complete XaaS solution for additive manufacturing includes necessary components, such as printing hardware, advanced 3D production software, specialized Ricoh labor, and essential supplies to propel businesses’ manufacturing capabilities forward with the power of rapid prototyping.April 2024: Meltio, a 3D printer manufacturer, and Accufacture, a Michigan-based industrial automation company, introduced the Alchemist 1, a new large-scale robotic DED 3D printing work cell made in the United States. Powered by Meltio’s laser metal deposition (LMD) 3D printing technology, Alchemist 1 is optimized for producing large-scale, fully dense metal parts. The robotic additive manufacturing work cell is also designed to be easily integrated into existing production lines.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Additive Manufacturing Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Additive Manufacturing Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Additive Manufacturing Market?

To stay informed about further developments, trends, and reports in the United States Additive Manufacturing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence