Key Insights

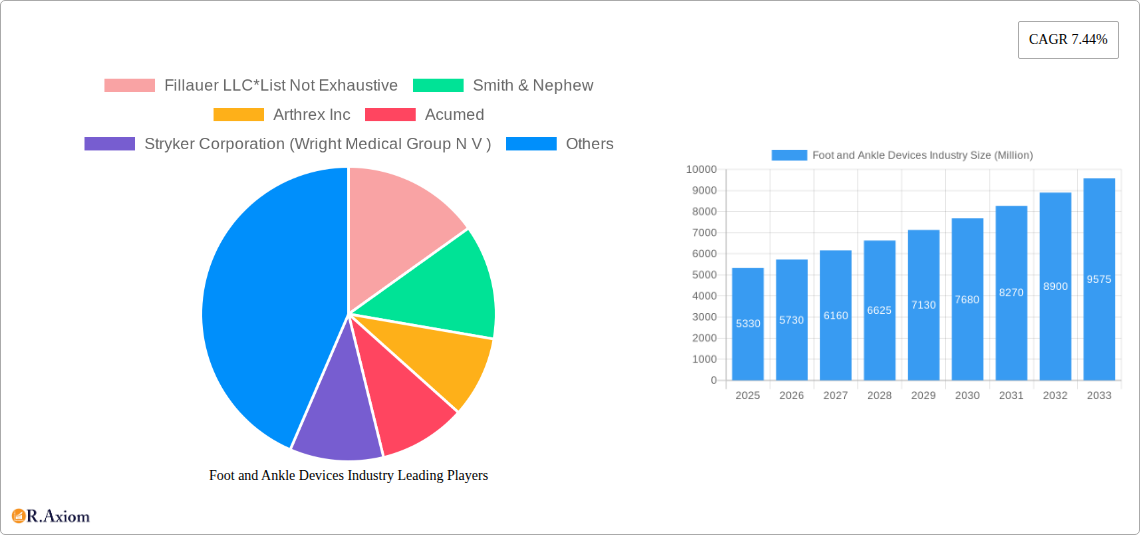

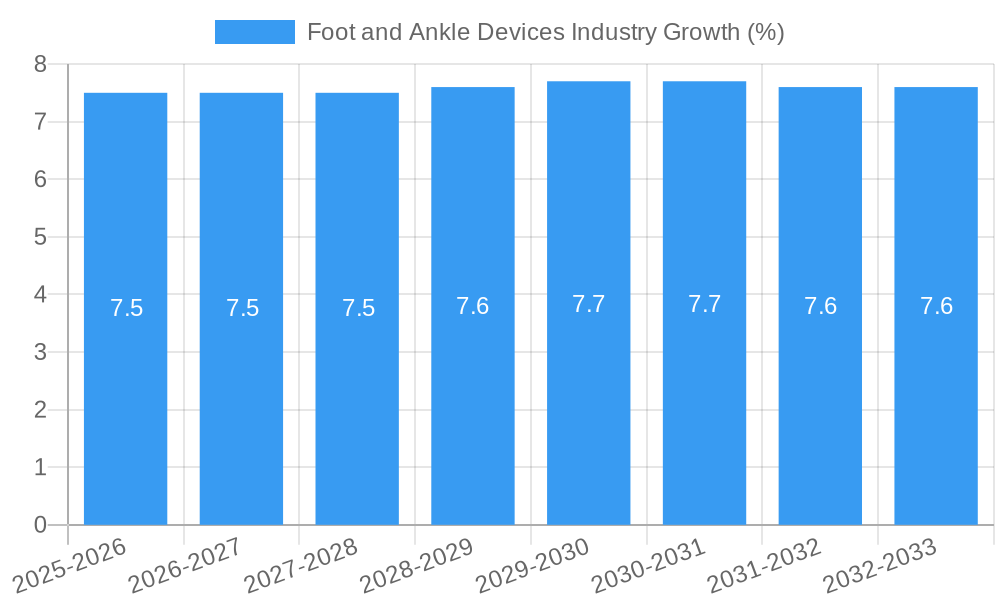

The global Foot and Ankle Devices Market is poised for substantial growth, projected to reach USD 4.65 billion with a robust Compound Annual Growth Rate (CAGR) of 7.44% during the study period of 2019-2033. This expansion is fueled by a confluence of factors, primarily driven by the increasing prevalence of foot and ankle disorders, such as osteoarthritis, diabetic foot complications, and sports-related injuries. An aging global population, coupled with a growing emphasis on active lifestyles and sports participation, further contributes to the demand for advanced orthopedic solutions. Technological advancements in implant design, materials science, and minimally invasive surgical techniques are revolutionizing treatment options, offering patients improved outcomes and faster recovery times. The market's segmentation reveals significant opportunities across various device types, with Ankle Replacement Devices and Biologics and Implants expected to witness particularly strong uptake due to the rising incidence of degenerative conditions and the demand for regenerative medicine.

The market dynamics are further shaped by key trends including the increasing adoption of patient-specific implants and personalized treatment approaches, alongside a growing focus on developing biodegradable and bioabsorbable materials for enhanced biocompatibility and reduced long-term complications. Minimally invasive surgical procedures are gaining traction, leading to reduced hospital stays and quicker rehabilitation, thereby bolstering the demand for specialized instruments and implants. While the market presents immense opportunities, certain restraints such as the high cost of advanced devices and procedures, coupled with reimbursement challenges in certain regions, could temper growth. However, the continuous innovation by leading companies like Stryker Corporation, Zimmer Biomet, and Smith & Nephew, alongside strategic collaborations and mergers, is expected to mitigate these challenges and drive market expansion. The Asia Pacific region, in particular, is anticipated to emerge as a significant growth engine, driven by increasing healthcare expenditure, rising awareness, and a growing patient pool.

Foot and Ankle Devices Industry Market Concentration & Innovation

The global foot and ankle devices market exhibits a moderate to high level of concentration, with several leading orthopedic companies dominating market share. Key players like Stryker Corporation (Wright Medical Group N V), Zimmer Biomet, Johnson & Johnson (DePuy Synthes), and Smith & Nephew hold significant positions, driven by their extensive product portfolios, robust R&D capabilities, and established distribution networks. Innovation is a critical market driver, fueling advancements in implant materials, surgical techniques, and minimally invasive solutions. Regulatory frameworks, particularly the FDA in the US and EMA in Europe, play a crucial role in shaping product development and market access, with stringent approval processes for new orthopedic implants and foot and ankle surgical devices. The threat of product substitutes is relatively low for definitive treatments like ankle replacement devices and fusion procedures, but emerging technologies such as advanced biologics and regenerative medicine may offer alternative pathways for certain conditions. End-user trends are increasingly focused on patient outcomes, faster recovery times, and improved quality of life, leading to a demand for less invasive and more personalized treatment options. Mergers and acquisitions (M&A) remain a significant strategy for market consolidation and portfolio expansion. For instance, the acquisition of Wright Medical by Stryker in 2020, valued at approximately $5.4 Billion, significantly reshaped the landscape. Other notable M&A activities contribute to the evolving competitive dynamics, with deal values in the hundreds of millions of dollars indicating strategic importance.

Foot and Ankle Devices Industry Trends & Insights

The foot and ankle devices market is poised for substantial growth, propelled by a confluence of factors including an aging global population, increasing prevalence of orthopedic disorders such as arthritis and diabetes-related foot complications, and a rising incidence of sports-related injuries. The compound annual growth rate (CAGR) for this sector is projected to be robust, estimated in the range of 6-8% over the forecast period. This upward trajectory is further amplified by advancements in medical technology, leading to the development of more sophisticated orthopedic implants, minimally invasive surgical tools, and biologic regenerative therapies. The growing awareness among patients and healthcare providers regarding the impact of foot and ankle conditions on overall mobility and quality of life is also a significant market penetration driver.

Technological disruptions are fundamentally reshaping surgical interventions. The adoption of robot-assisted surgery and advanced imaging techniques is improving surgical precision, reducing recovery times, and enhancing patient outcomes for procedures like fracture repair and osteotomy. Furthermore, the development of novel materials, such as bio-absorbable polymers and advanced alloys, is leading to the creation of orthopedic implants with improved biocompatibility and longevity.

Consumer preferences are increasingly leaning towards personalized treatment plans and less invasive procedures. Patients are actively seeking solutions that minimize pain, reduce hospital stays, and allow for a quicker return to their daily activities and sports. This demand is driving the innovation in external fixation devices and less invasive plate and screw fixation systems. The competitive landscape is characterized by intense R&D efforts and strategic collaborations. Companies are focusing on expanding their product portfolios to address a wider range of foot and ankle pathologies, from common deformities to complex trauma. The market penetration of advanced ankle replacement devices is steadily increasing as they offer a viable alternative to fusion for suitable candidates, thereby improving joint function and range of motion.

The interplay between these trends—demographic shifts, technological innovation, evolving patient expectations, and competitive pressures—creates a dynamic and growing market for foot and ankle devices. Healthcare systems worldwide are recognizing the economic and social burden of foot and ankle disorders, leading to increased investment in treatments and supportive technologies. This proactive approach, coupled with continuous innovation, ensures a promising outlook for the foot and ankle devices industry.

Dominant Markets & Segments in Foot and Ankle Devices Industry

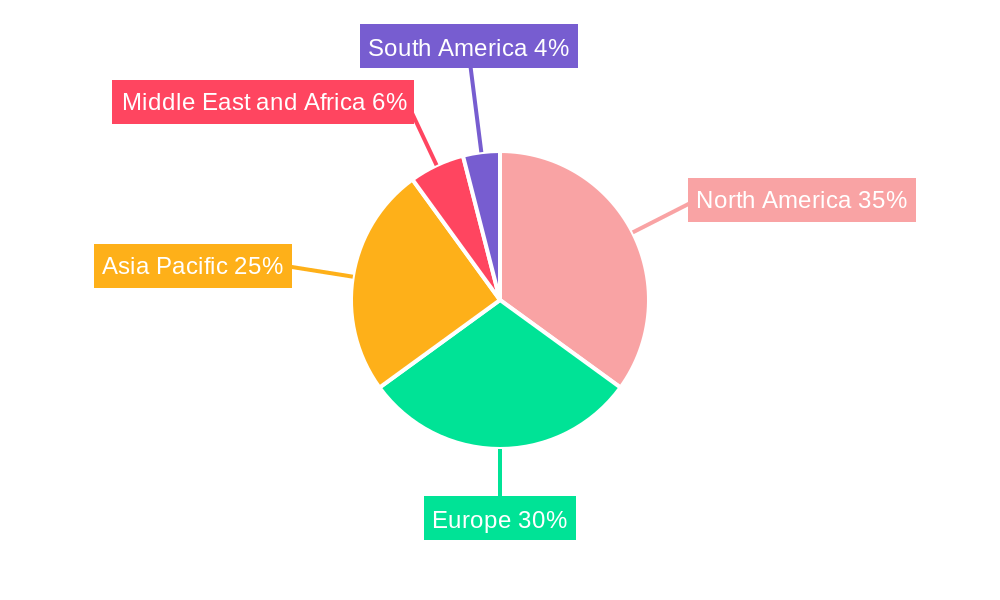

The foot and ankle devices market is experiencing significant growth across various geographical regions and product segments. North America, particularly the United States, stands out as the dominant region due to its advanced healthcare infrastructure, high disposable income, and a strong emphasis on technological adoption in medical treatments. The presence of major orthopedic companies, coupled with favorable reimbursement policies for advanced orthopedic implants and surgical procedures, further solidifies its leading position.

Within the Device Type segmentation, Plates, Screws, and Biologics and Implants constitute a substantial segment. This is driven by the high incidence of fractures, deformities, and degenerative conditions requiring surgical intervention. The demand for innovative and robust fracture repair solutions, including advanced plating systems and biocompatible screw designs, is continuously rising. Ankle Replacement Devices are also witnessing considerable traction as a therapeutic option for end-stage ankle arthritis, offering improved mobility and pain relief compared to fusion.

Regarding Procedure segmentation, Fracture Repair commands a significant market share. The prevalence of sports-related injuries, accidents, and age-related bone fragility contributes to a consistent demand for effective fracture management solutions. Fusion Procedures remain a cornerstone treatment for severe arthritis and deformities, especially when joint replacement is not feasible or desired. However, the market is also observing a growing preference for joint preservation techniques and motion-preserving implants.

Key drivers contributing to the dominance of specific segments include:

- Economic Policies: Favorable reimbursement policies from government and private insurers for surgical interventions and implantable devices in developed economies significantly boost market demand. For instance, Medicare and private insurance coverage for ankle replacement surgeries in the US directly impacts the sales of these devices.

- Infrastructure: The availability of sophisticated surgical centers, advanced diagnostic tools, and skilled orthopedic surgeons in leading regions like North America and Europe facilitates the adoption of cutting-edge foot and ankle surgical devices and techniques.

- Technological Advancements: Continuous innovation in biomaterials, surgical robotics, and implant design fuels the growth of specific segments. The development of titanium alloy orthopedic implants for trauma, as exemplified by Medline UNITE Foot & Ankle's offerings, enhances surgical outcomes and patient recovery.

- Disease Prevalence: The rising incidence of conditions like osteoarthritis, rheumatoid arthritis, diabetes-related foot complications, and sports injuries directly influences the demand for specific treatment modalities and associated orthopedic implants. The increasing aging population, susceptible to degenerative conditions, further propels the demand for ankle replacement devices and fusion procedures.

The Other De category within device types, encompassing a range of specialized instruments and implants for less common conditions, also contributes to the market's breadth, albeit with smaller individual shares. Similarly, Osteotomy and Other Procedures within the procedure segmentation represent important, albeit sometimes niche, areas of intervention driving the demand for specialized foot and ankle devices.

Foot and Ankle Devices Industry Product Developments

The foot and ankle devices market is characterized by rapid product innovation driven by the need for improved patient outcomes and surgeon efficiency. Recent developments include the launch of advanced external fixation devices and novel internal fixation systems. For instance, the Enovis Corporation's Enofix with Constrictor Technology (April 2023) represents a significant advancement in fracture repair, offering superior cyclic loading fixation. Similarly, Medline UNITE Foot & Ankle's introduction of a comprehensive titanium foot and ankle trauma system (April 2022) for ORIF surgeries signifies a move towards more complete and integrated trauma solutions. These innovations enhance the biomechanical stability of fixation, facilitate faster healing, and reduce the risk of complications. The focus is on developing orthopedic implants with enhanced biocompatibility, longevity, and minimally invasive application, providing surgeons with versatile tools to address a wide spectrum of foot and ankle pathologies.

Report Scope & Segmentation Analysis

This report meticulously analyzes the global Foot and Ankle Devices Industry. The market is segmented by Device Type, encompassing Ankle Replacement Devices, crucial for managing end-stage ankle arthritis; External Fixation Devices, vital for complex fracture management and limb reconstruction; Plates, Screws, and Biologics and Implants, the backbone of orthopedic trauma and reconstructive surgery; and Other Devices, including specialized instruments and consumables. By Procedure, the analysis covers Osteotomy, used for correcting bone deformities; Fracture Repair, addressing bone breaks; Fusion Procedures, for stabilizing painful or unstable joints; and Other Procedures, encompassing a variety of reconstructive and corrective interventions. Each segment is explored for its market size, growth projections, and competitive dynamics, providing detailed insights into their performance within the Foot and Ankle Devices Industry.

Key Drivers of Foot and Ankle Devices Industry Growth

The Foot and Ankle Devices Industry is propelled by several key growth drivers.

- Increasing Prevalence of Orthopedic Disorders: A rising incidence of conditions like osteoarthritis, rheumatoid arthritis, diabetes-related foot complications, and sports injuries directly fuels the demand for effective treatment solutions.

- Aging Global Population: As the world's population ages, the prevalence of degenerative joint diseases and age-related bone issues increases, leading to a higher demand for orthopedic implants and surgical interventions.

- Technological Advancements: Continuous innovation in orthopedic implants, surgical techniques, and biomaterials, such as the development of advanced ankle replacement devices and less invasive plate and screw fixation systems, drives market growth by offering improved patient outcomes and procedural efficiencies.

- Growing Healthcare Expenditure: Increased investment in healthcare infrastructure and a willingness to adopt advanced medical technologies in both developed and emerging economies support market expansion.

- Patient Awareness and Demand for Quality of Life: A greater understanding of foot and ankle conditions and a desire for improved mobility and pain relief encourage patients to seek surgical and non-surgical treatments.

Challenges in the Foot and Ankle Devices Industry Sector

Despite its growth, the Foot and Ankle Devices Industry faces several challenges.

- Stringent Regulatory Approvals: The rigorous and time-consuming approval processes for new orthopedic implants and surgical devices by regulatory bodies like the FDA can delay market entry and increase development costs.

- Reimbursement Policies: Complex and evolving reimbursement landscapes, particularly in certain healthcare systems, can impact the adoption rates of new and advanced foot and ankle surgical devices.

- High Cost of Advanced Devices: The premium pricing of cutting-edge orthopedic implants and technologies can pose a barrier to access, especially in price-sensitive markets.

- Limited Surgeon Training and Expertise: The adoption of novel surgical techniques and the use of specialized foot and ankle devices require adequate training for surgeons, which can be a bottleneck in certain regions.

- Competition and Market Saturation: Intense competition among established players and the emergence of new entrants can lead to pricing pressures and challenges in gaining significant market share for foot and ankle devices.

Emerging Opportunities in Foot and Ankle Devices Industry

The Foot and Ankle Devices Industry presents numerous emerging opportunities.

- Growth in Emerging Markets: The expanding healthcare infrastructure and increasing disposable incomes in Asia-Pacific, Latin America, and the Middle East offer significant untapped potential for foot and ankle devices.

- Advancements in Biologics and Regenerative Medicine: The development of novel biologic solutions for cartilage repair and bone regeneration presents an opportunity to offer less invasive and potentially more effective treatment options, complementing traditional orthopedic implants.

- Minimally Invasive Surgery (MIS): The increasing demand for MIS drives innovation in smaller, specialized instruments and implants for procedures like osteotomy and fracture repair, leading to faster recovery and reduced patient trauma.

- Personalized Medicine and Custom Implants: The trend towards patient-specific solutions, including custom-made orthopedic implants, tailored to individual anatomy, offers a niche but growing opportunity for advanced manufacturing and design capabilities.

- Digital Health Integration: The integration of digital technologies, such as AI-powered surgical planning tools and remote patient monitoring systems, can enhance surgical outcomes and improve the overall patient journey for foot and ankle treatments.

Leading Players in the Foot and Ankle Devices Industry Market

- Fillauer LLC

- Smith & Nephew

- Arthrex Inc

- Acumed

- Stryker Corporation (Wright Medical Group N V)

- Globus Medical Inc

- Orthofix US LLC

- Johnson & Johnson (DePuy Synthes)

- Zimmer Biomet

- Ortho Solutions UK Ltd

Key Developments in Foot and Ankle Devices Industry Industry

- April 2023: Enovis Corporation launched Enofix with Constrictor Technology, the latest addition to Enovis' growing suite of foot and ankle products. Enofix with Constrictor Technology is a repair system demonstrating superior fixation under cyclic loading.

- April 2022: The United States Food and Drug Administration approved the Calcaneal Fracture Plating System and IM Fibula Implant, which were launched by Medline UNITE Foot & Ankle. With the national release of these two devices, surgeons will have access to a complete titanium foot and ankle trauma system, allowing them to treat almost all fractures that call for ORIF with plate and screw fixation.

Strategic Outlook for Foot and Ankle Devices Industry Market

The strategic outlook for the Foot and Ankle Devices Industry is exceptionally positive, driven by a persistent rise in orthopedic conditions and an insatiable demand for enhanced mobility and pain relief. The increasing adoption of advanced orthopedic implants, particularly ankle replacement devices and innovative plate and screw fixation systems, will continue to fuel market expansion. Strategic focus on developing minimally invasive solutions and exploring the potential of biologics and regenerative medicine will be crucial for gaining a competitive edge. Furthermore, companies that successfully navigate the regulatory landscape, leverage technological advancements like robotics and AI, and expand their presence in high-growth emerging markets are poised for significant success. Collaborations, strategic partnerships, and targeted M&A activities will remain vital for portfolio enhancement and market consolidation, solidifying the industry's trajectory toward innovation and improved patient care in the coming years.

Foot and Ankle Devices Industry Segmentation

-

1. Device Type

- 1.1. Ankle Replacement Devices

- 1.2. External Fixation Devices

- 1.3. Plates

- 1.4. Screws

- 1.5. Biologics and Implants

- 1.6. Other De

-

2. Procedure

- 2.1. Osteotomy

- 2.2. Fracture Repair

- 2.3. Fusion Procedures

- 2.4. Other Procedures

Foot and Ankle Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Foot and Ankle Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.44% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Number of Sports Injuries and Road Accidents; Rising Incidences of Diabetes and Foot-related Disorders; Technological Advances in Foot and Ankle Surgeries

- 3.3. Market Restrains

- 3.3.1. Stringent Regulatory Guidelines; Huge Cost and Lack of Reimbursement for Devices

- 3.4. Market Trends

- 3.4.1. Fracture Repair Segment is Expected to Hold Significant Share in the Procedure Segment

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Ankle Replacement Devices

- 5.1.2. External Fixation Devices

- 5.1.3. Plates

- 5.1.4. Screws

- 5.1.5. Biologics and Implants

- 5.1.6. Other De

- 5.2. Market Analysis, Insights and Forecast - by Procedure

- 5.2.1. Osteotomy

- 5.2.2. Fracture Repair

- 5.2.3. Fusion Procedures

- 5.2.4. Other Procedures

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. North America Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. Ankle Replacement Devices

- 6.1.2. External Fixation Devices

- 6.1.3. Plates

- 6.1.4. Screws

- 6.1.5. Biologics and Implants

- 6.1.6. Other De

- 6.2. Market Analysis, Insights and Forecast - by Procedure

- 6.2.1. Osteotomy

- 6.2.2. Fracture Repair

- 6.2.3. Fusion Procedures

- 6.2.4. Other Procedures

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. Europe Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Device Type

- 7.1.1. Ankle Replacement Devices

- 7.1.2. External Fixation Devices

- 7.1.3. Plates

- 7.1.4. Screws

- 7.1.5. Biologics and Implants

- 7.1.6. Other De

- 7.2. Market Analysis, Insights and Forecast - by Procedure

- 7.2.1. Osteotomy

- 7.2.2. Fracture Repair

- 7.2.3. Fusion Procedures

- 7.2.4. Other Procedures

- 7.1. Market Analysis, Insights and Forecast - by Device Type

- 8. Asia Pacific Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Device Type

- 8.1.1. Ankle Replacement Devices

- 8.1.2. External Fixation Devices

- 8.1.3. Plates

- 8.1.4. Screws

- 8.1.5. Biologics and Implants

- 8.1.6. Other De

- 8.2. Market Analysis, Insights and Forecast - by Procedure

- 8.2.1. Osteotomy

- 8.2.2. Fracture Repair

- 8.2.3. Fusion Procedures

- 8.2.4. Other Procedures

- 8.1. Market Analysis, Insights and Forecast - by Device Type

- 9. Middle East and Africa Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Device Type

- 9.1.1. Ankle Replacement Devices

- 9.1.2. External Fixation Devices

- 9.1.3. Plates

- 9.1.4. Screws

- 9.1.5. Biologics and Implants

- 9.1.6. Other De

- 9.2. Market Analysis, Insights and Forecast - by Procedure

- 9.2.1. Osteotomy

- 9.2.2. Fracture Repair

- 9.2.3. Fusion Procedures

- 9.2.4. Other Procedures

- 9.1. Market Analysis, Insights and Forecast - by Device Type

- 10. South America Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Device Type

- 10.1.1. Ankle Replacement Devices

- 10.1.2. External Fixation Devices

- 10.1.3. Plates

- 10.1.4. Screws

- 10.1.5. Biologics and Implants

- 10.1.6. Other De

- 10.2. Market Analysis, Insights and Forecast - by Procedure

- 10.2.1. Osteotomy

- 10.2.2. Fracture Repair

- 10.2.3. Fusion Procedures

- 10.2.4. Other Procedures

- 10.1. Market Analysis, Insights and Forecast - by Device Type

- 11. North America Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 11.1.3 Mexico

- 12. Europe Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 Germany

- 12.1.2 United Kingdom

- 12.1.3 France

- 12.1.4 Italy

- 12.1.5 Spain

- 12.1.6 Rest of Europe

- 13. Asia Pacific Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Australia

- 13.1.5 South Korea

- 13.1.6 Rest of Asia Pacific

- 14. Middle East and Africa Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 GCC

- 14.1.2 South Africa

- 14.1.3 Rest of Middle East and Africa

- 15. South America Foot and Ankle Devices Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 Brazil

- 15.1.2 Argentina

- 15.1.3 Rest of South America

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Fillauer LLC*List Not Exhaustive

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Smith & Nephew

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Arthrex Inc

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Acumed

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Stryker Corporation (Wright Medical Group N V )

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Globus Medical Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Orthofix US LLC

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Johnson & Johnson (DePuy Synthes)

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Zimmer Biomet

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Ortho Solutions UK Ltd

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Fillauer LLC*List Not Exhaustive

List of Figures

- Figure 1: Global Foot and Ankle Devices Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Foot and Ankle Devices Industry Revenue (Million), by Device Type 2024 & 2032

- Figure 13: North America Foot and Ankle Devices Industry Revenue Share (%), by Device Type 2024 & 2032

- Figure 14: North America Foot and Ankle Devices Industry Revenue (Million), by Procedure 2024 & 2032

- Figure 15: North America Foot and Ankle Devices Industry Revenue Share (%), by Procedure 2024 & 2032

- Figure 16: North America Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Foot and Ankle Devices Industry Revenue (Million), by Device Type 2024 & 2032

- Figure 19: Europe Foot and Ankle Devices Industry Revenue Share (%), by Device Type 2024 & 2032

- Figure 20: Europe Foot and Ankle Devices Industry Revenue (Million), by Procedure 2024 & 2032

- Figure 21: Europe Foot and Ankle Devices Industry Revenue Share (%), by Procedure 2024 & 2032

- Figure 22: Europe Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Foot and Ankle Devices Industry Revenue (Million), by Device Type 2024 & 2032

- Figure 25: Asia Pacific Foot and Ankle Devices Industry Revenue Share (%), by Device Type 2024 & 2032

- Figure 26: Asia Pacific Foot and Ankle Devices Industry Revenue (Million), by Procedure 2024 & 2032

- Figure 27: Asia Pacific Foot and Ankle Devices Industry Revenue Share (%), by Procedure 2024 & 2032

- Figure 28: Asia Pacific Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa Foot and Ankle Devices Industry Revenue (Million), by Device Type 2024 & 2032

- Figure 31: Middle East and Africa Foot and Ankle Devices Industry Revenue Share (%), by Device Type 2024 & 2032

- Figure 32: Middle East and Africa Foot and Ankle Devices Industry Revenue (Million), by Procedure 2024 & 2032

- Figure 33: Middle East and Africa Foot and Ankle Devices Industry Revenue Share (%), by Procedure 2024 & 2032

- Figure 34: Middle East and Africa Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East and Africa Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: South America Foot and Ankle Devices Industry Revenue (Million), by Device Type 2024 & 2032

- Figure 37: South America Foot and Ankle Devices Industry Revenue Share (%), by Device Type 2024 & 2032

- Figure 38: South America Foot and Ankle Devices Industry Revenue (Million), by Procedure 2024 & 2032

- Figure 39: South America Foot and Ankle Devices Industry Revenue Share (%), by Procedure 2024 & 2032

- Figure 40: South America Foot and Ankle Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: South America Foot and Ankle Devices Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 3: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Procedure 2019 & 2032

- Table 4: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Germany Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: France Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Italy Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Spain Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Japan Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: India Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Australia Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: South Korea Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of Asia Pacific Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: GCC Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: South Africa Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Middle East and Africa Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Brazil Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Argentina Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of South America Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 32: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Procedure 2019 & 2032

- Table 33: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: United States Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Canada Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Mexico Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 38: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Procedure 2019 & 2032

- Table 39: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 40: Germany Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: United Kingdom Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: France Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Italy Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Spain Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: Rest of Europe Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 47: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Procedure 2019 & 2032

- Table 48: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 49: China Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Japan Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 51: India Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Australia Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 53: South Korea Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Rest of Asia Pacific Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 56: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Procedure 2019 & 2032

- Table 57: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: GCC Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 59: South Africa Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 60: Rest of Middle East and Africa Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 61: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 62: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Procedure 2019 & 2032

- Table 63: Global Foot and Ankle Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 64: Brazil Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 65: Argentina Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: Rest of South America Foot and Ankle Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Foot and Ankle Devices Industry?

The projected CAGR is approximately 7.44%.

2. Which companies are prominent players in the Foot and Ankle Devices Industry?

Key companies in the market include Fillauer LLC*List Not Exhaustive, Smith & Nephew, Arthrex Inc, Acumed, Stryker Corporation (Wright Medical Group N V ), Globus Medical Inc, Orthofix US LLC, Johnson & Johnson (DePuy Synthes), Zimmer Biomet, Ortho Solutions UK Ltd.

3. What are the main segments of the Foot and Ankle Devices Industry?

The market segments include Device Type, Procedure.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Number of Sports Injuries and Road Accidents; Rising Incidences of Diabetes and Foot-related Disorders; Technological Advances in Foot and Ankle Surgeries.

6. What are the notable trends driving market growth?

Fracture Repair Segment is Expected to Hold Significant Share in the Procedure Segment.

7. Are there any restraints impacting market growth?

Stringent Regulatory Guidelines; Huge Cost and Lack of Reimbursement for Devices.

8. Can you provide examples of recent developments in the market?

April 2023: Enovis Corporation launched Enofix with Constrictor Technology, the latest addition to Enovis' growing suite of foot and ankle products. Enofix with Constrictor Technology is a repair system demonstrating superior fixation under cyclic loading.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Foot and Ankle Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Foot and Ankle Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Foot and Ankle Devices Industry?

To stay informed about further developments, trends, and reports in the Foot and Ankle Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence