Key Insights

The North America Cardiac Assist Devices market is projected for substantial growth, driven by rising cardiovascular disease rates, an aging demographic, and significant advancements in heart failure treatment. Expected to reach $1.4 billion by 2025, the market will experience a Compound Annual Growth Rate (CAGR) of 5.8% through 2033. This expansion is attributed to the growing need for advanced therapies for end-stage heart failure. Ventricular Assist Devices (VADs), including LVADs and RVADs, are leading this trend, enhancing patient quality of life and survival. Intra-aortic Balloon Pumps (IABPs) remain vital for acute cardiac support, while Total Artificial Hearts (TAHs) offer a definitive solution for biventricular failure. The US, Canada, and Mexico form a key market, characterized by high healthcare spending and adoption of innovative cardiac solutions.

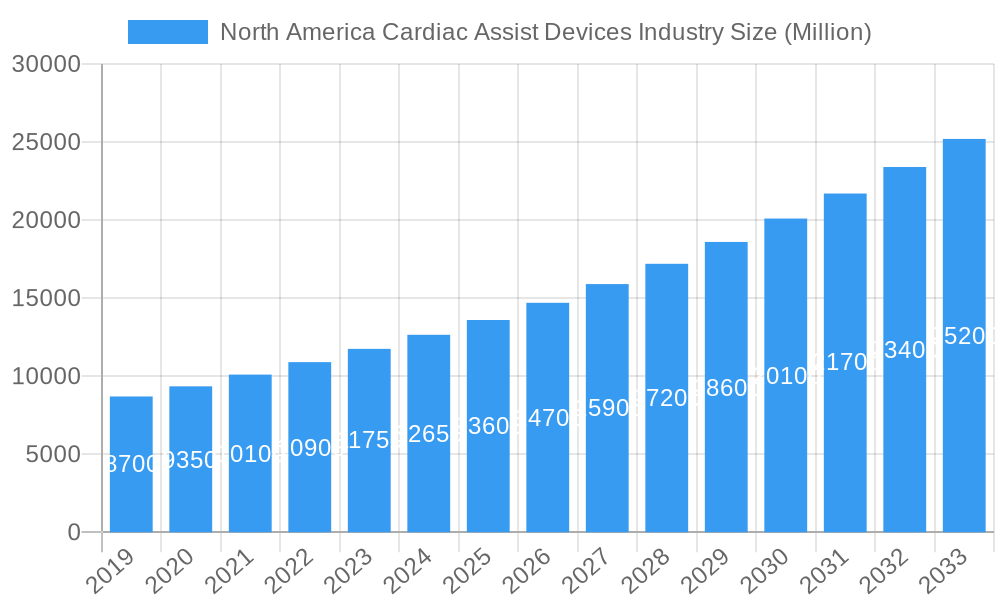

North America Cardiac Assist Devices Industry Market Size (In Billion)

Market growth faces challenges including high device and implantation costs, and the requirement for specialized surgical expertise and post-operative care. Inherent risks such as infection, bleeding, and stroke also necessitate careful patient selection and management. Nevertheless, ongoing research aims to develop smaller, more reliable, and cost-effective devices. Innovations in wireless power, anticoagulation, and biocompatible materials are being pursued to improve patient outcomes. Leading companies like Abiomed Inc., Abbott Laboratories, and Medtronic Plc are driving innovation through R&D and strategic alliances. The persistent demand for heart transplants further fuels the adoption of VADs as bridge-to-transplant therapy.

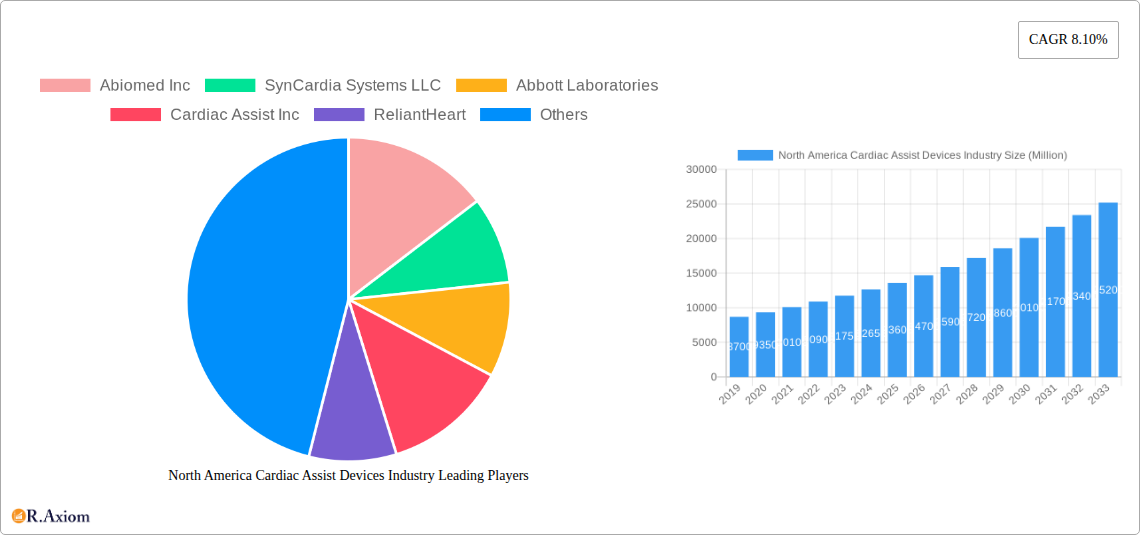

North America Cardiac Assist Devices Industry Company Market Share

North America Cardiac Assist Devices Industry Market Concentration & Innovation

The North America cardiac assist devices market exhibits moderate to high concentration, driven by a few dominant players and a landscape of specialized innovators. Key companies like Abiomed Inc., Abbott Laboratories, and Medtronic Plc hold significant market share, estimated at over 70% combined in 2025, due to their established product portfolios and extensive distribution networks. Innovation is the lifeblood of this sector, propelled by advancements in miniaturization, wireless technology, and bio-compatibility of devices. Companies are investing heavily in research and development, aiming to create less invasive, more durable, and patient-friendly solutions. For instance, the development of next-generation Ventricular Assist Devices (VADs) with improved battery life and reduced infection rates is a key area of focus. Regulatory frameworks, primarily governed by the U.S. Food and Drug Administration (FDA) and Health Canada, are stringent, emphasizing safety and efficacy, which acts as both a driver for robust product development and a barrier to entry for smaller firms. Product substitutes, such as advanced pharmacological treatments and heart transplantation, offer alternative solutions, but the growing demand for mechanical circulatory support, especially for end-stage heart failure patients, continues to drive the market for cardiac assist devices. End-user trends reveal a growing preference for implantable devices over external ones, and a focus on improving the quality of life for patients awaiting transplantation or as a destination therapy. Merger and acquisition (M&A) activity is present, with strategic acquisitions aimed at expanding product pipelines and market reach. For example, a potential acquisition in the Total Artificial Heart segment could reach a value of over $500 Million, indicating the strategic importance of consolidating capabilities in this niche.

North America Cardiac Assist Devices Industry Industry Trends & Insights

The North America cardiac assist devices industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033. This upward trajectory is underpinned by a confluence of factors, including the escalating prevalence of cardiovascular diseases, an aging population segment with a higher incidence of heart failure, and significant advancements in medical technology. The market penetration for advanced cardiac assist devices, particularly Ventricular Assist Devices (VADs), is steadily increasing as they become more reliable, accessible, and offer a viable alternative to heart transplantation. Technological disruptions are continuously reshaping the market. The development of smaller, more portable, and wirelessly rechargeable VADs is enhancing patient mobility and comfort, thereby improving their quality of life. Innovations in materials science are leading to more biocompatible and durable device components, reducing the risk of complications like thrombosis and infection. Furthermore, the integration of artificial intelligence (AI) and sophisticated monitoring systems is enabling personalized treatment strategies and proactive patient management. Consumer preferences are increasingly leaning towards less invasive procedures and devices that offer greater autonomy and a faster return to daily activities. Patients are actively seeking solutions that not only extend their lifespan but also improve their functional capacity. This shift is compelling manufacturers to prioritize user-friendly designs and comprehensive support systems. Competitive dynamics within the industry are intense, characterized by strategic partnerships, product development races, and a focus on market differentiation. Companies are investing in clinical trials and real-world evidence generation to validate the long-term efficacy and safety of their devices, thereby building trust with healthcare providers and patients. The expanding indications for cardiac assist devices, moving beyond bridge-to-transplant to destination therapy and bridge-to-candidacy, are further fueling market expansion. The increasing adoption of these devices in mid-stage heart failure patients, in addition to end-stage cases, represents a significant growth opportunity. The global economic landscape, while presenting occasional headwinds, generally supports increased healthcare spending, particularly in developed economies like the United States and Canada, which are the primary markets for cardiac assist devices. The demand for innovative cardiac assist devices is projected to reach an estimated market size of over $8 Billion by 2033.

Dominant Markets & Segments in North America Cardiac Assist Devices Industry

Within the North America cardiac assist devices industry, the United States stands as the overwhelmingly dominant market, accounting for an estimated 85% of the total regional market share in 2025. This dominance is attributed to a confluence of factors, including the highest prevalence of cardiovascular diseases, a well-established healthcare infrastructure, and substantial investment in medical research and development. Furthermore, the United States boasts the highest adoption rate for advanced cardiac assist devices, driven by a strong reimbursement landscape for these innovative technologies and a high density of specialized cardiac centers.

From a product segmentation perspective, Ventricular Assist Devices (VADs), particularly Left Ventricular Assist Devices (LVADs), currently hold the largest market share. This segment's leadership is propelled by several key drivers:

- Rising Incidence of Heart Failure: The increasing number of patients diagnosed with end-stage heart failure, especially ischemic cardiomyopathy and dilated cardiomyopathy, directly translates into a higher demand for LVADs as a life-saving therapy.

- Technological Advancements in LVADs: Continuous innovation in LVAD technology, including smaller pump sizes, improved durability, wireless power transmission, and enhanced anticoagulation profiles, has made them safer and more practical for long-term use. This has expanded their application from solely a bridge-to-transplant to destination therapy.

- Favorable Reimbursement Policies: In the United States, robust reimbursement policies from Medicare and private insurers cover the costs associated with LVAD implantation and long-term management, making these devices accessible to a broader patient population.

- Growing Awareness and Acceptance: Increased awareness among healthcare professionals and patients regarding the benefits of LVADs in improving survival rates and quality of life has fostered greater acceptance and adoption.

While LVADs currently lead, the Total Artificial Heart (TAH) segment, though smaller, is poised for significant growth.

- Addressing Donor Organ Shortage: TAHs offer a crucial alternative for patients who are not candidates for heart transplantation due to contraindications or prolonged waiting times for donor organs.

- Advancements in TAH Technology: Ongoing research and development are focused on making TAHs more compact, less prone to complications, and with improved biocompatibility, which will further drive their adoption.

Intra-aortic Balloon Pumps (IABPs), historically a cornerstone of cardiac support, continue to play a vital role, primarily as a temporary mechanical circulatory support device for acute conditions like cardiogenic shock.

- Established Clinical Efficacy: IABPs have a long-standing track record of efficacy in stabilizing hemodynamics in critically ill patients.

- Cost-Effectiveness for Short-Term Support: For short-term mechanical circulatory support, IABPs remain a cost-effective option.

However, the trend towards more permanent and advanced VADs for longer-term management is gradually influencing the market dynamics for IABPs.

Canada and Mexico represent growing markets within North America, with their respective shares estimated at around 10% and 5% in 2025.

- Canada: Benefits from a universal healthcare system that is increasingly recognizing the value of cardiac assist devices. Investment in advanced cardiac centers and growing awareness of VADs are key drivers.

- Mexico: Shows significant growth potential, driven by an increasing incidence of heart disease, a developing healthcare infrastructure, and a growing willingness to adopt advanced medical technologies, albeit with a more price-sensitive market.

North America Cardiac Assist Devices Industry Product Developments

Recent product developments in the North America cardiac assist devices industry are centered on enhancing patient mobility, reducing complications, and improving long-term device performance. Innovations in miniaturization have led to smaller, lighter devices, allowing for greater patient comfort and fewer restrictions on daily activities. Advancements in wireless power transfer and extended battery life are further minimizing external hardware and the risk of driveline infections, a significant concern with earlier generations of VADs. Furthermore, manufacturers are focusing on developing bio-compatible materials to reduce the incidence of blood clotting and immunological reactions. Smart monitoring capabilities, often integrated with mobile applications, are also becoming standard, enabling remote patient tracking and early detection of potential issues, thus improving patient outcomes and reducing hospital readmissions.

Report Scope & Segmentation Analysis

This report offers a comprehensive analysis of the North America cardiac assist devices industry, meticulously segmented by product type and geography.

Product Segmentation: The market is analyzed across Intra-aortic Balloon Pumps, Total Artificial Heart, and Ventricular Assist Devices (further segmented into Left Ventricular Assist Device and Right Ventricular Assist Device). Growth projections for each product segment are detailed, considering their specific applications and technological evolution. Market sizes for these segments in 2025 are estimated, along with competitive dynamics that define their respective market landscapes.

Geographical Segmentation: The analysis covers the North American region, with a detailed breakdown for the United States, Canada, and Mexico. This segmentation allows for an in-depth understanding of regional market nuances, including regulatory environments, healthcare spending patterns, and adoption rates of cardiac assist technologies. Growth projections and market sizes for each country are presented, alongside the competitive forces shaping their markets.

Key Drivers of North America Cardiac Assist Devices Industry Growth

The growth of the North America cardiac assist devices industry is primarily driven by the escalating prevalence of heart failure and cardiovascular diseases, particularly among the aging population. Significant technological advancements, such as miniaturization, wireless power, and improved biocompatibility of devices, are enhancing patient outcomes and quality of life. Favorable reimbursement policies in key markets like the United States are crucial, ensuring accessibility for a wider patient base. Furthermore, the increasing acceptance of cardiac assist devices as a viable treatment option, extending beyond bridge-to-transplant to destination therapy, is a substantial growth catalyst.

Challenges in the North America Cardiac Assist Devices Industry Sector

Despite robust growth, the North America cardiac assist devices industry faces several challenges. High device and implantation costs remain a significant barrier, impacting accessibility, especially in less affluent populations or regions with less comprehensive insurance coverage. Stringent regulatory approval processes for new devices, while ensuring safety, can lead to prolonged market entry timelines. Managing post-operative complications such as infection, thrombosis, and device malfunction requires intensive patient monitoring and healthcare resource allocation, adding to the overall cost of care. Moreover, the limited availability of trained healthcare professionals specializing in the implantation and management of these complex devices can also constrain market expansion.

Emerging Opportunities in North America Cardiac Assist Devices Industry

Emerging opportunities in the North America cardiac assist devices industry lie in expanding the application of these devices to earlier stages of heart failure, beyond end-stage treatment. The development of more compact, less invasive, and fully implantable VADs presents a significant avenue for growth. Advancements in artificial intelligence and remote patient monitoring offer opportunities to improve long-term device management, reduce complications, and enhance patient adherence. Furthermore, exploring new markets and increasing adoption in countries with growing healthcare expenditures and rising cardiovascular disease rates represents a substantial untapped potential. Collaboration with research institutions for novel technological integrations, such as advanced sensors and AI-driven diagnostics, also holds promise.

Leading Players in the North America Cardiac Assist Devices Industry Market

Abiomed Inc. SynCardia Systems LLC Abbott Laboratories Cardiac Assist Inc ReliantHeart Calon Cardio-Technology Ltd Bioheart Inc Medtronic Plc Cardiokinetix Inc LivaNova PLC (Cardiac Assist Inc )

Key Developments in North America Cardiac Assist Devices Industry Industry

- 2023/2024: Increased regulatory approvals for next-generation VADs with enhanced durability and reduced complication rates, leading to broader clinical adoption.

- 2023: Major manufacturers focusing on integrating advanced AI-powered monitoring systems into their VADs to enable predictive analytics for patient management.

- 2022/2023: Strategic partnerships formed between device manufacturers and leading cardiac research institutions to accelerate innovation in miniaturization and wireless power technology.

- 2022: LivaNova PLC completes the acquisition of TandemHeart, bolstering its portfolio in the VAD segment and expanding its market reach.

- 2021/2022: Growing emphasis on destination therapy indications for VADs, supported by positive long-term survival and quality-of-life data.

Strategic Outlook for North America Cardiac Assist Devices Industry Market

The strategic outlook for the North America cardiac assist devices industry is highly positive, driven by a sustained demand for advanced cardiac support solutions. Continued investment in research and development, focusing on miniaturization, wireless technology, and AI integration, will be paramount for market leaders to maintain their competitive edge. The expansion of VADs into earlier stages of heart failure and the increasing role of destination therapy will open up significant new patient populations. Furthermore, strategic collaborations and potential M&A activities are expected to shape the competitive landscape, consolidating expertise and market share. Addressing cost barriers and optimizing reimbursement strategies will be crucial for broader market penetration and ensuring equitable access to these life-saving technologies.

North America Cardiac Assist Devices Industry Segmentation

-

1. Product

- 1.1. Intra-aortic Balloon Pumps

- 1.2. Total Artificial Heart

-

1.3. Ventricular Assist Devices

- 1.3.1. Left Ventricular Assist Device

- 1.3.2. Right Ventricular Assist Device

-

2. Geography

-

2.1. North America

- 2.1.1. United States

- 2.1.2. Canada

- 2.1.3. Mexico

-

2.1. North America

North America Cardiac Assist Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

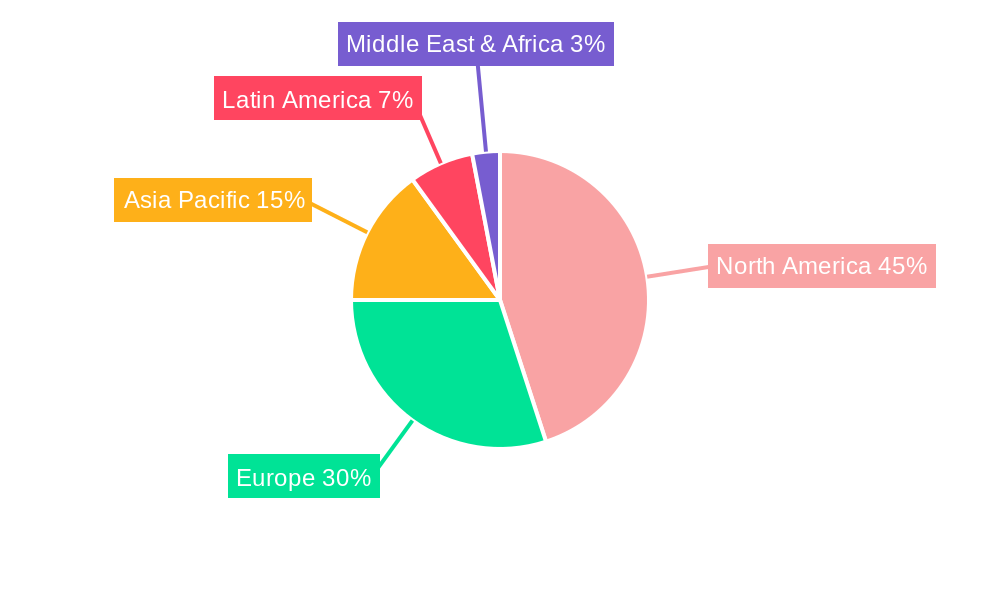

North America Cardiac Assist Devices Industry Regional Market Share

Geographic Coverage of North America Cardiac Assist Devices Industry

North America Cardiac Assist Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Intra-aortic Balloon Pumps

- 5.1.2. Total Artificial Heart

- 5.1.3. Ventricular Assist Devices

- 5.1.3.1. Left Ventricular Assist Device

- 5.1.3.2. Right Ventricular Assist Device

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. North America

- 5.2.1.1. United States

- 5.2.1.2. Canada

- 5.2.1.3. Mexico

- 5.2.1. North America

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Cardiac Assist Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Intra-aortic Balloon Pumps

- 6.1.2. Total Artificial Heart

- 6.1.3. Ventricular Assist Devices

- 6.1.3.1. Left Ventricular Assist Device

- 6.1.3.2. Right Ventricular Assist Device

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. North America

- 6.2.1.1. United States

- 6.2.1.2. Canada

- 6.2.1.3. Mexico

- 6.2.1. North America

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Abiomed Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 SynCardia Systems LLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Abbott Laboratories

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Cardiac Assist Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ReliantHeart

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Calon Cardio-Technology Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Bioheart Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Medtronic Plc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Cardiokinetix Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 LivaNova PLC (Cardiac Assist Inc )

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Abiomed Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Cardiac Assist Devices Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Cardiac Assist Devices Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Cardiac Assist Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: North America Cardiac Assist Devices Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 3: North America Cardiac Assist Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: North America Cardiac Assist Devices Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 5: North America Cardiac Assist Devices Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: North America Cardiac Assist Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States North America Cardiac Assist Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Cardiac Assist Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Cardiac Assist Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Cardiac Assist Devices Industry?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the North America Cardiac Assist Devices Industry?

Key companies in the market include Abiomed Inc, SynCardia Systems LLC, Abbott Laboratories, Cardiac Assist Inc, ReliantHeart, Calon Cardio-Technology Ltd, Bioheart Inc, Medtronic Plc, Cardiokinetix Inc, LivaNova PLC (Cardiac Assist Inc ).

3. What are the main segments of the North America Cardiac Assist Devices Industry?

The market segments include Product, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Heart Diseases; Advancements in Technology; Shortage of Heart Donors in Transplantation.

6. What are the notable trends driving market growth?

Total Artificial Hearts Segment Dominates the North American Cardiac Assist Devices Market.

7. Are there any restraints impacting market growth?

Risk Associated with Device Implantation.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Cardiac Assist Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Cardiac Assist Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Cardiac Assist Devices Industry?

To stay informed about further developments, trends, and reports in the North America Cardiac Assist Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence