Key Insights

The global handheld ultrasound device market is poised for substantial growth, projected to reach approximately USD 2.86 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.23%. This expansion is fueled by increasing demand for point-of-care diagnostics, growing adoption of portable medical devices, and advancements in miniaturization and imaging technology. The market is witnessing a significant shift towards mobile and handheld solutions, offering enhanced accessibility, reduced costs, and improved patient outcomes, particularly in resource-limited settings and emergency situations. Key applications driving this growth include gynecology, cardiovascular imaging, urology, and anesthesiology, where the convenience and immediate diagnostic capabilities of handheld devices are invaluable. Furthermore, the increasing prevalence of chronic diseases and the aging global population are creating sustained demand for advanced yet portable diagnostic tools.

The market landscape for handheld ultrasound devices is characterized by intense competition and continuous innovation. Companies are focusing on developing more intuitive interfaces, enhancing image quality, and integrating artificial intelligence (AI) for automated analysis and interpretation. While the market presents significant opportunities, certain factors like the high initial cost of advanced devices and the need for extensive training can act as restraints. However, the strong underlying drivers, including the push for decentralized healthcare services and the expanding scope of point-of-care ultrasound (POCUS) in diverse medical specialties, are expected to outweigh these challenges. The Asia Pacific region, particularly China and India, is anticipated to emerge as a rapidly growing market due to increasing healthcare expenditure, a rising patient base, and a burgeoning medical device manufacturing sector, further contributing to the overall positive market trajectory.

This in-depth report provides a definitive analysis of the global Handheld Ultrasound Devices Industry, offering a comprehensive overview of market dynamics, growth trajectories, and strategic imperatives. Covering the historical period from 2019 to 2024, the base year of 2025, and projecting growth through 2033, this study is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving landscape of portable diagnostic imaging. With an estimated market size of $3,500 million in 2025, the industry is poised for significant expansion driven by technological advancements, increasing healthcare accessibility, and a growing demand for point-of-care solutions.

Handheld Ultrasound Devices Industry Market Concentration & Innovation

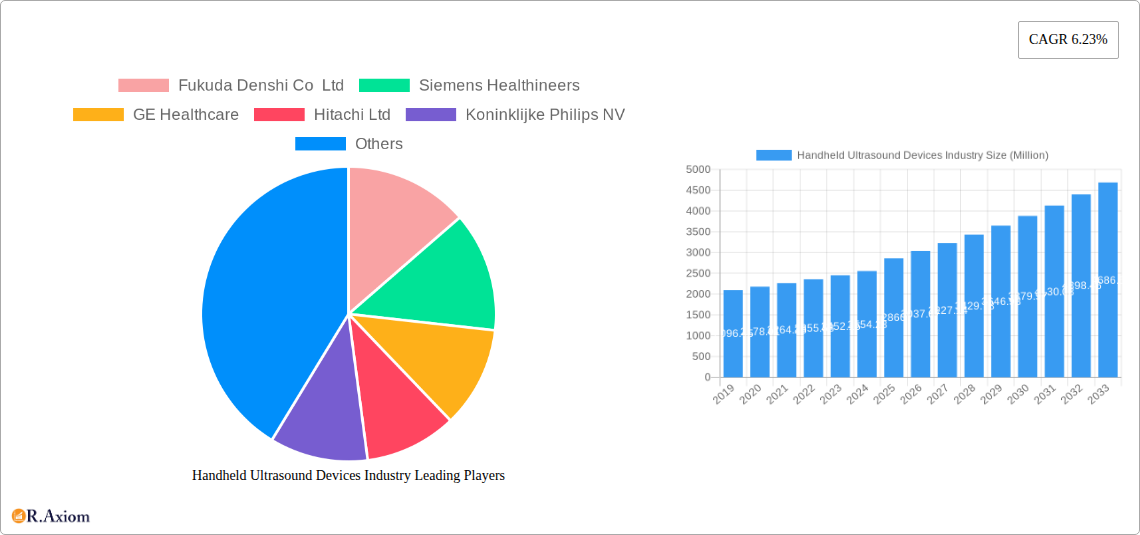

The Handheld Ultrasound Devices Industry exhibits a moderate to high level of market concentration, with key players like GE Healthcare, Siemens Healthineers, and Koninklijke Philips NV holding substantial market shares. In 2025, GE Healthcare is estimated to command a market share of approximately 22%, followed by Siemens Healthineers at 19%, and Koninklijke Philips NV at 17%. Innovation remains a critical differentiator, fueled by ongoing research and development in miniaturization, artificial intelligence integration, and enhanced imaging capabilities. Regulatory frameworks, such as FDA approvals and CE marking, play a crucial role in market entry and product validation, ensuring patient safety and efficacy. Product substitutes, while present in broader diagnostic imaging, are increasingly challenged by the portability and cost-effectiveness of handheld ultrasound. End-user trends highlight a growing preference for user-friendly interfaces and cloud-connectivity for seamless data management. Mergers and acquisitions (M&A) are expected to shape the competitive landscape, with an estimated total M&A deal value of $650 million anticipated between 2025 and 2033, aimed at consolidating market presence and acquiring innovative technologies.

Handheld Ultrasound Devices Industry Industry Trends & Insights

The global Handheld Ultrasound Devices Industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 8.5% from 2025 to 2033. This expansion is propelled by a confluence of factors, including the escalating demand for accessible and affordable diagnostic tools, particularly in emerging economies and remote healthcare settings. The increasing prevalence of chronic diseases and the aging global population further fuel the need for continuous patient monitoring and rapid bedside diagnostics. Technological disruptions are at the forefront of this evolution, with advancements in artificial intelligence (AI) and machine learning (ML) significantly enhancing diagnostic accuracy and workflow efficiency. AI-powered image analysis, for instance, assists clinicians in identifying subtle abnormalities, thereby reducing diagnostic errors and improving patient outcomes. The miniaturization of ultrasound technology has led to the development of highly portable and user-friendly handheld devices, making them ideal for point-of-care applications, emergency medicine, and home healthcare. Consumer preferences are shifting towards solutions that offer greater convenience, faster diagnostic turnaround times, and reduced healthcare costs without compromising on quality. Competitive dynamics are characterized by intense innovation, strategic partnerships, and market penetration efforts by established players and agile new entrants. Companies are increasingly focusing on developing specialized handheld ultrasound devices tailored for specific applications, such as gynecology, cardiovascular diagnostics, and musculoskeletal imaging. Market penetration is expected to rise significantly, reaching an estimated 45% in developed markets and 25% in developing regions by 2033, underscoring the growing adoption of this transformative technology across the healthcare spectrum. The integration of wireless connectivity and cloud-based data management solutions further enhances the utility and accessibility of handheld ultrasound devices, enabling remote consultations and collaborative diagnostics.

Dominant Markets & Segments in Handheld Ultrasound Devices Industry

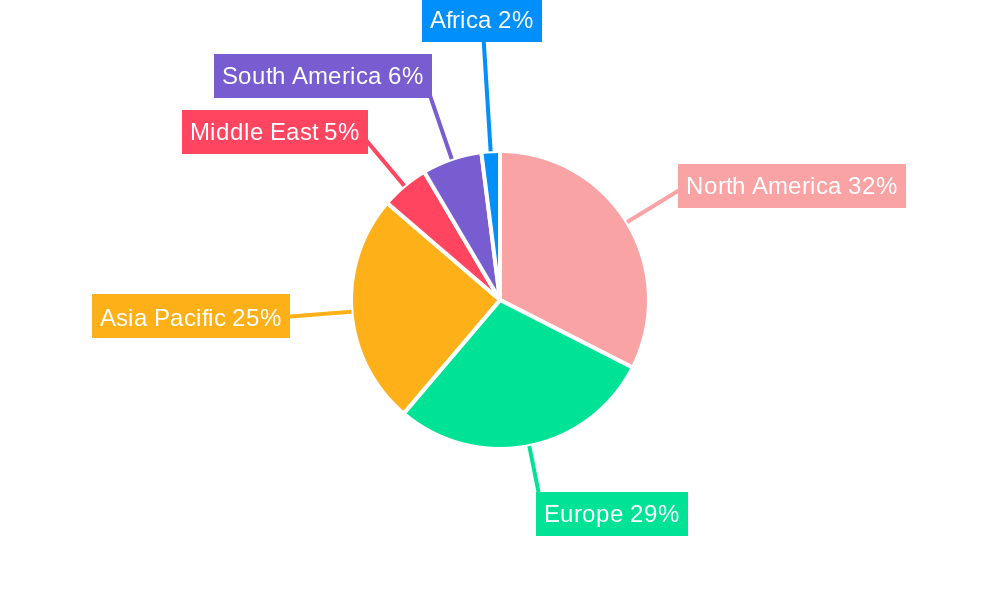

North America currently holds the dominant position in the Handheld Ultrasound Devices Industry, driven by factors such as high healthcare expenditure, advanced technological infrastructure, and a strong emphasis on early disease detection and preventive care. The United States, in particular, contributes significantly to this regional dominance due to the presence of leading healthcare providers, extensive research and development activities, and favorable reimbursement policies. Economic policies promoting healthcare innovation and infrastructure development further bolster market growth.

Within the device type segmentation, the Handheld Ultrasound Device segment is projected to exhibit the fastest growth, outpacing the Mobile Ultrasound Device segment. This is attributed to the increasing demand for ultra-portable, battery-operated devices that can be used seamlessly at the patient's bedside or in remote locations. The market size for Handheld Ultrasound Devices is estimated to reach $2,200 million in 2025, with a projected CAGR of 9.2% during the forecast period.

In terms of applications, the Cardiovascular segment currently dominates the market, accounting for an estimated market share of 28% in 2025, valued at $980 million. This dominance is fueled by the high global burden of cardiovascular diseases and the growing need for accessible and non-invasive diagnostic tools for cardiac assessment.

- Cardiovascular: Driven by the high prevalence of heart disease and the need for rapid bedside diagnostics, including echo, Doppler, and vascular assessments. Economic factors like insurance coverage for cardiac procedures and technological advancements in cardiac imaging software are key drivers.

- Gynecology: Increasing adoption for prenatal care, fertility assessments, and point-of-care gynecological examinations, especially in underserved areas. Government initiatives promoting maternal health contribute to growth.

- Musculoskeletal: Growing use in sports medicine, physical therapy, and orthopedics for diagnosing soft tissue injuries, joint effusions, and guiding procedures. Increased sports participation and the demand for non-invasive imaging solutions are key catalysts.

- Anesthesiology: Essential for guiding regional anesthesia, nerve blocks, and central venous access, enhancing patient safety and procedural success. The rising number of surgical procedures drives demand.

- Urology: Used for bladder volume assessment, prostate imaging, and guiding procedures. Increasing awareness and accessibility of point-of-care diagnostics are important.

- Others: Encompasses a broad range of applications including emergency medicine, critical care, point-of-care ultrasound (POCUS) training, and veterinary diagnostics, all contributing to the overall market expansion.

Handheld Ultrasound Devices Industry Product Developments

Product developments in the Handheld Ultrasound Devices Industry are characterized by a relentless pursuit of miniaturization, enhanced imaging quality, and AI-driven diagnostic assistance. Companies are introducing devices with superior resolution, deeper penetration, and advanced Doppler capabilities, enabling more accurate diagnoses across a wider range of applications. The integration of AI algorithms for automated measurements, image optimization, and anomaly detection is a significant trend, enhancing user-friendliness and diagnostic confidence. Competitive advantages stem from features like extended battery life, wireless connectivity, intuitive user interfaces, and specialized probes designed for specific clinical needs, such as superficial imaging or deep abdominal scans. The market fit is being solidified by devices that cater to the growing demand for point-of-care diagnostics in diverse settings, from emergency rooms to rural clinics.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Handheld Ultrasound Devices Industry across several key segments to provide granular insights.

- Type of Device: The market is segmented into Mobile Ultrasound Devices and Handheld Ultrasound Devices. The Handheld Ultrasound Device segment is projected to witness a higher CAGR due to its inherent portability and ease of use in various clinical scenarios. Market size for Handheld Ultrasound Devices is estimated at $2,200 million in 2025, with a projected CAGR of 9.2% during the forecast period. Mobile Ultrasound Devices, while established, are expected to grow at a steady pace.

- Application: The analysis encompasses Gynecology, Cardiovascular, Urology, Musculoskeletal, Anesthesiology, and Others. The Cardiovascular segment leads in market share, estimated at $980 million in 2025, with significant growth expected. Gynecology and Musculoskeletal segments are also poised for substantial expansion. The "Others" category includes a diverse range of applications in emergency medicine, critical care, and veterinary diagnostics, collectively contributing to market diversification.

Key Drivers of Handheld Ultrasound Devices Industry Growth

The growth of the Handheld Ultrasound Devices Industry is primarily driven by several key factors. Technologically, the miniaturization of ultrasound components, advancements in battery technology, and the integration of AI and machine learning for enhanced image analysis and diagnostic support are crucial enablers. Economically, increasing healthcare expenditure globally, particularly in emerging markets, coupled with a growing demand for cost-effective diagnostic solutions, is fueling adoption. Regulatory bodies are also playing a role by streamlining approval processes for innovative portable devices, thereby facilitating market access. The increasing prevalence of chronic diseases and the need for point-of-care diagnostics in emergency medicine and remote settings further amplify these growth drivers.

Challenges in the Handheld Ultrasound Devices Industry Sector

Despite its promising growth, the Handheld Ultrasound Devices Industry faces several challenges. High initial manufacturing costs for advanced portable devices can be a barrier to adoption, especially for smaller healthcare facilities or in resource-constrained regions. Stringent regulatory approval processes in certain geographies can lead to prolonged market entry timelines, hindering rapid product deployment. Intense competition among established players and emerging startups puts pressure on pricing and necessitates continuous innovation to maintain market share. Supply chain disruptions, as observed in recent global events, can impact the availability of critical components and affect production volumes. Furthermore, the need for comprehensive training for healthcare professionals to effectively utilize the advanced features of handheld ultrasound devices presents an ongoing challenge.

Emerging Opportunities in Handheld Ultrasound Devices Industry

The Handheld Ultrasound Devices Industry is ripe with emerging opportunities. The expansion of telehealth and remote patient monitoring presents a significant avenue for growth, as handheld ultrasound devices can be integrated into home healthcare setups for continuous monitoring and virtual consultations. The burgeoning field of veterinary medicine offers another untapped market, with increasing demand for portable diagnostic tools for animal care. Furthermore, the growing adoption of point-of-care ultrasound (POCUS) in medical education and training programs creates a sustained demand for user-friendly and accessible devices. Emerging economies with rapidly developing healthcare infrastructures and a growing middle class represent a vast untapped market, offering substantial growth potential for affordable and portable ultrasound solutions.

Leading Players in the Handheld Ultrasound Devices Industry Market

- Fukuda Denshi Co Ltd

- Siemens Healthineers

- GE Healthcare

- Hitachi Ltd

- Koninklijke Philips NV

- Fujifilm SonoSite Inc

- Canon Medical Systems Corporation

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Samsung Healthcare

Key Developments in Handheld Ultrasound Devices Industry Industry

- 2023/08: GE Healthcare launches a new generation of its portable ultrasound system, featuring enhanced AI capabilities for improved diagnostic accuracy.

- 2023/05: Koninklijke Philips NV announces strategic partnerships to expand the reach of its handheld ultrasound devices in underserved markets.

- 2022/11: Siemens Healthineers introduces a compact handheld ultrasound device optimized for point-of-care applications in emergency medicine.

- 2022/07: Fujifilm SonoSite Inc. expands its product portfolio with a new handheld ultrasound system designed for musculoskeletal imaging.

- 2021/12: Samsung Healthcare unveils an advanced handheld ultrasound device with enhanced connectivity features for seamless data integration.

Strategic Outlook for Handheld Ultrasound Devices Industry Market

The strategic outlook for the Handheld Ultrasound Devices Industry remains exceptionally positive, driven by sustained innovation and expanding market reach. Key growth catalysts include the continued integration of AI and machine learning to enhance diagnostic capabilities and user experience, further solidifying the role of these devices in precision medicine. The increasing demand for cost-effective and portable diagnostic solutions in emerging economies and remote healthcare settings presents a significant opportunity for market penetration. Strategic partnerships, collaborations for product development, and focused market entry strategies will be crucial for companies aiming to capitalize on these trends. The ongoing evolution of telehealth and remote patient monitoring will also create new avenues for growth, positioning handheld ultrasound as an integral component of future healthcare delivery models.

Handheld Ultrasound Devices Industry Segmentation

-

1. Type of Device

- 1.1. Mobile Ultrasound Device

- 1.2. Handheld Ultrasound Device

-

2. Application

- 2.1. Gynecology

- 2.2. Cardiovascular

- 2.3. Urology

- 2.4. Musculoskeletal

- 2.5. Anesthesiology

- 2.6. Others

Handheld Ultrasound Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

- 4. Middle East

-

5. GCC

- 5.1. South Africa

- 5.2. Rest of Middle East

-

6. South America

- 6.1. Brazil

- 6.2. Argentina

- 6.3. Rest of South America

Handheld Ultrasound Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

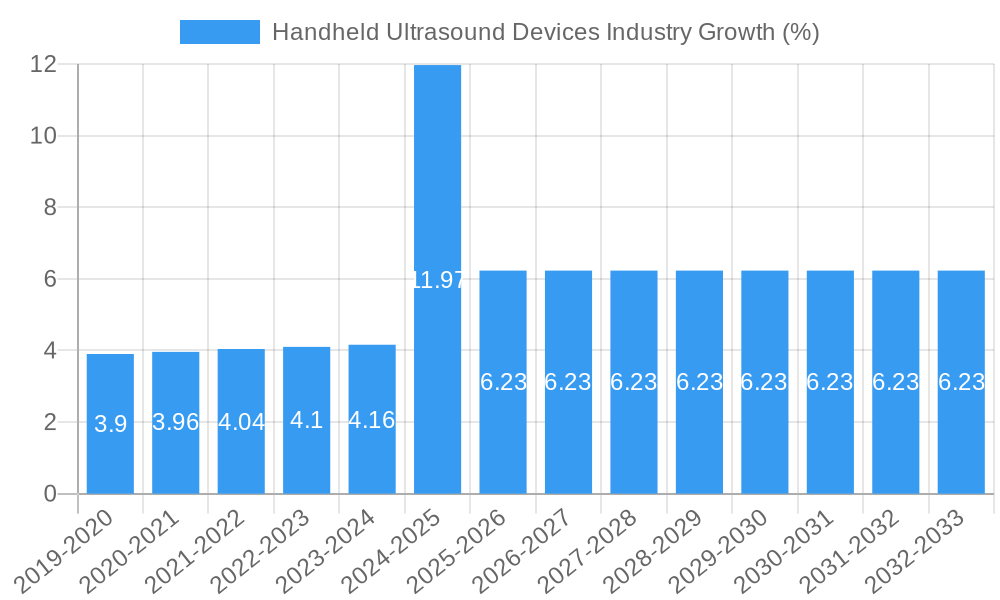

| Growth Rate | CAGR of 6.23% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Increasing Spectrum of Applications of Portable Ultrasound; Rising Advancements in Technology; Increasing Prevalence of Chronic Diseases

- 3.3. Market Restrains

- 3.3.1. ; High Cost of Portable Ultrasound Systems; Lack of Dedicated Training Programs by Companies

- 3.4. Market Trends

- 3.4.1. Mobile Ultrasound Devices is Expected to Grow with High CAGR Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type of Device

- 5.1.1. Mobile Ultrasound Device

- 5.1.2. Handheld Ultrasound Device

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Gynecology

- 5.2.2. Cardiovascular

- 5.2.3. Urology

- 5.2.4. Musculoskeletal

- 5.2.5. Anesthesiology

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East

- 5.3.5. GCC

- 5.3.6. South America

- 5.1. Market Analysis, Insights and Forecast - by Type of Device

- 6. North America Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type of Device

- 6.1.1. Mobile Ultrasound Device

- 6.1.2. Handheld Ultrasound Device

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Gynecology

- 6.2.2. Cardiovascular

- 6.2.3. Urology

- 6.2.4. Musculoskeletal

- 6.2.5. Anesthesiology

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Type of Device

- 7. Europe Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type of Device

- 7.1.1. Mobile Ultrasound Device

- 7.1.2. Handheld Ultrasound Device

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Gynecology

- 7.2.2. Cardiovascular

- 7.2.3. Urology

- 7.2.4. Musculoskeletal

- 7.2.5. Anesthesiology

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Type of Device

- 8. Asia Pacific Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type of Device

- 8.1.1. Mobile Ultrasound Device

- 8.1.2. Handheld Ultrasound Device

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Gynecology

- 8.2.2. Cardiovascular

- 8.2.3. Urology

- 8.2.4. Musculoskeletal

- 8.2.5. Anesthesiology

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Type of Device

- 9. Middle East Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type of Device

- 9.1.1. Mobile Ultrasound Device

- 9.1.2. Handheld Ultrasound Device

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Gynecology

- 9.2.2. Cardiovascular

- 9.2.3. Urology

- 9.2.4. Musculoskeletal

- 9.2.5. Anesthesiology

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Type of Device

- 10. GCC Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type of Device

- 10.1.1. Mobile Ultrasound Device

- 10.1.2. Handheld Ultrasound Device

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Gynecology

- 10.2.2. Cardiovascular

- 10.2.3. Urology

- 10.2.4. Musculoskeletal

- 10.2.5. Anesthesiology

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Type of Device

- 11. South America Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Type of Device

- 11.1.1. Mobile Ultrasound Device

- 11.1.2. Handheld Ultrasound Device

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Gynecology

- 11.2.2. Cardiovascular

- 11.2.3. Urology

- 11.2.4. Musculoskeletal

- 11.2.5. Anesthesiology

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Type of Device

- 12. North America Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 United States

- 12.1.2 Canada

- 12.1.3 Mexico

- 13. Europe Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 Germany

- 13.1.2 United Kingdom

- 13.1.3 France

- 13.1.4 Italy

- 13.1.5 Spain

- 13.1.6 Rest of Europe

- 14. Asia Pacific Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 China

- 14.1.2 Japan

- 14.1.3 India

- 14.1.4 Australia

- 14.1.5 South Korea

- 14.1.6 Rest of Asia Pacific

- 15. GCC Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1 South Africa

- 15.1.2 Rest of Middle East

- 16. South America Handheld Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1 Brazil

- 16.1.2 Argentina

- 16.1.3 Rest of South America

- 17. Competitive Analysis

- 17.1. Global Market Share Analysis 2024

- 17.2. Company Profiles

- 17.2.1 Fukuda Denshi Co Ltd

- 17.2.1.1. Overview

- 17.2.1.2. Products

- 17.2.1.3. SWOT Analysis

- 17.2.1.4. Recent Developments

- 17.2.1.5. Financials (Based on Availability)

- 17.2.2 Siemens Healthineers

- 17.2.2.1. Overview

- 17.2.2.2. Products

- 17.2.2.3. SWOT Analysis

- 17.2.2.4. Recent Developments

- 17.2.2.5. Financials (Based on Availability)

- 17.2.3 GE Healthcare

- 17.2.3.1. Overview

- 17.2.3.2. Products

- 17.2.3.3. SWOT Analysis

- 17.2.3.4. Recent Developments

- 17.2.3.5. Financials (Based on Availability)

- 17.2.4 Hitachi Ltd

- 17.2.4.1. Overview

- 17.2.4.2. Products

- 17.2.4.3. SWOT Analysis

- 17.2.4.4. Recent Developments

- 17.2.4.5. Financials (Based on Availability)

- 17.2.5 Koninklijke Philips NV

- 17.2.5.1. Overview

- 17.2.5.2. Products

- 17.2.5.3. SWOT Analysis

- 17.2.5.4. Recent Developments

- 17.2.5.5. Financials (Based on Availability)

- 17.2.6 Fujifilm SonoSite Inc

- 17.2.6.1. Overview

- 17.2.6.2. Products

- 17.2.6.3. SWOT Analysis

- 17.2.6.4. Recent Developments

- 17.2.6.5. Financials (Based on Availability)

- 17.2.7 Canon Medical Systems Corporation

- 17.2.7.1. Overview

- 17.2.7.2. Products

- 17.2.7.3. SWOT Analysis

- 17.2.7.4. Recent Developments

- 17.2.7.5. Financials (Based on Availability)

- 17.2.8 Shenzhen Mindray

- 17.2.8.1. Overview

- 17.2.8.2. Products

- 17.2.8.3. SWOT Analysis

- 17.2.8.4. Recent Developments

- 17.2.8.5. Financials (Based on Availability)

- 17.2.9 Samsung Healthcare

- 17.2.9.1. Overview

- 17.2.9.2. Products

- 17.2.9.3. SWOT Analysis

- 17.2.9.4. Recent Developments

- 17.2.9.5. Financials (Based on Availability)

- 17.2.1 Fukuda Denshi Co Ltd

List of Figures

- Figure 1: Global Handheld Ultrasound Devices Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Global Handheld Ultrasound Devices Industry Volume Breakdown (K Unit, %) by Region 2024 & 2032

- Figure 3: North America Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 4: North America Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 5: North America Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: North America Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 7: Europe Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 8: Europe Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 9: Europe Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Europe Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 11: Asia Pacific Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 12: Asia Pacific Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 13: Asia Pacific Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: Asia Pacific Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 15: GCC Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 16: GCC Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 17: GCC Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: GCC Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 19: South America Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 20: South America Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 21: South America Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 22: South America Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 23: North America Handheld Ultrasound Devices Industry Revenue (Million), by Type of Device 2024 & 2032

- Figure 24: North America Handheld Ultrasound Devices Industry Volume (K Unit), by Type of Device 2024 & 2032

- Figure 25: North America Handheld Ultrasound Devices Industry Revenue Share (%), by Type of Device 2024 & 2032

- Figure 26: North America Handheld Ultrasound Devices Industry Volume Share (%), by Type of Device 2024 & 2032

- Figure 27: North America Handheld Ultrasound Devices Industry Revenue (Million), by Application 2024 & 2032

- Figure 28: North America Handheld Ultrasound Devices Industry Volume (K Unit), by Application 2024 & 2032

- Figure 29: North America Handheld Ultrasound Devices Industry Revenue Share (%), by Application 2024 & 2032

- Figure 30: North America Handheld Ultrasound Devices Industry Volume Share (%), by Application 2024 & 2032

- Figure 31: North America Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 32: North America Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 33: North America Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 34: North America Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 35: Europe Handheld Ultrasound Devices Industry Revenue (Million), by Type of Device 2024 & 2032

- Figure 36: Europe Handheld Ultrasound Devices Industry Volume (K Unit), by Type of Device 2024 & 2032

- Figure 37: Europe Handheld Ultrasound Devices Industry Revenue Share (%), by Type of Device 2024 & 2032

- Figure 38: Europe Handheld Ultrasound Devices Industry Volume Share (%), by Type of Device 2024 & 2032

- Figure 39: Europe Handheld Ultrasound Devices Industry Revenue (Million), by Application 2024 & 2032

- Figure 40: Europe Handheld Ultrasound Devices Industry Volume (K Unit), by Application 2024 & 2032

- Figure 41: Europe Handheld Ultrasound Devices Industry Revenue Share (%), by Application 2024 & 2032

- Figure 42: Europe Handheld Ultrasound Devices Industry Volume Share (%), by Application 2024 & 2032

- Figure 43: Europe Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 44: Europe Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 45: Europe Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 46: Europe Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 47: Asia Pacific Handheld Ultrasound Devices Industry Revenue (Million), by Type of Device 2024 & 2032

- Figure 48: Asia Pacific Handheld Ultrasound Devices Industry Volume (K Unit), by Type of Device 2024 & 2032

- Figure 49: Asia Pacific Handheld Ultrasound Devices Industry Revenue Share (%), by Type of Device 2024 & 2032

- Figure 50: Asia Pacific Handheld Ultrasound Devices Industry Volume Share (%), by Type of Device 2024 & 2032

- Figure 51: Asia Pacific Handheld Ultrasound Devices Industry Revenue (Million), by Application 2024 & 2032

- Figure 52: Asia Pacific Handheld Ultrasound Devices Industry Volume (K Unit), by Application 2024 & 2032

- Figure 53: Asia Pacific Handheld Ultrasound Devices Industry Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Handheld Ultrasound Devices Industry Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 56: Asia Pacific Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 57: Asia Pacific Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 58: Asia Pacific Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 59: Middle East Handheld Ultrasound Devices Industry Revenue (Million), by Type of Device 2024 & 2032

- Figure 60: Middle East Handheld Ultrasound Devices Industry Volume (K Unit), by Type of Device 2024 & 2032

- Figure 61: Middle East Handheld Ultrasound Devices Industry Revenue Share (%), by Type of Device 2024 & 2032

- Figure 62: Middle East Handheld Ultrasound Devices Industry Volume Share (%), by Type of Device 2024 & 2032

- Figure 63: Middle East Handheld Ultrasound Devices Industry Revenue (Million), by Application 2024 & 2032

- Figure 64: Middle East Handheld Ultrasound Devices Industry Volume (K Unit), by Application 2024 & 2032

- Figure 65: Middle East Handheld Ultrasound Devices Industry Revenue Share (%), by Application 2024 & 2032

- Figure 66: Middle East Handheld Ultrasound Devices Industry Volume Share (%), by Application 2024 & 2032

- Figure 67: Middle East Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 68: Middle East Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 69: Middle East Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 70: Middle East Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 71: GCC Handheld Ultrasound Devices Industry Revenue (Million), by Type of Device 2024 & 2032

- Figure 72: GCC Handheld Ultrasound Devices Industry Volume (K Unit), by Type of Device 2024 & 2032

- Figure 73: GCC Handheld Ultrasound Devices Industry Revenue Share (%), by Type of Device 2024 & 2032

- Figure 74: GCC Handheld Ultrasound Devices Industry Volume Share (%), by Type of Device 2024 & 2032

- Figure 75: GCC Handheld Ultrasound Devices Industry Revenue (Million), by Application 2024 & 2032

- Figure 76: GCC Handheld Ultrasound Devices Industry Volume (K Unit), by Application 2024 & 2032

- Figure 77: GCC Handheld Ultrasound Devices Industry Revenue Share (%), by Application 2024 & 2032

- Figure 78: GCC Handheld Ultrasound Devices Industry Volume Share (%), by Application 2024 & 2032

- Figure 79: GCC Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 80: GCC Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 81: GCC Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 82: GCC Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

- Figure 83: South America Handheld Ultrasound Devices Industry Revenue (Million), by Type of Device 2024 & 2032

- Figure 84: South America Handheld Ultrasound Devices Industry Volume (K Unit), by Type of Device 2024 & 2032

- Figure 85: South America Handheld Ultrasound Devices Industry Revenue Share (%), by Type of Device 2024 & 2032

- Figure 86: South America Handheld Ultrasound Devices Industry Volume Share (%), by Type of Device 2024 & 2032

- Figure 87: South America Handheld Ultrasound Devices Industry Revenue (Million), by Application 2024 & 2032

- Figure 88: South America Handheld Ultrasound Devices Industry Volume (K Unit), by Application 2024 & 2032

- Figure 89: South America Handheld Ultrasound Devices Industry Revenue Share (%), by Application 2024 & 2032

- Figure 90: South America Handheld Ultrasound Devices Industry Volume Share (%), by Application 2024 & 2032

- Figure 91: South America Handheld Ultrasound Devices Industry Revenue (Million), by Country 2024 & 2032

- Figure 92: South America Handheld Ultrasound Devices Industry Volume (K Unit), by Country 2024 & 2032

- Figure 93: South America Handheld Ultrasound Devices Industry Revenue Share (%), by Country 2024 & 2032

- Figure 94: South America Handheld Ultrasound Devices Industry Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Type of Device 2019 & 2032

- Table 4: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Type of Device 2019 & 2032

- Table 5: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 6: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 7: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: United States Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United States Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 13: Canada Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: Mexico Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Mexico Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 19: Germany Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Germany Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: United Kingdom Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: United Kingdom Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: France Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: France Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 25: Italy Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Italy Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 27: Spain Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Spain Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 29: Rest of Europe Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of Europe Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 31: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 33: China Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: China Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 35: Japan Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Japan Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 37: India Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: India Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 39: Australia Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Australia Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 41: South Korea Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: South Korea Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 43: Rest of Asia Pacific Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Rest of Asia Pacific Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 45: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 46: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 47: South Africa Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: South Africa Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 49: Rest of Middle East Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Rest of Middle East Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 51: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 52: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 53: Brazil Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Brazil Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 55: Argentina Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: Argentina Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 57: Rest of South America Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: Rest of South America Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 59: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Type of Device 2019 & 2032

- Table 60: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Type of Device 2019 & 2032

- Table 61: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 62: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 63: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 64: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 65: United States Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 66: United States Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 67: Canada Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 68: Canada Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 69: Mexico Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 70: Mexico Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 71: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Type of Device 2019 & 2032

- Table 72: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Type of Device 2019 & 2032

- Table 73: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 74: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 75: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 76: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 77: Germany Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 78: Germany Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 79: United Kingdom Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 80: United Kingdom Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 81: France Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 82: France Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 83: Italy Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 84: Italy Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 85: Spain Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 86: Spain Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 87: Rest of Europe Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 88: Rest of Europe Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 89: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Type of Device 2019 & 2032

- Table 90: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Type of Device 2019 & 2032

- Table 91: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 92: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 93: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 94: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 95: China Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 96: China Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 97: Japan Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 98: Japan Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 99: India Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 100: India Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 101: Australia Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 102: Australia Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 103: South Korea Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 104: South Korea Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 105: Rest of Asia Pacific Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 106: Rest of Asia Pacific Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 107: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Type of Device 2019 & 2032

- Table 108: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Type of Device 2019 & 2032

- Table 109: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 110: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 111: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 112: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 113: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Type of Device 2019 & 2032

- Table 114: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Type of Device 2019 & 2032

- Table 115: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 116: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 117: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 118: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 119: South Africa Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 120: South Africa Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 121: Rest of Middle East Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 122: Rest of Middle East Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 123: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Type of Device 2019 & 2032

- Table 124: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Type of Device 2019 & 2032

- Table 125: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 126: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 127: Global Handheld Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 128: Global Handheld Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 129: Brazil Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 130: Brazil Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 131: Argentina Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 132: Argentina Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 133: Rest of South America Handheld Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 134: Rest of South America Handheld Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Handheld Ultrasound Devices Industry?

The projected CAGR is approximately 6.23%.

2. Which companies are prominent players in the Handheld Ultrasound Devices Industry?

Key companies in the market include Fukuda Denshi Co Ltd, Siemens Healthineers, GE Healthcare, Hitachi Ltd, Koninklijke Philips NV, Fujifilm SonoSite Inc, Canon Medical Systems Corporation, Shenzhen Mindray, Samsung Healthcare.

3. What are the main segments of the Handheld Ultrasound Devices Industry?

The market segments include Type of Device, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.86 Million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Spectrum of Applications of Portable Ultrasound; Rising Advancements in Technology; Increasing Prevalence of Chronic Diseases.

6. What are the notable trends driving market growth?

Mobile Ultrasound Devices is Expected to Grow with High CAGR Over the Forecast Period.

7. Are there any restraints impacting market growth?

; High Cost of Portable Ultrasound Systems; Lack of Dedicated Training Programs by Companies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Handheld Ultrasound Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Handheld Ultrasound Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Handheld Ultrasound Devices Industry?

To stay informed about further developments, trends, and reports in the Handheld Ultrasound Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence