Key Insights

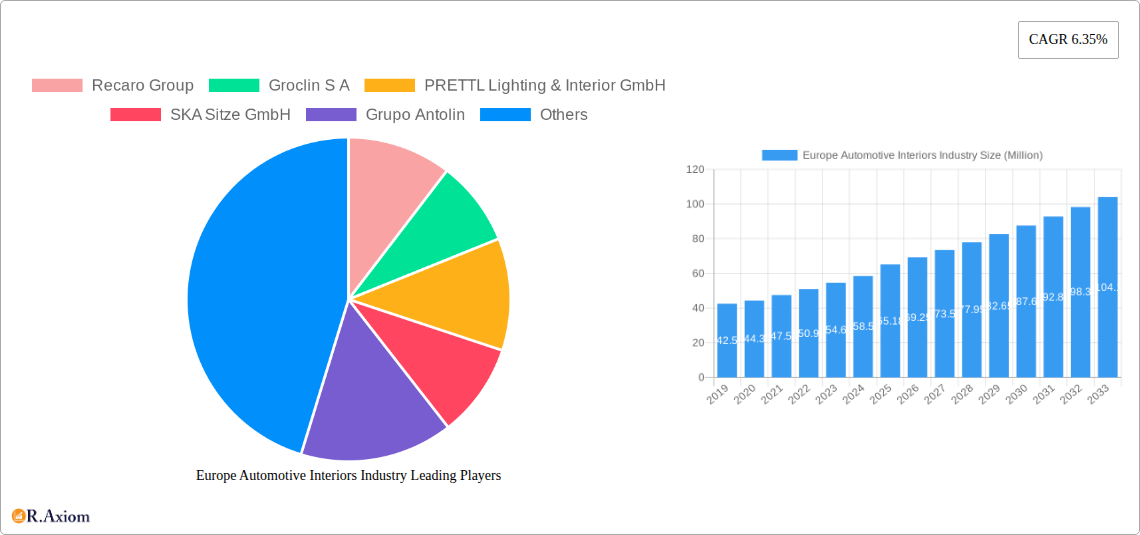

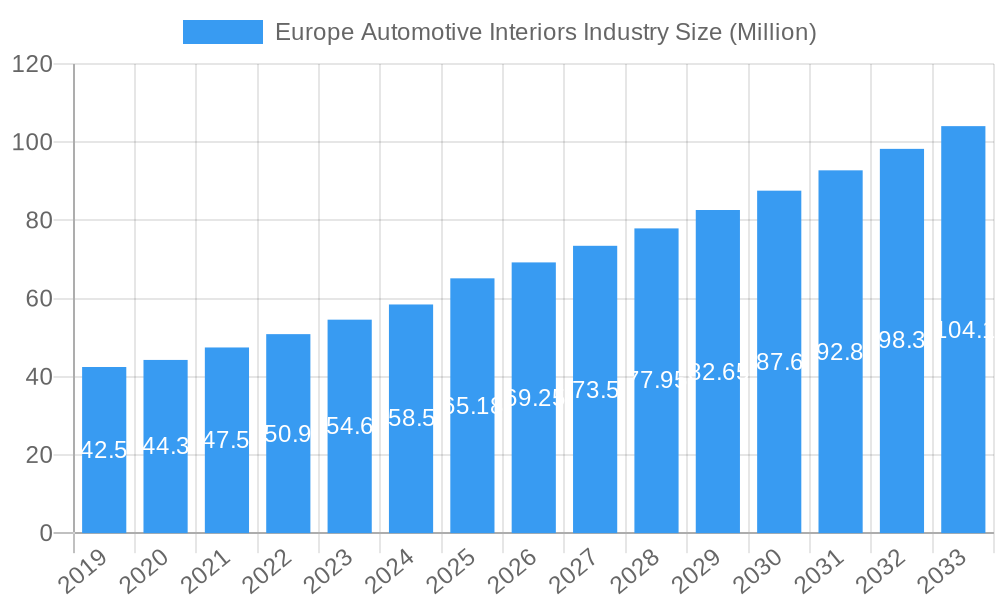

The European automotive interiors market is poised for robust expansion, projected to reach an estimated USD 65.18 billion by 2025, driven by a significant Compound Annual Growth Rate (CAGR) of 6.35%. This growth is largely fueled by evolving consumer demand for enhanced in-vehicle experiences, encompassing advanced infotainment systems, personalized interior lighting, and sophisticated instrument panels. The increasing integration of smart technologies and the consumer's desire for premium comfort and connectivity are paramount drivers. Furthermore, the burgeoning trend towards sustainable and lightweight materials in automotive components, including body panels and interior trims, is shaping manufacturing processes and product development. This focus on sustainability not only addresses environmental concerns but also contributes to improved fuel efficiency, a key consideration in the current automotive landscape. The shift towards electric vehicles (EVs) is also a substantial catalyst, as EV interiors often feature innovative designs and advanced technological integrations to cater to a new generation of drivers.

Europe Automotive Interiors Industry Market Size (In Million)

The market's expansion will be further propelled by advancements in seating technologies, with companies like Recaro Group and Adient PLC investing in ergonomic and feature-rich solutions. The development of advanced instrument clusters and integrated infotainment systems by players such as Faurecia and PRETTL Lighting & Interior GmbH will also play a crucial role. While the market benefits from these strong drivers, it also faces certain restraints. Increasing raw material costs and supply chain complexities, particularly in light of global geopolitical factors, could impact profit margins and production timelines. Additionally, the high cost of R&D for cutting-edge technologies might pose a challenge for smaller market players. Despite these hurdles, the dominant segments of passenger cars and commercial vehicles are expected to continue their upward trajectory, supported by innovation in component types like infotainment systems, instrument panels, and interior lighting. Europe, with its strong automotive manufacturing base and advanced consumer preferences, is a pivotal region for this market's development.

Europe Automotive Interiors Industry Company Market Share

Europe Automotive Interiors Industry Market Report: Comprehensive Analysis and Future Outlook (2019–2033)

This in-depth report provides a detailed analysis of the Europe automotive interiors market, encompassing a comprehensive study period from 2019 to 2033, with a base year of 2025. It delves into market dynamics, key trends, dominant segments, product innovations, growth drivers, challenges, emerging opportunities, and leading players. The report offers actionable insights for stakeholders navigating the evolving landscape of automotive interior components, from infotainment systems and instrument panels to lighting and body panels, across passenger cars and commercial vehicles.

Europe Automotive Interiors Industry Market Concentration & Innovation

The Europe automotive interiors market exhibits a moderate level of concentration, with several key players driving innovation and shaping market dynamics. The competitive landscape is characterized by a mix of established global suppliers and specialized regional manufacturers. Innovation is primarily driven by the relentless pursuit of enhanced occupant experience, safety, and sustainability. Key innovation drivers include advancements in materials science for lighter and more durable components, the integration of smart technologies for connected and autonomous vehicles, and the development of eco-friendly and recyclable materials. Regulatory frameworks, such as stringent emissions standards and safety regulations, also play a crucial role in shaping product development and mandating the adoption of innovative solutions. The increasing focus on electric vehicles (EVs) presents a significant opportunity for interior innovation, demanding new designs and functionalities to accommodate battery integration and optimize cabin space. While mergers and acquisitions (M&A) are present, they are often strategic, focusing on acquiring specific technological capabilities or expanding market reach. The market share distribution among the top players is dynamic, with continuous efforts to gain an edge through technological superiority and cost-effectiveness.

- Innovation Drivers:

- Smart materials for weight reduction and improved aesthetics.

- Integration of advanced driver-assistance systems (ADAS) and human-machine interfaces (HMI).

- Development of sustainable and bio-based interior materials.

- Personalization and modular interior designs.

- Noise, Vibration, and Harshness (NVH) reduction technologies.

Europe Automotive Interiors Industry Industry Trends & Insights

The Europe automotive interiors market is poised for robust growth, propelled by several interconnected trends and insights. The increasing demand for premium features, enhanced comfort, and personalized experiences within vehicles is a significant market growth driver. As consumer expectations rise, automakers are investing heavily in sophisticated interior solutions, including advanced infotainment systems, ambient lighting, and ergonomic seating. The rapid acceleration of electric vehicle adoption is fundamentally reshaping interior design. EVs necessitate unique interior configurations to optimize cabin space and integrate new technologies. This shift is driving demand for lightweight materials, advanced battery thermal management solutions integrated into the cabin, and innovative dashboard designs to accommodate larger displays and virtual cockpits. Furthermore, the growing emphasis on sustainability is influencing material selection, with a surge in demand for recycled plastics, bio-based composites, and vegan leather alternatives. The integration of digitalization and connectivity is another pivotal trend. In-vehicle infotainment systems are becoming more sophisticated, offering seamless smartphone integration, personalized user experiences, and access to a wider array of digital services. This digital transformation is also fostering the development of smart surfaces and haptic feedback systems. The competitive dynamics within the industry are intensifying, with suppliers focusing on differentiation through technological innovation, strategic partnerships, and the ability to offer integrated interior solutions. The market penetration of advanced interior technologies is steadily increasing across various vehicle segments, driven by both consumer demand and OEM mandates. The projected Compound Annual Growth Rate (CAGR) for the European automotive interiors market is expected to be substantial, reflecting these positive industry dynamics.

Dominant Markets & Segments in Europe Automotive Interiors Industry

The passenger car segment overwhelmingly dominates the Europe automotive interiors market. This is primarily driven by the sheer volume of passenger vehicle production and sales across the continent, coupled with a higher propensity among consumers of passenger cars to demand advanced and premium interior features. Within the passenger car segment, the demand for sophisticated infotainment systems and advanced instrument panels is particularly high, reflecting the increasing consumer focus on connectivity, entertainment, and driver information.

- Key Drivers of Passenger Car Dominance:

- High production volumes and consumer demand for personal mobility.

- Strong preference for advanced technology and comfort features.

- Growth in the premium and luxury vehicle segments.

- Increasing adoption of electric and hybrid passenger vehicles, necessitating new interior designs and functionalities.

While the commercial vehicle segment is smaller in comparison, it is experiencing steady growth, particularly in areas related to fleet management, driver comfort, and safety. The demand for durable and functional interiors that can withstand rigorous use is paramount in this segment. Innovations in driver ergonomics and advanced telematics are gaining traction to improve driver efficiency and well-being.

- Key Drivers of Commercial Vehicle Growth:

- Increased focus on driver comfort and productivity in long-haul operations.

- Integration of advanced safety systems and driver monitoring.

- Demand for durable and easy-to-clean interior materials.

- Growth in logistics and e-commerce, driving commercial vehicle sales.

From a component perspective, Infotainment Systems represent a high-growth segment. The integration of advanced displays, voice control, and seamless connectivity is no longer a luxury but a necessity for modern vehicles, driving significant investment in this area. The development of AI-powered assistants and personalized user interfaces is further fueling this trend.

- Drivers of Infotainment Systems Dominance:

- Consumer demand for connectivity and advanced entertainment options.

- Integration with ADAS features and vehicle diagnostics.

- Evolution of in-car digital services and over-the-air (OTA) updates.

Instrument Panels are also a crucial and evolving segment. The shift towards digital cockpits, customizable displays, and minimalist designs is transforming the traditional instrument panel into a dynamic interface. The integration of haptic feedback and augmented reality displays are emerging trends.

- Drivers of Instrument Panel Dominance:

- Transition to digital cockpits and virtual displays.

- Demand for integrated vehicle information and control.

- Aesthetic considerations and premium interior design.

Interior Lighting is witnessing a renaissance with the rise of ambient lighting and customizable color schemes. This segment plays a vital role in enhancing the cabin ambiance and improving the user experience, particularly in premium vehicles.

- Drivers of Interior Lighting Dominance:

- Enhancement of cabin aesthetics and mood.

- Integration with driver assistance and safety alerts.

- Growing trend of personalization in vehicle interiors.

Body Panels within the interior context, such as door panels and trims, are seeing innovation in terms of material sustainability, acoustic properties, and integrated functionalities like smart storage solutions and charging ports.

- Drivers of Body Panel Innovations:

- Use of lightweight and sustainable materials.

- Improved acoustic insulation for enhanced NVH performance.

- Integration of convenience features and design elements.

Other Component Types, encompassing a broad range of elements like seating systems, headliners, and floor mats, are also experiencing evolution driven by comfort, ergonomics, and sustainability. Advanced seat designs with enhanced adjustability, heating, cooling, and massage functions are becoming increasingly prevalent.

- Drivers of Other Component Type Evolution:

- Focus on occupant comfort and ergonomic design.

- Development of lightweight and durable seating materials.

- Integration of smart textiles and heating/cooling elements.

Europe Automotive Interiors Industry Product Developments

Product development in the Europe automotive interiors sector is heavily focused on enhancing the occupant experience through technological integration and sustainable material innovation. Key innovations include the development of intelligent seating systems with advanced ergonomic adjustments and integrated comfort features, as well as the proliferation of customizable ambient lighting solutions that adapt to driving conditions or passenger preferences. The integration of sophisticated infotainment systems with AI-powered voice assistants and larger, higher-resolution displays continues to be a major trend. Furthermore, there is a significant push towards using lightweight, recycled, and bio-based materials for interior components, contributing to vehicle fuel efficiency and reduced environmental impact. The competitive advantage lies in offering seamlessly integrated, user-friendly, and sustainable interior solutions that meet the evolving demands of both automakers and end-users.

Report Scope & Segmentation Analysis

This report comprehensively analyzes the Europe automotive interiors market segmented by vehicle type and component type. The Vehicle Type segmentation includes Passenger Cars and Commercial Vehicles. The Component Type segmentation encompasses Infotainment Systems, Instrument Panels, Interior Lighting, Body Panels, and Other Component Types.

For Passenger Cars, the market is expected to witness sustained growth, driven by premiumization trends and the rapid adoption of EVs. Growth projections indicate a significant market size, with competitive dynamics focused on technological innovation and enhanced user experience.

The Commercial Vehicles segment, while smaller, presents steady growth opportunities, particularly in fleet efficiency and driver comfort. Projections show a consistent market expansion, with competition centered on durability, functionality, and integration of telematics.

In the Infotainment Systems segment, high growth is anticipated due to increasing consumer demand for connectivity and advanced digital services. Market sizes are substantial, with competitive dynamics driven by software innovation and seamless integration.

The Instrument Panels segment is projected for strong growth as digital cockpits and customizable displays become standard. Market sizes are significant, with competition focused on aesthetics, functionality, and integration of new display technologies.

Interior Lighting is expected to see robust growth driven by personalization trends and its role in enhancing cabin ambiance. Market sizes are growing, with competition emphasizing advanced LED technology and smart control systems.

Body Panels (interior) are projected for moderate growth, with a focus on sustainable materials and improved acoustic properties. Market sizes are considerable, with competition centered on material innovation and aesthetic integration.

Other Component Types, including seating, are anticipated to experience steady growth, driven by comfort, ergonomics, and new material applications. Market sizes are diverse, with competition focusing on advanced design and functionality.

Key Drivers of Europe Automotive Interiors Industry Growth

The Europe automotive interiors industry is experiencing robust growth fueled by several key factors. The accelerating transition towards electric vehicles (EVs) is a significant catalyst, demanding novel interior designs, lightweight materials, and integrated battery management systems. Consumer demand for enhanced comfort, sophisticated infotainment, and personalized experiences further drives innovation and spending on premium interior features. Stricter environmental regulations and a growing consumer awareness of sustainability are pushing the adoption of recycled, bio-based, and lightweight materials, contributing to both reduced emissions and improved vehicle efficiency. Furthermore, advancements in digital technologies, including AI, connectivity, and advanced HMI, are transforming the in-car experience, leading to higher adoption rates of smart interior solutions.

Challenges in the Europe Automotive Interiors Industry Sector

Despite the positive growth trajectory, the Europe automotive interiors sector faces several challenges. Supply chain disruptions, exacerbated by geopolitical events and material shortages, continue to pose a significant risk to production timelines and cost management. Increasing regulatory scrutiny regarding material composition, recyclability, and safety standards necessitates continuous adaptation and investment in compliance. The high cost of research and development for advanced technologies, coupled with intense price pressure from OEMs, can strain profit margins for suppliers. Moreover, the evolving nature of automotive design, with a shift towards minimalist interiors and integrated functionalities, requires significant retooling and adaptation of manufacturing processes, presenting a substantial capital investment challenge.

Emerging Opportunities in Europe Automotive Interiors Industry

Emerging opportunities in the Europe automotive interiors market are closely tied to technological advancements and evolving consumer preferences. The growth of autonomous driving is creating new possibilities for interior configurations, focusing on passenger comfort, entertainment, and productivity during transit. The increasing demand for personalized and customizable interiors presents a significant opportunity for suppliers offering modular solutions and advanced HMI interfaces. The circular economy and sustainability initiatives are driving innovation in the use of recycled and bio-based materials, creating new markets for eco-friendly interior components. Furthermore, the expansion of the EV market necessitates specialized interior solutions, including advanced thermal management and innovative storage designs, offering substantial growth potential.

Leading Players in the Europe Automotive Interiors Industry Market

- Recaro Group

- Groclin S A

- PRETTL Lighting & Interior GmbH

- SKA Sitze GmbH

- Grupo Antolin

- GUMOTEX Automotive Břeclav sro

- EFI Automotive Group

- Faurecia

- Adient PLC

- Grammer AG

Key Developments in Europe Automotive Interiors Industry Industry

- April 2023: Marelli demonstrated its latest innovations at Auto Shanghai 2023, focusing on co-creating the future of mobility. Their electromechanical actuator, known as full active electromechanics technology, minimizes roll, pitch, yaw, and vibration through the self-generated reactive force and provides sound damping inside the vehicle.

- April 2023: Schaeffler, a leading automotive technology company, introduced a new damping solution aimed at reducing vehicle vibrations and noise. The company's innovative "VibSense" technology combines sensors and algorithms to detect and analyze vibrations, allowing for targeted damping interventions.

- January 2023: Panasonic Automotive announced the update of the SkipGenin-vehicle infotainment system to offer industry-first wakeword access to Siri and Alexa. This system provides customers simultaneous access to Siri while using Apple CarPlay or Alexa.

- November 2022: Daewon Precision Ind. Co., Ltd. (Daewon Precision) announced the completion of a new plant of car seats for the Hyundai Genesis brand, which will be produced at the brand-new Daewon Premium Mechanism (DPM) plant. It will also provide seat components for the Genesis brand of electric vehicles (EVs), whose mass production is expected to begin in or after 2025.

- October 2022: Lear Corporation opened its new manufacturing facility in Meknes. The new plant, which was constructed on an area of 54,000 sq m, including 18,200 sq m dedicated to production, required an investment of USD 18.2 million. It enabled the creation of more than 2,000 direct jobs that would grow to 2,600 jobs in 2023.

Strategic Outlook for Europe Automotive Interiors Industry Market

The strategic outlook for the Europe automotive interiors industry remains highly positive, driven by ongoing technological advancements and evolving consumer expectations. The continued electrification of the automotive fleet will necessitate innovative interior solutions tailored for EVs, presenting a substantial growth catalyst. The increasing demand for digital integration, enhanced connectivity, and personalized user experiences will drive further investment in smart interior technologies and advanced HMI. Sustainability will remain a core strategic imperative, pushing for wider adoption of circular economy principles and eco-friendly materials. Partnerships and collaborations between automakers and interior suppliers will be crucial for developing integrated, next-generation interior systems that deliver superior occupant comfort, safety, and entertainment, ensuring continued market expansion and innovation.

Europe Automotive Interiors Industry Segmentation

-

1. Vehicle Type

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Component Type

- 2.1. Infotainment Systems

- 2.2. Instrument Panels

- 2.3. Interior Lighting

- 2.4. Body Panels

- 2.5. Other Component Types

Europe Automotive Interiors Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

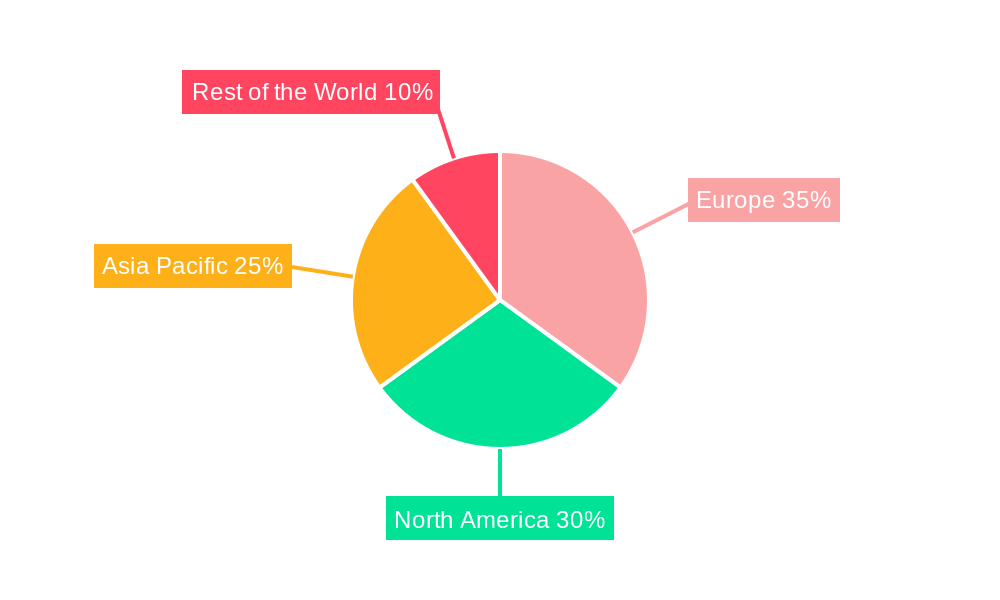

Europe Automotive Interiors Industry Regional Market Share

Geographic Coverage of Europe Automotive Interiors Industry

Europe Automotive Interiors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. RAX Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Component Type

- 5.2.1. Infotainment Systems

- 5.2.2. Instrument Panels

- 5.2.3. Interior Lighting

- 5.2.4. Body Panels

- 5.2.5. Other Component Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Europe Automotive Interiors Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Component Type

- 6.2.1. Infotainment Systems

- 6.2.2. Instrument Panels

- 6.2.3. Interior Lighting

- 6.2.4. Body Panels

- 6.2.5. Other Component Types

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Recaro Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Groclin S A

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 PRETTL Lighting & Interior GmbH

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 SKA Sitze GmbH

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Grupo Antolin

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 GUMOTEX Automotive B?eclav sro*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 EFI Automotive Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Faurecia

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Adient PLC

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Grammer AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Recaro Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Automotive Interiors Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Automotive Interiors Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Automotive Interiors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: Europe Automotive Interiors Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 3: Europe Automotive Interiors Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe Automotive Interiors Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 5: Europe Automotive Interiors Industry Revenue Million Forecast, by Component Type 2020 & 2033

- Table 6: Europe Automotive Interiors Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: France Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Automotive Interiors Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Interiors Industry?

The projected CAGR is approximately 6.35%.

2. Which companies are prominent players in the Europe Automotive Interiors Industry?

Key companies in the market include Recaro Group, Groclin S A, PRETTL Lighting & Interior GmbH, SKA Sitze GmbH, Grupo Antolin, GUMOTEX Automotive B?eclav sro*List Not Exhaustive, EFI Automotive Group, Faurecia, Adient PLC, Grammer AG.

3. What are the main segments of the Europe Automotive Interiors Industry?

The market segments include Vehicle Type, Component Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 65.18 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Popularity for Aftermarket Vehicle Modification May Drive the Market.

6. What are the notable trends driving market growth?

Interior Lighting is Anticipated to Register Highest Growth.

7. Are there any restraints impacting market growth?

Stringent Regulations Against Modifications.

8. Can you provide examples of recent developments in the market?

April 2023: Marelli demonstrated its latest innovations at Auto Shanghai 2023, focusing on co-creating the future of mobility. Their electromechanical actuator, known as full active electromechanics technology, minimizes roll, pitch, yaw, and vibration through the self-generated reactive force and provides sound damping inside the vehicle.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Interiors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Interiors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Interiors Industry?

To stay informed about further developments, trends, and reports in the Europe Automotive Interiors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence