Key Insights

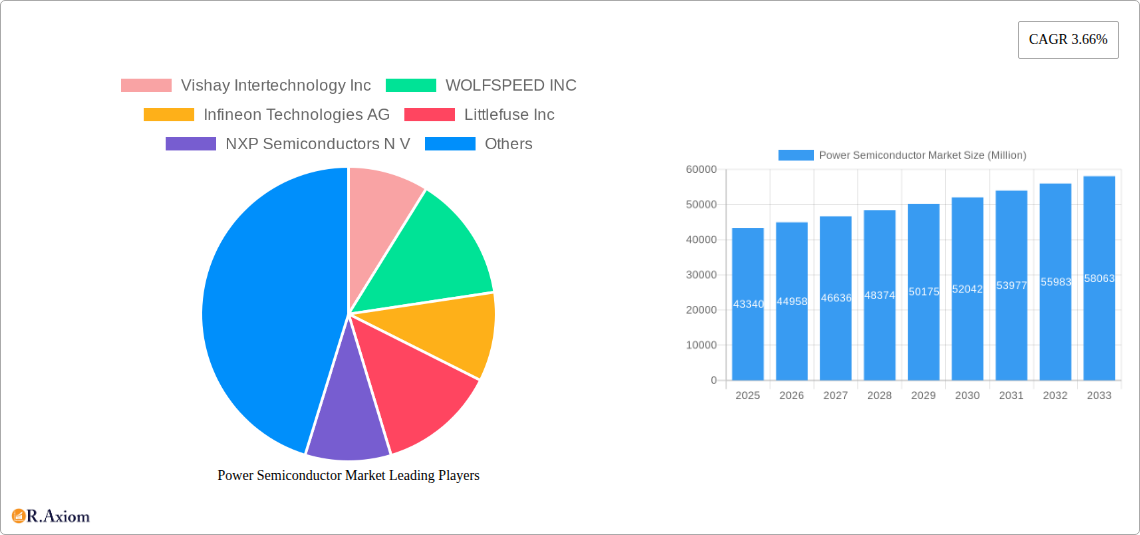

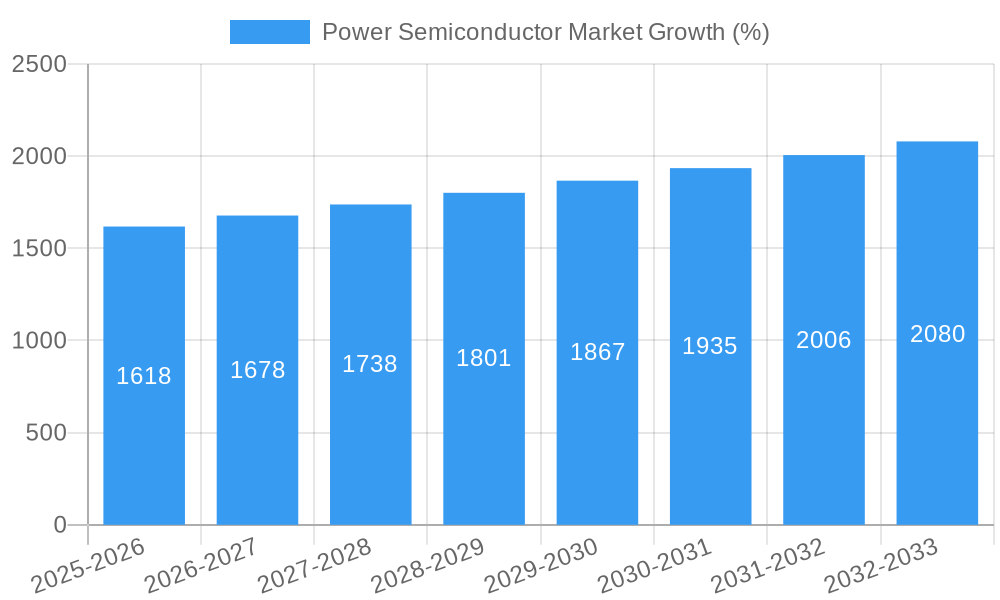

The power semiconductor market, valued at $43.34 billion in 2025, is projected to experience robust growth, driven by the increasing demand for energy-efficient electronics across diverse sectors. The Compound Annual Growth Rate (CAGR) of 3.66% from 2025 to 2033 indicates a steady expansion, fueled primarily by the automotive industry's electrification trend, the proliferation of renewable energy sources requiring efficient power management, and the surging adoption of high-power applications in data centers and industrial automation. Significant advancements in silicon carbide (SiC) and gallium nitride (GaN) technologies are further accelerating market growth, enabling higher power density, improved efficiency, and reduced energy loss compared to traditional silicon-based semiconductors. The market segmentation reveals a strong presence of discrete components, particularly SiC and GaN modules, reflecting the industry's shift towards more efficient power conversion solutions. Leading companies like Infineon, Wolfspeed, and STMicroelectronics are actively investing in R&D and expanding their product portfolios to capitalize on this growth trajectory. While challenges such as the high cost of SiC and GaN components and potential supply chain disruptions exist, the long-term outlook for the power semiconductor market remains positive, driven by sustained technological innovation and the global push for energy efficiency.

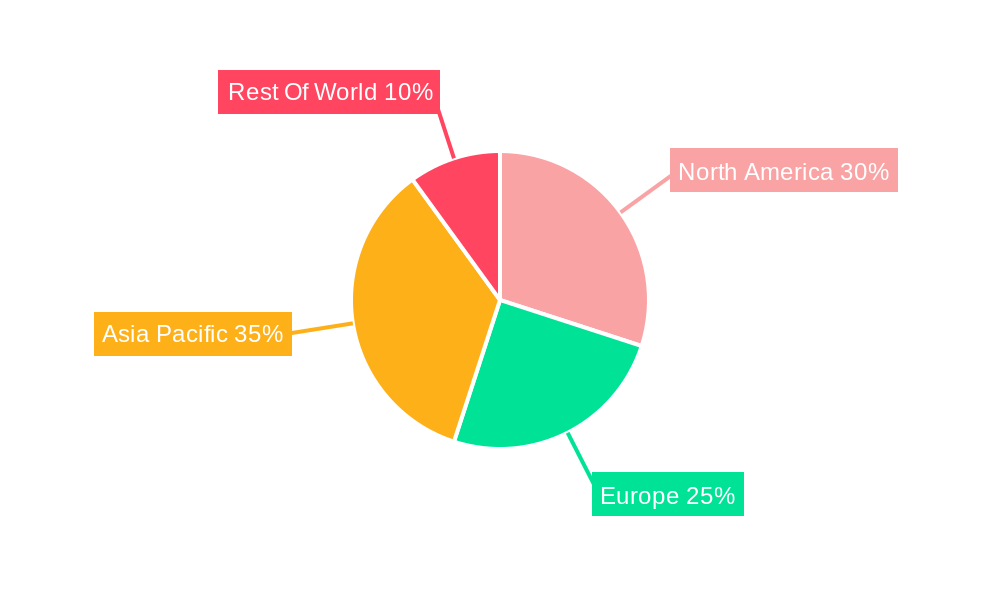

The growth across various segments is expected to be uneven. The automotive segment is anticipated to be the largest and fastest-growing end-user industry, driven by the rising demand for electric vehicles and hybrid electric vehicles. The consumer electronics segment is also poised for significant expansion due to the increased adoption of energy-efficient appliances and portable devices. Within components, the demand for modules (including SiC and GaN) will likely outpace the growth of individual discrete components, reflecting the preference for integrated and efficient power management solutions. Geographically, the Asia-Pacific region is projected to be a key growth driver, propelled by the rapid industrialization and significant investments in renewable energy infrastructure across several countries. North America and Europe will also maintain substantial market shares, driven by strong technological advancements and ongoing investments in renewable energy and energy-efficient technologies.

This in-depth report provides a comprehensive analysis of the Power Semiconductor Market, covering market size, segmentation, growth drivers, challenges, and key players. The report utilizes data from the historical period (2019-2024), base year (2025), and estimated year (2025) to forecast market trends up to 2033. The study includes detailed insights into market concentration, innovation, industry trends, dominant segments, product developments, and key players' strategies. This report is essential for industry stakeholders, investors, and anyone seeking a comprehensive understanding of this dynamic market.

Power Semiconductor Market Market Concentration & Innovation

The Power Semiconductor market is characterized by a moderately concentrated landscape with a few major players holding significant market share. While exact market share figures vary depending on the segment (discrete, modules, power ICs, etc.), companies like Infineon Technologies AG, STMicroelectronics NV, and ON Semiconductor Corporation consistently rank among the top contenders. The market's concentration is further influenced by the high capital investment required for research and development and manufacturing. Innovation is a critical driver, with continuous advancements in materials (Silicon Carbide (SiC) and Gallium Nitride (GaN)), packaging, and manufacturing processes pushing the boundaries of performance and efficiency. Strict regulatory frameworks, particularly concerning energy efficiency and environmental standards, incentivize innovation and drive the adoption of advanced semiconductor technologies.

Product substitution is a significant factor, with SiC and GaN-based devices progressively replacing traditional silicon-based semiconductors in applications demanding higher efficiency and power density. The market also observes significant M&A activity, as larger players seek to expand their product portfolios and market reach. While precise deal values for all M&A activities are not publicly available, significant multi-Million dollar transactions involving technology licensing and acquisitions of smaller firms specializing in specific technologies regularly take place. End-user trends, such as the rising demand for electric vehicles and renewable energy technologies, significantly influence market dynamics.

- Market Share: Infineon, STMicroelectronics, and ON Semiconductor hold a significant, yet evolving, market share (xx%).

- M&A Activity: Significant M&A activity is observed (Total value estimated at xx Million during 2019-2024).

- Innovation Drivers: Advancements in materials (SiC, GaN), packaging, and manufacturing processes.

- Regulatory Frameworks: Stringent energy efficiency and environmental regulations drive innovation.

- Product Substitution: Gradual replacement of silicon with SiC and GaN-based semiconductors.

Power Semiconductor Market Industry Trends & Insights

The Power Semiconductor market is experiencing robust growth, driven by the escalating demand for energy-efficient electronics across various sectors. The compound annual growth rate (CAGR) during the forecast period (2025-2033) is projected to be xx%, fueled by several key factors. Technological disruptions, such as the wider adoption of SiC and GaN technologies, are revolutionizing the industry, enabling higher power density and efficiency in applications like electric vehicles, renewable energy systems, and data centers. Consumer preferences for smaller, lighter, and more energy-efficient devices further fuel market expansion. The competitive landscape is highly dynamic, with ongoing technological advancements and strategic collaborations among industry players. Market penetration of SiC and GaN-based power semiconductors is steadily increasing, exceeding xx% in certain niche applications (e.g., electric vehicle inverters). This trend is expected to accelerate as manufacturing costs decrease and performance advantages become increasingly apparent.

Dominant Markets & Segments in Power Semiconductor Market

The Automotive sector is currently the dominant end-user industry for power semiconductors, driven by the rapid growth of electric vehicles (EVs) and hybrid electric vehicles (HEVs). The increasing adoption of advanced driver-assistance systems (ADAS) and the electrification of powertrains further fuels this demand. Within the component segment, discrete power semiconductors hold the largest market share, though the adoption of modules (SiC and GaN) is rapidly increasing due to their improved power density and efficiency. Silicon remains the most widely used material, but SiC and GaN are gaining traction in high-power, high-frequency applications.

- Dominant End-user Industry: Automotive (driven by EV adoption and ADAS).

- Dominant Component: Discrete semiconductors.

- Dominant Material: Silicon, with growing adoption of SiC and GaN.

- Key Drivers (Automotive): Rising EV sales, increasing demand for ADAS, government incentives for electric vehicle adoption.

- Key Drivers (Industrial): Automation in manufacturing, renewable energy infrastructure development, power grid modernization.

Power Semiconductor Market Product Developments

Recent product innovations focus on enhancing efficiency, reducing size, and improving thermal management. Companies are actively developing high-voltage, high-frequency SiC and GaN-based devices that offer significant advantages over traditional silicon-based alternatives. These advancements are improving the overall performance of power systems in diverse applications, such as electric vehicles, renewable energy systems, data centers, and consumer electronics. The competitive advantage lies in the ability to deliver superior performance, cost-effectiveness, and reliability. Furthermore, companies are investing heavily in innovative packaging technologies to improve thermal performance and reduce overall system size.

Report Scope & Segmentation Analysis

This report segments the Power Semiconductor market across various dimensions:

By End-user Industry: Automotive, Consumer Electronics, IT and Telecommunication, Military and Aerospace, Power, Industrial, Other End-user Industries. Each segment's growth is projected based on its respective growth drivers, market size, and competitive landscape. Automotive and Industrial segments exhibit the highest growth rate.

By Component: Discrete, Modules (SiC and GaN), Power ICs. The market size for each segment is estimated and forecast, with discrete components holding the largest share currently, though the modules segment is growing rapidly.

By Material: Silicon, Silicon Carbide (SiC), Gallium Nitride (GaN). Silicon currently dominates, but SiC and GaN show significant growth potential driven by their superior properties.

Key Drivers of Power Semiconductor Market Growth

The Power Semiconductor market's growth is driven by several key factors, including:

- Increasing demand for electric vehicles: The global shift towards electric mobility is significantly boosting the demand for high-efficiency power semiconductors.

- Growth of renewable energy: The increasing adoption of solar and wind energy requires efficient power conversion systems, driving demand for power semiconductors.

- Advancements in data center infrastructure: Data centers need high-efficiency power semiconductors to manage the increasing power demands.

- Government regulations promoting energy efficiency: Stringent regulations are driving the adoption of energy-efficient semiconductor technologies.

Challenges in the Power Semiconductor Market Sector

The Power Semiconductor market faces certain challenges:

- Supply chain disruptions: The global semiconductor shortage has impacted the availability of power semiconductors, leading to price increases and delays.

- High manufacturing costs: The production of advanced power semiconductors, particularly SiC and GaN devices, involves high capital expenditures.

- Intense competition: The market is characterized by intense competition among established and emerging players.

Emerging Opportunities in Power Semiconductor Market

Several opportunities exist in the Power Semiconductor Market:

- Growing demand for high-efficiency power systems: The demand for energy-efficient electronic devices is expected to grow rapidly, creating opportunities for power semiconductors.

- Expansion into new applications: Power semiconductors are finding their way into new applications such as drones, robotics, and 5G infrastructure.

- Development of next-generation materials: Research and development of new materials with superior properties can offer significant advancements in power semiconductors.

Leading Players in the Power Semiconductor Market Market

- Vishay Intertechnology Inc

- WOLFSPEED INC

- Infineon Technologies AG

- Littlefuse Inc

- NXP Semiconductors N V

- Microchip Technology Inc

- Mistibushi Electric Corporation

- Toshiba Corporation

- Fuji Electric Co Ltd

- Rohm Co Ltd

- Magnachip Semiconductor Corp

- QORVO INC

- Alpha & Omega Semiconductor

- Broadcom Inc

- STMicroelectronics NV

- Renesas Electric Corporation

- ON Semiconductor Corporation

- Texas Instruments Incorporated

- Nexperia Holding B V (Wingtech Technology Co Ltd)

- Semikron Danfoss Holding A/S (Danfoss A/S)

Key Developments in Power Semiconductor Market Industry

- May 2023: Infineon Technologies AG launched the OptiMOS7 40V MOSFET family, a new generation of power MOSFETs for automotive applications, offering significant performance benefits in compact packages. This launch strengthens Infineon's position in the automotive power semiconductor market.

- May 2023: Toshiba Electronics Europe launched a new 150V N-channel power MOSFET (TPH9R00CQ5), designed for high-performance switching power supplies in communication base stations and industrial applications. This product enhances Toshiba's offerings in high-power applications.

Strategic Outlook for Power Semiconductor Market Market

The Power Semiconductor market is poised for continued growth, driven by increasing demand from diverse sectors and ongoing technological advancements. The adoption of SiC and GaN-based devices will be a key growth catalyst, transforming power electronics efficiency and performance. Further market expansion is expected in emerging applications, requiring manufacturers to stay innovative and adapt to changing customer demands. The strategic focus on improving energy efficiency, reducing system size, and enhancing reliability will remain paramount for success in this dynamic and competitive market.

Power Semiconductor Market Segmentation

-

1. Component

-

1.1. Discrete

- 1.1.1. Rectifier

- 1.1.2. Bipolar

- 1.1.3. MOSFET

- 1.1.4. IGBT

- 1.1.5. Other Discrete Components (Thyristor and HEMT)

- 1.2. Modules

-

1.3. Power IC

- 1.3.1. Multichannel PMICS

- 1.3.2. Switchin

- 1.3.3. Linear Regulators

- 1.3.4. BMICs

- 1.3.5. Other Components

-

1.1. Discrete

-

2. Material

- 2.1. Silicon/Germanium

- 2.2. Silicon Carbide (SiC)

- 2.3. Gallium Nitride (GaN)

-

3. End-user Industry

- 3.1. Automotive

- 3.2. Consumer Electronics

- 3.3. IT and Telecommunication

- 3.4. Military and Aerospace

- 3.5. Power

- 3.6. Industrial

- 3.7. Other End-user Industries

Power Semiconductor Market Segmentation By Geography

- 1. United States

- 2. Europe

- 3. Japan

- 4. China

- 5. South Korea

- 6. Taiwan

Power Semiconductor Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.66% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Consumer Electronics and Wireless Communications; Growing Demand for Energy-Efficient Battery-powered Portable Devices

- 3.3. Market Restrains

- 3.3.1. Shortage of Silicon Wafers and Variable Driving Requirement

- 3.4. Market Trends

- 3.4.1. MOSFETs to be the Largest Discrete Semiconductor Component

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Discrete

- 5.1.1.1. Rectifier

- 5.1.1.2. Bipolar

- 5.1.1.3. MOSFET

- 5.1.1.4. IGBT

- 5.1.1.5. Other Discrete Components (Thyristor and HEMT)

- 5.1.2. Modules

- 5.1.3. Power IC

- 5.1.3.1. Multichannel PMICS

- 5.1.3.2. Switchin

- 5.1.3.3. Linear Regulators

- 5.1.3.4. BMICs

- 5.1.3.5. Other Components

- 5.1.1. Discrete

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Silicon/Germanium

- 5.2.2. Silicon Carbide (SiC)

- 5.2.3. Gallium Nitride (GaN)

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Automotive

- 5.3.2. Consumer Electronics

- 5.3.3. IT and Telecommunication

- 5.3.4. Military and Aerospace

- 5.3.5. Power

- 5.3.6. Industrial

- 5.3.7. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Europe

- 5.4.3. Japan

- 5.4.4. China

- 5.4.5. South Korea

- 5.4.6. Taiwan

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. United States Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Discrete

- 6.1.1.1. Rectifier

- 6.1.1.2. Bipolar

- 6.1.1.3. MOSFET

- 6.1.1.4. IGBT

- 6.1.1.5. Other Discrete Components (Thyristor and HEMT)

- 6.1.2. Modules

- 6.1.3. Power IC

- 6.1.3.1. Multichannel PMICS

- 6.1.3.2. Switchin

- 6.1.3.3. Linear Regulators

- 6.1.3.4. BMICs

- 6.1.3.5. Other Components

- 6.1.1. Discrete

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Silicon/Germanium

- 6.2.2. Silicon Carbide (SiC)

- 6.2.3. Gallium Nitride (GaN)

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Automotive

- 6.3.2. Consumer Electronics

- 6.3.3. IT and Telecommunication

- 6.3.4. Military and Aerospace

- 6.3.5. Power

- 6.3.6. Industrial

- 6.3.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Europe Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Discrete

- 7.1.1.1. Rectifier

- 7.1.1.2. Bipolar

- 7.1.1.3. MOSFET

- 7.1.1.4. IGBT

- 7.1.1.5. Other Discrete Components (Thyristor and HEMT)

- 7.1.2. Modules

- 7.1.3. Power IC

- 7.1.3.1. Multichannel PMICS

- 7.1.3.2. Switchin

- 7.1.3.3. Linear Regulators

- 7.1.3.4. BMICs

- 7.1.3.5. Other Components

- 7.1.1. Discrete

- 7.2. Market Analysis, Insights and Forecast - by Material

- 7.2.1. Silicon/Germanium

- 7.2.2. Silicon Carbide (SiC)

- 7.2.3. Gallium Nitride (GaN)

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Automotive

- 7.3.2. Consumer Electronics

- 7.3.3. IT and Telecommunication

- 7.3.4. Military and Aerospace

- 7.3.5. Power

- 7.3.6. Industrial

- 7.3.7. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Japan Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Discrete

- 8.1.1.1. Rectifier

- 8.1.1.2. Bipolar

- 8.1.1.3. MOSFET

- 8.1.1.4. IGBT

- 8.1.1.5. Other Discrete Components (Thyristor and HEMT)

- 8.1.2. Modules

- 8.1.3. Power IC

- 8.1.3.1. Multichannel PMICS

- 8.1.3.2. Switchin

- 8.1.3.3. Linear Regulators

- 8.1.3.4. BMICs

- 8.1.3.5. Other Components

- 8.1.1. Discrete

- 8.2. Market Analysis, Insights and Forecast - by Material

- 8.2.1. Silicon/Germanium

- 8.2.2. Silicon Carbide (SiC)

- 8.2.3. Gallium Nitride (GaN)

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Automotive

- 8.3.2. Consumer Electronics

- 8.3.3. IT and Telecommunication

- 8.3.4. Military and Aerospace

- 8.3.5. Power

- 8.3.6. Industrial

- 8.3.7. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. China Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Discrete

- 9.1.1.1. Rectifier

- 9.1.1.2. Bipolar

- 9.1.1.3. MOSFET

- 9.1.1.4. IGBT

- 9.1.1.5. Other Discrete Components (Thyristor and HEMT)

- 9.1.2. Modules

- 9.1.3. Power IC

- 9.1.3.1. Multichannel PMICS

- 9.1.3.2. Switchin

- 9.1.3.3. Linear Regulators

- 9.1.3.4. BMICs

- 9.1.3.5. Other Components

- 9.1.1. Discrete

- 9.2. Market Analysis, Insights and Forecast - by Material

- 9.2.1. Silicon/Germanium

- 9.2.2. Silicon Carbide (SiC)

- 9.2.3. Gallium Nitride (GaN)

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Automotive

- 9.3.2. Consumer Electronics

- 9.3.3. IT and Telecommunication

- 9.3.4. Military and Aerospace

- 9.3.5. Power

- 9.3.6. Industrial

- 9.3.7. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. South Korea Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Discrete

- 10.1.1.1. Rectifier

- 10.1.1.2. Bipolar

- 10.1.1.3. MOSFET

- 10.1.1.4. IGBT

- 10.1.1.5. Other Discrete Components (Thyristor and HEMT)

- 10.1.2. Modules

- 10.1.3. Power IC

- 10.1.3.1. Multichannel PMICS

- 10.1.3.2. Switchin

- 10.1.3.3. Linear Regulators

- 10.1.3.4. BMICs

- 10.1.3.5. Other Components

- 10.1.1. Discrete

- 10.2. Market Analysis, Insights and Forecast - by Material

- 10.2.1. Silicon/Germanium

- 10.2.2. Silicon Carbide (SiC)

- 10.2.3. Gallium Nitride (GaN)

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Automotive

- 10.3.2. Consumer Electronics

- 10.3.3. IT and Telecommunication

- 10.3.4. Military and Aerospace

- 10.3.5. Power

- 10.3.6. Industrial

- 10.3.7. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Taiwan Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Discrete

- 11.1.1.1. Rectifier

- 11.1.1.2. Bipolar

- 11.1.1.3. MOSFET

- 11.1.1.4. IGBT

- 11.1.1.5. Other Discrete Components (Thyristor and HEMT)

- 11.1.2. Modules

- 11.1.3. Power IC

- 11.1.3.1. Multichannel PMICS

- 11.1.3.2. Switchin

- 11.1.3.3. Linear Regulators

- 11.1.3.4. BMICs

- 11.1.3.5. Other Components

- 11.1.1. Discrete

- 11.2. Market Analysis, Insights and Forecast - by Material

- 11.2.1. Silicon/Germanium

- 11.2.2. Silicon Carbide (SiC)

- 11.2.3. Gallium Nitride (GaN)

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Automotive

- 11.3.2. Consumer Electronics

- 11.3.3. IT and Telecommunication

- 11.3.4. Military and Aerospace

- 11.3.5. Power

- 11.3.6. Industrial

- 11.3.7. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. North America Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Europe Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Asia Pacific Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Rest Of The World Power Semiconductor Market Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Vishay Intertechnology Inc

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 WOLFSPEED INC

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Infineon Technologies AG

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Littlefuse Inc

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 NXP Semiconductors N V

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Microchip Technology Inc

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Mistibushi Electric Corporation

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Toshiba Corporation

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Fuji Electric Co Ltd

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Rohm Co Ltd

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Magnachip Semiconductor Corp

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 QORVO INC

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Alpha & Omega Semiconductor

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.14 Broadcom Inc

- 16.2.14.1. Overview

- 16.2.14.2. Products

- 16.2.14.3. SWOT Analysis

- 16.2.14.4. Recent Developments

- 16.2.14.5. Financials (Based on Availability)

- 16.2.15 STMicroelectronics NV

- 16.2.15.1. Overview

- 16.2.15.2. Products

- 16.2.15.3. SWOT Analysis

- 16.2.15.4. Recent Developments

- 16.2.15.5. Financials (Based on Availability)

- 16.2.16 Renesas Electric Corporation

- 16.2.16.1. Overview

- 16.2.16.2. Products

- 16.2.16.3. SWOT Analysis

- 16.2.16.4. Recent Developments

- 16.2.16.5. Financials (Based on Availability)

- 16.2.17 ON Semiconductor Corporation

- 16.2.17.1. Overview

- 16.2.17.2. Products

- 16.2.17.3. SWOT Analysis

- 16.2.17.4. Recent Developments

- 16.2.17.5. Financials (Based on Availability)

- 16.2.18 Texas Instruments Incorporated

- 16.2.18.1. Overview

- 16.2.18.2. Products

- 16.2.18.3. SWOT Analysis

- 16.2.18.4. Recent Developments

- 16.2.18.5. Financials (Based on Availability)

- 16.2.19 Nexperia Holding B V (Wingtech Technology Co Ltd)

- 16.2.19.1. Overview

- 16.2.19.2. Products

- 16.2.19.3. SWOT Analysis

- 16.2.19.4. Recent Developments

- 16.2.19.5. Financials (Based on Availability)

- 16.2.20 Semikron Danfoss Holding A/S (Danfoss A/S)

- 16.2.20.1. Overview

- 16.2.20.2. Products

- 16.2.20.3. SWOT Analysis

- 16.2.20.4. Recent Developments

- 16.2.20.5. Financials (Based on Availability)

- 16.2.1 Vishay Intertechnology Inc

List of Figures

- Figure 1: Global Power Semiconductor Market Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 8: Rest Of The World Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 9: Rest Of The World Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 10: United States Power Semiconductor Market Revenue (Million), by Component 2024 & 2032

- Figure 11: United States Power Semiconductor Market Revenue Share (%), by Component 2024 & 2032

- Figure 12: United States Power Semiconductor Market Revenue (Million), by Material 2024 & 2032

- Figure 13: United States Power Semiconductor Market Revenue Share (%), by Material 2024 & 2032

- Figure 14: United States Power Semiconductor Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 15: United States Power Semiconductor Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 16: United States Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 17: United States Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Power Semiconductor Market Revenue (Million), by Component 2024 & 2032

- Figure 19: Europe Power Semiconductor Market Revenue Share (%), by Component 2024 & 2032

- Figure 20: Europe Power Semiconductor Market Revenue (Million), by Material 2024 & 2032

- Figure 21: Europe Power Semiconductor Market Revenue Share (%), by Material 2024 & 2032

- Figure 22: Europe Power Semiconductor Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 23: Europe Power Semiconductor Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 24: Europe Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 25: Europe Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 26: Japan Power Semiconductor Market Revenue (Million), by Component 2024 & 2032

- Figure 27: Japan Power Semiconductor Market Revenue Share (%), by Component 2024 & 2032

- Figure 28: Japan Power Semiconductor Market Revenue (Million), by Material 2024 & 2032

- Figure 29: Japan Power Semiconductor Market Revenue Share (%), by Material 2024 & 2032

- Figure 30: Japan Power Semiconductor Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 31: Japan Power Semiconductor Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 32: Japan Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 33: Japan Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 34: China Power Semiconductor Market Revenue (Million), by Component 2024 & 2032

- Figure 35: China Power Semiconductor Market Revenue Share (%), by Component 2024 & 2032

- Figure 36: China Power Semiconductor Market Revenue (Million), by Material 2024 & 2032

- Figure 37: China Power Semiconductor Market Revenue Share (%), by Material 2024 & 2032

- Figure 38: China Power Semiconductor Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 39: China Power Semiconductor Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 40: China Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 41: China Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 42: South Korea Power Semiconductor Market Revenue (Million), by Component 2024 & 2032

- Figure 43: South Korea Power Semiconductor Market Revenue Share (%), by Component 2024 & 2032

- Figure 44: South Korea Power Semiconductor Market Revenue (Million), by Material 2024 & 2032

- Figure 45: South Korea Power Semiconductor Market Revenue Share (%), by Material 2024 & 2032

- Figure 46: South Korea Power Semiconductor Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 47: South Korea Power Semiconductor Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 48: South Korea Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 49: South Korea Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

- Figure 50: Taiwan Power Semiconductor Market Revenue (Million), by Component 2024 & 2032

- Figure 51: Taiwan Power Semiconductor Market Revenue Share (%), by Component 2024 & 2032

- Figure 52: Taiwan Power Semiconductor Market Revenue (Million), by Material 2024 & 2032

- Figure 53: Taiwan Power Semiconductor Market Revenue Share (%), by Material 2024 & 2032

- Figure 54: Taiwan Power Semiconductor Market Revenue (Million), by End-user Industry 2024 & 2032

- Figure 55: Taiwan Power Semiconductor Market Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 56: Taiwan Power Semiconductor Market Revenue (Million), by Country 2024 & 2032

- Figure 57: Taiwan Power Semiconductor Market Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Power Semiconductor Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Power Semiconductor Market Revenue Million Forecast, by Component 2019 & 2032

- Table 3: Global Power Semiconductor Market Revenue Million Forecast, by Material 2019 & 2032

- Table 4: Global Power Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 5: Global Power Semiconductor Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Power Semiconductor Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 9: Power Semiconductor Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Power Semiconductor Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 13: Power Semiconductor Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Global Power Semiconductor Market Revenue Million Forecast, by Component 2019 & 2032

- Table 15: Global Power Semiconductor Market Revenue Million Forecast, by Material 2019 & 2032

- Table 16: Global Power Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 17: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Power Semiconductor Market Revenue Million Forecast, by Component 2019 & 2032

- Table 19: Global Power Semiconductor Market Revenue Million Forecast, by Material 2019 & 2032

- Table 20: Global Power Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 21: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Global Power Semiconductor Market Revenue Million Forecast, by Component 2019 & 2032

- Table 23: Global Power Semiconductor Market Revenue Million Forecast, by Material 2019 & 2032

- Table 24: Global Power Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 25: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Global Power Semiconductor Market Revenue Million Forecast, by Component 2019 & 2032

- Table 27: Global Power Semiconductor Market Revenue Million Forecast, by Material 2019 & 2032

- Table 28: Global Power Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 29: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Global Power Semiconductor Market Revenue Million Forecast, by Component 2019 & 2032

- Table 31: Global Power Semiconductor Market Revenue Million Forecast, by Material 2019 & 2032

- Table 32: Global Power Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 33: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

- Table 34: Global Power Semiconductor Market Revenue Million Forecast, by Component 2019 & 2032

- Table 35: Global Power Semiconductor Market Revenue Million Forecast, by Material 2019 & 2032

- Table 36: Global Power Semiconductor Market Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 37: Global Power Semiconductor Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Power Semiconductor Market?

The projected CAGR is approximately 3.66%.

2. Which companies are prominent players in the Power Semiconductor Market?

Key companies in the market include Vishay Intertechnology Inc, WOLFSPEED INC, Infineon Technologies AG, Littlefuse Inc, NXP Semiconductors N V, Microchip Technology Inc, Mistibushi Electric Corporation, Toshiba Corporation, Fuji Electric Co Ltd, Rohm Co Ltd, Magnachip Semiconductor Corp, QORVO INC, Alpha & Omega Semiconductor, Broadcom Inc, STMicroelectronics NV, Renesas Electric Corporation, ON Semiconductor Corporation, Texas Instruments Incorporated, Nexperia Holding B V (Wingtech Technology Co Ltd), Semikron Danfoss Holding A/S (Danfoss A/S).

3. What are the main segments of the Power Semiconductor Market?

The market segments include Component, Material, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 43.34 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Consumer Electronics and Wireless Communications; Growing Demand for Energy-Efficient Battery-powered Portable Devices.

6. What are the notable trends driving market growth?

MOSFETs to be the Largest Discrete Semiconductor Component.

7. Are there any restraints impacting market growth?

Shortage of Silicon Wafers and Variable Driving Requirement.

8. Can you provide examples of recent developments in the market?

May 2023: Infineon Technologies AG launched the OptiMOS7 40V MOSFET family, its latest generation of power MOSFETs for automotive applications in various lead-free and robust power packages. The new family combines 300 mm thin-wafer technology with innovative packaging to deliver significant performance benefits in tiny packages. It makes the MOSFETs ideal for all standard and future automotive 40V MOSFET applications, such as electric power steering, braking systems, disconnect switches new zone architectures.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Power Semiconductor Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Power Semiconductor Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Power Semiconductor Market?

To stay informed about further developments, trends, and reports in the Power Semiconductor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence