Key Insights

The Canadian Artificial Organs and Bionics Market is set for significant expansion, projected to reach a market size of $32.9 billion by 2025, with a compound annual growth rate (CAGR) of 11.5% through 2033. This growth is driven by the rising incidence of chronic diseases and organ failure, an aging population, and continuous advancements in medical technology. Demand for artificial organs, such as hearts and kidneys, remains high due to transplant waitlists and increasing accessibility of innovative solutions. The bionics sector, particularly in vision, hearing, and orthopedics, is revolutionizing patient care by restoring function and enhancing quality of life. Favorable market conditions are further supported by government initiatives promoting healthcare innovation and rising Canadian disposable incomes.

Canada Artificial Organs and Bionics Market Market Size (In Billion)

Key growth drivers include the escalating prevalence of diabetes-related kidney failure, cardiovascular diseases necessitating artificial hearts, and an aging demographic experiencing hearing and vision impairments. Technological innovations, including miniaturization, enhanced biocompatibility, and AI integration in bionic devices, are accelerating market adoption. Potential restraints include the high cost of advanced bionic devices and artificial organs, alongside complexities in regulatory approvals and reimbursement policies. Nevertheless, ongoing research and development by leading companies, coupled with growing awareness and acceptance of these transformative technologies, are expected to overcome these challenges, ensuring sustained and dynamic market growth in Canada throughout the forecast period.

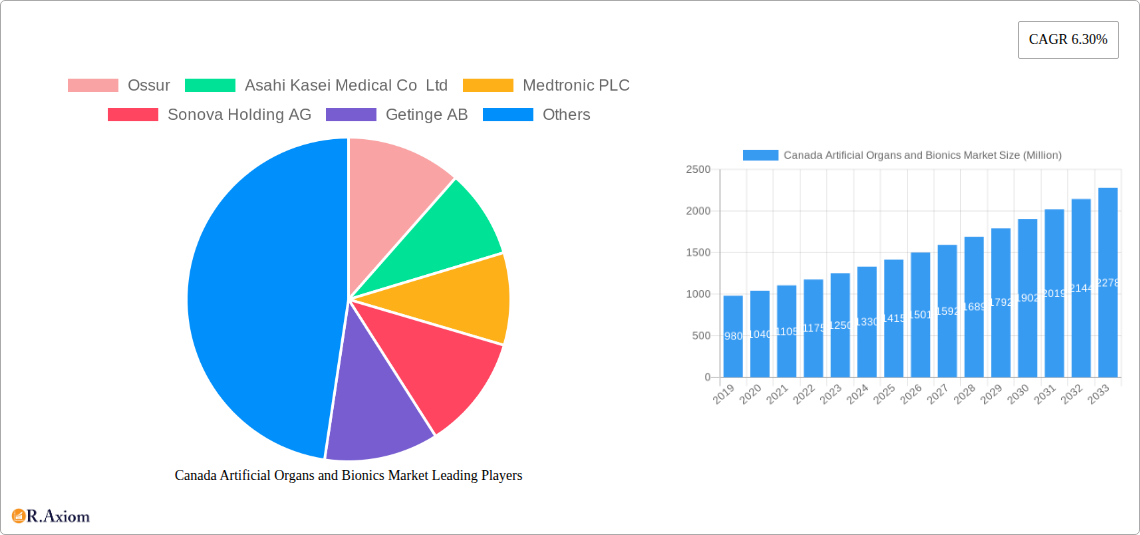

Canada Artificial Organs and Bionics Market Company Market Share

Canada Artificial Organs and Bionics Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a detailed examination of the Canada Artificial Organs and Bionics Market, offering critical insights into its current landscape, historical performance, and future trajectory. Spanning the study period of 2019–2033, with a base and estimated year of 2025, the report delves into market dynamics, segmentation, key players, and emerging trends. Leveraging high-traffic keywords such as "artificial organs Canada," "bionics market Canada," "medical devices Canada," "prosthetics Canada," "implants Canada," "healthcare innovation Canada," and "rehabilitation technology Canada," this report is designed to be an indispensable resource for industry stakeholders, investors, researchers, and policymakers.

Canada Artificial Organs and Bionics Market Market Concentration & Innovation

The Canadian artificial organs and bionics market exhibits a moderate to high level of concentration, driven by a few dominant players who are at the forefront of innovation and technological advancement. Companies like Medtronic PLC, Boston Scientific Corporation, and Asahi Kasei Medical Co Ltd hold significant market share through their extensive product portfolios and robust research and development capabilities. Innovation is a key differentiator, with a continuous focus on developing more biocompatible, efficient, and patient-friendly devices. This includes advancements in implantable devices, robotic prosthetics, and sophisticated sensory restoration technologies. The regulatory framework, overseen by Health Canada, plays a crucial role in ensuring product safety and efficacy, influencing the pace of market entry for new innovations. Product substitutes, such as traditional therapies and assistive devices, exist but are increasingly being surpassed by the superior functional outcomes offered by artificial organs and bionics. End-user trends are heavily influenced by an aging population, rising prevalence of chronic diseases, and a growing demand for improved quality of life and rehabilitation solutions. Mergers and acquisitions (M&A) activities are expected to continue as companies seek to expand their product lines, gain access to new technologies, and strengthen their market positions. For instance, strategic partnerships and acquisitions in the range of tens to hundreds of millions of dollars are anticipated to reshape the competitive landscape. The market share distribution among leading players is dynamic, with a constant push for technological breakthroughs to capture a larger segment.

Canada Artificial Organs and Bionics Market Industry Trends & Insights

The Canada Artificial Organs and Bionics Market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.8% over the forecast period of 2025–2033. This robust expansion is fueled by several interconnected industry trends and insights. A primary growth driver is the escalating prevalence of chronic diseases and organ failure, including cardiovascular diseases, kidney disease, and respiratory ailments, which directly increases the demand for artificial organs such as artificial hearts, kidneys, and lungs. Simultaneously, the rising incidence of sensory impairments and mobility challenges, attributed to an aging demographic and lifestyle factors, propels the adoption of bionic solutions like cochlear implants, vision bionics, and orthopedic bionics. Technological advancements represent another significant catalyst. Innovations in materials science, miniaturization, robotics, and artificial intelligence are leading to the development of more sophisticated, durable, and user-friendly bionic devices and artificial organs. These advancements are not only improving the functionality and longevity of existing solutions but also enabling the creation of entirely new therapeutic applications. For example, the integration of AI in bionic limbs allows for more intuitive control and adaptive movement, significantly enhancing user experience and independence. Consumer preferences are also evolving, with a growing emphasis on personalized medicine and minimally invasive procedures. Patients are increasingly seeking treatments that offer better quality of life, faster recovery times, and reduced long-term complications. This demand is pushing manufacturers to develop advanced implantable devices and regenerative medicine approaches. The competitive landscape is characterized by intense innovation and strategic collaborations among established medical device giants and agile startups. Companies are investing heavily in research and development to secure patents and establish a competitive edge in a rapidly evolving market. Market penetration for advanced bionic solutions is steadily increasing as awareness grows and reimbursement policies adapt to cover these sophisticated technologies. Furthermore, government initiatives and healthcare reforms aimed at improving access to advanced medical treatments and promoting patient outcomes are creating a favorable environment for market expansion. The integration of telemedicine and digital health platforms is also playing a role, facilitating remote patient monitoring and follow-up care for individuals using artificial organs and bionics, thereby improving overall patient management and system efficiency. The focus on evidence-based outcomes and cost-effectiveness continues to shape product development and market adoption strategies within Canada.

Dominant Markets & Segments in Canada Artificial Organs and Bionics Market

The Canadian artificial organs and bionics market is segmented into two primary categories: Artificial Organs and Bionics, each with sub-segments that demonstrate varying growth trajectories and market dominance.

Artificial Organs

- Artificial Heart: This segment holds a significant position due to the high prevalence of cardiovascular diseases in Canada. The increasing demand for advanced heart failure therapies, including ventricular assist devices (VADs) and total artificial hearts (TAHs), is a key driver. Economic policies supporting advanced cardiac care and hospital infrastructure equipped for complex surgeries contribute to its dominance.

- Artificial Kidneys: The rising rates of end-stage renal disease (ESRD) and the limitations of traditional dialysis treatments are fueling the growth of artificial kidneys, including wearable and implantable dialysis devices. Government investments in chronic kidney disease management and preventative healthcare programs bolster this segment.

- Artificial Lungs: While a more nascent segment, artificial lungs, particularly extracorporeal membrane oxygenation (ECMO) devices, are crucial for critical care. Advancements in ECMO technology for severe respiratory distress conditions, such as ARDS, are driving demand. Infrastructure for intensive care units and skilled medical professionals are essential drivers.

- Cochlear Implants: This segment is a leader within the bionics category, driven by the growing awareness and diagnosis of hearing loss, especially among the aging population and children with congenital hearing impairments. Favorable reimbursement policies from provincial healthcare plans and strong advocacy groups contribute to its dominance.

- Other Organ Types: This encompasses a range of emerging artificial organs like artificial livers and pancreases. While currently smaller in market share, ongoing research and development, coupled with a growing understanding of organ failure complexities, indicate significant future potential.

Bionics

- Vision Bionics: This segment, primarily encompassing retinal implants and advanced prosthetic eyes, is gaining traction due to technological breakthroughs in restoring partial sight. The increasing incidence of age-related macular degeneration and diabetic retinopathy supports its growth.

- Ear Bionics: Beyond cochlear implants, this segment includes advanced hearing aids and other auditory assistive devices that utilize sophisticated digital signal processing. The broad applicability across various age groups and types of hearing loss makes it a substantial market.

- Orthopedic Bionic: This is a dominant segment within bionics, featuring advanced prosthetic limbs, exoskeletons, and bionic braces. The rising number of amputations due to trauma, diabetes, and vascular diseases, coupled with the demand for enhanced mobility and rehabilitation, fuels this segment. The integration of AI and robotics in prosthetics significantly boosts its market appeal.

- Cardiac Bionics: This segment largely overlaps with artificial hearts but also includes implantable cardioverter-defibrillators (ICDs) and pacemakers that incorporate bionic functionalities for more precise cardiac rhythm management. The widespread adoption of these devices for managing arrhythmias and preventing sudden cardiac death solidifies its importance.

The dominance of specific segments is influenced by the availability of advanced healthcare infrastructure, physician expertise, patient awareness, and the comprehensiveness of provincial healthcare coverage for these medical technologies.

Canada Artificial Organs and Bionics Market Product Developments

Product development in the Canadian artificial organs and bionics market is characterized by a relentless pursuit of enhanced functionality, improved biocompatibility, and greater patient comfort. Innovations are increasingly focusing on intelligent devices that adapt to user needs and integrate seamlessly with the human body. For instance, next-generation bionic limbs are incorporating advanced sensory feedback mechanisms, allowing users to feel touch and pressure, thereby revolutionizing prosthetics. In the realm of artificial organs, advancements in materials science are leading to more durable and less immunogenic implants, extending device lifespan and reducing the risk of complications. The miniaturization of components is also a key trend, enabling less invasive implantation procedures and improving aesthetic outcomes. Competitive advantages are being carved out through superior battery life, wireless connectivity for remote monitoring and adjustments, and personalized fitting solutions. These product developments are not only addressing unmet clinical needs but also expanding the addressable market for these transformative technologies.

Report Scope & Segmentation Analysis

This report provides a granular analysis of the Canada Artificial Organs and Bionics Market segmented by Type. The Artificial Organs segment encompasses Artificial Hearts, Artificial Kidneys, Artificial Lungs, Cochlear Implants, and Other Organ Types. The Bionics segment includes Vision Bionics, Ear Bionics, Orthopedic Bionic, and Cardiac Bionics. For each segment, market sizes, growth projections, and competitive dynamics have been analyzed for the historical period (2019–2024) and the forecast period (2025–2033). For example, the Cochlear Implants segment is projected to witness a CAGR of approximately 8.5%, driven by increasing diagnoses of hearing loss and supportive government initiatives, with an estimated market size of over $200 Million by 2028. Conversely, advancements in Artificial Lungs technology, while crucial for critical care, may show a more moderate but steady growth in market size as the technology matures and becomes more accessible.

Key Drivers of Canada Artificial Organs and Bionics Market Growth

The growth of the Canada Artificial Organs and Bionics Market is propelled by a confluence of critical factors.

- Rising Prevalence of Chronic Diseases: An aging population and lifestyle-related health issues contribute to an increased incidence of organ failure and chronic conditions requiring advanced medical interventions.

- Technological Advancements: Continuous innovation in areas like AI, robotics, biomaterials, and miniaturization is leading to the development of more effective, durable, and patient-friendly artificial organs and bionic devices.

- Growing Demand for Enhanced Quality of Life: Patients and their families are increasingly seeking solutions that restore function, improve mobility, and enhance overall well-being and independence.

- Supportive Healthcare Policies and Reimbursement: Government initiatives and evolving provincial healthcare coverage are making these advanced medical technologies more accessible and affordable.

- Increased Awareness and Diagnosis: Greater public and medical awareness of the benefits of artificial organs and bionics, coupled with improved diagnostic capabilities, leads to higher adoption rates.

Challenges in the Canada Artificial Organs and Bionics Market Sector

Despite the promising growth, the Canada Artificial Organs and Bionics Market faces several significant challenges.

- High Cost of Devices and Procedures: The advanced nature of these technologies often translates to substantial upfront costs, posing a barrier to widespread adoption, especially for individuals without comprehensive insurance coverage.

- Complex Regulatory Approval Pathways: While essential for patient safety, the rigorous and lengthy approval processes by Health Canada can sometimes slow down the market entry of innovative products.

- Limited Reimbursement Policies: Inconsistent or insufficient reimbursement policies across different provinces for certain advanced bionic and artificial organ technologies can hinder patient access.

- Need for Specialized Training and Infrastructure: The implantation and management of many artificial organs and bionic devices require highly skilled medical professionals and specialized healthcare facilities, which may not be universally available.

- Long-Term Performance and Maintenance Concerns: Ensuring the long-term efficacy, durability, and biocompatibility of implanted devices, along with addressing potential maintenance and upgrade needs, remains a critical consideration for both patients and healthcare providers.

Emerging Opportunities in Canada Artificial Organs and Bionics Market

The Canada Artificial Organs and Bionics Market is ripe with emerging opportunities. The development of more sophisticated and user-friendly regenerative medicine techniques presents a long-term opportunity to potentially reduce the reliance on mechanical implants. The increasing integration of artificial intelligence (AI) and machine learning (ML) in bionic devices is enabling predictive maintenance, personalized therapy adjustments, and more intuitive user control. Furthermore, the expansion of tele-rehabilitation services enabled by digital health platforms offers new avenues for remote patient monitoring and therapy, particularly beneficial for individuals in remote areas. There is also a growing opportunity in the development of pediatric bionic solutions to address congenital conditions and support the growth and development of children. Finally, increased partnerships between academic institutions, research centers, and industry players are fostering a collaborative environment for innovation and accelerating the translation of groundbreaking research into clinical applications.

Leading Players in the Canada Artificial Organs and Bionics Market Market

- Ossur

- Asahi Kasei Medical Co Ltd

- Medtronic PLC

- Sonova Holding AG

- Getinge AB

- Ekso Bionics Holdings Inc

- Boston Scientific Corporation

- Baxter International Inc

- Berlin Heart GmbH

- Med-El Elektromedizinische Gerate GmbH

Key Developments in Canada Artificial Organs and Bionics Market Industry

- September 2022: Axonics completed the first implant of its Axonics F15 sacral neuromodulation (SNM) system for patients in Canada suffering from bladder and bowel dysfunction. The SNM is the only approved implantable bionic solution globally for urinary or bowel incontinence, marking a significant advancement in neuromodulation therapies.

- August 2022: GN Hearing launched new ReSound OMNIA hearing aids globally, starting with the United States and Canada, along with the equivalent Beltone Achieve line-up, in the popular Receiver-in-Ear (RIE) style, enhancing auditory restoration options.

Strategic Outlook for Canada Artificial Organs and Bionics Market Market

The strategic outlook for the Canada Artificial Organs and Bionics Market is exceptionally bright, driven by a persistent demand for improved healthcare outcomes and a commitment to technological innovation. Future growth catalysts will likely include further advancements in personalized bionic solutions tailored to individual patient anatomy and needs, alongside the development of more efficient and less invasive artificial organ technologies. The increasing integration of digital health platforms for remote monitoring and patient engagement will also play a pivotal role, enhancing patient care pathways and operational efficiencies. Strategic collaborations between medical device manufacturers, research institutions, and healthcare providers are expected to accelerate the development and adoption of next-generation technologies. As healthcare systems continue to prioritize quality of life and functional restoration for patients, the market for artificial organs and bionics is well-positioned for sustained expansion and transformative impact on Canadian healthcare.

Canada Artificial Organs and Bionics Market Segmentation

-

1. Type

-

1.1. Artificial Organ

- 1.1.1. Artificial Heart

- 1.1.2. Artificial Kidneys

- 1.1.3. Artificial Lungs

- 1.1.4. Cochlear Implants

- 1.1.5. Other Organ Types

-

1.2. Bionics

- 1.2.1. Vision Bionics

- 1.2.2. Ear Bionics

- 1.2.3. Orthopedic Bionic

- 1.2.4. Cardiac Bionics

-

1.1. Artificial Organ

Canada Artificial Organs and Bionics Market Segmentation By Geography

- 1. Canada

Canada Artificial Organs and Bionics Market Regional Market Share

Geographic Coverage of Canada Artificial Organs and Bionics Market

Canada Artificial Organs and Bionics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Incidences of Organ Failure; Scarcity of Donor Organs

- 3.3. Market Restrains

- 3.3.1. High Cost of Procedure; Risk of Compatibility and Malfunctions

- 3.4. Market Trends

- 3.4.1. Artificial Kidney Segment is Expected to Witness Significant Growth During the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Artificial Organs and Bionics Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Artificial Organ

- 5.1.1.1. Artificial Heart

- 5.1.1.2. Artificial Kidneys

- 5.1.1.3. Artificial Lungs

- 5.1.1.4. Cochlear Implants

- 5.1.1.5. Other Organ Types

- 5.1.2. Bionics

- 5.1.2.1. Vision Bionics

- 5.1.2.2. Ear Bionics

- 5.1.2.3. Orthopedic Bionic

- 5.1.2.4. Cardiac Bionics

- 5.1.1. Artificial Organ

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Ossur

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Asahi Kasei Medical Co Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Medtronic PLC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Sonova Holding AG

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Getinge AB

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Ekso Bionics Holdings Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Boston Scientific Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Baxter International Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Berlin Heart GmbH

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Med-El Elektromedizinische Gerate GmbH

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Ossur

List of Figures

- Figure 1: Canada Artificial Organs and Bionics Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Artificial Organs and Bionics Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Artificial Organs and Bionics Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Canada Artificial Organs and Bionics Market Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Canada Artificial Organs and Bionics Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Canada Artificial Organs and Bionics Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 5: Canada Artificial Organs and Bionics Market Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Canada Artificial Organs and Bionics Market Volume K Unit Forecast, by Type 2020 & 2033

- Table 7: Canada Artificial Organs and Bionics Market Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Canada Artificial Organs and Bionics Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Artificial Organs and Bionics Market?

The projected CAGR is approximately 11.5%.

2. Which companies are prominent players in the Canada Artificial Organs and Bionics Market?

Key companies in the market include Ossur, Asahi Kasei Medical Co Ltd, Medtronic PLC, Sonova Holding AG, Getinge AB, Ekso Bionics Holdings Inc, Boston Scientific Corporation, Baxter International Inc, Berlin Heart GmbH, Med-El Elektromedizinische Gerate GmbH.

3. What are the main segments of the Canada Artificial Organs and Bionics Market?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Incidences of Organ Failure; Scarcity of Donor Organs.

6. What are the notable trends driving market growth?

Artificial Kidney Segment is Expected to Witness Significant Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Procedure; Risk of Compatibility and Malfunctions.

8. Can you provide examples of recent developments in the market?

In September 2022, Axonics completed the first implant of its Axonics F15 sacral neuromodulation (SNM) system for patients in Canada suffering from bladder and bowel dysfunction. The SNS is the only approved implantable bionic solution globally for urinary or bowel incontinence.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Artificial Organs and Bionics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Artificial Organs and Bionics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Artificial Organs and Bionics Market?

To stay informed about further developments, trends, and reports in the Canada Artificial Organs and Bionics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence